Exercise 6-20 (LO 6-9)

Requirement 1

When goods are shipped FOB shipping point, title transfers from the seller to the

buyer at the time of shipment. This means that Mulligan Corporation (buyer) receives

Requirement 2

Balance Sheet

Income Statement

Year

Assets

Liabilities

Stockholders’

Equity

Revenues

Cost of

Goods Sold

Gross Profit

Exercise 6-21

Requirement 1

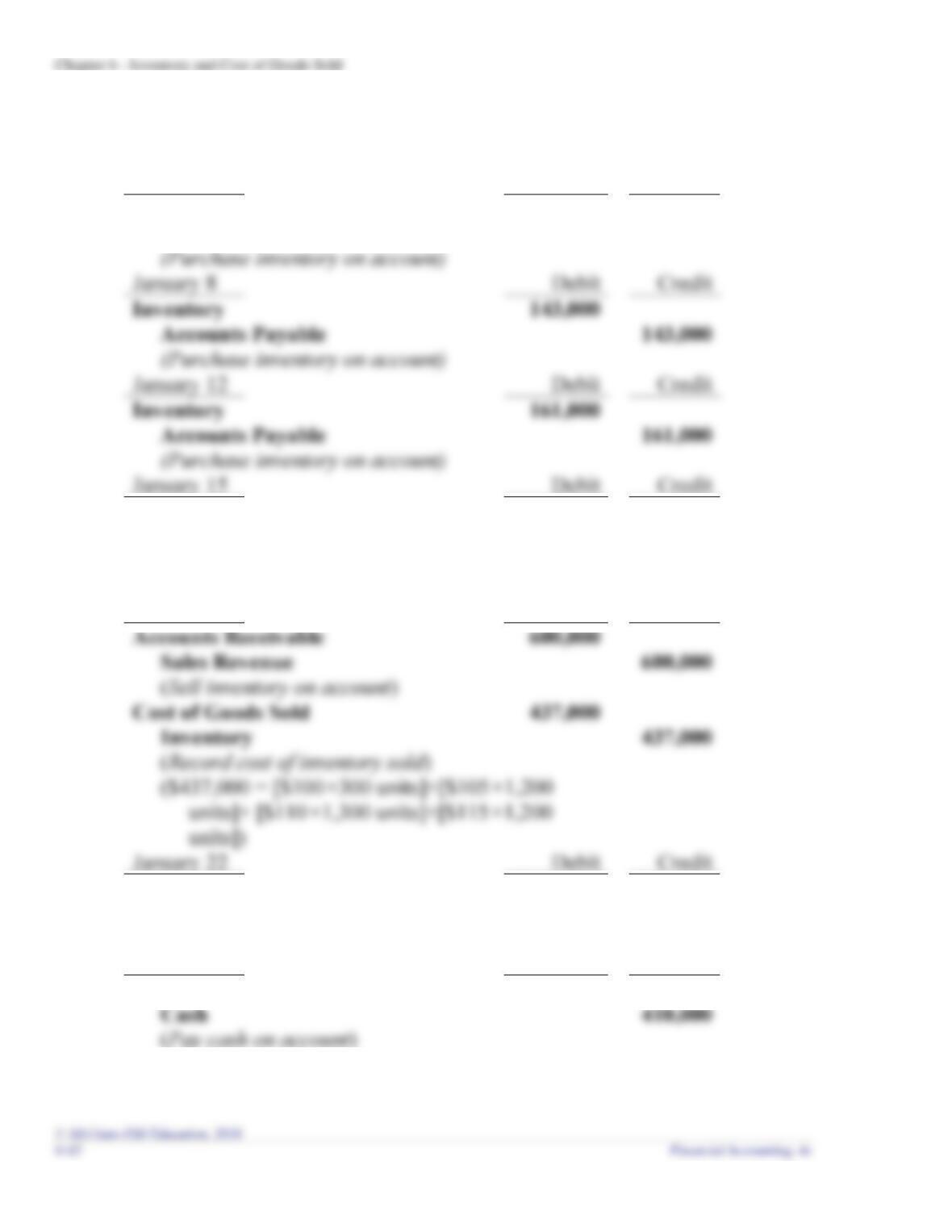

January 3

Debit

Credit

Inventory

126,000

Accounts Payable

126,000

January 8

Debit

Credit

Inventory

143,000

Accounts Payable

143,000

January 12

Debit

Credit

Inventory

161,000

Accounts Payable

161,000

January 15

Debit

Credit

Accounts Payable

11,500

Inventory

11,500

(Return defective inventory)

