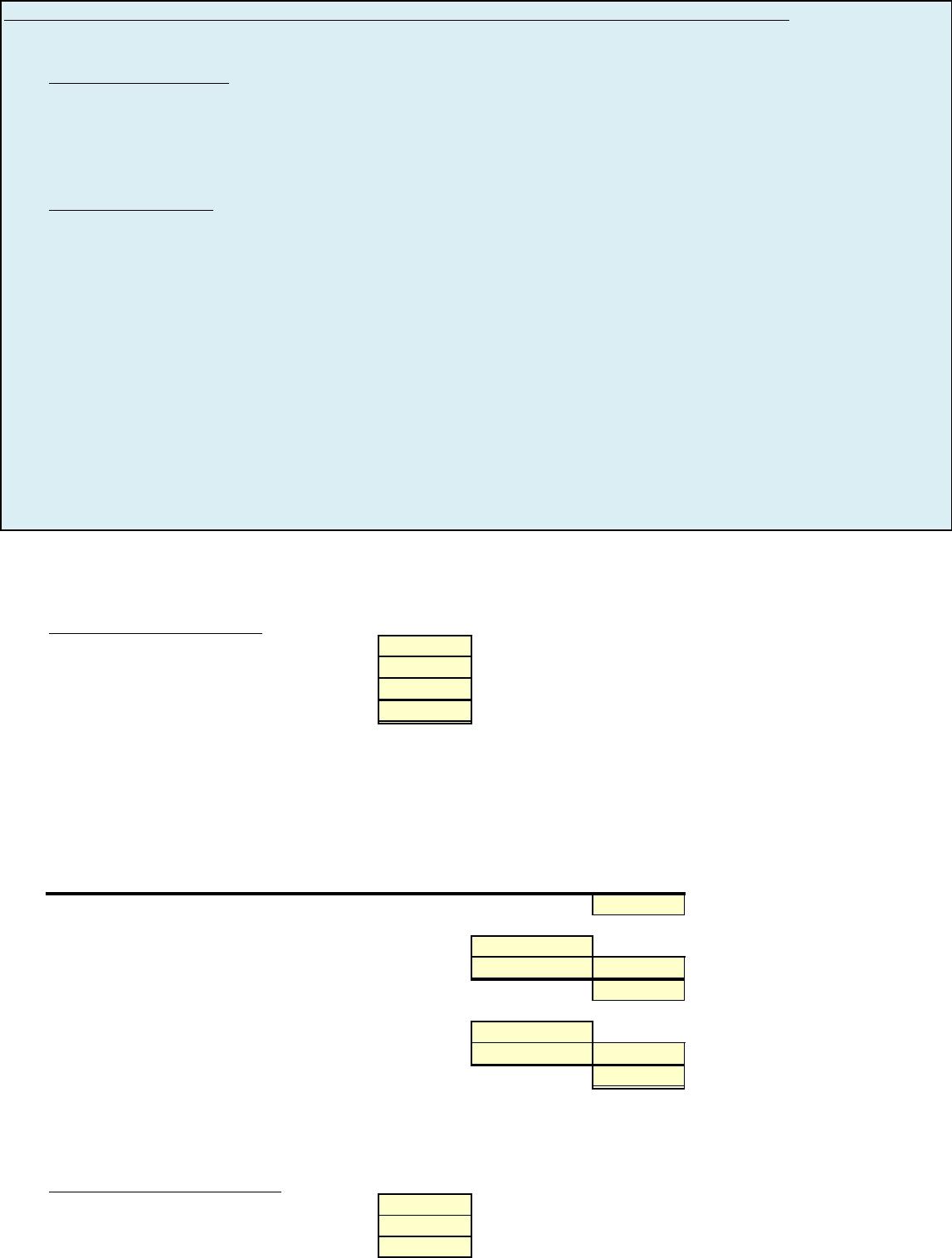

E6-1 Compute break-even point and margin of safety

The Soma Inn is trying to determine its break-even point. The inn has 75 rooms that are rented at $60

a night. Operating costs are as follows.

