1. Merchandising businesses acquire merchandise for resale to customers. It is the selling of

merchandise, instead of providing a service, that makes the activities of a merchandising

b

usiness different from the activities of a service business.

4. a. 1% discount allowed if paid within 15 days of date of invoice; entire amount of invoice

due within 60 days of date of invoice.

b. Payment due within 30 days of date of invoice with no discount.

c. Payment due by the end of the month in which the sale was made with no discount.

5. Sales to customers who use MasterCard or VISA cards are recorded as cash sales.

b

p

8. Sales, Cost of Merchandise Sold, Merchandise Inventory

9. Cost of Merchandise Sold would be debited; Merchandise Inventory would be credited.

10. Loss from Merchandise Inventory Shrinkage would be debited.

CHAPTER 6

ACCOUNTING FOR MERCHANDISING BUSINESSES

DISCUSSION QUESTIONS

CHAPTER 6 Accounting for Merchandising Businesses

PE 6-1A

a. $771,800 ($366,100 + $1,420,000 – $1,014,300)

PE 6-2B

a. $74,448. Purchase of $84,150 [$85,000 – ($85,000 × 1%)] less the return of

$9,702 [$9,800 – ($9,800 × 1%)]

b. Accounts Payable

PE 6-3A

a. Accounts Receivable [$94,800 – ($94,800 × 2%)] 92,904

Sales 92,904

Cost of Merchandise Sold 56,900

Merchandise Inventory 56,900

PRACTICE EXERCISES

CHAPTER 6 Accounting for Merchandising Businesses

PE 6-3B

a. Accounts Receivable [$78,600 – ($78,600 × 1%)] 77,814

Sales 77,814

Cost of Merchandise Sold 47,200

Merchandise Inventory 47,200

PE 6-4A

a. $100,993. Purchase of $119,592 [$120,800 – ($120,800 × 1%)] less return of

$19,899 [($20,100 – ($20,100 × 1%)] plus $1,300 of shipping.

PE 6-4B

a. $51,579. Purchase of $58,014 [$58,600 – ($58,600 × 1%)] less return of

$6,435 [($6,500 – ($6,500 × 1%)].

CHAPTER 6 Accounting for Merchandising Businesses

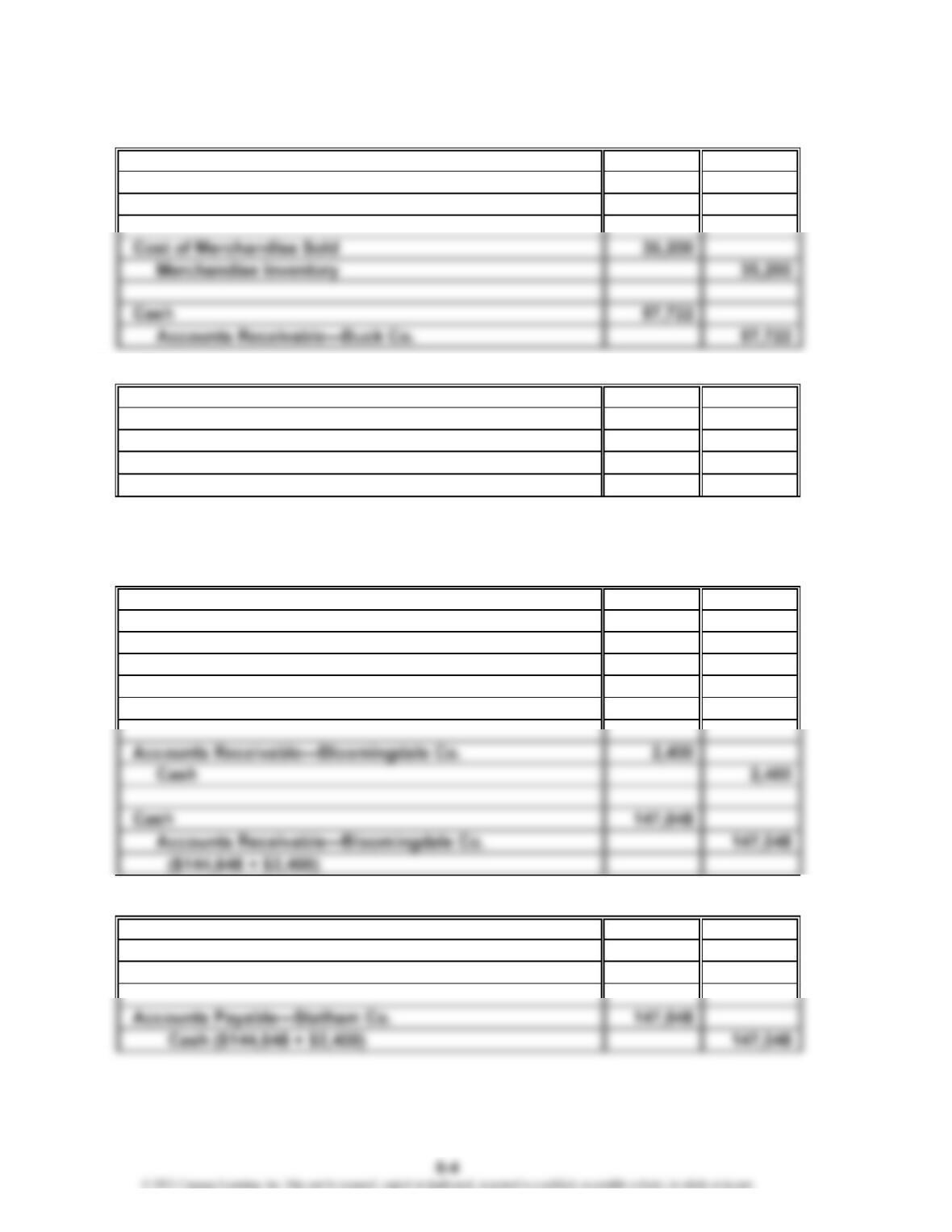

PE 6-5A

Sally Co. journal entries:

Accounts Receivable—Buck Co. 57,722

Sales 57,722

[$58,900 – ($58,900 × 2%)]

Buck Co. journal entries:

Merchandise Inventory [$58,900 – ($58,900 × 2%)] 57,722

Accounts Payable—Sally Co. 57,722

Accounts Payable—Sally Co. 57,722

Cash 57,722

PE 6-5B

Statham Co. journal entries:

Accounts Receivable—Bloomingdale Co. 144,648

Sales 144,648

[$147,600 – ($147,600 × 2%)]

