Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

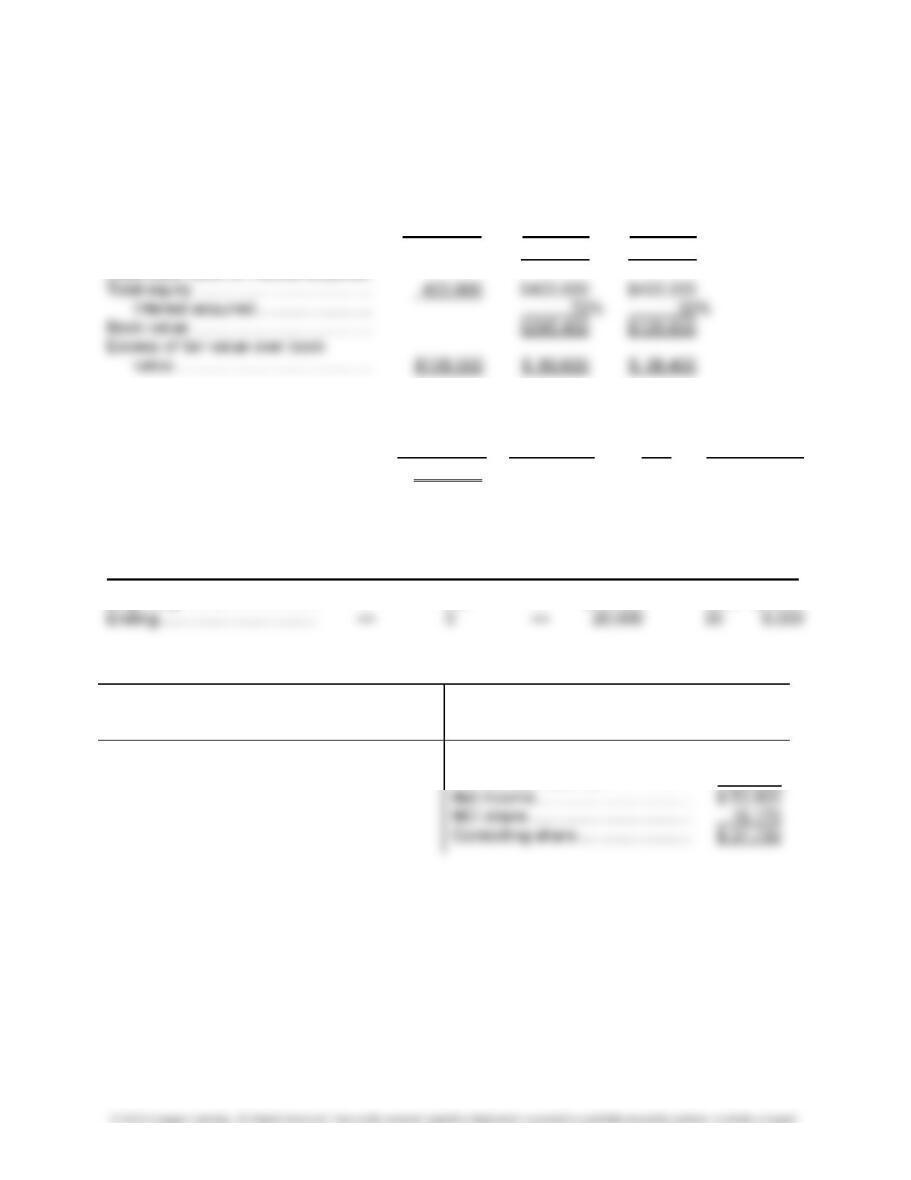

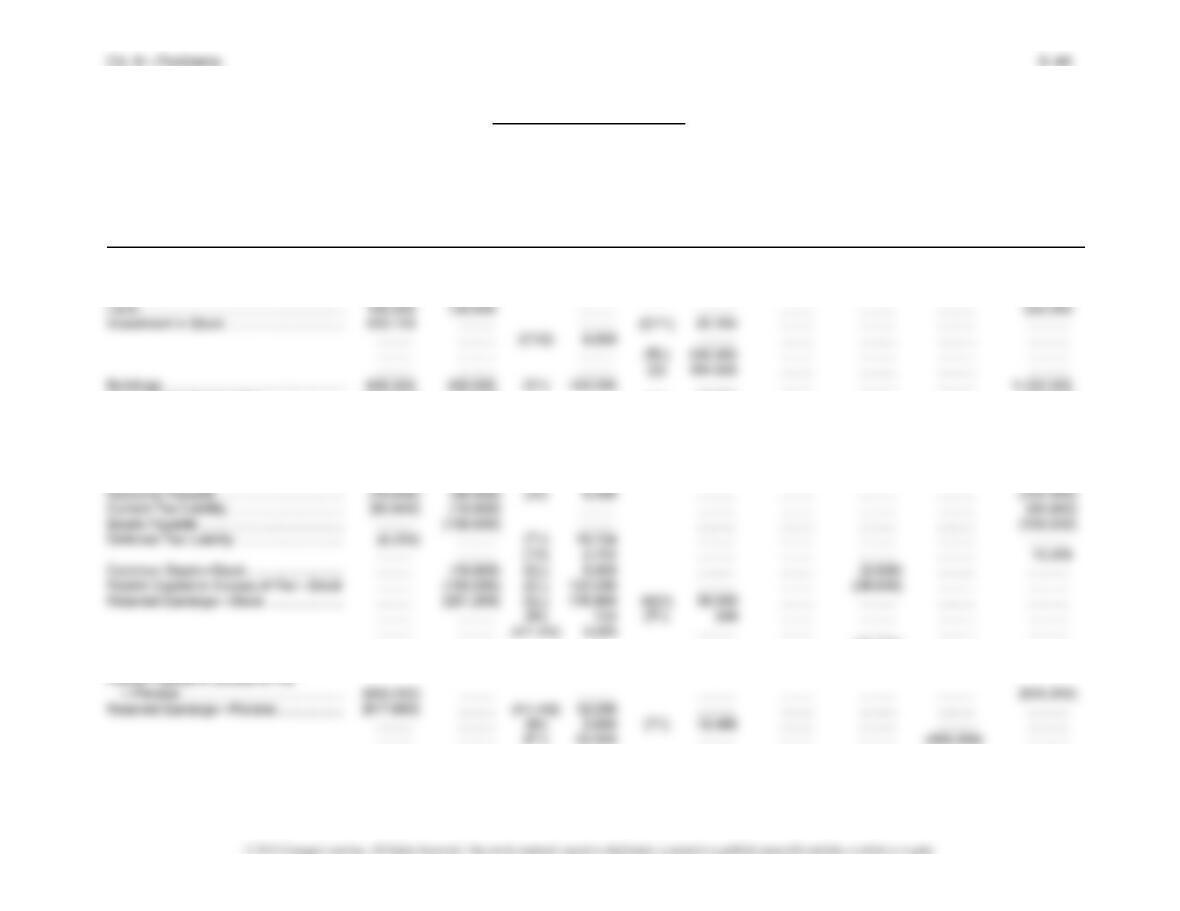

Problem 6-9, Concluded

Parson Company and Subsidiary Solar Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

(Concluded)

Eliminations Consolidated Controlling Consolidated

Trial Balance and Adjustments Income Retained Balance

Parson Solar Dr. Cr. Statement NCI Earnings Sheet

Sales ...................................................... (950,000) (400,000) (IS) 100,000 .......... (1,250,000) .......... .......... ..........

Interest Expense .................................... .......... 8,000 .......... .......... 8,000 .......... .......... ..........

Gain on Sale of Fixed Asset ................... .......... (25,000) (F1) 25,000 .......... ......... .......... .......... ..........

Subsidiary Income .................................. (57,600) .......... (CY1) 57,600 .......... ......... .......... .......... ..........

Dividends Declared—Solar .................... .......... 10,000 .......... (CY2) 8,000 ......... 2,000 .......... ..........

Eliminations and Adjustments:

(CY1) Current-year subsidiary income.

(CY2) Current-year dividend.

(EL) Eliminate controlling interest in subsidiary equity.

(D)/(NCI) Distribute excess and adjust NCI per D&D schedule.

(BI) Defer beginning inventory profit.

(EI) Defer ending inventory profit.

(F1) Fixed asset profit at beginning of year.

(F2) Fixed asset profit realized.

6–37 Ch. 6—Problems

PROBLEM 6-10

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (70%) (30%)

Fair value of subsidiary ..................... $550,000 $385,000 $165,000

Less book value of interest acquired:

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Goodwill ............................................ $128,000 debit D

Intercompany Inventory Profit Deferral

Parent Parent Parent Sub Sub Sub

Amount Percent Profit Amount Percent Profit

Beginning .............................. — 0% — $10,000 30% $3,000

Subsidiary Solan Company Income Distribution

Ending inventory profit .................. $6,000 Internally generated income ........ $ 80,000

Beginning inventory profit ........... 3,000

Adjusted income ......................... $ 77,000

Tax provision (30%) .................... (23,100)