Salaries $10,600 per month

Utilities 2,400 per month

Depreciation 1,500 per month

Maintenance 800 per month

Maid service 8 per room

Other costs 34 per room

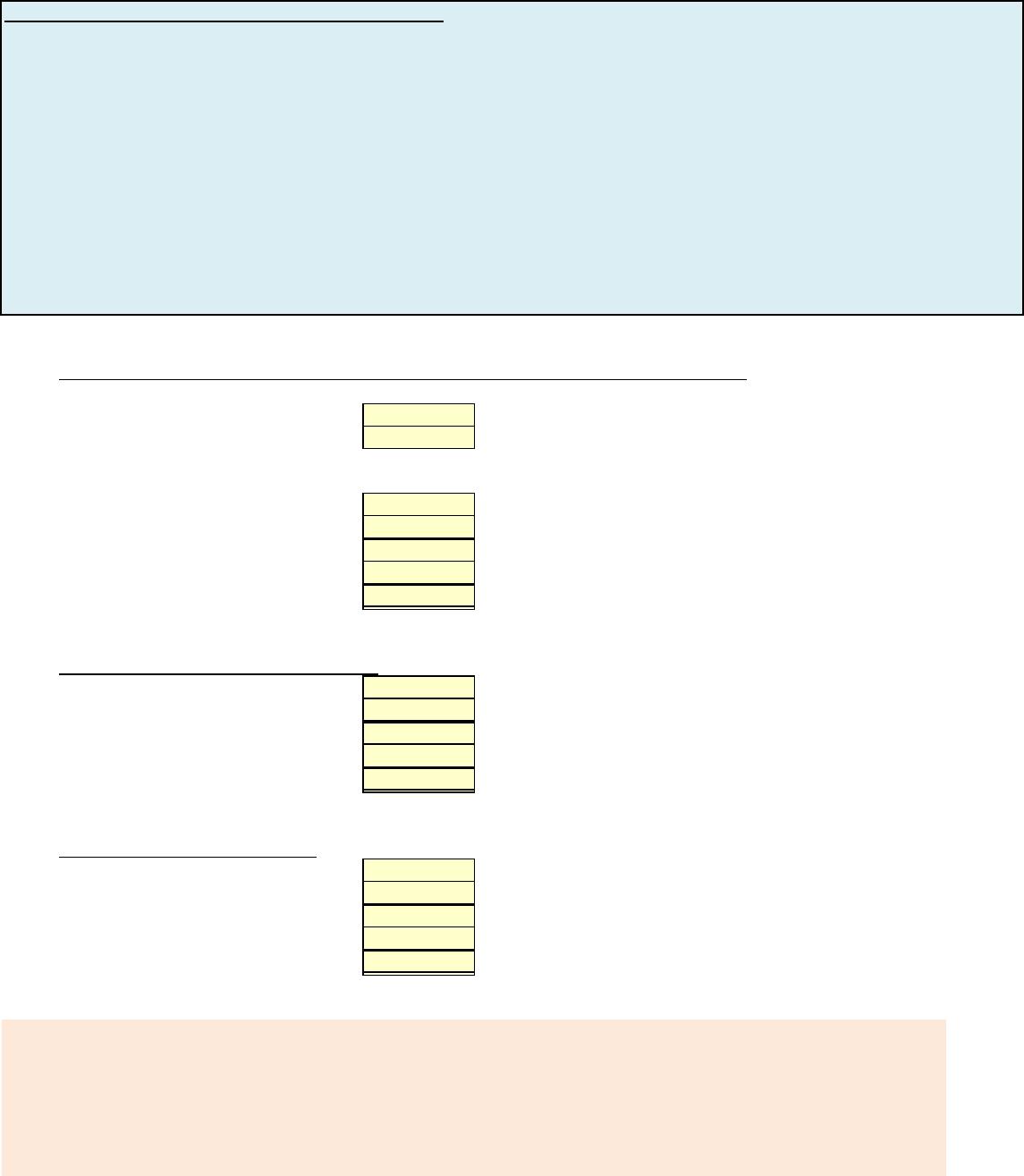

Instructions

(a) Determine the inn’s break-even point in (1) number of rented rooms per month and

(2) dollars.

(b) If the inn plans on renting an average of 50 rooms per day (assuming a 30-day month),

what is (1) the monthly margin of safety in dollars and (2) the margin of safety ratio?

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

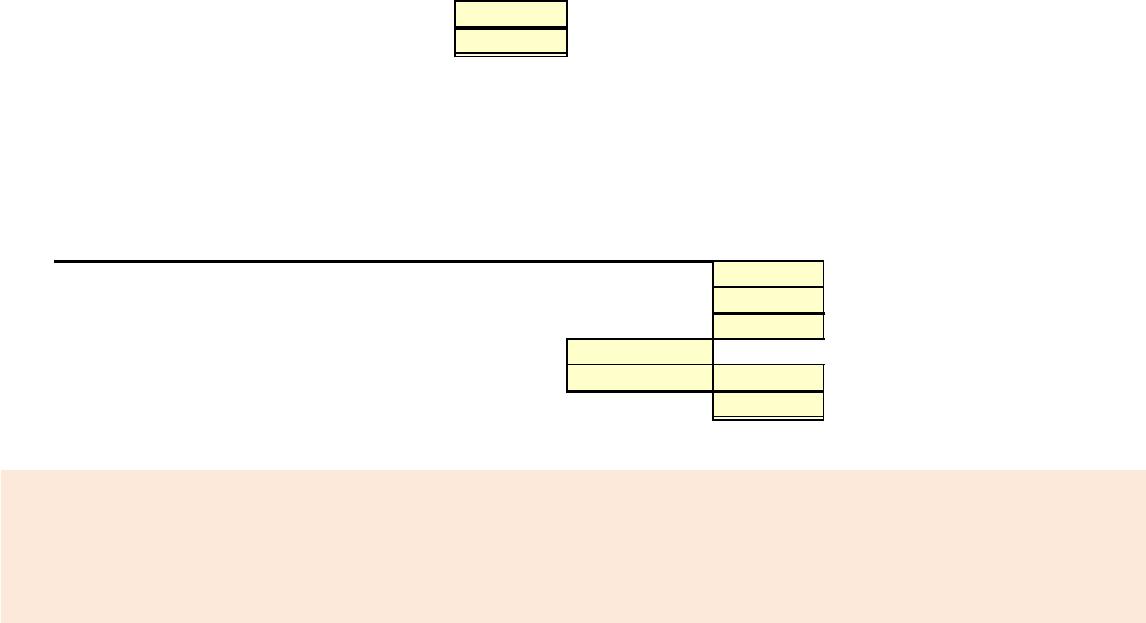

(a) Determine the inn’s break-even point in (1) number of rented rooms per month and

(2) dollars.