Cost of Merchandise Sold 88,600

Merchandise Inventory 88,600

Bloomingdale Co. journal entries:

Merchandise Inventory 147,048

Accounts Payable—Statham Co. 147,048

[$147,600 – ($147,600 × 2%)] + $2,400

CHAPTER 6 Accounting for Merchandising Businesses

PE 6-6A

Nov. 30 Cost of Merchandise Sold 13,000

PE 6-6B

Dec. 31 Cost of Merchandise Sold 19,700

PE 6-7A

Sales ($3,600,000 × 0.008) 28,800

Customer Refunds Payable 28,800

PE 6-7B

PE 6-8A

a. 20Y3 20Y2

Asset turnover 3.3 3.4

*

$2,310,000 ÷ [($680,000 + $720,000) ÷ 2]

**

$2,278,000 ÷ [($660,000 + $680,000) ÷ 2]

PE 6-8B

a. 20Y3 20Y2

Asset turnove

r

2.6 2.4

*

$663,000 ÷ [($240,000 + $270,000) ÷ 2]

**

$516,000 ÷ [($190,000 + $240,000) ÷ 2]

***

***

CHAPTER 6 Accounting for Merchandising Businesses

Ex. 6-1

a. $12,843,600 ($45,870,000 – $33,026,400)

Ex. 6-2

$32,918 million ($42,879 million – $9,961 million)

Ex. 6-3

Balance Sheet Accounts Income Statement Accounts

100 Assets 400 Revenues

110 Cash 410 Sales

112 Accounts Receivable 500 Expenses

114 Merchandise Inventory 510 Cost of Merchandise Sold

123 Store Equipment 523 Store Supplies Expense

124 Accumulated Depreciation— 524 Delivery Expense

Store Equipment 529 Miscellaneous Selling

125 Office Equipment Expense

126 Accumulated Depreciation— 530 Office Salaries Expense

Office Equipment 531 Rent Expense

Note: The order and number of some of the accounts within subclassifications is

somewhat arbitrary, as in accounts 115–117, accounts 210–213, accounts 520–524,

EXERCISES

CHAPTER 6 Accounting for Merchandising Businesses

Ex. 6-4

a. $67,320. Purchase of $83,160 [$84,000 – ($84,000 × 1%)], less return of $15,840

[$16,000 – ($16,000 × 1%)]

b. Merchandise Inventory

Ex. 6-5

The offer of Supplier Two is lower than the offer of Supplier One. Details are as follows:

Supplier One Supplier Two

List price $20,000 $19,500

Ex. 6-6

(1) Purchased merchandise on account at a cost of $39,200, which is $40,000 less

the 2% discount of $800.

(2) Paid freight, $450.

Ex. 6-7

a. Merchandise Inventory [$53,000 – ($53,000 × 2%)] 51,940

Accounts Payable 51,940

CHAPTER 6 Accounting for Merchandising Businesses

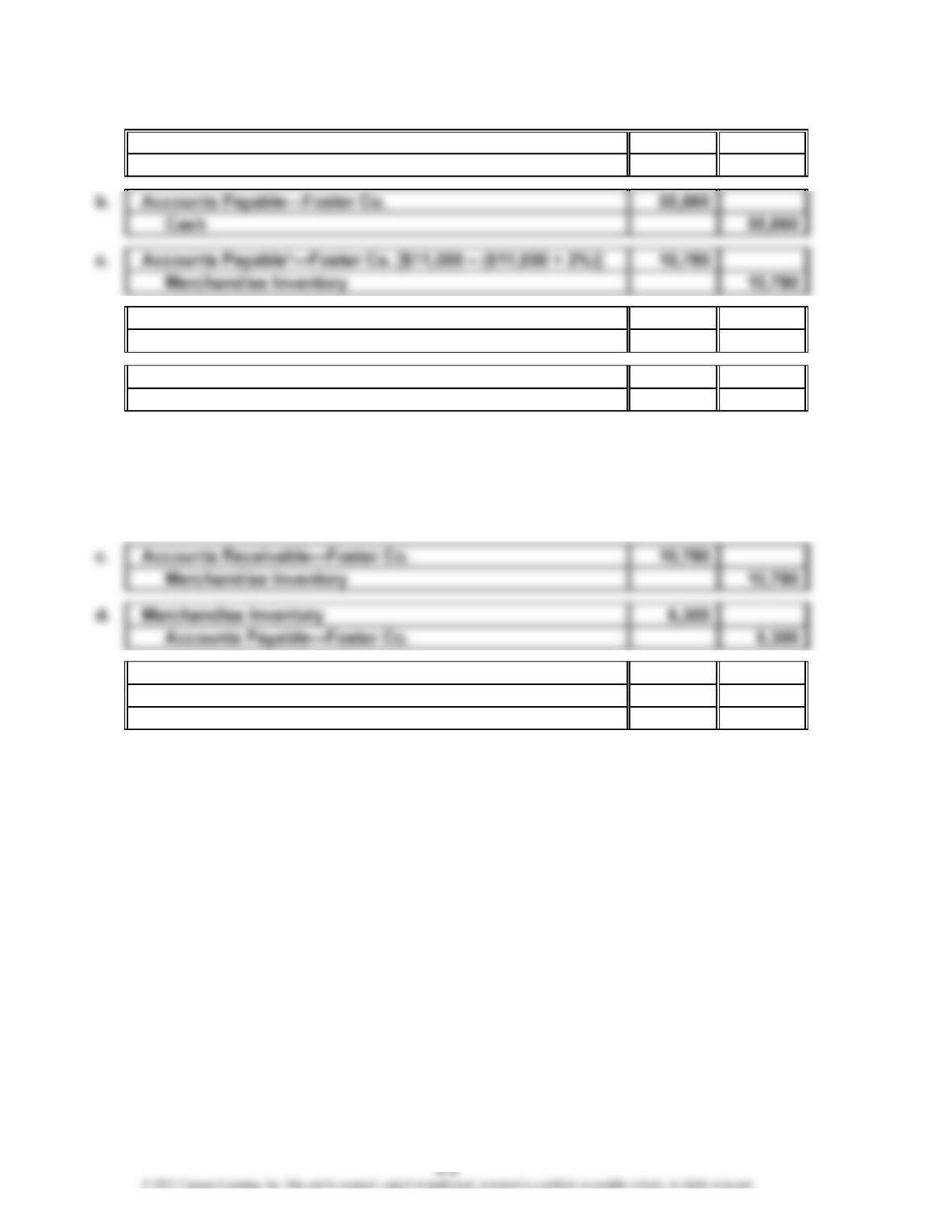

Ex. 6-8

a. Merchandise Inventory [$57,000 – ($57,000 × 2%)] 55,860

Accounts Payable—Foster Co. 55,860

d. Merchandise Inventory 6,300

Accounts Payable—Foster Co. 6,300

e. Cash 4,480

Accounts Payable—Foster Co. 4,480

*Note: The debit of $10,780 to Accounts Payable in entry (c) is the amount of refund due from

