CHAPTER 6 Accounting for Merchandising Businesses

Comp. Prob. 2 (Continued)

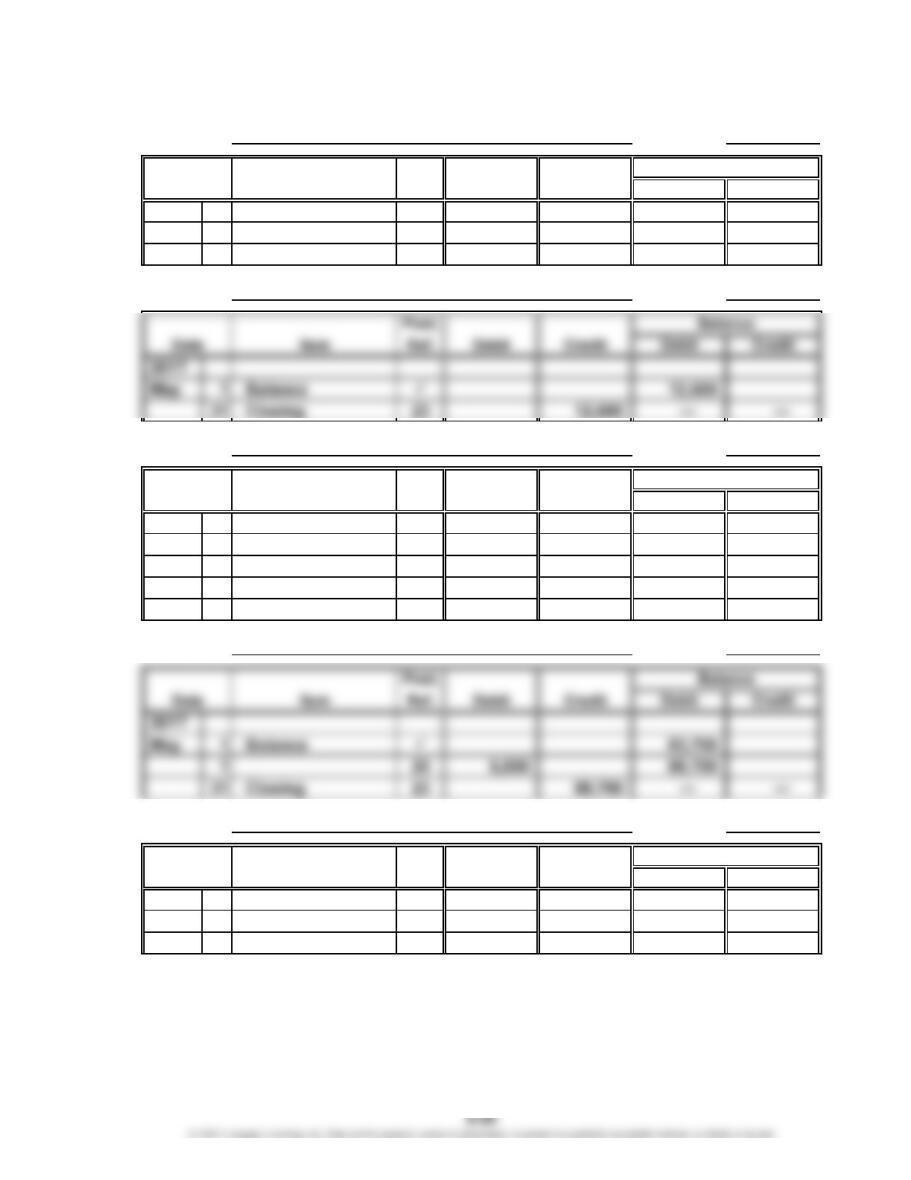

Account No. 523

Post.

Item Ref. Debit Credit Debit Credit

20Y7

May 31 Adjusting 22 9,800 9,800

31 Closing 23 9,800 — —

Account No. 529

Account No. 530

Post.

Item Ref. Debit Credit Debit Credit

20Y7

May 1 Balance 382,100

28 21 29,000 411,100

31 Adjusting 22 6,600 417,700

31 Closing 23 417,700 — —

Account No. 531

Account No. 532

Post.