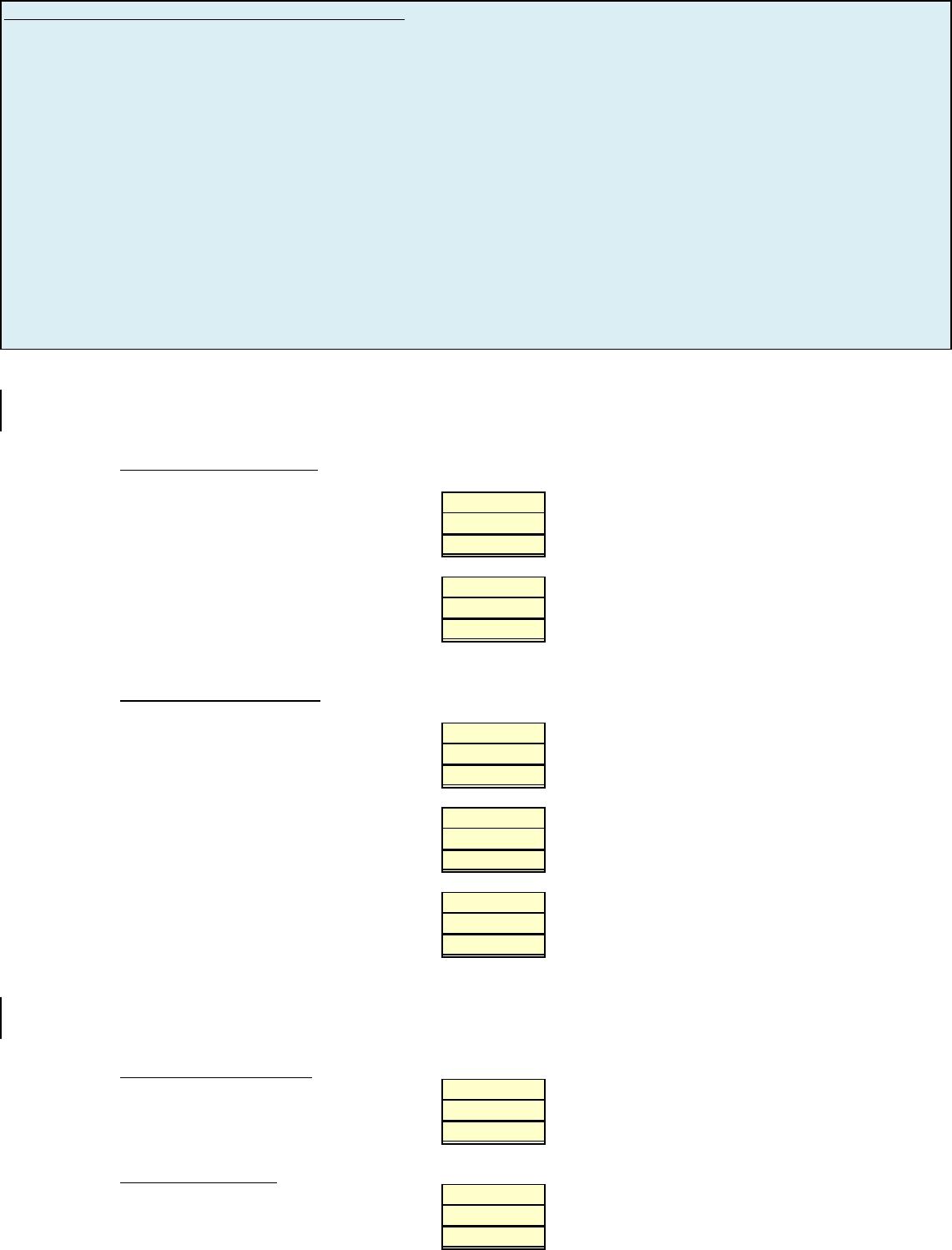

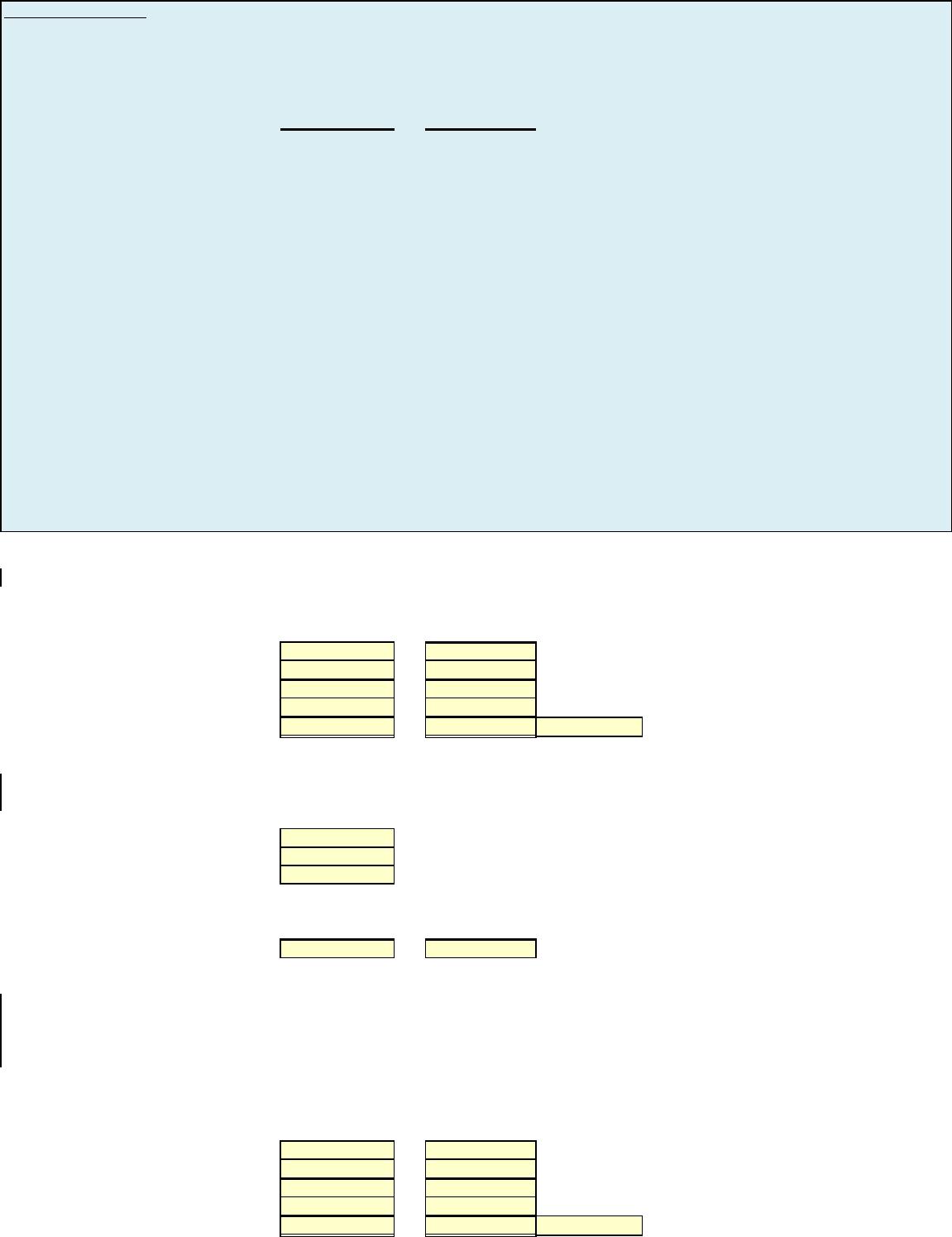

(a)(1) Break-even point in rooms

Rental per room Value

Variable cost per room Value

Contribution margin per room ?

Fixed costs Value

Contribution margin per room Value

Break-even point in rooms ?

(a)(2) Break-even point in dollars

Contribution margin per room Value

Rental per room Value

Contribution margin ratio ?

Break-even point in rooms Value

Rental per room Value

Break-even point in dollars ?

OR

Fixed cost Value

contribution margin ratio Value

Break-even point in dollars ?

(b) If the inn plans on renting an average of 50 rooms per day (assuming a 30-day month),

what is (1) the monthly margin of safety in dollars and (2) the margin of safety ratio?

(b)(1) Margin of safety in dollars

Actual sales Value

Break-even Sales

Value

Margin of safety in dollars ?

(b)(2) Margin of safety ratio

Margin of safety in dollars Value

Actual sales Value

Margin of safety ratio ?

After you have completed E6-1, consider the following additional questions.

1. Assume that the rental rate per room changed to $65 per night. Recalculate break-even point

in units and dollars. Round CM ratio to one decimal point.

2. If the inn plans to rent 60 rooms average per day at the new rate of $65 per night, recalculate the margin

of safety in dollars and the margin of safety ratio.