Foster Co. It is computed as the amount that was paid for the returned merchandise, $11,000,

less the purchase discount of $220 ($11,000 × 2%). The credit to Accounts Payable of $6,300

in entry (d) reduces the debit balance in the account payable to $4,480, which is the amount of

the cash refund in entry (e). The alternative entries below yield the same final results.

e. Cash 4,480

Accounts Payable—Foster Co. 6,300

Accounts Receivable—Foster Co. 10,780

CHAPTER 6 Accounting for Merchandising Businesses

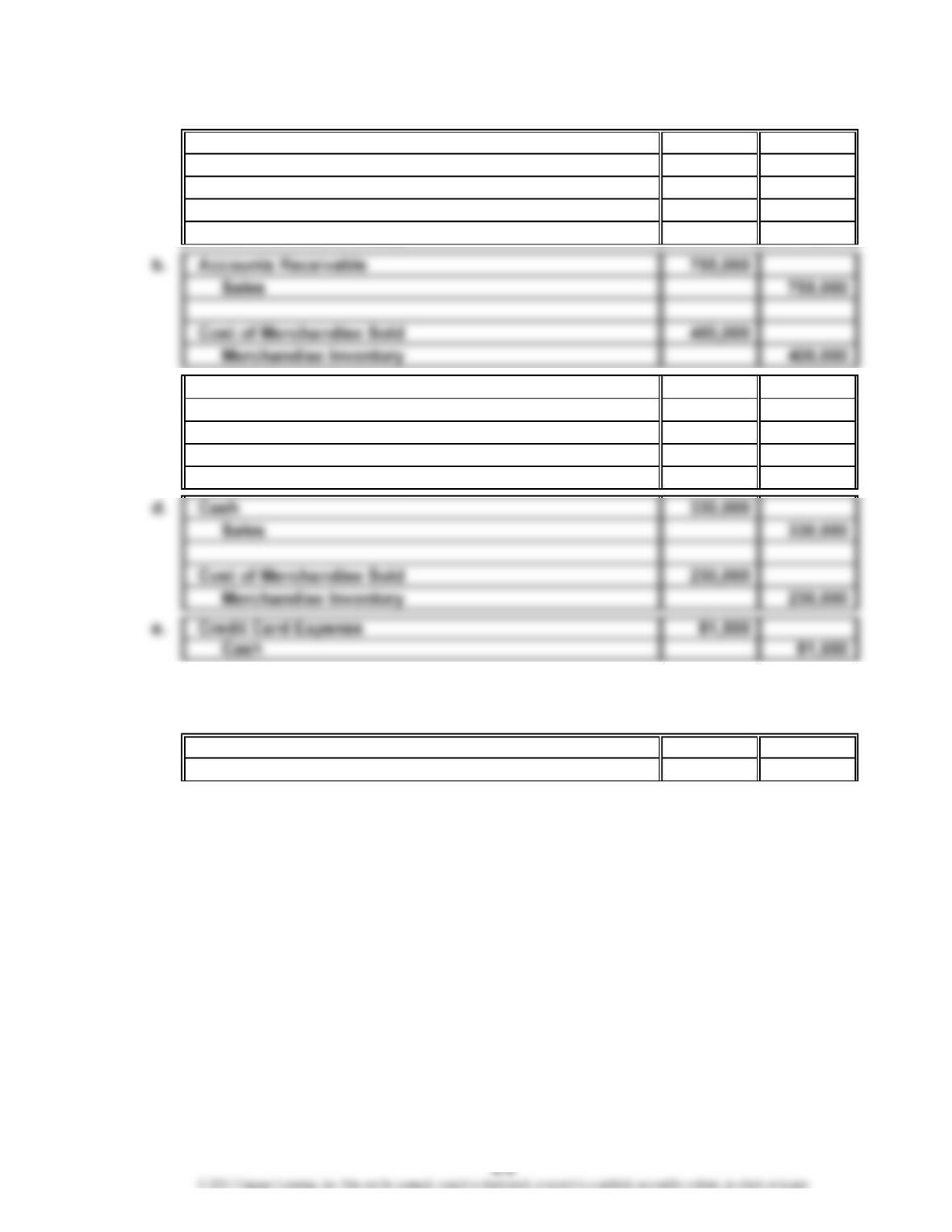

Ex. 6-9

a. Cash 116,300

Sales 116,300

Cost of Merchandise Sold 72,000

Merchandise Inventory 72,000

c. Cash 1,950,000

Sales 1,950,000

Cost of Merchandise Sold 1,250,000

Merchandise Inventory 1,250,000

Ex. 6-10

Customer Refunds Payable 3,000

Cash 3,000

CHAPTER 6 Accounting for Merchandising Businesses

Ex. 6-11

(1) Sold merchandise on account for $14,850, $15,000 less discount of 1%.

(2) Recorded the cost of the merchandise sold and reduced the merchandise

inventory account, $8,800.

Ex. 6-12

a. $55,370 [$56,500 – ($56,500 × 2%)]

b. $57,470 ($55,370 + $2,100)

c.