Item Ref. Debit Credit Debit Credit

20Y7

May 31 Adjusting 22 12,000 12,000

31 Closing 23 12,000 — —

Balance

Date

Account: Rent Expense

Account: Insurance Expense

Account: Store Supplies Expense

Balance

Date

Account: Miscellaneous Selling Expense

Account: Office Salaries Expense

Balance

Date

CHAPTER 6 Accounting for Merchandising Businesses

Comp. Prob. 2 (Continued)

Account No. 539

Account: Miscellaneous Administrative Expense

CHAPTER 6 Accounting for Merchandising Businesses

Comp. Prob. 2 (Continued)

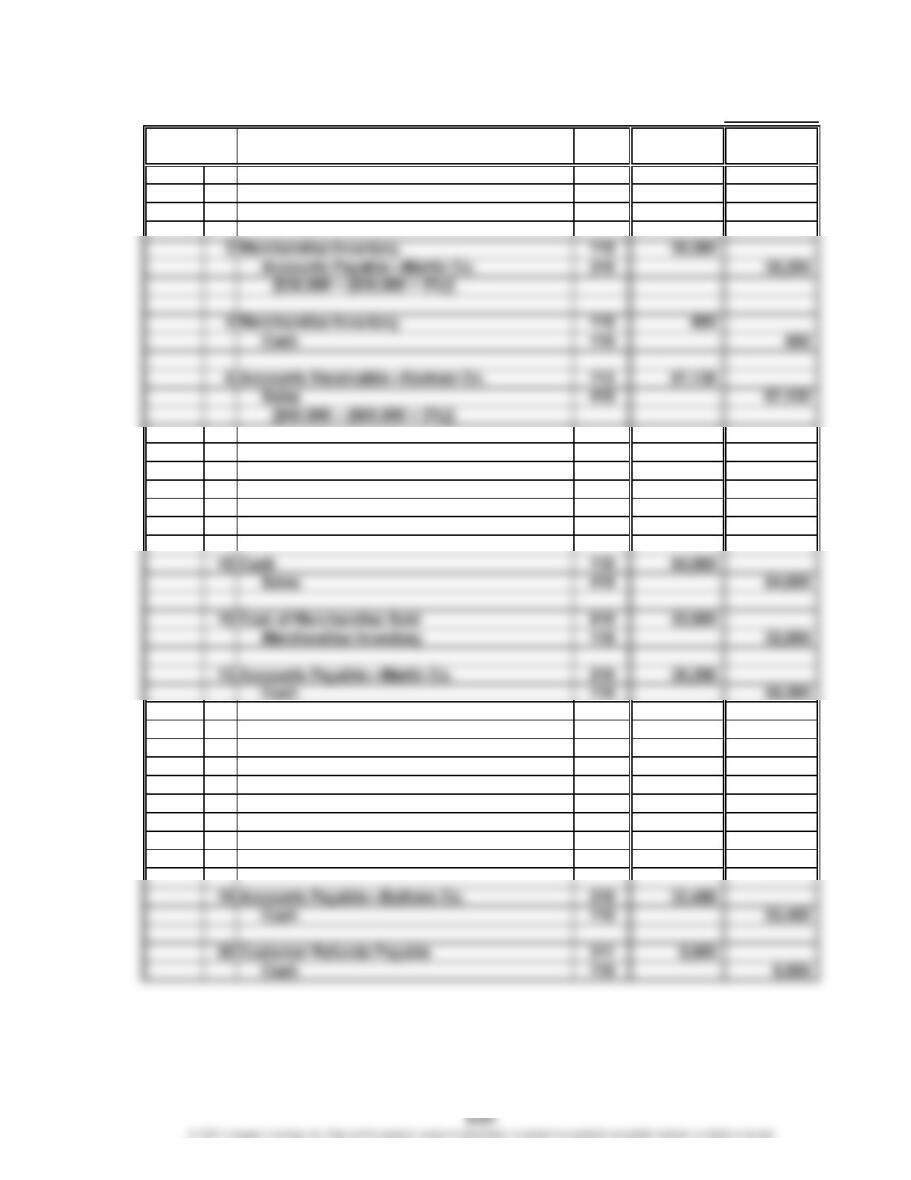

1. and 2. Page 20

Post.

Ref. Debit Credit

20Y7

May 1 Rent Expense 531 5,000

Cash 110 5,000

6 Cost of Merchandise Sold 510 41,000

Merchandise Inventory 115 41,000

7 Cash 110 22,300

Accounts Receivable—Halstad Co. 112 22,300

15 Advertising Expense 521 11,000

Cash 110 11,000

16 Cash 110 67,130

Accounts Receivable—Korman Co. 112 67,130

19 Merchandise Inventory 115 18,700

Cash 110 18,700

Date

JOURNAL

CHAPTER 6 Accounting for Merchandising Businesses

Comp. Prob. 2 (Continued)

