CHAPTER 6

SOLUTIONS TO EXERCISES—SET B

EXERCISE 6-1B

Ending inventory⎯physical count ………………………………………… $375,000

2. No effect−title does not transfer to Fallen until

goods are received ………………………………………………….. 0

4. Add to inventory: Title remains with Fallen until

purchaser receives goods ……………………………………….. 41,000

5. The goods did not arrive prior to year-end. The goods,

EXERCISE 6-2B

Ending inventory-as reported ………………………………………………..

$740,000

1.

holding them as a consignee. ……………………………………………

Subtract from inventory: The goods belong

2.

40,000

Add to inventory: The goods belong to

3.

Subtract from inventory: Office supplies should

4.

Add to inventory: The goods belong to Doobie

until they are shipped (Jan. 1). ………………………………………….

29,000

5.

indicates that Doobie knows this over-shipment is

an attempt to improve Doobie’s reported income by

Add to inventory: Siebring Sales ordered goods with

a cost of $6,000. Doobie should record the

corresponding sales revenue of $10,000.

Doobie’s decision to ship extra “unordered”

6.

Correct inventory …………………………………………………………………

Subtract from inventory: GAAP requires that

EXERCISE 6-3B

(a) Do not include—Nyguen does not own items held on consignment.

(b) Include in inventory—Nyguen still owns the items as they were only

shipped on consignment.

EXERCISE 6-4B

(a) FIFO

Beginning inventory (20 X $100) ……………………………. $ 2,000

Purchases

Sept. 12 (45 X $103) ………………………………………… $4,635

PROOF

Date Units Unit Cost Total Cost

9/1 20 $100 $ 2,000

9/12 45 103 4,635

PROOF

Date Units Unit Cost Total Cost

9/26 50 $105 $ 5,250

9/19 20 104 2,080

(b)

Cost of

goods

EXERCISE 6-5B

(a) FIFO

Beginning inventory (21 X $9) …………………………………… $189

Purchases

May 15 (25 X $10) ……………………………………………….. $250

PROOF

Date Units Unit Cost Total Cost

5/1 21 $ 9 $189

(b) AVERAGE-COST

$857 ÷ 84 = $10.202 weighted-average unit cost

PROOF

Units Unit Cost Total Cost

EXERCISE 6-5B (Continued)

(c) LIFO

Cost of goods available for sale ………………………………………….. $857

PROOF

Date Units Unit Cost Total Cost

5/24 38 $11 $418

EXERCISE 6-6B

(a) FIFO Cost of Goods Sold

(b) It could choose to sell specific units purchased at specific costs if it

wished to impact earnings selectively. If it wished to minimize earnings

(c) The FIFO method provides a more appropriate balance sheet valuation

EXERCISE 6-7B

(a) (1) FIFO

Beginning inventory (120 X $5) ……………………………. $ 600

Purchases

June 12 (370 X $6) ………………………………………… $2,220

(2) LIFO

Cost of goods available for sale ………………………….. $6,320

(3) AVERAGE-COST

Cost of Goods Total Units Weighted-Average

(b) The FIFO method will produce the highest ending inventory because costs

have been rising. Under this method, the earliest costs are assigned to

(c) The average-cost ending inventory ($1,021.44) is higher than LIFO

EXERCISE 6-8B

LIFO FIFO

(a) Sales ……………………………………………………….…… $96,000 $96,000

Cost of goods sold ……………………………………….. 38,000 29,000

LIFO FIFO

(b) Sales ……………………………………………………….…… $96,000 $96,000

Less: Cash paid for inventory purchases ……… 32,000 32,000

LIFO FIFO

(c) Net cash provided by operating activities ……… $37,700 $35,000

EXERCISE 6-9B

Cost/Unit

Market

Value/Unit

Lower-of-Cost-

or-Market

Units

Inventory at

Lower-of-Cost-

or-Market

Cameras:

Minolta

$160

$156

$156

5

$ 780

Canon

7

Light Meters:

Vivitar

Kodak

Total

EXERCISE 6-10B

2013

2014

Inventory

turnover

$15,762

($1,693 +$1,926) ÷ 2

$18,038

($1,926 +$2,290) ÷ 2

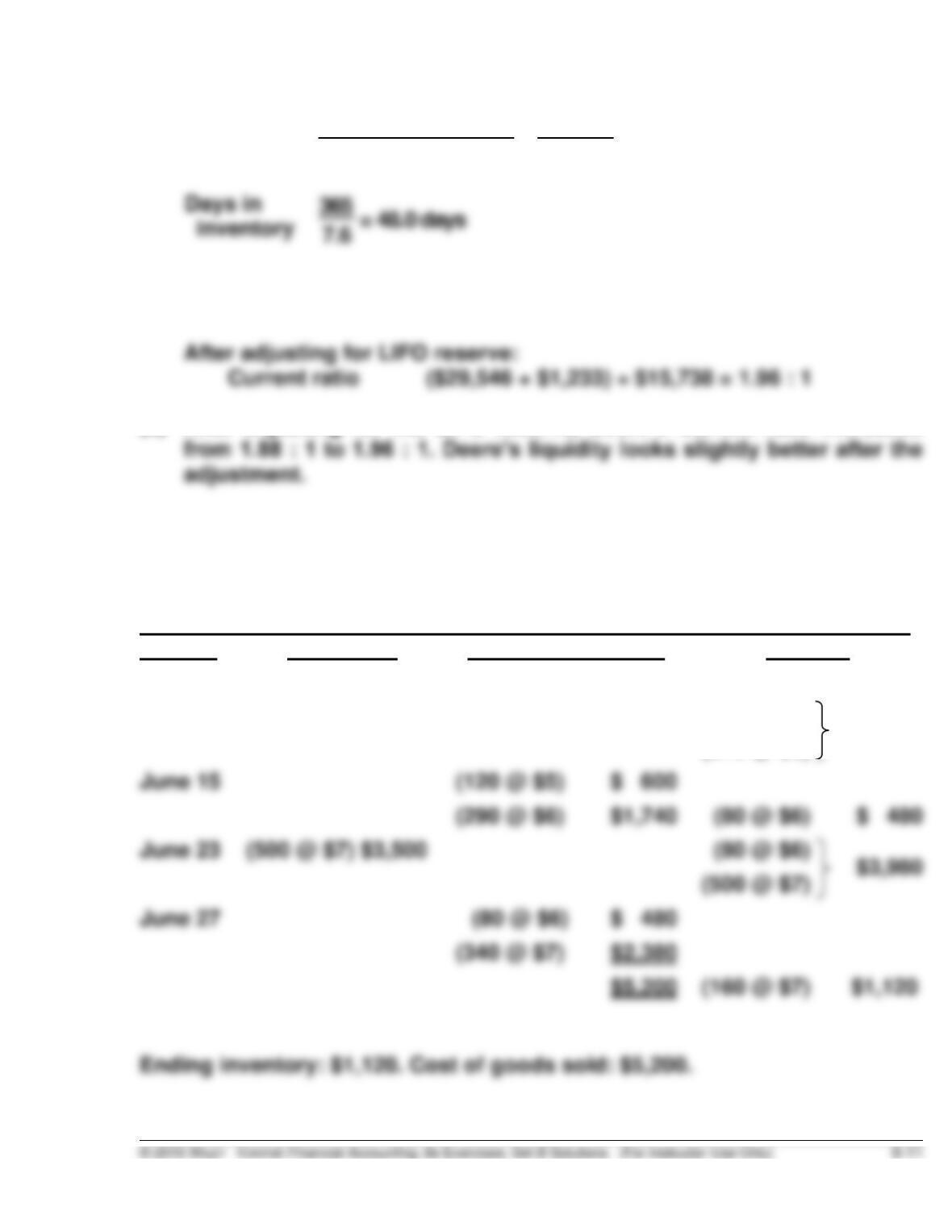

Days in

inventory

365

8.7 =42.0 days

365

8.6 =42.4 days

EXERCISE 6-11B

(a)

Inventory

turnover

$16,253

($1,957+ $2,337) ÷ 2 =$16,253

$2,147 = 7.6

(b) Based on data presented:

Current ratio $29,546 ÷ $15,738 = 1.88 : 1

(c) After adjusting for the LIFO reserve, Deere’s current ratio increases

*EXERCISE 6-12B

(a)

FIFO

Date

Purchases

Cost of goods sold

Balance

June 1

(120 @ $5)

$ 600

June 12

(370 @ $6) $2,220

(120 @ $5)

$2,820

(370 @ $6)

June 15

(120 @ $5)

$ 600

(290 @ $6)

$1,740

June 23

(500 @ $7) $3,500

(500 @ $7)

June 27

$ 480

*EXERCISE 6-12B (Continued)

LIFO

Date

Purchases

Cost of Goods Sold

Balance

June 1

(120 @ $5)

$ 600

June 12

(370 @ $6) $2,220

(120 @ $5)

June 15

(370 @ $6)

$ 400

June 23

(500 @ $7) $3,500

(500 @ $7)

June 27

Ending inventory: $960. Cost of goods sold: $5,360.