E6-1 Solution

(a) Determine the inn’s break-even point in (1) number of rented rooms per month and (2) dollars.

(a)(1) Breakeven point in rooms

Rental per room $60

(a)(2) Break-even point in dollars

Contribution margin per room $18

Rental per room $60

(b) If the inn plans on renting an average of 50 rooms per day (assuming a 30-day month),

what is (1) the monthly margin of safety in dollars and (2) the margin of safety ratio?

(b)(1) Margin of safety in dollars

Expected rental revenues $90,000

Break-even Sales $51,000

E6-1 Solution to additional question

1. Assume that the rental rate per room changed to $65 per night. Recalculate break-even point

in units and dollars. Round CM ratio to one decimal point.

(a)(1) Break-even point in rooms

Rental per room $65

Variable cost per room $42

(a)(2) Break-even point in dollars

Contribution margin per room $23

Rental per room $65

2. If the inn plans to rent 60 rooms average per day at the new rate of $65 a night,

recalculate the margin of safety in dollars and the margin of safety ratio.

(a) Margin of safety in dollars

Expected rental revenues $117,000

(b) Margin of safety ratio

Margin of safety in dollars $73,761

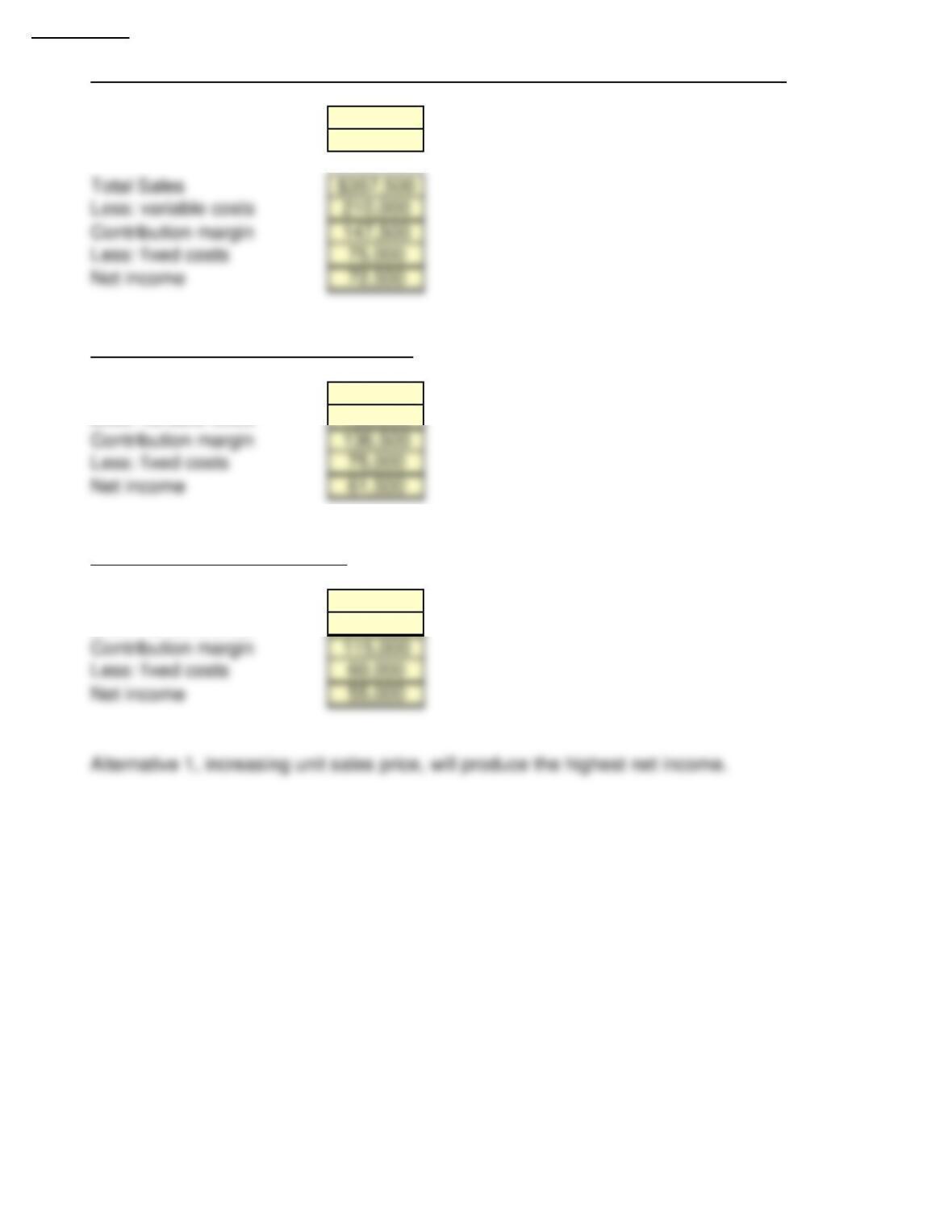

E6-3 Compute net income under different alternatives

Barnes Company reports the following operating results for the month of August: sales $325,000

(units 5,000); variable costs $210,000; and fixed costs $75,000. Management is considering the following

independent courses of action to increase net income.

1. Increase selling price by 10% with no change in total variable costs or sales volume.

2. Reduce variable costs to 58% of sales.

3. Reduce fixed costs by $15,000.

Instructions

Compute the net income to be earned under each alternative. Which course of action will produce the

highest net income?