Ex. 6-13

a. $15,700 ($20,500 – $4,800)

b. $25,256 [($31,100 – $5,900) – ($25,200 × 2%) + $560]

e. $41,778 [$42,200 – ($42,200 × 1%)]

Ex. 6-14

a. Accounts Receivable—Balboa Co. 254,500

Sales 254,500

Cost of Merchandise Sold 152,700

Merchandise Inventory 152,700

$57,470

CHAPTER 6 Accounting for Merchandising Businesses

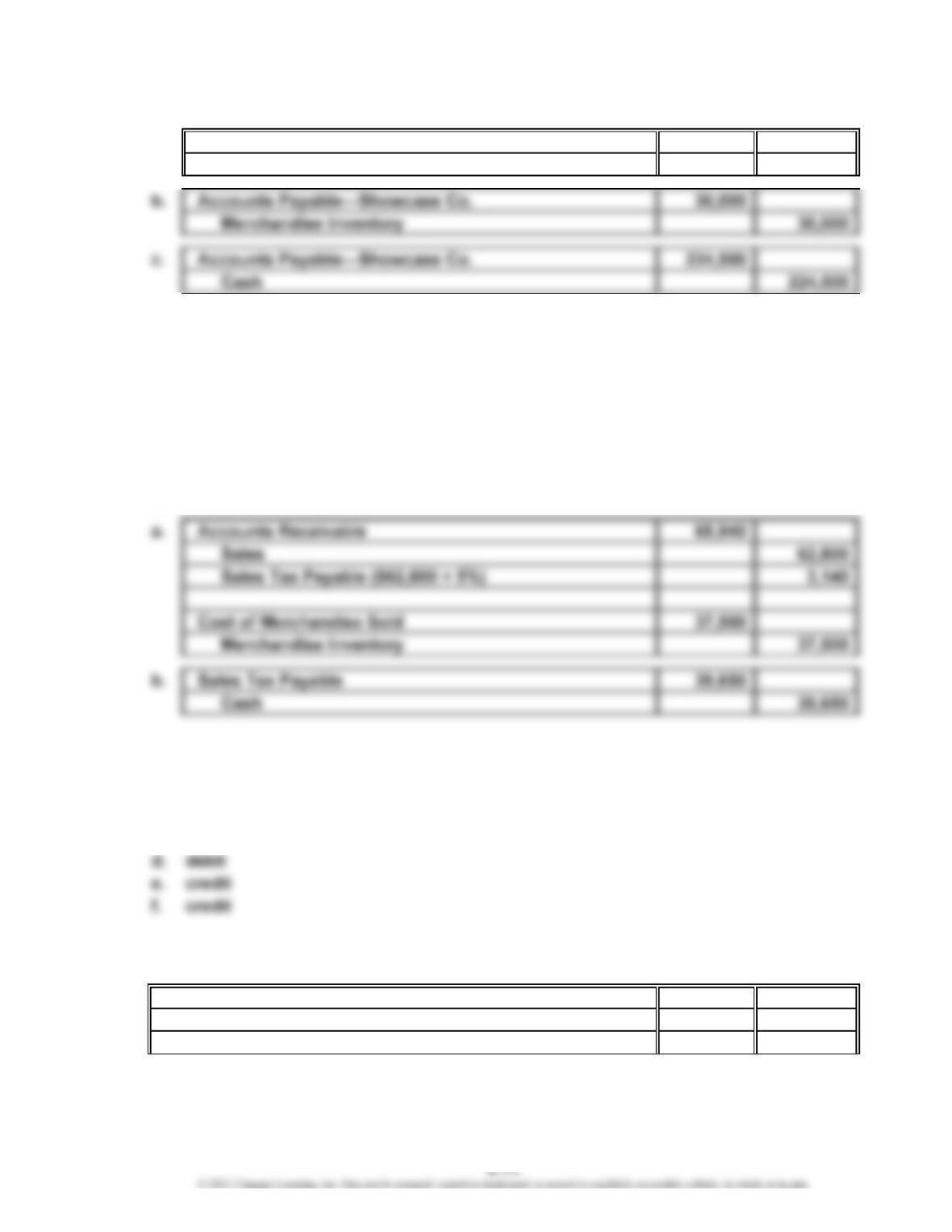

Ex. 6-15

a. Merchandise Inventory 254,500

Accounts Payable—Showcase Co. 254,500

Ex. 6-16

a. At the time of sale

b. $36,000

c. $38,880 [$36,000 + ($36,000 × 8%)]