($11,500 = $115×100 units)

January 19

Debit

Credit

Accounts Receivable

600,000

Sales Revenue

600,000

(Sell inventory on account)

Cost of Goods Sold

437,000

Inventory

437,000

January 22

Debit

Credit

Cash

580,000

Accounts Receivable

580,000

(Receive cash on account)

January 24

Debit

Credit

Accounts Payable

410,000

Cash

410,000

(Pay cash on account)

Chapter 6 – Inventory and Cost of Goods Sold

Exercise 6-21 (continued)

Requirement 1 (concluded)

January 27

Debit

Credit

Allowance for Uncollectible Accounts

2,500

Accounts Receivable

2,500

January 31

Debit

Credit

Cash

128,000

Requirement 2

(a) January 31

Debit

Credit

Cost of Goods Sold

1,500

Inventory

1,500

(b) January 31

Debit

Credit

Bad Debt Expense

3,000

Allowance for Uncollectible

Accounts

3,000

(c) January 31

Debit

Credit

Interest Expense

Interest Payable

200

Income Tax Expense

Income Tax Payable

Exercise 6-21 (continued)

Requirement 3

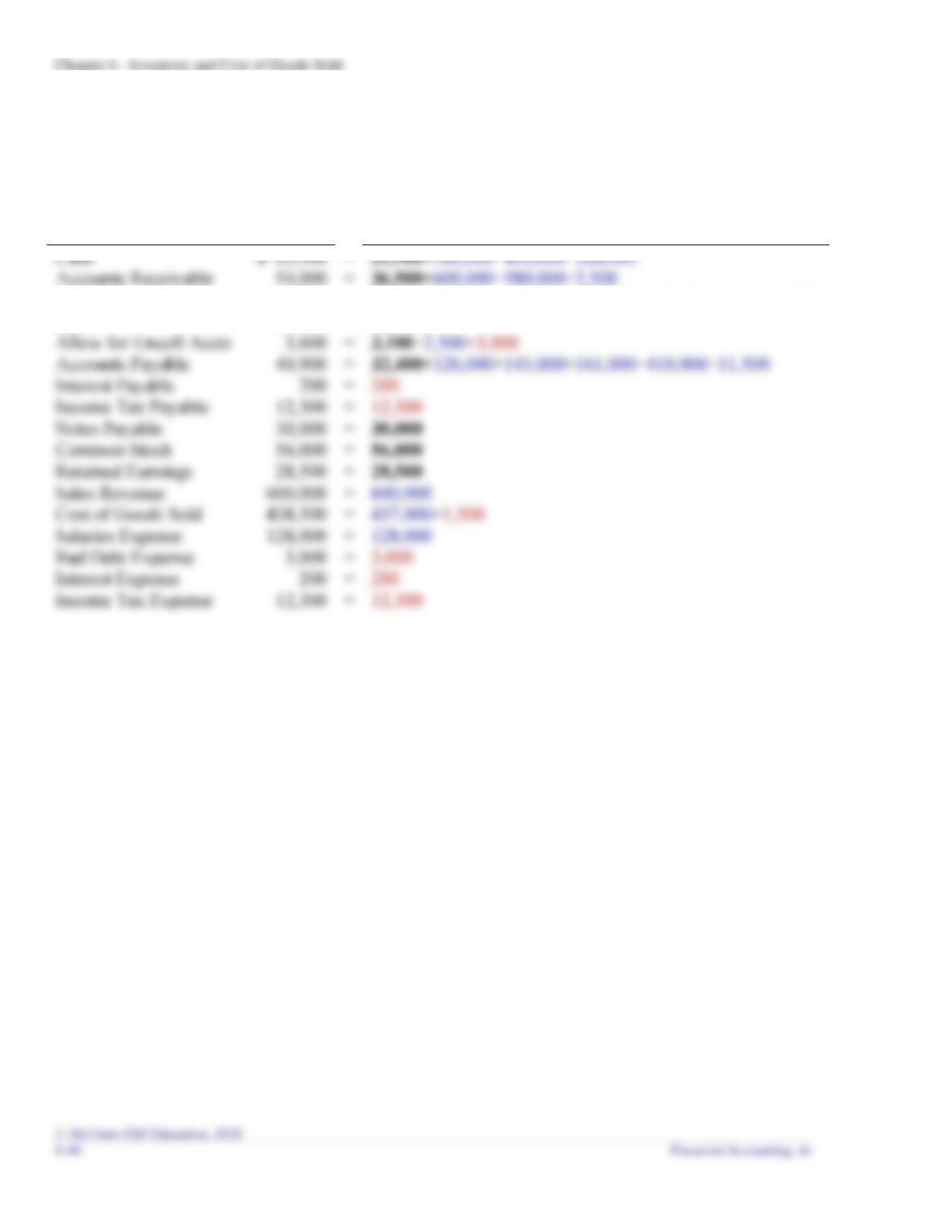

Big Blast Fireworks

Adjusted Trial Balance

January 31, 2018

Accounts

Debit

Credit

Cash

$ 63,900

Accounts Receivable

54,000

Land

61,600

Allowance for Uncollectible

Accounts

$ 3,600

Accounts Payable

40,900

Interest Payable

Income Tax Payable

12,300

Common Stock

56,000

Retained Earnings

28,500

Sales Revenue

Salaries Expense

128,000

Interest Expense

Income Tax Expense

12,300

Totals

$771,500

Exercise 6-21 (continued)

Requirement 3 (concluded)

Accounts

Ending

Balance

Beginning balance in bold, entries during January in blue,

and adjusting entries in red.