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

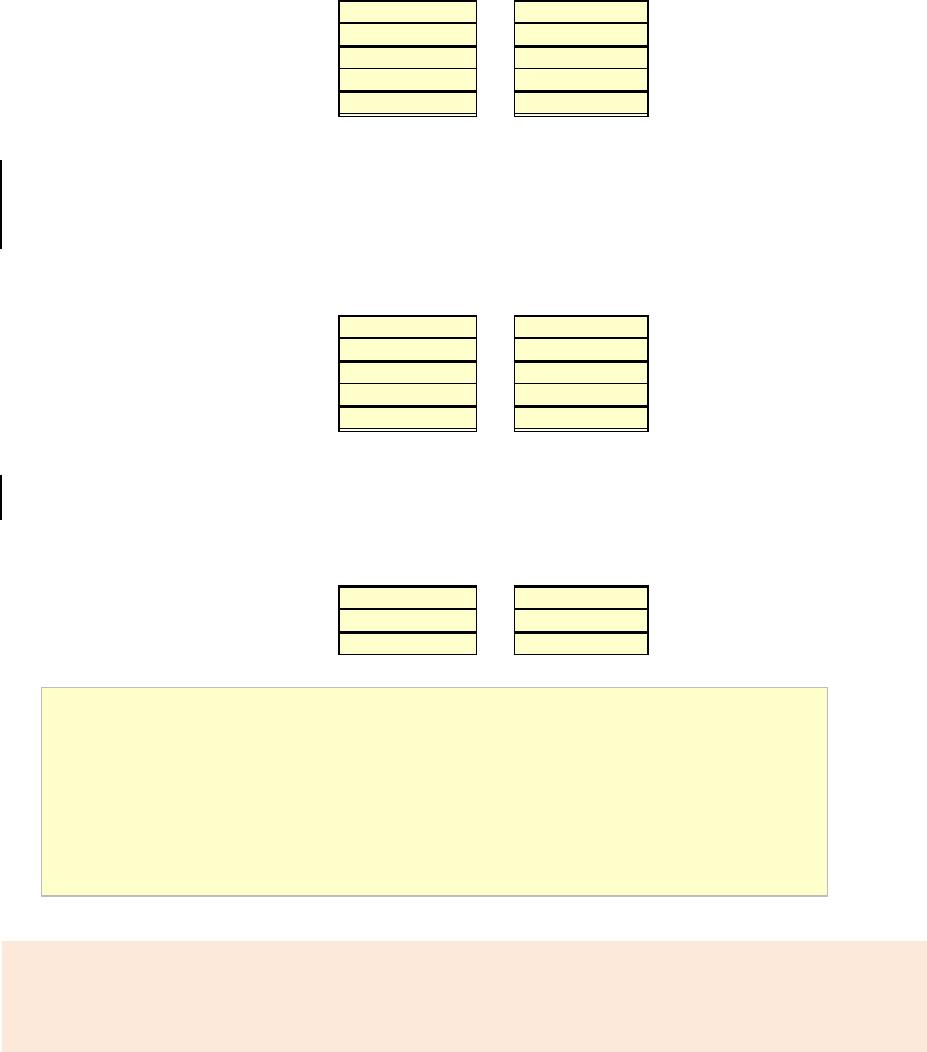

1. Increase selling price by 10% with no change in total variable costs or sales volume.

Current selling price ?

New selling price ?

(Round to nearest cent)

Total sales ?

Less: variable costs ?

Contribution margin ?

Less: fixed costs Value

Net income ?

2. Reduce variable costs to 58% of sales.

Total Sales Value

Less: variable costs Value

Contribution margin ?

Less: fixed costs Value

Net income ?

3. Reduce fixed costs by $15,000.

Total Sales Value

Less: variable costs Value

Contribution margin ?

Less: fixed costs Value

Net income ?

After you have completed E6-3, consider the following additional questions.

1. Assume that unit selling price increased 5% with no change in total variable costs or sales volume.

2.

Assume variable costs decreased to 53% of sales.

3. Assume that fixed costs increased by $20,000.

Which course of action will produce the highest net income?

E3 – Solution

1. Increase selling price by 10% with no change in total variable costs or sales volume.

Current selling price $65

New selling price $71.50

2. Reduce variable costs to 58% of sales.

Total Sales $325,000

Less: variable costs 188,500

3. Reduce fixed costs by $15,000

Total Sales $325,000

Less: variable costs 210,000

E3 – Solution to additional question

1. Assume that unit selling price increased 5% with no change in total variable costs or sales volume.

Current selling price $65

New selling price $68.25

2. Assume variable cost decreased to 53% of sales.

Total Sales $325,000

Less: variable costs 172,250

3. Assume that fixed increased by $20,000.

Total Sales $325,000

Less: variable costs 210,000

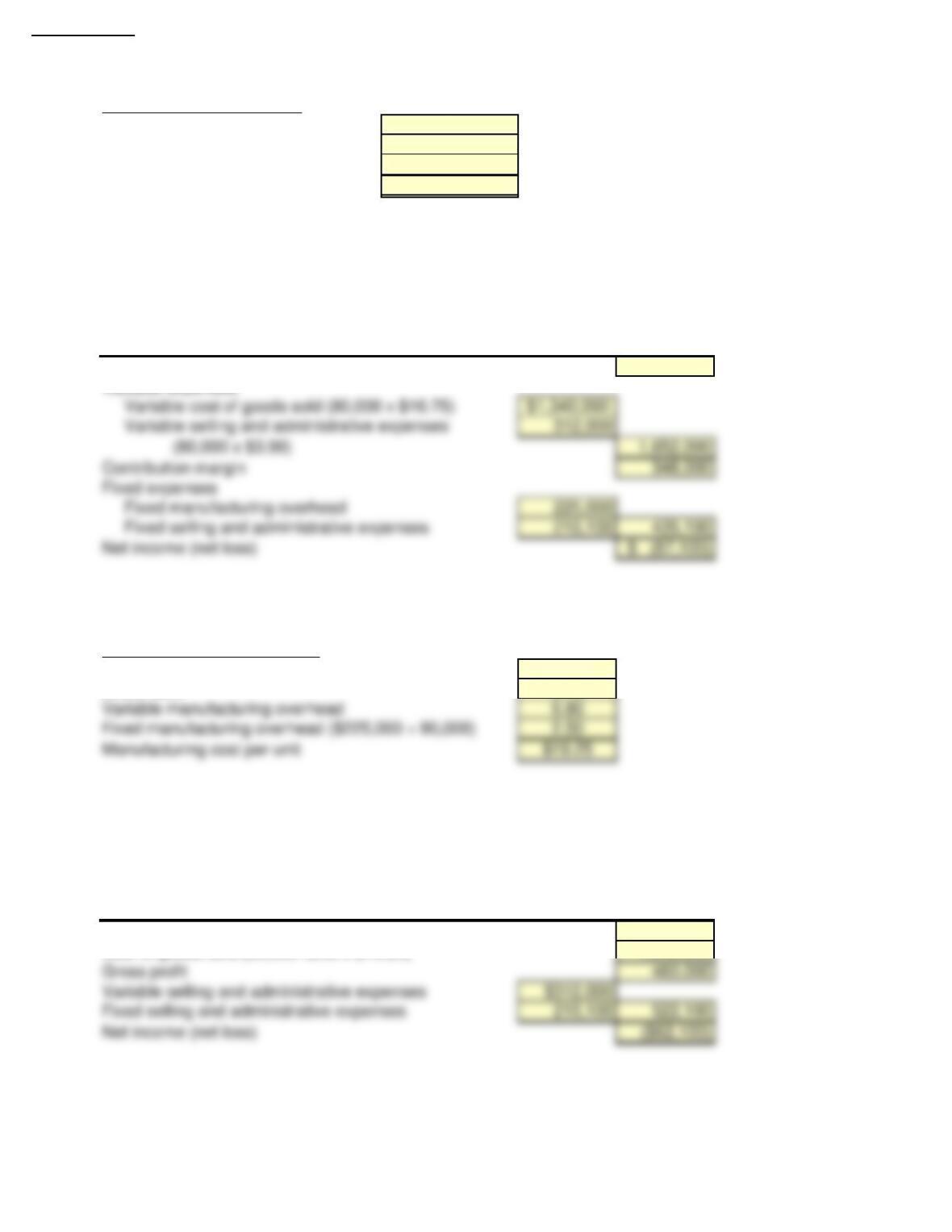

E6-17 Compute product cost and prepare an income statement under variable and absorption costing

Siren Company builds custom fishing lures for sporting goods stores. In its first year of operations, 2017,

the company incurred the following costs.