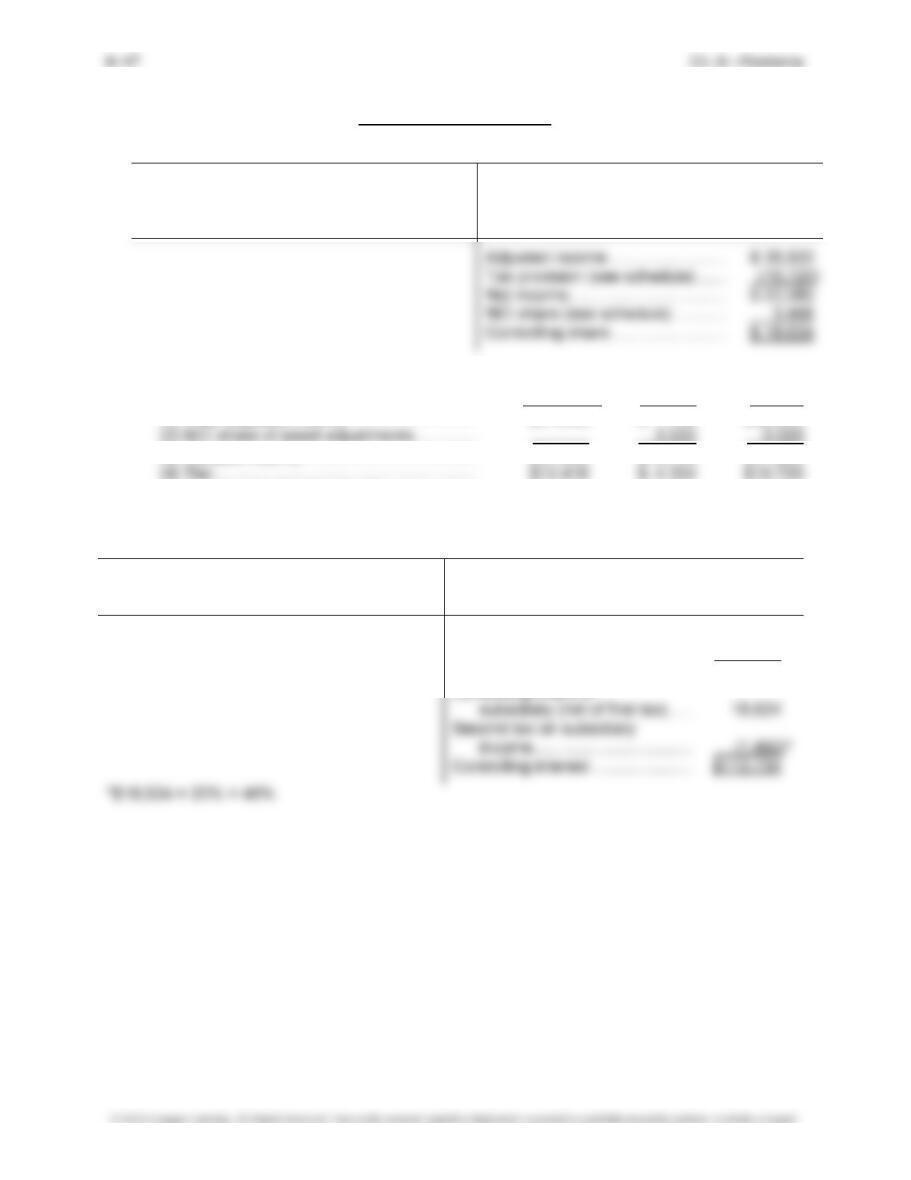

Problem 6-10, Continued

Parent Perko Company Income Distribution

Internally generated income ........ $100,000

Realized gain .............................. 7,000

Adjusted income ......................... $107,000

Tax provision (30%) .................... (32,100)

Net income .................................. $ 74,900

DTA/DTL adjustments:

To beginning retained earnings: Parent Sub

Subsidiary transactions:

Beginning inventory ............................................ $ 3,000

Remaining fixed asset profit ............................... —

Total ................................................................... $ 3,000

First tax .............................................................. $ 900 $ 630 $ 270

Second tax ......................................................... $ 88 88

To current year:

Subsidiary transactions:

Beginning inventory ............................................ $ (3,000)

Ending inventory ................................................ 6,000

Fixed asset sale ................................................. —

Realized fixed asset ........................................... —

Total ................................................................... $ 3,000

First tax .............................................................. $ 900 $ 630 $ 270