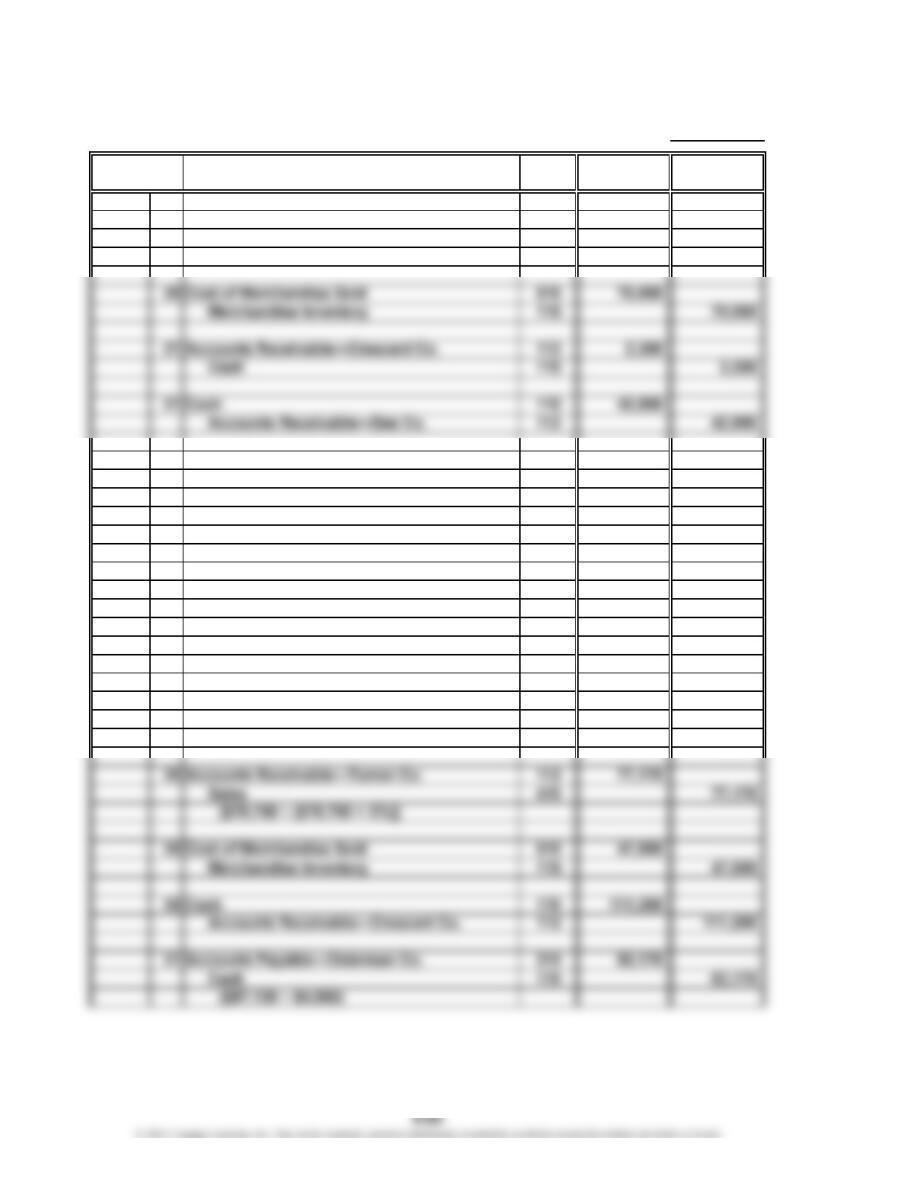

Page 21

Post.

Ref. Debit Credit

20Y7

May 20 Accounts Receivable—Crescent Co. 112 108,900

Sales 410 108,900

[$110,000 – ($110,000 × 1%)]

21 Merchandise Inventory 115 87,120

Accounts Payable—Osterman Co. 210 87,120

[$88,000 – ($88,000 × 1%)]

24 Accounts Payable—Osterman Co. 210 4,950

Merchandise Inventory 115 4,950

26 Customer Refunds Payable 211 800

Cash 110 800

28 Sales Salaries Expense 520 56,000

Office Salaries Expense 530 29,000

Cash 110 85,000

29 Store Supplies 118 2,400

Cash 110 2,400

3.

Account Debit Credit

No. Balances Balances

Cash 110 99,430

Accounts Receivable 112 245,875

Merchandise Inventory 115 599,150

Accounts Payable 210 63,150

Customer Refunds Payable 211 44,200

Salaries Payable 212 —

Lynn Tolley, Capital 310 685,300

Lynn Tolley, Drawing 311 135,000

Sales 410 5,376,205

Cost of Merchandise Sold 510 3,013,000

Sales Salaries Expense 520 720,800

May 31, 20Y7

Palisade Creek Co.