Cash

=

21,900+580,000−410,000−128,000

Accounts Receivable

54,000

=

36,500+600,000−580,000−2,500

Inventory

10,000

=

30,000+126,000+143,000+161,000−437,000−11,500−1,500

Land

61,600

=

61,600

Allow for Uncoll Accts

=

3,100−2,500+3,000

Accounts Payable

40,900

=

32,400+126,000+143,000+161,000−410,000−11,500

Interest Payable

=

Income Tax Payable

12,300

=

Notes Payable

30,000

=

30,000

Common Stock

56,000

=

Retained Earnings

28,500

=

Sales Revenue

600,000

=

Cost of Goods Sold

438,500

=

Salaries Expense

128,000

=

Bad Debt Expense

=

Interest Expense

=

Income Tax Expense

12,300

=

Chapter 6 – Inventory and Cost of Goods Sold

Exercise 6-21 (continued)

Requirement 4

Big Blast Fireworks

Multiple-Step Income Statement

For the year ended January 31, 2018

Sales revenue

$600,000

Cost of goods sold

438,500

Gross profit

$161,500

Salaries expense

128,000

Total operating expenses

Interest expense

Income tax expense

Requirement 5

Big Blast Fireworks

Classified Balance Sheet

January 31, 2018

Assets

Liabilities

Cash

$ 63,900

Accounts payable

$ 40,900

Accounts receivable

54,000

Interest payable

200

Less: Allowance

Income tax payable

Inventory

53,400

Notes payable

Land

Common stock

56,000

Retained earnings

46,500

*

Total assets

$185,900

Exercise 6-21 (continued)

Requirement 6

January 31, 2018

Debit

Credit

Sales Revenue

600,000

Retained Earnings

600,000

Retained Earnings

582,000

Salaries Expense

128,000

Bad Debt Expense

Interest Expense

Income Tax Expense

Exercise 6-21 (concluded)