Second tax ......................................................... $ 88 $ 88

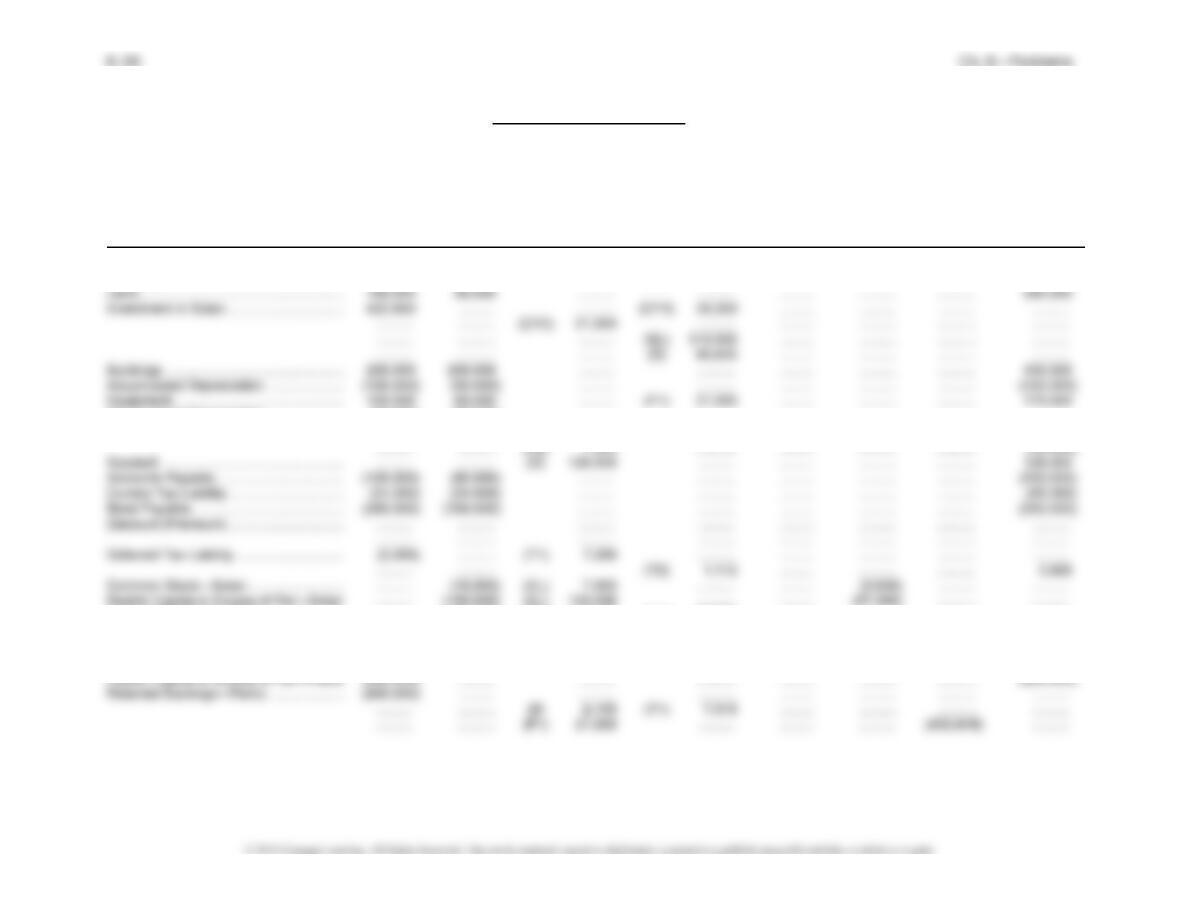

Problem 6-10, Continued

Perko Company and Subsidiary Solan Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

Eliminations Consolidated Controlling Consolidated

Trial Balance and Adjustments Income Retained Balance

Perko Solan Dr. Cr. Statement NCI Earnings Sheet

Accounts Receivable .............................. 282,576 295,000 .......... .......... ......... .......... .......... 577,576

Inventory ................................................ 110,000 85,000 .......... (EI) 6,000 ......... .......... .......... 189,000

Accumulated Depreciation ..................... (35,000) (20,000) .......... .......... ......... .......... .......... ..........

.......... .......... .......... .......... ......... .......... .......... ..........

Retained Earnings—Solan ..................... .......... (250,000) (EL) 175,000 (NCI) 38,400 ......... .......... .......... ..........

.......... .......... (BI) 900 (T1) 270 ......... .......... .......... ..........

.......... .......... .......... .......... ......... (112,770) .......... ..........

Common Stock—Perko .......................... (100,000) .......... .......... .......... ......... .......... .......... (100,000)