Variable Costs per Unit

Direct materials $7.50

Direct labor $3.45

Variable manufacturing overhead $5.80

Variable selling and administrative expenses $3.90

Fixed Costs per Year

Fixed manufacturing overhead $225,000

Fixed selling and administrative expenses $210,100

Siren Company sells the fishing lures for $25. During 2017, the company sold 80,000

lures and produced 90,000 lures.

Instructions

(a) Assuming the company uses variable costing, calculate Siren’s manufacturing cost

per unit for 2017.

(b)

Prepare a variable costing income statement for 2017.

(c ) Assuming the company uses absorption costing, calculate Siren’s manufacturing cost

per unit for 2017.

(d) Prepare an absorption costing income statement for 2017.

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

(a) Assuming the company uses variable costing, calculate Siren’s manufacturing cost per unit for 2017.

Unit Cost (Variable costing)

Direct materials Value

Direct labor Value

Variable manufacturing overhead Value

Manufacturing cost per unit ?

(b)

Prepare a variable costing income statement for 2017.

Sales Value

Variable expenses

Variable cost of goods sold Value

Variable selling and administrative expenses Value ?

Contribution margin ?

Fixed expenses

Fixed manufacturing overhead Value

Fixed selling and administrative expenses Value ?

Net income ?

(c ) Assuming the company uses absorption costing, calculate Siren’s manufacturing cost per unit for 2017.

Unit Cost (Absorption costing)

Direct materials Value

Direct labor Value

Variable manufacturing overhead Value

SIREN COMPANY

Income Statement

For the Year Ended December 31, 2017

Variable Costing

Fixed manufacturing overhead Value

Manufacturing cost per unit ?

(d) Prepare an absorption costing income statement for 2017.

Sales Value

Cost of goods sold Value

Gross profit Value

Variable selling and administrative expenses Value

Fixed selling and administrative expenses Value Value

Net income Value

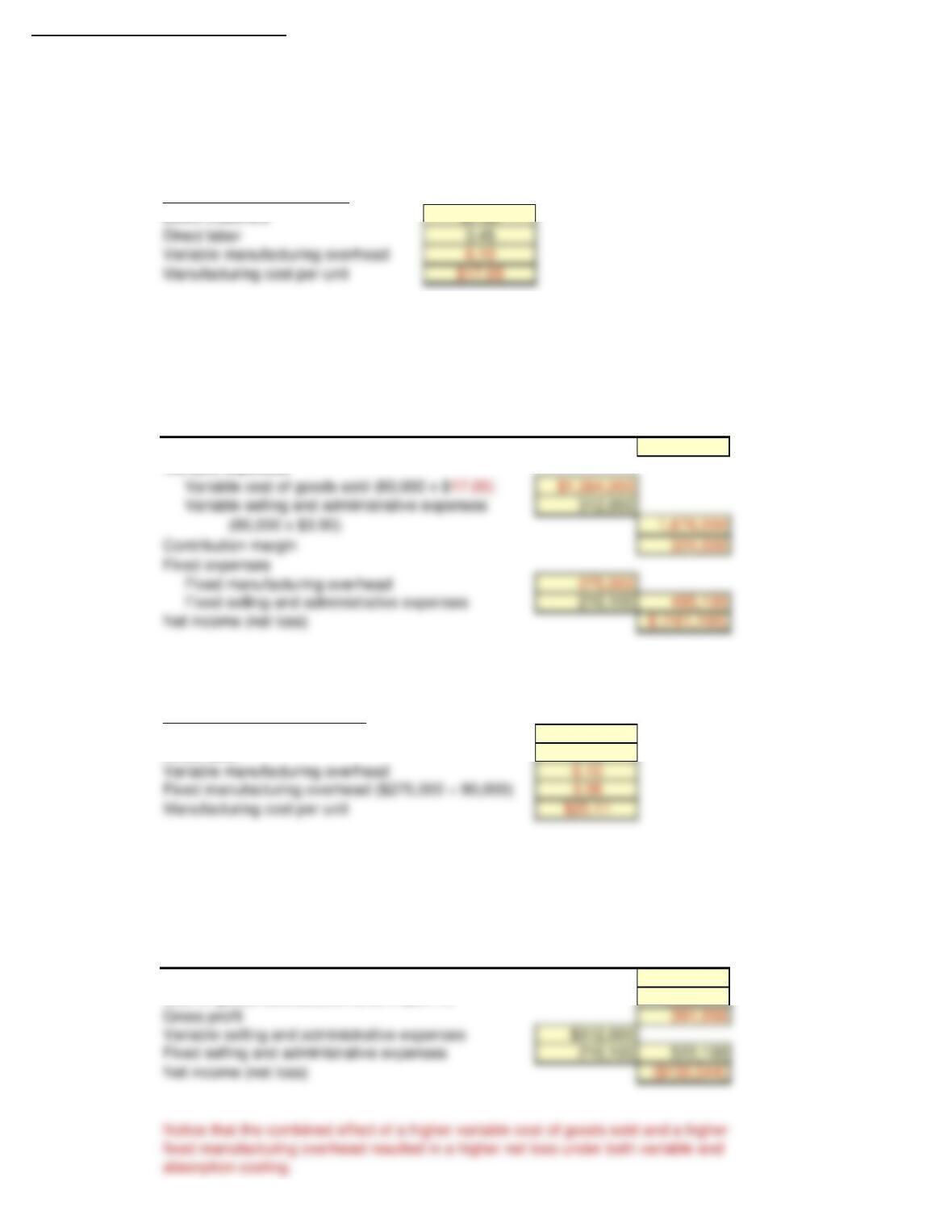

After you have completed E6-17, consider the following additional question.