Unadjusted Trial Balance

CHAPTER 6 Accounting for Merchandising Businesses

Comp. Prob. 2 (Continued)

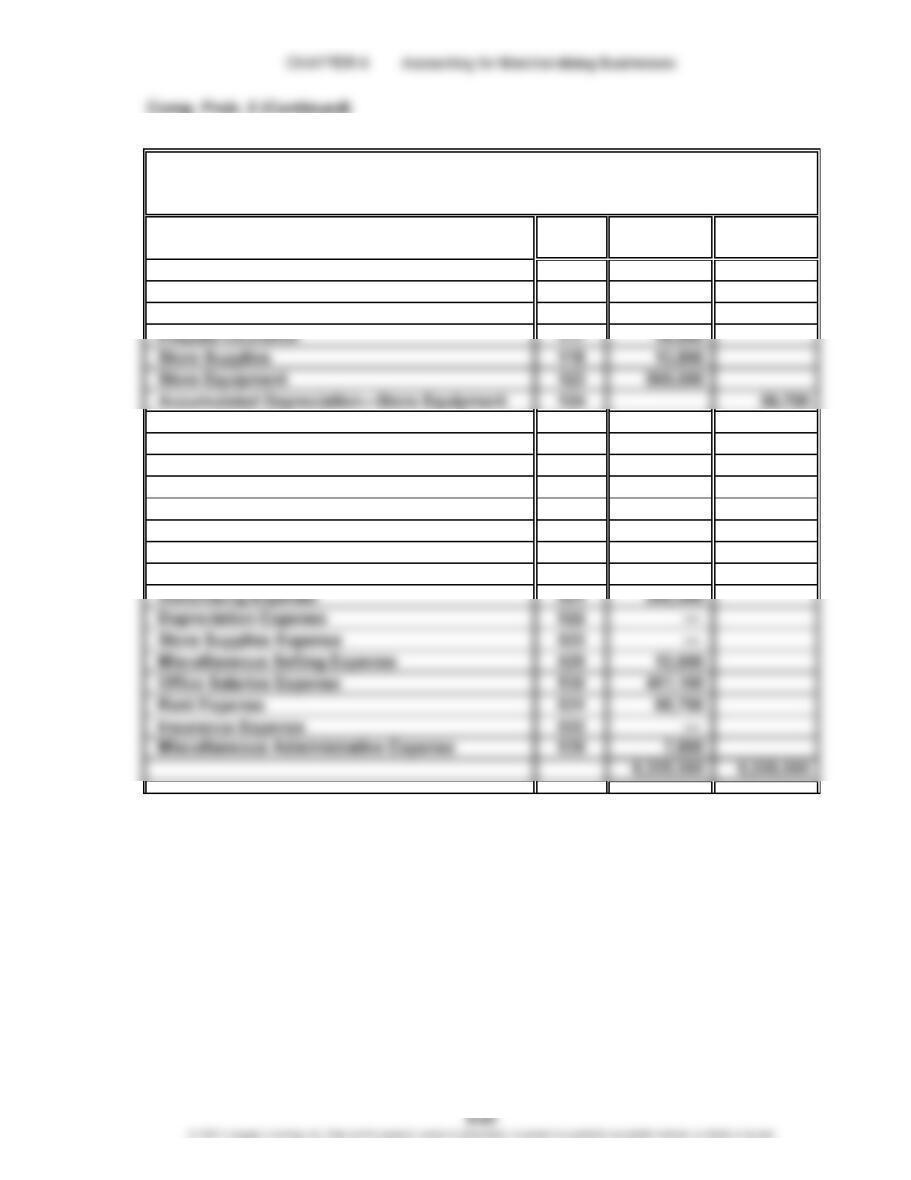

4. and 6. Page 22

Post.