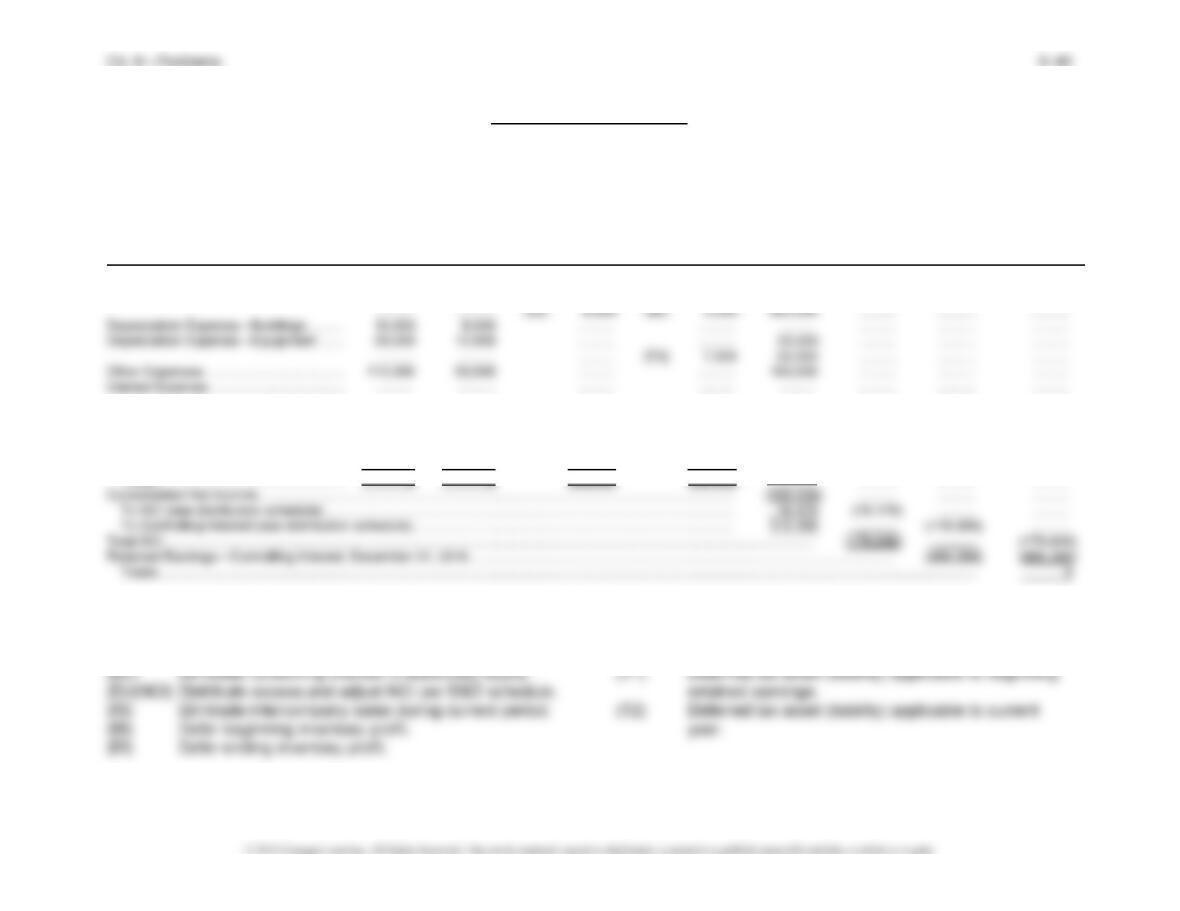

Problem 6-10, Concluded

Perko Company and Subsidiary Solan Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

(Concluded)

Eliminations Consolidated Controlling Consolidated

Trial Balance and Adjustments Income Retained Balance

Perko Solan Dr. Cr. Statement NCI Earnings Sheet

Sales ...................................................... (590,000) (370,000) (IS) 60,000 .......... (900,000) .......... .......... ..........

Cost of Goods Sold ................................ 340,000 220,000 .......... (IS) 60,000 ......... .......... .......... ..........

.......... .......... .......... .......... ......... .......... .......... ..........

Provision for Tax .................................... 32,352 24,000 (T2) 1,112 .......... 57,464 .......... .......... ..........

Subsidiary Income .................................. (39,200) .......... (CY1) 39,200 .......... ......... .......... .......... ..........

Dividends Declared—Solan ................... .......... 30,000 .......... (CY2) 21,000 ......... 9,000 .......... ..........

Dividends Declared—Perko ................... 60,000 .......... .......... .......... ......... .......... 60,000 ..........

Totals .................................................. 0 0 608,600 608,600 ......... .......... .......... ..........

Eliminations and Adjustments:

(CY1) Current-year subsidiary income.

(CY2) Current-year dividend.

(F1) Fixed asset profit at beginning of year.

(F2) Fixed asset profit realized.

6–41 Ch. 6—Problems

PROBLEM 6-11

(1) Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary .............. $562,500 $450,000 $112,500

Less book value of interest acquired:

Common stock ...................... $ 10,000

Paid-in capital in excess of par 190,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Buildings .................................... $100,000 debit D1 20 $ 5,000

(2) Account Adjustments Annual Current Prior

to Be Amortized Life Amount Year Years Total Key

Buildings ........................ 20 $ 5,000 $ 5,000 $ 5,000 $10,000 (A1)

Intercompany Inventory Profit Deferral

Parent Parent Parent Sub Sub Sub

Amount Percent Profit Amount Percent Profit

Problem 6-11, Continued

Subsidiary Stock Company Income Distribution

Amortizations .............................. $15,000 Internally generated income ........ $ 42,000

Ending inventory profit ................ 4,800 Beginning inventory profit ............ 3,600

Adjusted income .......................... $ 25,800

Tax provision (see schedule) ....... (11,520)

Subsidiary tax schedule: Controlling NCI Total

(1) Total adjusted income ............................. $20,640 $5,160 $25,800

(2) NCI share of asset adjustments

($15,000 × 20%) .................................. 3,000 3,000

Parent Penske Company Income Distribution

Internally generated income ........ $205,000

Realized gain .............................. 8,000

Adjusted income ......................... $213,000

Tax provision (40%) .................... (85,200)