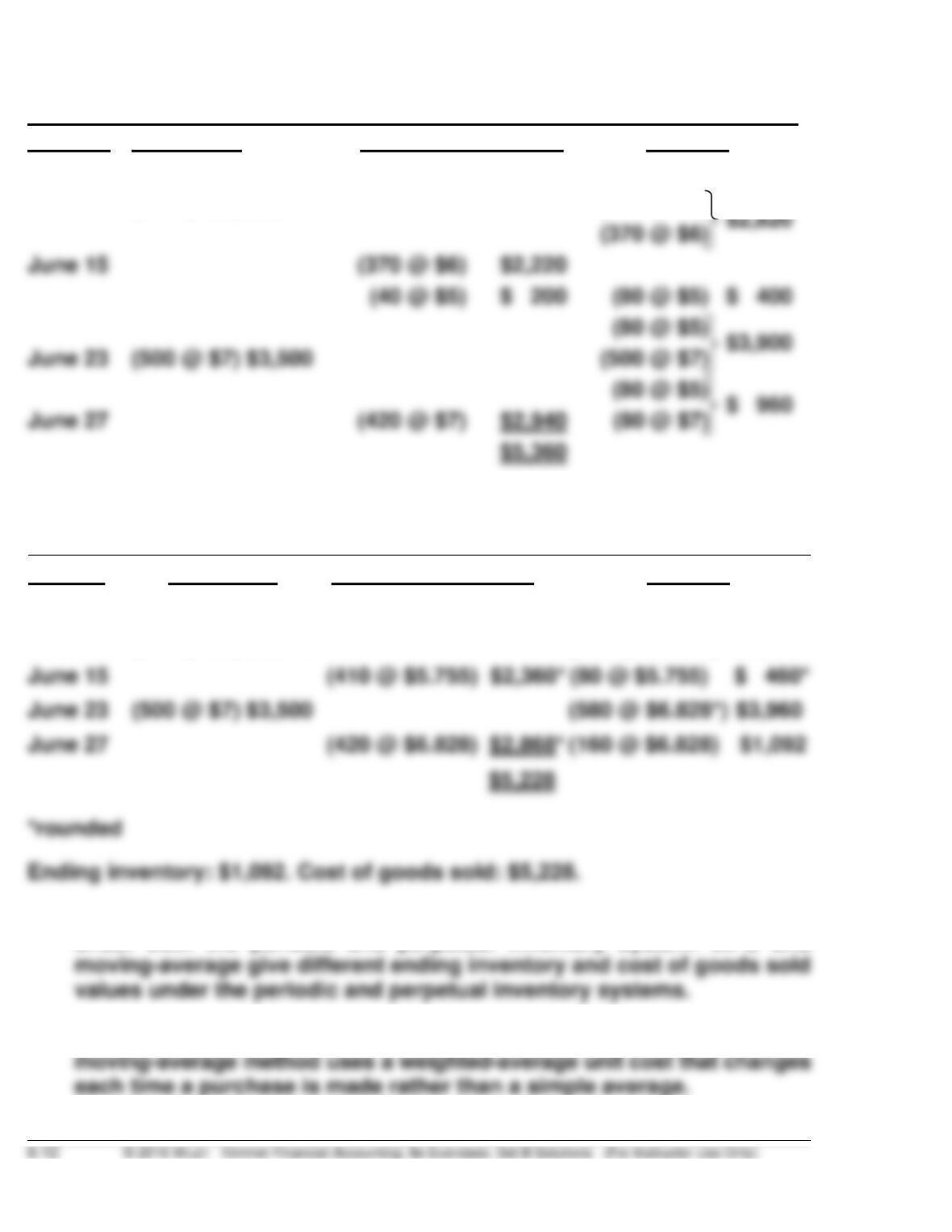

MOVING-AVERAGE

Date

Purchases

Cost of Goods Sold

Balance

June 1

(120 @ $5)

$ 600

June 12

(370 @ $6) $2,220

(490 @ $5.755)

$2,820

June 15

(80 @ $5.755)

$ 460*

June 23

(500 @ $7) $3,500

(580 @ $6.828*)