d. Sales Tax Payable

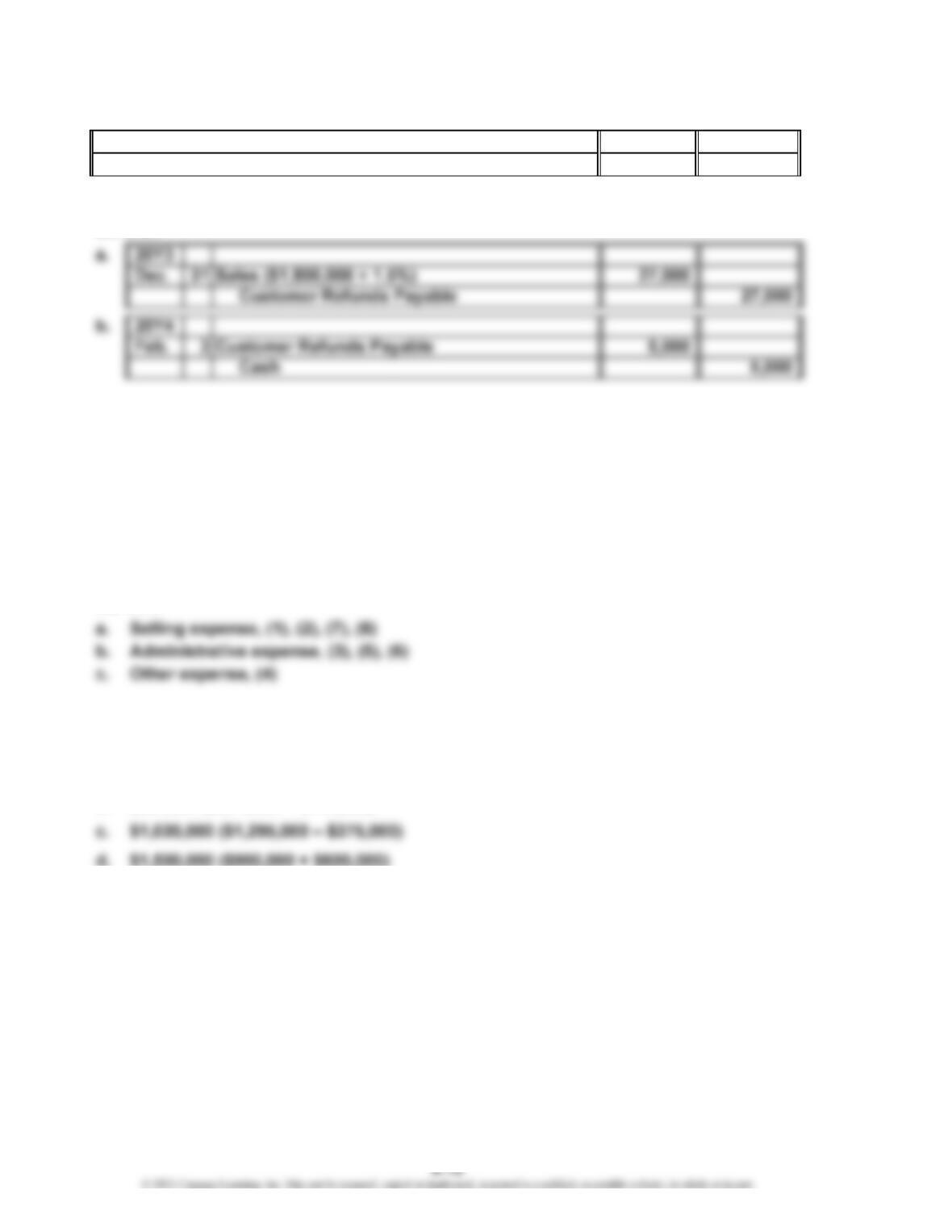

Ex. 6-17

Ex. 6-18

a. debit

b. credit

c. debit

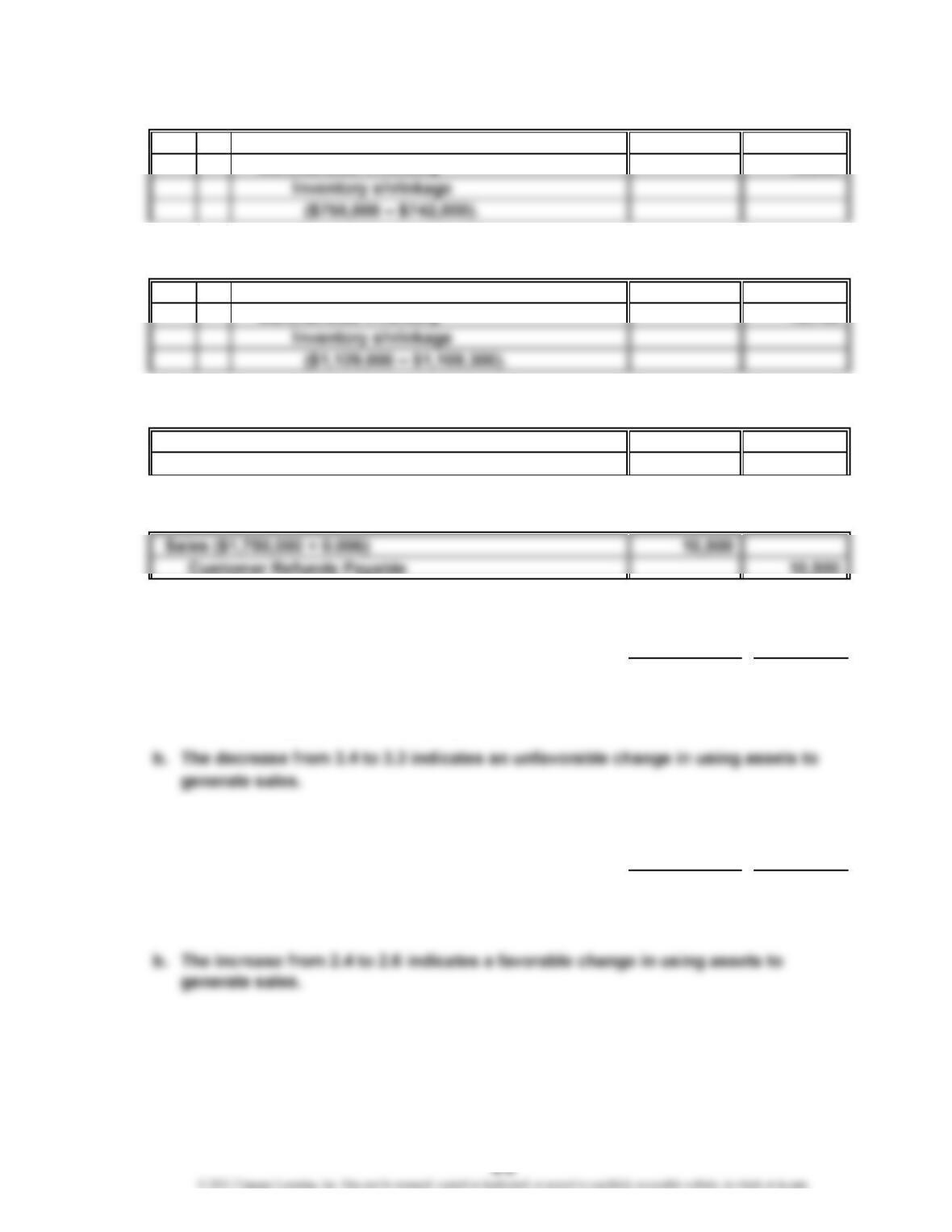

Ex. 6-19

Cost of Merchandise Sold 45,200

Merchandise Inventory 45,200

Inventory shrinkage ($2,780,000 – $2,734,800).

CHAPTER 6 Accounting for Merchandising Businesses

Ex. 6-20

Sales ($51,600,000 × 1.2%) 619,200

Customer Refunds Payable 619,200

Ex. 6-21

Ex. 6-22

a. Gross profit: $76,550,000 ($191,350,000 – $114,800,000)

b. No. There could be other revenue and expense items that affect the amount

of net income.

c. Customer Refunds Payable is a liability account with a normal credit balance.

Ex. 6-23

Ex. 6-24

a. $379,900 ($463,400 – $83,500)

b. $687,500 ($277,500 + $410,000)

d. $1,500,000 ($900,000 + $600,000)

CHAPTER 6 Accounting for Merchandising Businesses

Ex. 6-25

a.

Sales $3,582,000

Cost of merchandise sold 2,123,000

Gross profit $1,459,000

Expenses:

Selling expenses $400,000

Administrative expenses 302,000

Total expenses 702,000

Danns Furnishings Company

Income Statement

For the Year Ended March 31, 20Y4

CHAPTER 6 Accounting for Merchandising Businesses

Ex. 6-26

1. Deducting the cost of merchandise sold from sales yields gross profit (not income

from operations).

2. Deducting the total expenses from gross profit yields income from operations

(or operating income).