Net income .................................. $127,800

Controlling share of

6–43 Ch. 6—Problems

Problem 6-11, Continued

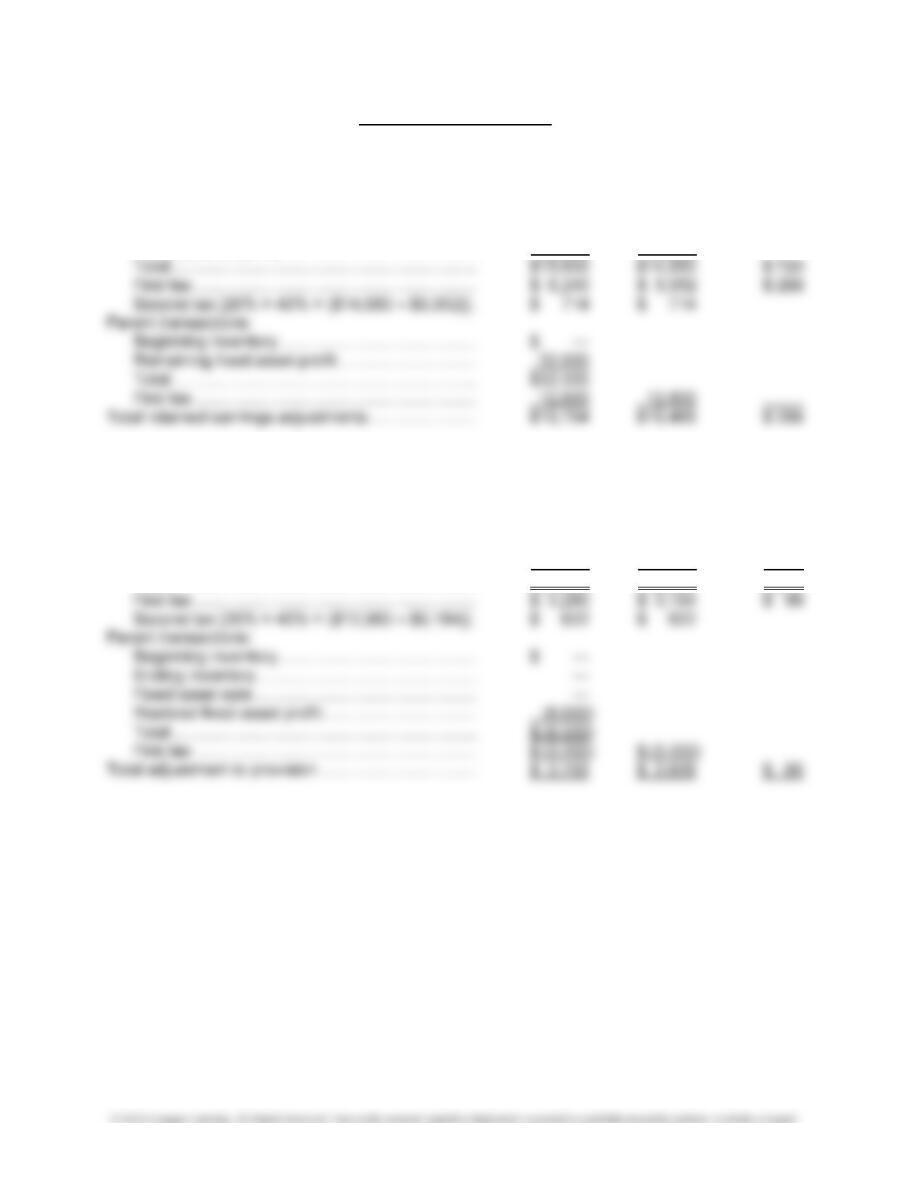

DTA/DTL adjustments:

To beginning retained earnings: Total Parent Sub

Subsidiary transactions:

Beginning inventory ............................................ $ 3,600 $ 2,880 $ 720

Remaining fixed asset profit ............................... — — —

Amortizations (80%) ........................................... 12,000 12,000

To current year:

Subsidiary transactions:

Beginning inventory ............................................ $ (3,600) $ (2,880) $(720)

Ending inventory ................................................ 4,800 3,840 960

Fixed asset sale ................................................. —

Realized fixed asset ........................................... —

Amortizations (80%) ........................................... 12,000 12,000

Total ................................................................... $13,200 $12,960 $ 240

Problem 6-11, Continued

Penske Company and Subsidiary Stock Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

Eliminations Consolidated Controlling Consolidated

Trial Balance and Adjustments Income Retained Balance

Penske Stock Dr. Cr. Statement NCI Earnings Sheet

Cash ....................................................... 92,400 53,200 .......... .......... ......... .......... .......... 145,600

Accounts Receivable .............................. 150,600 90,000 .......... (IA) 6,000 ......... .......... .......... 234,600

Inventory ................................................ 105,000 90,000 .......... (EI) 4,800 ......... .......... .......... 190,200

Accumulated Depreciation ..................... (250,000) (70,000) .......... (A1) 10,000 ......... .......... .......... (330,000)

Equipment .............................................. 210,000 120,000 (D2) 50,000 (F1) 40,000 ......... .......... .......... 340,000

Accumulated Depreciation ..................... (115,000) (90,000) .......... (A2) 20,000 ......... .......... .......... ...........