(b) FIFO gives the same ending inventory and cost of goods sold values

under both the periodic and perpetual inventory system. LIFO and

(c) The simple average would be [($5 + $6 + $7) ÷ 3] or $6. However, the

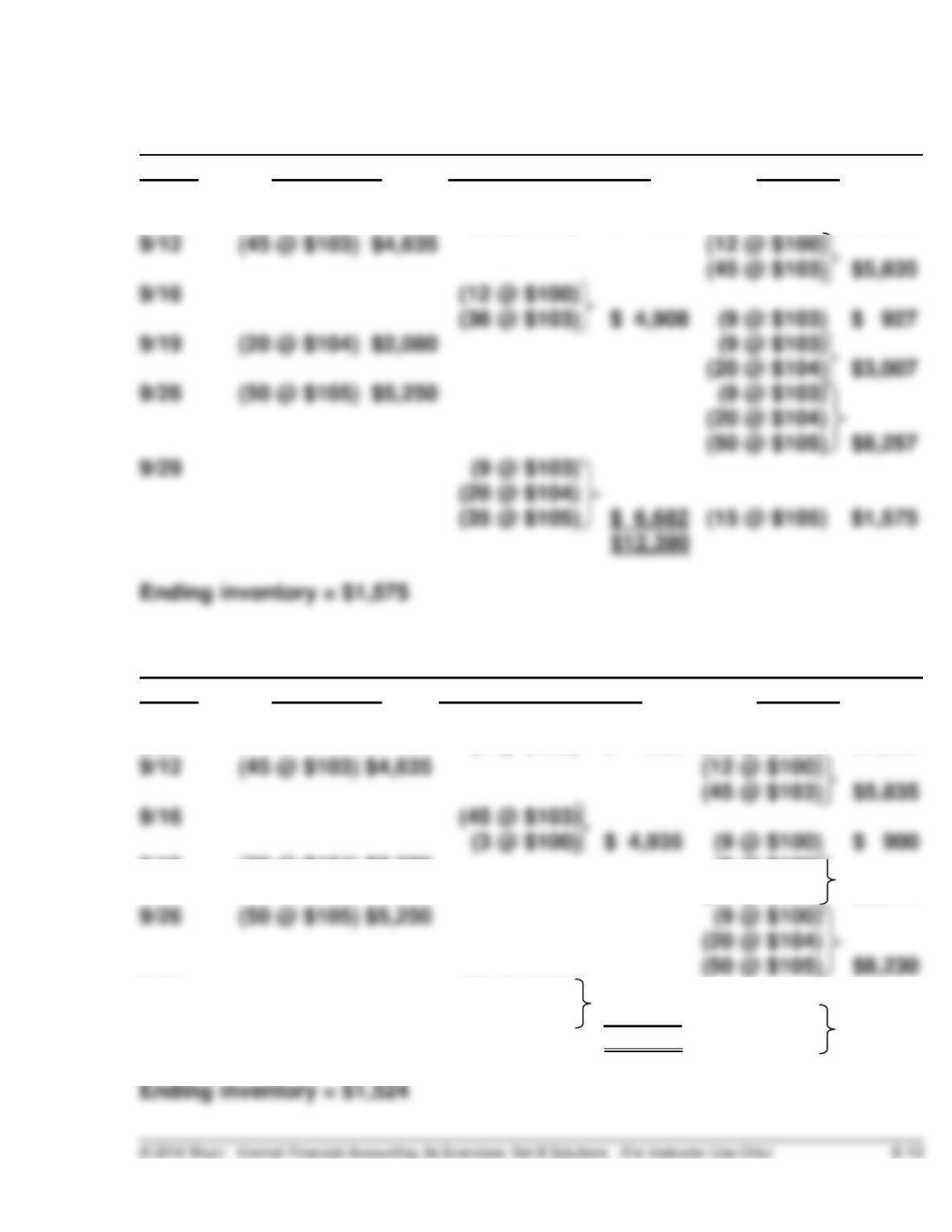

*EXERCISE 6-13B

(a)

FIFO

Date Purchases Cost of Goods Sold Balance

9/1 (20 @ $100) $2,000

9/5 (8 @ $100) $ 800 (12 @ $100) $1,200

LIFO

Date Purchases Cost of Goods Sold Balance

9/1 (20 @ $100) $2,000

9/5 (8 @ $100) $ 800 (12 @ $100) $1,200

9/19 (20 @ $104) $2,080 (9 @ $100)

(20 @ $104) $2,980

9/29 (50 @ $105)

(14 @ $104) $ 6,706 (9 @ $100)

$12,441 (6 @ $104) $1,524

*EXERCISE 6-13B (Continued)

MOVING-AVERAGE

Date Purchases Cost of Goods Sold Balance

9/1 (20 @ $100) $2,000

9/5 (8 @ $100) $ 800 (12 @ $100) $1,200

9/12 (45 @ $103) $4,635 (57 @ $102.368)a $5,835

*Rounded

a($1,200 + $4,635) ÷ 57 = $102.368

*EXERCISE 6-14B

2013 2014

Beginning inventory …………………………………………… $ 20,000 $ 26,000

Cost of goods purchased ……………………………………. 164,000 175,000

*EXERCISE 6-15B

(a)

2013 2014

Sales revenue ………………………………………………. $210,000 $250,000

Cost of goods sold

Beginning inventory ………………………………. 32,000 32,000

(b) The cumulative effect on total gross profit for the two years is zero as

shown below:

(c) Dear Mr./Ms. President:

Because your ending inventory of December 31, 2013 was overstated

by $8,000, your net income for 2013 was overstated and net income for

2014 was understated by $8,000.

In a periodic system, the cost of goods sold is calculated by deducting

the cost of ending inventory from the total cost of goods you have

available for sale in the period. Therefore, if this ending inventory

figure is overstated, as it was in December 2013, the cost of goods