A corrected income statement is as follows:

Sales $8,595,000

Cost of merchandise sold 6,110,000

Gross profit $2,485,000

Expenses:

Selling expenses $800,000

Administrative expenses 575,000

Ex. 6-27

Revenues:

Sales $9,332,500

Rent revenue 60,000

Total revenues $9,392,500

Custom Wire & Tubing Company

Income Statement

For the Year Ended April 30, 20Y6

Curbstone Company

Income Statement

For the Year Ended August 31, 20Y5

CHAPTER 6 Accounting for Merchandising Businesses

Ex. 6-28

(b) Cost of Merchandise Sold

(d) Delivery Expense

(f) Sales

Ex. 6-29

20Y4

Mar. 31 Sales 3,582,000

Cost of Merchandise Sold 2,123,000

Selling Expenses 400,000

Administrative Expenses 302,000

Ex. 6-30

20Y7

July 31 Sales 1,745,000

Administrative Expenses 534,000

Cost of Merchandise Sold 941,000

Interest Expense 7,000

Selling Expenses 194,000

Store Supplies Expense 25,500

Closing Entries

Closing Entries

CHAPTER 6 Accounting for Merchandising Businesses

Ex. 6-31

a. Year 2: 2.44 {$108,203 ÷ [($44,003 + $44,529) ÷ 2]}

Year 1: 2.31 {$100,904 ÷ [($44,529 + $42,966) ÷ 2]}

Ex. 6-32

a. 3.22 {$121,162 ÷ [($38,118 + $37,197) ÷ 2]}

b. Although Kroger and Tiffany are both retail stores, Tiffany sells jewelry using a

much longer operating cycle than Kroger uses selling groceries. Thus, Kroger is

able to generate $3.22 of sales for every dollar of assets. Tiffany, however, is only

able to generate $0.82 in sales per dollar of assets. This difference is reasonable