.......... .......... (F1) 8,000 .......... ......... .......... .......... ...........

.......... .......... (F2) 8,000 .......... ......... .......... .......... (209,000)

Goodwill ................................................. .......... 30,000 (D3) 42,500 .......... ......... .......... .......... 72,500

.......... .......... .......... .......... ......... (79,308) .......... ...........

Common Stock—Penske ....................... (100,000) .......... .......... .......... ......... .......... .......... (100,000)

Problem 6-11, Concluded

Penske Company and Subsidiary Stock Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

(Concluded)

Eliminations Consolidated Controlling Consolidated

Trial Balance and Adjustments Income Retained Balance

Penske Stock Dr. Cr. Statement NCI Earnings Sheet

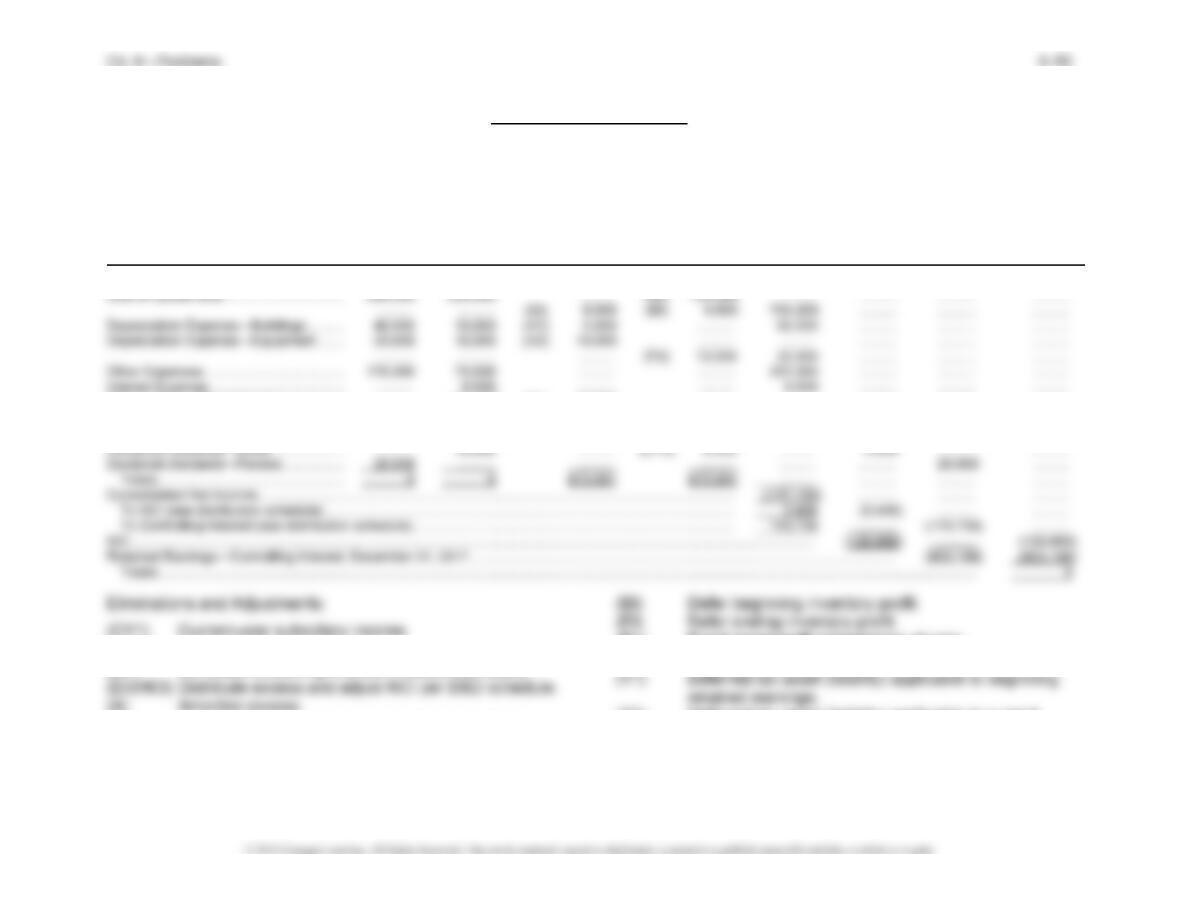

Sales ...................................................... (890,000) (350,000) (IS) 30,000 .......... (1,210,000) .......... .......... ...........

Cost of Goods Sold ................................ 480,000 220,000 .......... (IS) 30,000 ......... .......... .......... ...........