1. Assume that variable overhead costs changed to $6.10 per unit and total fixed manufacturing overhead

increased to $275,000. What is the impact of these changes on the unit product costs and net income

under variable and absorption costing.

Absorption Costing

SIREN COMPANY

Income Statement

For the Year Ended December 31, 2017

E6-17 Solution

(a) Assuming the company uses variable costing, calculate Siren’s manufacturing cost per unit for 2017.

Unit Cost (Variable costing)

Direct materials $7.50

Direct labor 3.45

Variable manufacturing overhead 5.80

Manufacturing cost per unit $16.75

(b) Prepare a variable costing income statement for 2017.

Sales (80,000 lures x $25) $2,000,000

Variable expenses

(c) Assuming the company uses absorption costing, calculate Siren’s manufacturing cost per unit for 2017.

Unit Cost (Absorption costing)

Direct materials $7.50

Direct labor 3.45

(d) Prepare an absorption costing income statement for 2017.

Sales (80,000 lures x $25) $2,000,000

Cost of goods sold (80,000 lures x $19.25) 1,540,000

Absorption Costing

SIREN COMPANY

Income Statement

For the Year Ended December 31, 2017

SIREN COMPANY

Income Statement

For the Year Ended December 31, 2017

Variable Costing

E6-17 Solution to additional question

1. Assume that variable overhead costs changed to $6.10 per unit and total fixed manufacturing overhead

increased to $275,000. What is the impact of these changes on the unit product costs and net income

under variable and absorption costing.

(a) Assuming the company uses variable costing, calculate Siren’s manufacturing cost per unit for 2017.

Unit Cost (Variable costing)

Direct materials $7.50

(b) Prepare a variable costing income statement for 2017.

Sales (80,000 lures x $25) $2,000,000

Variable expenses

(c ) Assuming the company uses absorption costing, calculate Siren’s manufacturing cost per unit for 2017.

Unit Cost (Absorption costing)

Direct materials $7.50

Direct labor 3.45

(d) Prepare an absorption costing income statement for 2017.

Sales (80,000 lures x $25) $2,000,000

Cost of goods sold (80,000 lures x $20.11) 1,608,444

Income Statement

For the Year Ended December 31, 2017

Absorption Costing

SIREN COMPANY

Income Statement

For the Year Ended December 31, 2017

Variable Costing

SIREN COMPANY

CD6 EXCEL Tutorial

CURRENT DESIGNS

Current Designs manufactures two different types of kayak, rotomolded kayaks and composite kayaks.

The following information is available for each product line.

Rotomolded Composite

Sales price/unit $950 $2,000

Variable costs/unit $570 $1,340

The company‘s fixed costs are $820,000. An analysis of the sales mix identifies that rotomolded kayaks

make up 80% of the total units sold.

Instructions

(a) Determine the weighted-average unit contribution margin for Current Designs.

(b) Determine the break-even points in units for Current Designs and identify how many units of each

type of kayak will be sold at the break-even point. (Round to the nearest whole number.)

(c ) Assume that the sales mix changes, and rotomolded kayaks now make up 70% of total units sold.

Calculate the total number of units that would need to be sold to earn a net income of $2,000,000

and identify how many units of each type of kayak will be sold at this level of income. (Round to the

nearest whole number.)

(d) Assume that Current Designs will have sales of $3,000,000 with two-thirds of the sales dollars in

rotomolded kayaks and one-third of the sales dollars in composite kayaks. Assuming $660,000 of fixed

costs are allocated to the rotomolded kayaks and $160,000 to the composite kayaks, prepare a CVP

income statement for each product line.

(e ) Using the information in part (d), calculate the degree of operating leverage for each product line and

interpret your findings. (Round to two decimal places.)

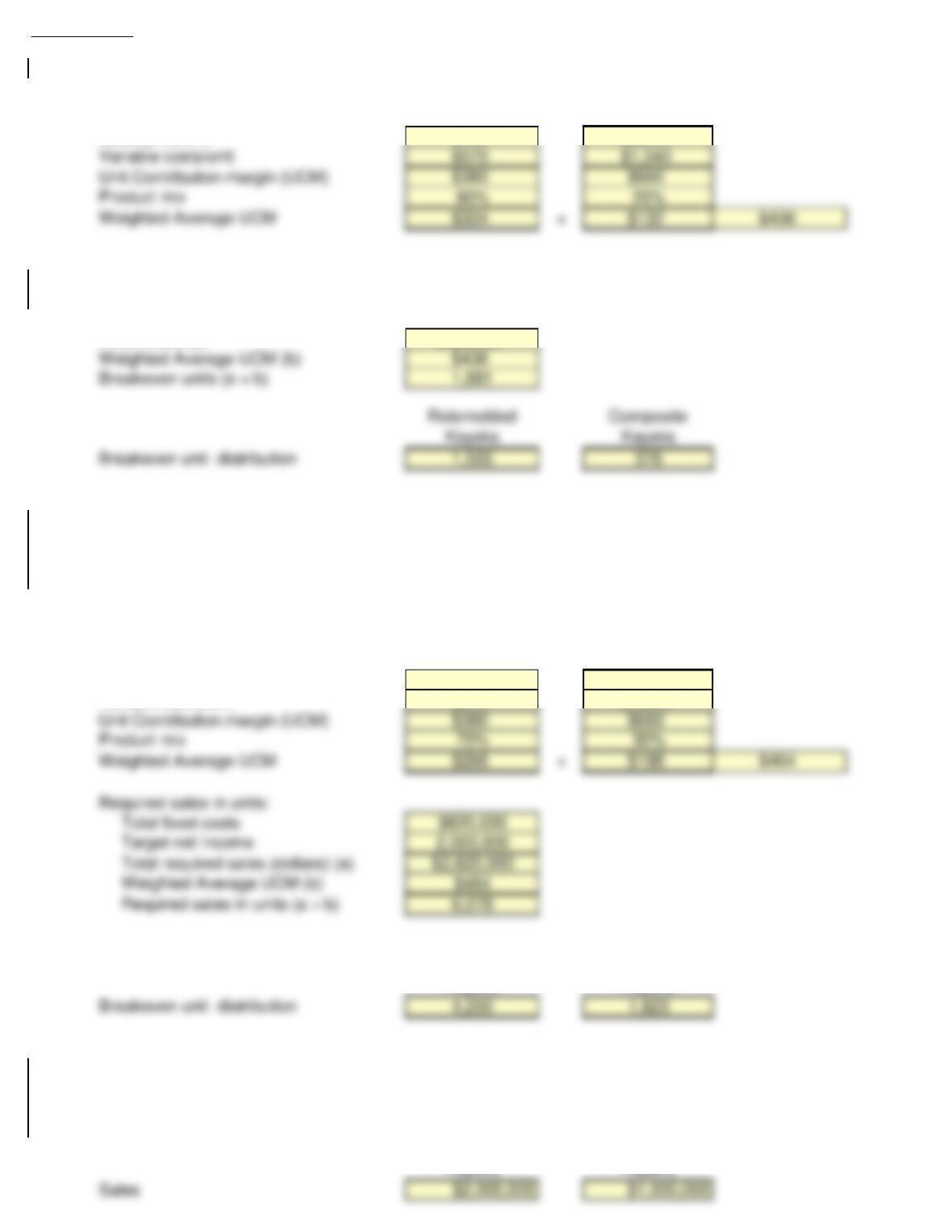

(a) Determine the weighted-average unit contribution margin for Current Designs.