Ref. Debit Credit

20Y7

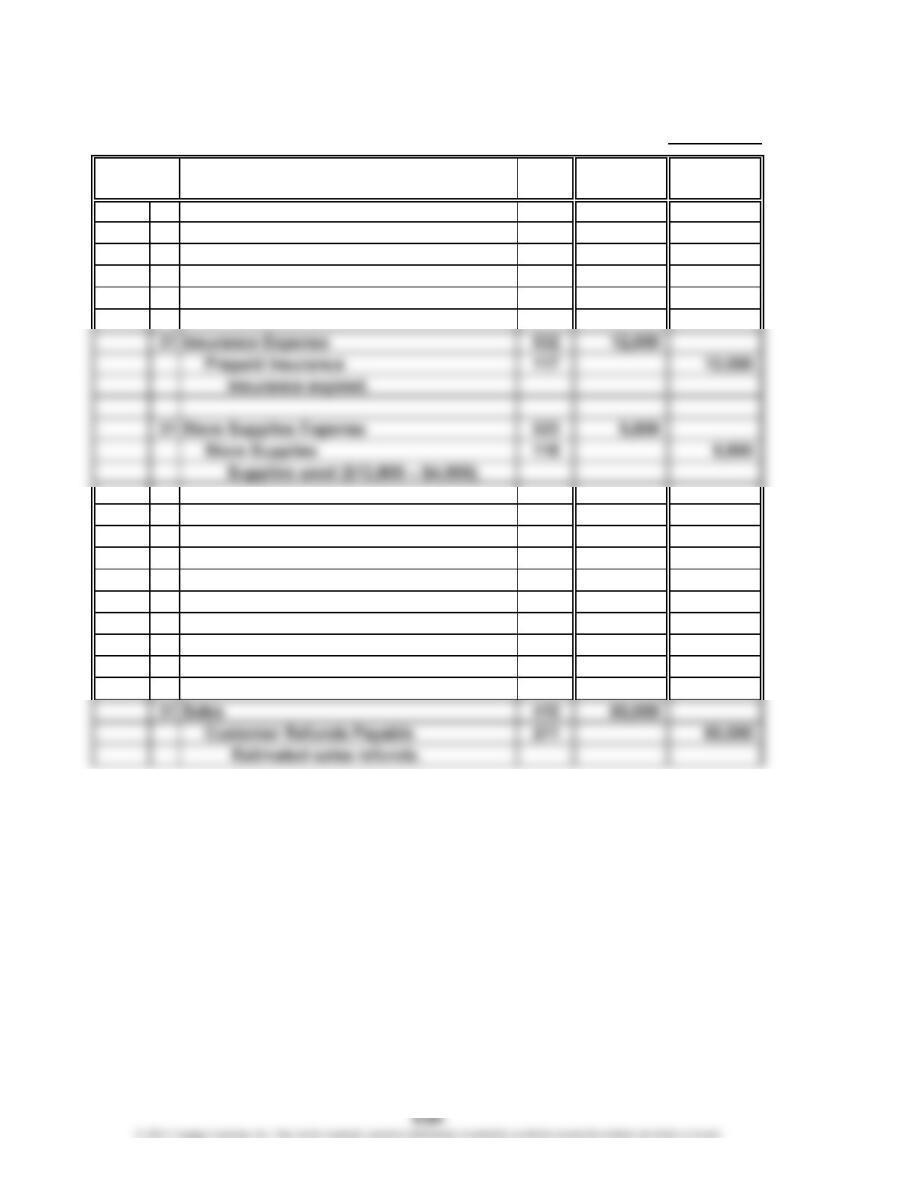

May 31 Cost of Merchandise Sold 510 13,950

Merchandise Inventory 115 13,950

Inventory shrinkage

($599,150 – $585,200).

31 Depreciation Expense 522 14,000

Accum. Depr.—Store Equipment 124 14,000

Store equipment depreciation.

31 Sales Salaries Expense 520 7,000

Office Salaries Expense 530 6,600

Salaries Payable 212 13,600

Accrued salaries.

Date

JOURNAL

Adjusting Entries

CHAPTER 6 Accounting for Merchandising Businesses

Comp. Prob. 2 (Continued)

7.

Account Debit Credit

No. Balances Balances

Cash 110 99,430

Accounts Receivable 112 245,875

Merchandise Inventory 115 585,200

Accounts Payable 210 63,150

Customer Refunds Payable 211 104,200

Salaries Payable 212 13,600

Lynn Tolley, Capital 310 685,300

Lynn Tolley, Drawing 311 135,000

Sales 410 5,316,205

Cost of Merchandise Sold 510 3,026,950

Sales Salaries Expense 520 727,800

Advertising Expense 521 292,000

Depreciation Expense 522 14,000

May 31, 20Y7

Palisade Creek Co.

Adjusted Trial Balance

CHAPTER 6 Accounting for Merchandising Businesses

Comp. Prob. 2 (Continued)

8.

Sales $5,316,205

Cost of merchandise sold 3,026,950

Gross profit $2,289,255

Expenses:

Total selling expenses $1,056,200

Administrative expenses:

Office salaries expense $417,700

Rent expense 88,700

Lynn Tolley, capital, June 1, 20Y6 $ 685,300

Net income for the year $ 706,855

Palisade Creek Co.

Statement of Owner’s Equity

For the Year Ended May 31, 20Y7

Palisade Creek Co.