.......... .......... (EI) 4,800 (BI) 3,600 671,200 .......... .......... ...........

.......... .......... .......... .......... ......... .......... .......... ...........

Provision for Income Tax ....................... 83,613 16,800 .......... (T2) 2,702 97,711 .......... .......... ...........

Subsidiary Income .................................. (20,160) .......... (CY1) 20,160 .......... ......... .......... .......... ...........

(CY2) Current-year dividend.

(EL) Eliminate controlling interest in subsidiary equity.

(D)/(NCI) Distribute excess and adjust NCI per D&D schedule.

(A) Amortize excess.

(IS) Eliminate intercompany sales during current period.

(EI) Defer ending inventory profit.

(F1) Fixed asset profit at beginning of year.

(F2) Fixed asset profit realized.

(T1) Deferred tax asset (liability) applicable to beginning

retained earnings.

PROBLEM 6-12

(1) Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary .............. $562,500 $450,000 $112,500

Less book value interest acquired:

Common stock ....................... $ 10,000

Paid-in capital in excess of par 190,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Buildings .................................... $100,000 debit D1 20 $ 5,000

Equipment.................................. 50,000 debit D2 5 10,000

(2) Account Adjustments Annual Current Prior

to Be Amortized Life Amount Year Years Total Key

Buildings ........................ 20 $ 5,000 $ 5,000 $10,000 $15,000 (A1)

Equipment...................... 5 10,000 10,000 20,000 30,000 (A2)

Problem 6-12, Continued

Subsidiary Stock Company Income Distribution

Amortizations .............................. $15,000 Internally generated income ........ $ 72,000

Ending inventory profit ................ 3,000 Beginning inventory profit ............ 4,800

Equipment gain ........................... 25,000 Realized gain ............................... 5,000

Subsidiary tax schedule: Controlling NCI Total

(1) Total adjusted income ............................. $31,040 $ 7,760 $38,800

(3) Taxable income ...................................... $31,040 $10,760 $41,800

(5) Net income (line 1 – line 4) ..................... $18,624 $ 3,456 $22,080

Parent Penske Company Income Distribution

Ending inventory profit .................. $6,000 Internally generated income ........ $159,000

Realized gain .............................. 8,000

Adjusted income ......................... $161,000

Tax provision (40%) .................... (64,400)

Net income .................................. $ 96,600

Controlling share of

Problem 6-12, Continued

DTA/DTL adjustments:

To beginning retained earnings: Parent Sub

Subsidiary transactions:

Beginning inventory ............................................ $ 4,800 $ 3,840 $ 960

Total RE adjustments ............................................... $22,456 $22,072 $ 384

To current year:

Subsidiary transactions:

Beginning inventory ............................................ $ (4,800) $ (3,840) $ (960)

Ending inventory ................................................ 3,000 2,400 600

6–49 Ch. 6—Problems

Problem 6-12, Continued

Penske Company and Subsidiary Stock Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2017

Buildings ................................................ 900,000 250,000 (D1) 100,000 .......... ......... .......... .......... 1,250,000

Accumulated Depreciation ..................... (290,000) (80,000) .......... (A1) 15,000 ......... .......... .......... (385,000)

Equipment .............................................. 210,000 120,000 (D2) 50,000 (F1) 65,000 ......... .......... .......... 315,000

Accumulated Depreciation ..................... (140,000) (100,000) .......... (A2) 30,000 ......... .......... .......... ..........

.......... .......... (BI) 960 (T1) 384 ......... .......... .......... ..........

.......... .......... (A1–A2) 6,000 .......... ......... .......... .......... ..........

.......... .......... .......... .......... ......... (79,204) .......... ..........

Common Stock—Penske ....................... (100,000) .......... .......... .......... ......... .......... .......... (100,000)

Problem 6-12, Concluded

Penske Company and Subsidiary Stock Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2017

(Concluded)

Eliminations Consolidated Controlling Consolidated

Trial Balance and Adjustments Income Retained Balance

Penske Stock Dr. Cr. Statement NCI Earnings Sheet

Sales ...................................................... (950,000) (400,000) (IS) 100,000 .......... (1,250,000) .......... .......... ..........

Gain on Sale of Fixed Asset ................... .......... (25,000) (F1) 25,000 .......... ......... .......... .......... ..........

Provision for Income Taxes .................... 66,365 28,800 .......... (T2) 12,555 82,610 .......... .......... ..........

Subsidiary Income .................................. (34,560) .......... (CY1) 34,560 .......... ......... .......... .......... ..........

(CY2) Current-year dividend.

(EL) Eliminate controlling interest in subsidiary equity.

(IS) Eliminate intercompany sales during current period.

(IA) Eliminate intercompany unpaid trade accounts.

(F1) Fixed asset profit at beginning of year.

(F2) Fixed asset profit realized.

(T2) Deferred tax asset (liability) applicable to current

year.