Rotomolded

Kayaks

Composite

Kayaks

Sales price/unit Value Value

Variable costs/unit Value Value

Unit Contribution margin (UCM) ? ?

Product mix Value Value

Weighted Average UCM ? + ? ?

(b) Determine the break-even points in units for Current Designs and identify how many units of each

type of kayak will be sold at the break-even point. (Round to the nearest whole number.)

Fixed costs Value

Weighted Average UCM Value

Breakeven units ?

Rotomolded

Kayaks

Composite

Kayaks

Breakeven unit distribution ? ?

(c ) Assume that the sales mix changes, and rotomolded kayaks now make up 70% of total units sold.

Calculate the total number of units that would need to be sold to earn a net income of $2,000,000

and identify how many units of each type of kayak will be sold at this level of income. (Round to the

nearest whole number.)

Target net income in units:

Rotomolded

Kayaks

Composite

Kayaks

Sales price/unit Value Value

Variable costs/unit Value Value

Unit Contribution margin (UCM) ? ?

Product mix Value Value

Weighted Average UCM ? + ? ?

Required sales in units:

Total fixed costs Value Value

Target net income Value Value

Total required sales (dollars) ? ?

Weighted Average UCM ? ?

Required sales in units ? ?

(d) Assume that Current Designs will have sales of $3,000,000 with two-thirds of the sales dollars in

rotomolded kayaks and one-third of the sales dollars in composite kayaks. Assuming $660,000 of fixed

costs are allocated to the rotomolded kayaks and $160,000 to the composite kayaks, prepare a CVP

income statement for each product line.

Rotomolded

Kayaks

Composite

Kayaks

Sales Value Value

Variable Costs Value Value

Contribution Margin ? ?

Fixed Costs Value Value

Net Income ? ?

(e ) Using the information in part (d), calculate the degree of operating leverage for each product line and

interpret your findings. (Round to two decimal places.)

Rotomolded

Kayaks

Composite

Kayaks

Contribution Margin (a) Value Value

Net Income (b) Value Value

Degree of Operating Leverage (a ÷ b)

? ?

After you have completed CD6, consider the following additional question.

1. Assume that variable cost per unit for the rotomolded kayak and composite kayak changed to $610 and

$1,400 respectively. Show impact of these changes on each of the scenarios provided.

Interpretation of findings:

CD6 Solution

(a) Determine the weighted-average unit contribution margin for Current Designs.

Rotomolded

Kayaks

Composite

Kayaks

Rotomolded

Kayaks

Composite

Kayaks

Sales price/unit $950 $2,000

(b) Determine the break-even points in units for Current Designs and identify how many units of each

type of kayak will be sold at the break-even point. (Round to the nearest whole number.)

Fixed costs (a) $820,000

(c ) Assume that the sales mix changes, and rotomolded kayaks now make up 70% of total units sold.

Calculate the total number of units that would need to be sold to earn a net income of $2,000,000

and identify how many units of each type of kayak will be sold at this level of income. (Round to the

nearest whole number.)

Target net income in units:

Rotomolded

Kayaks

Composite

Kayaks

Sales price/unit $950 $2,000

Variable costs/unit $570 $1,340

Rotomolded

Kayaks

Composite

Kayaks

(d) Assume that Current Designs will have sales of $3,000,000 with two-thirds of the sales dollars in

rotomolded kayaks and one-third of the sales dollars in composite kayaks. Assuming $660,000 of fixed

costs are allocated to the rotomolded kayaks and $160,000 to the composite kayaks, prepare a CVP

income statement for each product line.

Rotomolded

Composite

Variable Costs 1,200,000 670,000

Contribution Margin 800,000 330,000

(e ) Using the information in part (d), calculate the degree of operating leverage for each product line and

interpret your findings. (Round to two decimal places.)

Rotomolded

Kayaks

Composite

Kayaks

Contribution Margin (a) $800,000 $330,000

CD6 Solution to additional question

1. Assume that variable cost per unit for the rotomolded kayak and composite kayak changed to $610 and

$1,400 respectively. Show impact of these changes on each of the scenarios provided.

(a) Determine the weighted-average unit contribution margin for Current Designs.

Rotomolded

Kayaks

Composite Kayaks

Sales price/unit $950 $2,000

(b) Determine the break-even points in units for Current Designs and identify how many units of each

type of kayak will be sold at the break-even point. (Round to the nearest whole number.)

Fixed costs (a) $820,000

Rotomolded

Kayaks

Composite Kayaks

Breakeven unit distribution 1,673 418

(c ) Assume that the sales mix changes, and rotomolded kayaks now make up 70% of total units sold.

Calculate the total number of units that would need to be sold to earn a net income of $2,000,000

and identify how many units of each type of kayak will be sold at this level of income. (Round to the

nearest whole number.)

Target net income in units:

Rotomolded

Kayaks

Composite Kayaks

Rotomolded

Kayaks

Composite Kayaks

Sales price/unit $950 $2,000

Variable costs/unit $610 $1,400

Required sales in units:

Total fixed costs $820,000

Target net income $2,000,000

(d) Assume that Current Designs will have sales of $3,000,000 with two-thirds of the sales dollars in

rotomolded kayaks and one-third of the sales dollars in composite kayaks. Assuming $660,000 of fixed

costs are allocated to the rotomolded kayaks and $160,000 to the composite kayaks, prepare a CVP

income statement for each product line.

Rotomolded

Kayaks

Composite Kayaks

Sales $2,000,000 $1,000,000

Variable Costs $1,284,211 $700,000

(e ) Using the information in part (d), calculate the degree of operating leverage for each product line and

interpret your findings. (Round to two decimal places.)

Rotomolded

Kayaks

Composite Kayaks