Income Statement

For the Year Ended May 31, 20Y7

CHAPTER 6 Accounting for Merchandising Businesses

Comp. Prob. 2 (Continued)

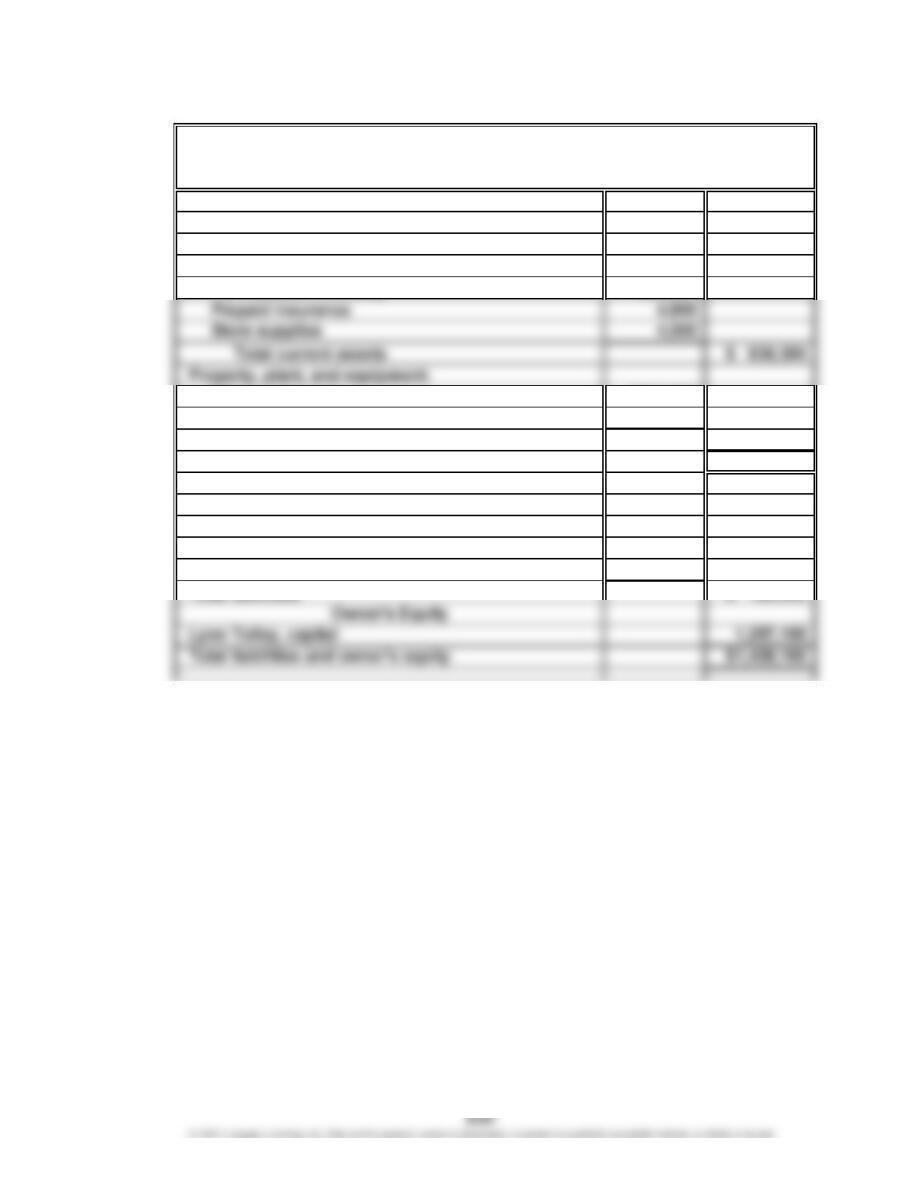

Current assets:

Cash $ 99,430

Accounts receivable 245,875

Merchandise inventory 585,200

Store equipment $569,500

Less accumulated depreciation 70,700

Total property, plant, and equipment 498,800

Total assets $1,438,105

Current liabilities:

Accounts payable $ 63,150

Customer refunds payable 104,200

Salaries payable 13,600

Liabilities

Assets

Palisade Creek Co.

Balance Sheet

May 31, 20Y7

CHAPTER 6 Accounting for Merchandising Businesses

Comp. Prob. 2 (Continued)

9.

Page

23

Post.

Ref. Debit Credit

20Y7

May 31 Sales 410 5,316,205

Cost of Merchandise Sold 510 3,026,950

Sales Salaries Expense 520 727,800

Advertising Expense 521 292,000

Depreciation Expense 522 14,000

Store Supplies Expense 523 9,800

Date

JOURNAL

Closing Entries

CHAPTER 6 Accounting for Merchandising Businesses

Comp. Prob. 2 (Continued)

10.

Account Debit Credit

No. Balances Balances

Cash 110 99,430

Accounts Receivable 112 245,875

Merchandise Inventory 115 585,200

Prepaid Insurance 117 4,800

Store Supplies 118 4,000

May 31, 20Y7

Palisade Creek Co.