Requirement 7

(a) The inventory turnover ratio is:

Inventory

Cost of Goods Sold

$438,500

(b) The gross profit ratio is:

Gross Profit

(Sales − Cost of Goods Sold)

($600,000 − $438,500)

(c) Based on the inventory turnover ratio and the gross profit ratio, Big Blast

Chapter 6 – Inventory and Cost of Goods Sold

PROBLEMS: SET A

Problem 6-1A (LO 6-3)

Requirement 1 Specific identification

Date

Transaction

Number

of units

Unit

cost

Ending

Inventory

Oct. 1

Beginning inventory

1

$900

$ 900

Oct. 30

Purchase

7

930

6,510

Date

Transaction

Number

of units

Unit

cost

Oct. 1

Beginning inventory

$900

Oct. 1

Beginning inventory

900

Oct. 10

Purchase

910

Oct. 10

Purchase

910

Oct. 20

Purchase

Requirement 2 FIFO

Date

Transaction

Number

of units

Unit

cost

Ending

Inventory

Oct. 20

Purchase

1

$920

$ 920

Oct. 30

Purchase

7

930

6,510

8

Date

Transaction

Number

of units

Unit

cost

Oct. 1

Beginning inventory

$900

Oct. 20

Purchase

920

Chapter 6 – Inventory and Cost of Goods Sold

Problem 6-1A (concluded)

Requirement 3 LIFO

Date

Transaction

Number

of units

Unit

Cost

Ending

Inventory

Oct. 1

Beginning inventory

6

$900

$5,400

Oct. 10

Purchase

2

910

1,820

8

Date

Transaction

of units

Cost

Oct. 10

Purchase

3

$910

Oct. 20

Purchase

4

920

Oct. 30

Purchase

Requirement 4 Weighted average

Date

Transaction

Number

of units

Unit

cost

Total

Cost

Oct. 1

Beginning inventory

6

$900

$ 5,400

Oct. 10

Purchase

5

910

4,550

Oct. 20

Purchase

4

3,680

Oct. 30

Purchase

7

930

Problem 6-2A (LO 6-3, 6-4, 6-5)

Requirement 1 Specific identification

Date

Transaction

Number

of units

Unit

cost

Ending

Inventory

Mar. 1

Beginning inventory

1

$250

$ 250

Mar. 9

Purchase

2

270

540

Mar. 22

Purchase

2

280

560

Date

Transaction

Number

of units

Unit

cost

Mar. 1

Beginning inventory

$250

$3,750

Mar. 9

Purchase

270

Mar. 1

Beginning inventory

250

Requirement 2 FIFO

Date

Transaction

Number

of units

Unit

cost

Ending

Inventory

Mar. 22

Purchase

5

$280

$1,400

Mar. 30

Purchase

9

300

2,700

Date

Transaction

of units

cost

Mar. 9

Purchase

270

2,700

Mar. 22

Purchase

280

1,400

$9,100

Problem 6-2A (continued)

Requirement 3 LIFO

Date

Transaction

Number

of units

Unit

cost

Ending

Inventory

Date

Transaction

Number

of units

Unit

cost

Cost of

Goods Sold

Mar. 1

Beginning inventory

6

$250

$1,500

Mar. 9

Purchase

10

270

2,700

Mar. 22

Purchase

10

280

2,800

Mar. 30

Purchase

9

2,700

Requirement 4 Weighted average

Date

Transaction

Number

of units

Unit

cost

Total

Cost

Mar. 1

Beginning inventory

20

$250

$ 5,000

Mar. 9

Purchase

10

270

2,700

Mar. 22

Purchase

10

2,800

Mar. 30

Purchase

9

2,700

Problem 6-2A (concluded)