when one considers the sales rate for jewelry and the cost of holding jewelry

CHAPTER 6 Accounting for Merchandising Businesses

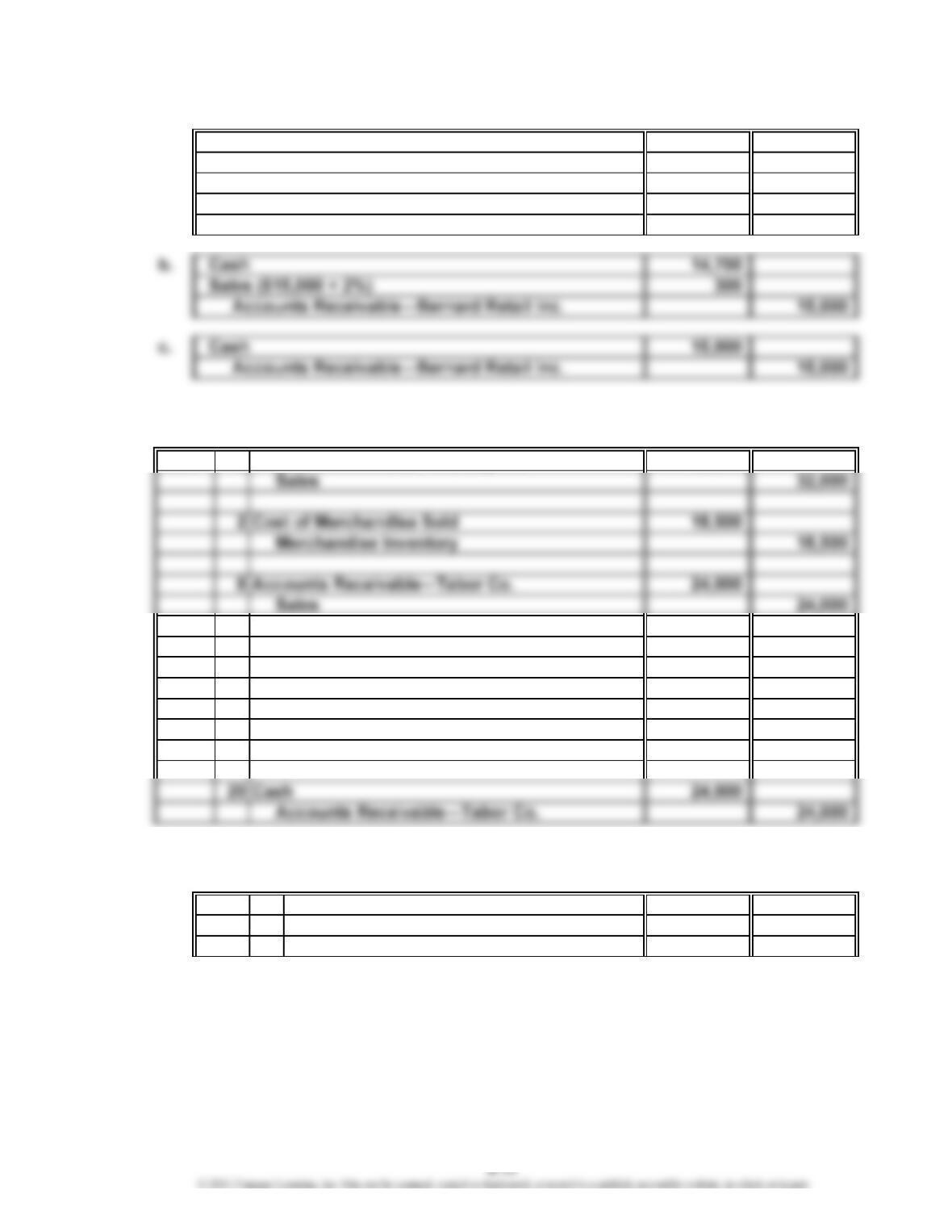

Appendix 1 Ex. 6-33

a. Accounts Receivable—Bernard Retail Inc. 15,000

Sales 15,000

Cost of Merchandise Sold 8,000

Merchandise Inventory 8,000

Appendix 1 Ex. 6-34

Mar. 2 Accounts Receivable—Parsley Co. 32,000

8 Cost of Merchandise Sold 14,400

Merchandise Inventory 14,400

11 Cash 31,680

Sales ($32,000 × 1%) 320

Accounts Receivable—Parsley Co. 32,000

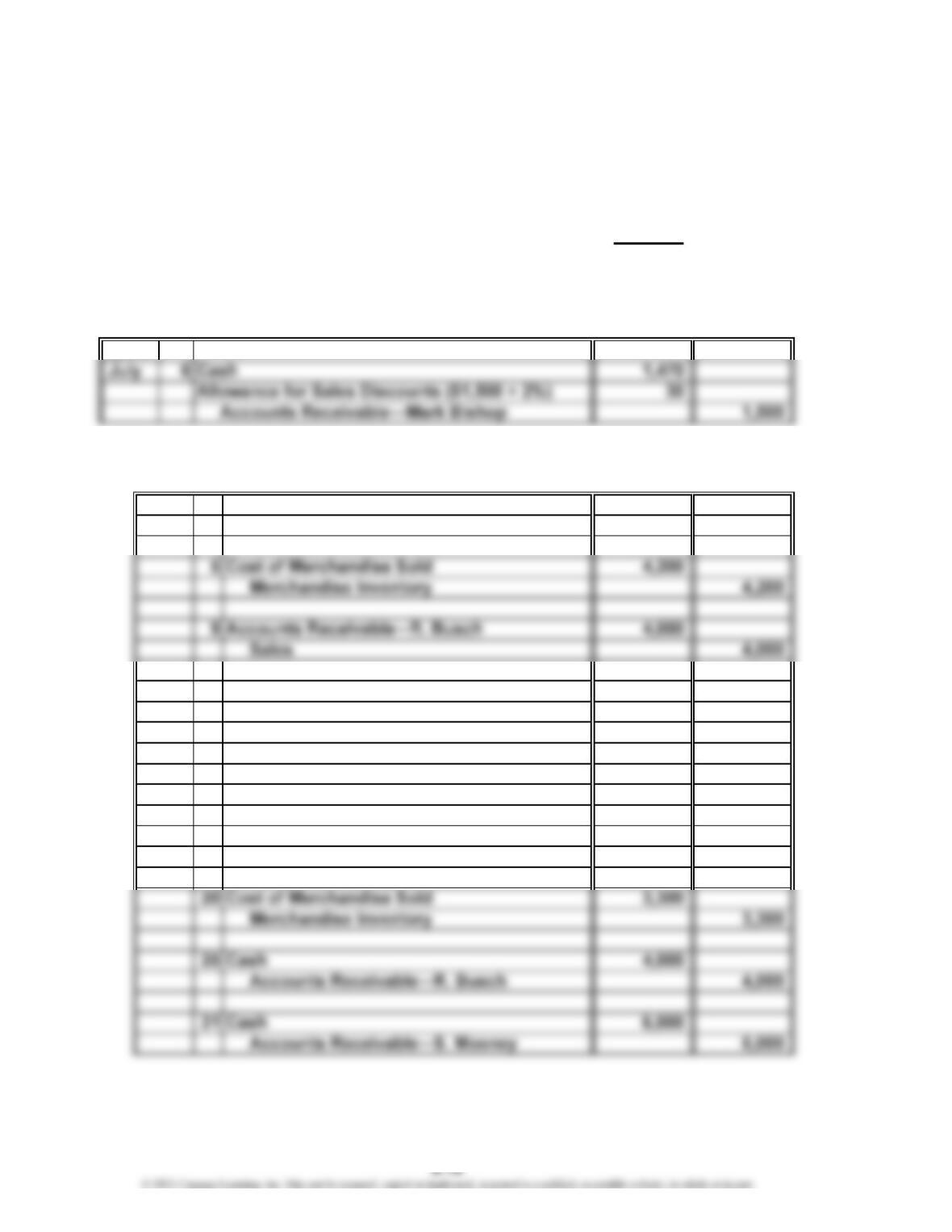

Appendix 1 Ex. 6-35

a. 20Y4

June 30 Sales 7,000

Allowance for Sales Discounts 7,000

CHAPTER 6 Accounting for Merchandising Businesses

Appendix 1 Ex. 6-35 (Concluded)

b. Sales would be reported as $9,993,000 ($10,000,000 − $7,000) on the income

statement. Accounts receivable would be reported as a current asset on the

balance sheet as follows:

Accounts receivable $850,000

Less allowance for sales discounts 7,400

Net accounts receivable $842,600

Appendix 1 Ex. 6-36

20Y4

Appendix 1 Ex. 6-37

a. Aug. 5 Accounts Receivable—M. Quinn 7,500

Sales 7,500

9 Cost of Merchandise Sold 2,100

Merchandise Inventory 2,100

15 Cash 7,350

Sales ($7,500 × 2%) 150

Accounts Receivable—M. Quinn 7,500

20 Accounts Receivable—S. Mooney 6,000

Sales 6,000

CHAPTER 6 Accounting for Merchandising Businesses

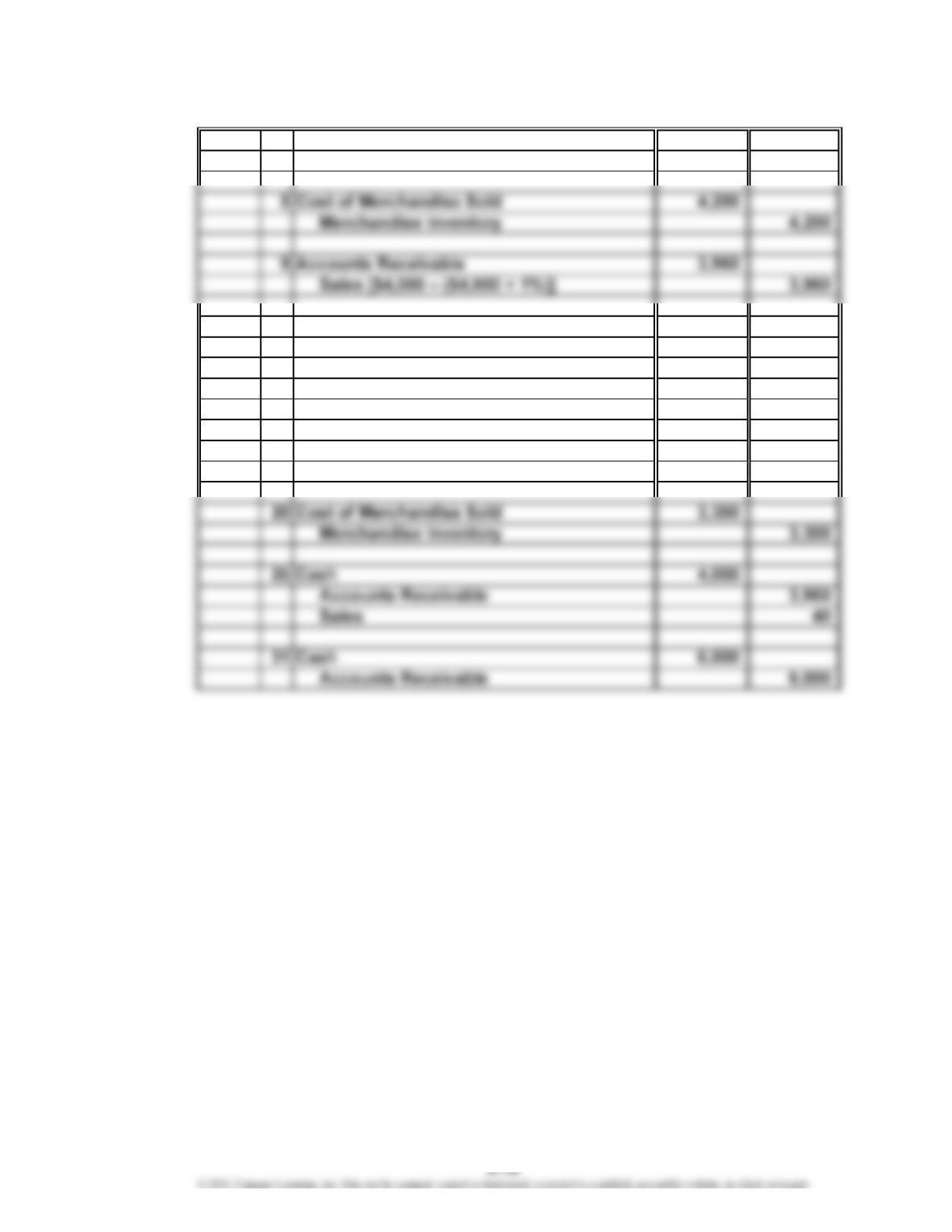

Appendix 1 Ex. 6-37 (Concluded)

b. Aug. 5 Accounts Receivable 7,350

Sales [$7,500 – ($7,500 × 2%)] 7,350

9 Cost of Merchandise Sold 2,100

Merchandise Inventory 2,100

15 Cash 7,350

Accounts Receivable 7,350

20 Accounts Receivable 6,000

Sales 6,000

c. Gross method: $17,350 ($7,500 + $4,000 − $150 + $6,000)

Net method: $17,350 ($7,350 + $3,960 + $6,000 + $40)

d. The gross method requires an end-of-period adjusting entry.

CHAPTER 6 Accounting for Merchandising Businesses

Appendix 2 Ex. 6-38

a. Feb. 18 Accounts Receivable—Brewster Co. 23,520

Sales [$24,000 − ($24,000) × 2%)] 23,520

18 Cost of Merchandise Sold 12,200

Merchandise Inventory 12,200

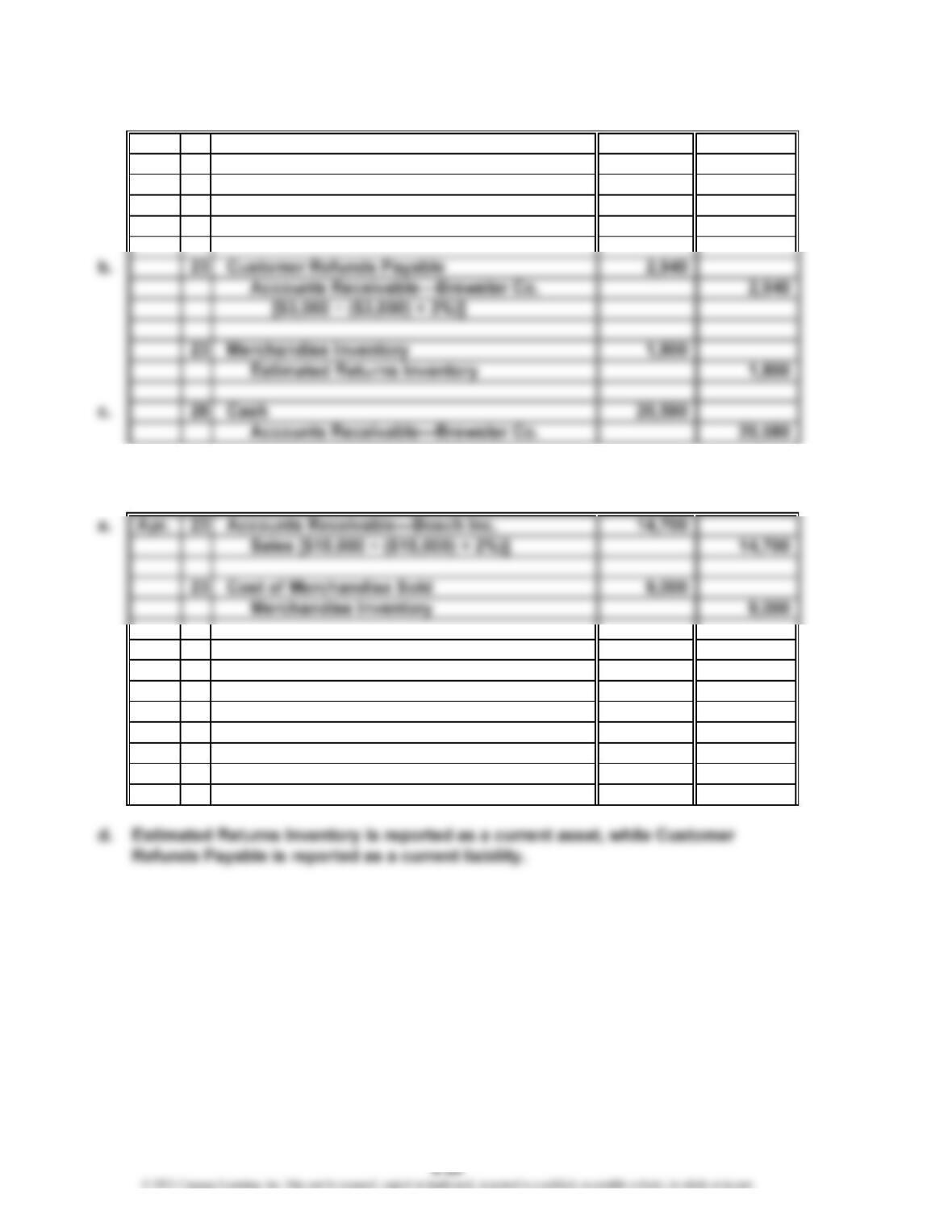

Appendix 2 Ex. 6-39

b. May 2 Cash 14,700

Accounts Receivable—Bosch Inc. 14,700

c. 11 Customer Refunds Payable 2,450

Cash 2,450

11 Merchandise Inventory 1,300

Estimated Returns Inventory 1,300