Post-Closing Trial Balance

CHAPTER 6 Accounting for Merchandising Businesses

Comp. Prob. 2 (Concluded)

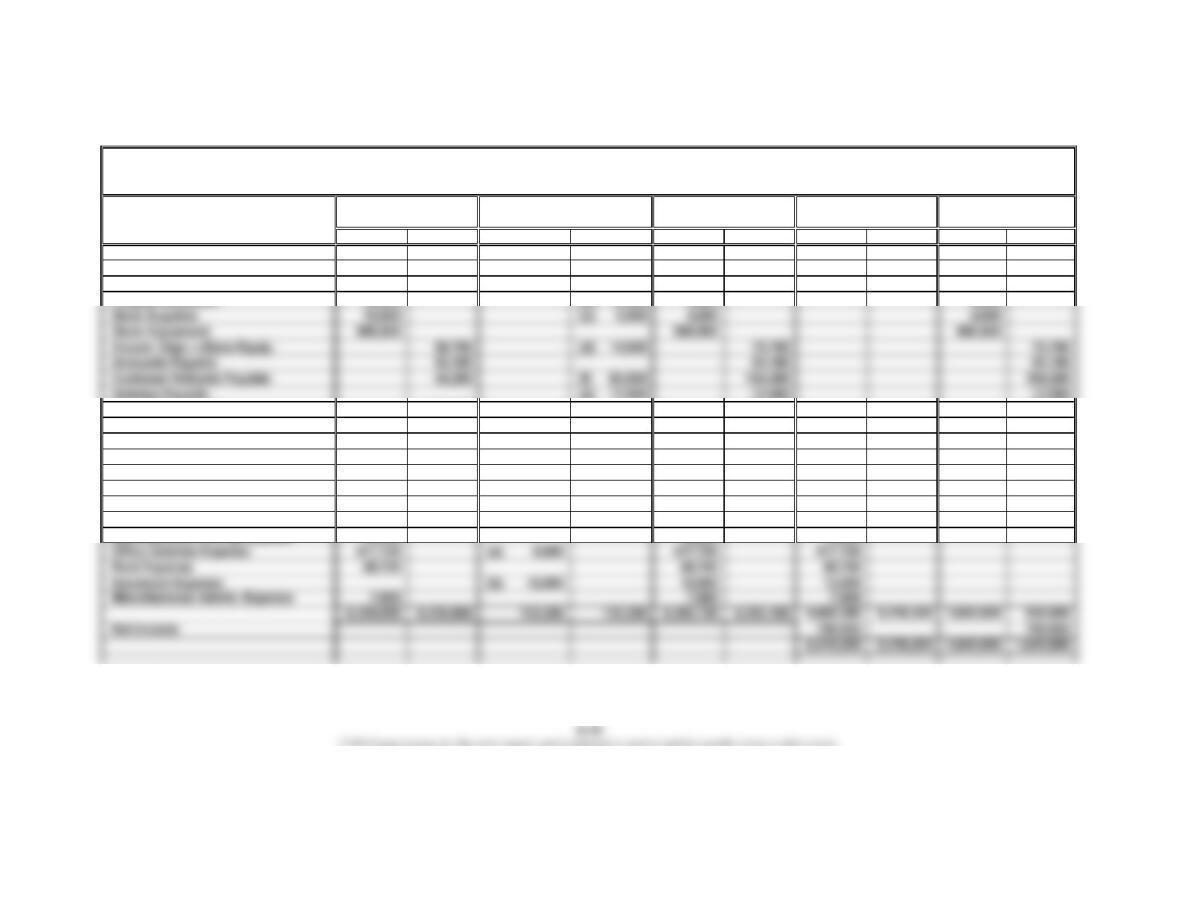

5. (Optional)*

Account Title Debit Credit Debit Credit Debit Credit Debit Credit

Cash 99,430 99,430 99,430

Accounts Receivable 245,875 245,875 245,875

Merchandise Inventory 599,150 (a) 13,950 585,200 585,200

Salaries Payable (e) 13,600 13,600 13,600

Lynn Tolley, Capital 685,300 685,300 685,300

Lynn Tolley, Drawing 135,000 135,000 135,000

Sales 5,376,205 (f) 60,000 5,316,205 5,316,205

Cost of Merchandise Sold 3,013,000 (a) 13,950 3,026,950 3,026,950

Sales Salaries Expense 720,800 (e) 7,000 727,800 727,800

Advertising Expense 292,000 292,000 292,000

Depreciation Expense (d) 14,000 14,000 14,000

Store Supplies Expense (c) 9,800 9,800 9,800

* This solution is applicable only if the end-of-period spreadsheet (work sheet) is used.

Palisade Creek Co.