Requirement 5

Specific

Identification

FIFO

LIFO

Weighted-

average

Cost

Sales revenue

$15,300

$15,300

$15,300

$15,300.00

Cost of goods sold

Gross profit

Requirement 6

FIFO provides the more meaningful measure of ending inventory. The amount of

Requirement 7

March 31

Debit

Credit

Cost of Goods Sold

600

Inventory

600*

Chapter 6 – Inventory and Cost of Goods Sold

Problem 6-3A (LO 6-2, 6-5)

Requirement 1

July 3

Debit

Credit

Inventory

2,300

Accounts Payable

(Purchase inventory on account)

July 4

Inventory

110

Cash

110

(Pay freight-in)

July 9

Inventory

(Return inventory on account)

July 11

Accounts Payable

2,100

Inventory

Cash

2,079

July 12

Accounts Receivable

5,800

Sales Revenue

5,800

(Sell inventory on account)

Cost of Goods Sold

3,000

Inventory

(Record cost of inventory sold)

July 15

Cash

5,800

Accounts Receivable

(Receive cash on account)

Problem 6-3A (concluded)

Requirement 1 (continued)

July 18

Debit

Credit

Inventory

3,100

Accounts Payable

3,100

(Purchase inventory on account)

July 22

Cash

4,200

Sales Revenue

Cost of Goods Sold

Inventory

(Record cost of inventory sold)

July 28

Accounts Payable

300

Inventory

300

(Return inventory on account)

July 30

Accounts Payable

Cash

Requirement 2

CD City

Multiple-step Income Statement (partial)

For the month of July

Net sales

$10,000

Cost of goods sold

Gross profit

Problem 6-4A (LO 6-6)

Requirement 1

Inventory

items

Quantity

Cost

Per unit

Total

Cost

Vans

4

$27,000

$108,000

Trucks

7

18,000

126,000

4-door sedans

5

17,000

Sports cars

1

37,000

SUVs

6

180,000

Requirement 2

Inventory

items

Quantity

Cost

Per unit

NRV

per unit

Lower of

Cost and

NRV

per unit

Total

Vans

4

$27,000

$25,000

$25,000

$100,000

Trucks

7

18,000

17,000

17,000

119,000

2-door sedans

3

13,000

15,000

13,000

Sports cars

1

37,000

37,000

SUVs

6

28,000

28,000

Requirement 3

Because the total of lower of cost and net realizable value ($548,000) is less than total

cost ($575,000), inventory is written down for the difference ($27,000).

Debit

Credit

Requirement 4

The write-down of inventory from cost to net realizable value reduces total assets and

increases total expenses, leading to lower net income and lower retained earnings.

6-58 Financial Accounting, 4e

Problem 6-5A (LO 6-3, 6-6)

Requirement 1 FIFO

Date

Transaction

Number

of units

Unit

cost

Ending

Inventory

Mar. 12

Purchase

40

$16

$ 640

Sep. 17

Purchase

60

Date

Transaction

of units

Goods Sold

Jan. 1

Beginning inventory

$21

Mar. 12

Purchase

50

16

Requirement 2 LIFO

Date

Transaction

Number

of units

Unit

cost

Ending

Inventory

Jan. 1

Beginning inventory

100

$21

Date

Transaction

Number

of units

Unit

cost

Cost of

Goods Sold

Jan. 1

Beginning inventory

20

$21

$ 420

Sep. 17

Purchase

60

Chapter 6 – Inventory and Cost of Goods Sold

Problem 6-5A (concluded)

Requirement 3

Ending Inventory

Cost

NRV

Lower of Cost

and NRV

FIFO

FIFO

Problem 6-6A (LO 6-2, 6-3, 6-4, 6-5, 6-6)

Requirement 1

October 4

Debit

Credit

Inventory

6,500

Accounts Payable

(Purchase inventory on account)

October 5

Inventory

600

Cash

600

(Pay freight-in)

October 9

Inventory

(Return inventory on account)

October 12

Accounts Payable

6,000

Inventory

120

October 15

Accounts Receivable

(Sell inventory on account)

Cost of Goods Sold

Inventory

($8,440 = ($50 × 50 units) + ($54 × 110 units))

October 19

Cash

Accounts Receivable

(Receive cash on account)