End-of-Period Spreadsheet (Work Sheet)

For the Year Ended May 31, 20Y7

BalanceUnadjusted Adjusted Income

SheetTrial Balance

Debit Credit

Trial Balance StatementAdjustments

CHAPTER 6 Accounting for Merchandising Businesses

CP 6-1

Margie has been placed in a very difficult position. Someone she trusts and respects

has asked her to do something that is clearly unethical. If Margie makes the

adjusting entry, her boss could very well be terminated. Yet, Margie’s primary

responsibility has to be on preparing relevant and representationally faithful financial

information that is useful for decision making. Margie should, therefore, make the

appropriate adjusting entry. Being right, however, doesn’t always make a decision

easy. Margie’s actions could result in the termination of her boss and mentor.

CP 6-2

Standards of Ethical Conduct for Management Accountants requires management

accountants to perform in a competent manner and to comply with relevant laws,

regulations, and technical standards. If Shelby Davey intentionally subtracted

CP 6-3

A sample solution based on The Home Depot Inc.’s Form 10-K for the fiscal year ended

February 3, 2019, follows:

1. a. $37,160 million in 2018; $34,356 million in 2017; $32,313 million in 2016

b. 34.3% ($37,160 million/$108,203 million) in 2018; 34.0% ($34,356 million/$100,904

million) in 2017; 34.2% ($32,313 million/$94,595 million) in 2016

2. The company’s financial performance has improved between 2016 and 2017 and

again between 2017 and 2018. A majority of the above measures have improved

during this period.

CASES & PROJECTS

CP 6-4

To: Suzi Nomro

President, Watercraft Supply Company

From: A+ student

Re: Proposal to Increase Net Income

If the proposed changes in credit terms increase sales by 10% as expected, and if th

e

ratio of cost of merchandise sold to sales remails at 60%, this proposal has the potential

to increase net income by $64,200, from $321,000 to $385,200. This increase will be drive

n

There are several potential risks associated with this type of proposal. First, the

accuracy of the estimates used to project the effects of the proposed changes are not

certain. If the increase in sales does not materialize, Watercraft Supply Company could

incur significant costs of carrying excess inventory stocked in anticipation of increasing

sales. At the same time it is incurring these additional inventory costs, cash collections

from customers will be reduced by the amount of the discounts. This could create a

liquidity problem for Watercraft Supply.

CHAPTER 6 Accounting for Merchandising Businesses

CP 6-4 (Concluded)

Revenues:

Sales $1,485,000

Interest revenue 15,000

Total revenues $1,500,000

Notes:

a. Projected sales

[$1,350,000 + (10% × $1,350,000)]………………………

…

$1,485,000

b. Projected cost of merchandise sold

($1,485,000 × 60%)…………………………………………

…

$ 891,000

Watercraft Supply Company

Projected Income Statement

For the Year Ended October 31, 20Y3

CHAPTER 6 Accounting for Merchandising Businesses

CP 6-5

Cam Pfeifer is correct. The accounts payable due to suppliers could be included on

the balance sheet at an amount of $314,500 ($269,500 + $45,000). This is the amount

that will be expected to be paid to satisfy the obligation (liability) to suppliers.

However, this is proper only if Rustic Furniture Co. has a history of taking all

CP 6-6

1. If Mark doesn’t need the stereo immediately (by the next day), Wholesale Stereo

offers the best buy, as shown below.

Wholesale Stereo:

List price……………………………………………………………………

…

$1,200.00

Shipping and handling (not including next-day air)………………… 49.99

Total…………………………………………………………………………

…

$1,249.99

…

…

List price……………………………………………………………………

…

$1,175.00

Less 2% cash discount.…………………………………………………

…

23.50

Subtotal……………………………………………………………………… $1,151.50

Sales tax (9%).……………………………………………………………… 103.64

Total…………………………………………………………………………

…

$1,255.14

…

CHAPTER 6 Accounting for Merchandising Businesses

CP 6-6 (Concluded)

Because both Wholesale Stereo and Tru-Sound Systems will accept Mark’s VISA,

the ability to use a credit card would not affect the buying decision. Tru-Sound

Systems will, however, allow Mark to pay his bill in three installments (the first

due immediately). This would allow Mark to save some interest charges on his

VISA for two months. If we assume that Mark would have otherwise used his VISA

and that Mark’s VISA carries an interest of 1.5% per month on the unpaid balance,

The total interest savings would be $19.41 ($12.81 + $6.60). This interest

savings still would not be enough to offset the price advantage of Wholesale

Stereo, as shown below.

Tru-Sound Systems price (see above)……………………………………

…

$1,280.75

Less interest savings…………………………………………………………

…

19.41

Total………………………………………………………………………………

…

$1,261.34