Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 6

Chapter 6

Inventories and Cost of Sales

QUESTIONS

1. (a) FIFO: The cost of the first (earliest) items purchased in inventory flow to cost of

2. Merchandise inventory is disclosed on the balance sheet as a current asset. It is

3. Incidental costs sometimes are ignored in computing the cost of inventory because

the expense of tracking such costs on a precise basis can outweigh the benefits

4. LIFO will result in the lower cost of goods sold when costs are declining because it

assigns the most recent, lower cost purchases to cost of goods sold.

5. The full-disclosure principle requires that the nature of the accounting change, the

7. No; the consistency concept does not preclude changes in accounting methods

8. Many people make important business decisions based on period-to-period

fluctuations in a company's financial numbers, including gross profit and net

368

9. An inventory error that causes an understatement (or overstatement) for net income

in one accounting period, if not corrected, will cause an overstatement (or

11. The accounting constraint of conservatism guides preparers of accounting reports

to select the less optimistic estimate in uncertain situations where two estimates of

15. Cost of goods available for sale equals ending inventory plus cost of sales. As of

16. Cost of goods available for sale equals ending inventory plus cost of sales. As of

17. Inventory (in KRW millions) comprises 15.1% (computed as ₩18,811,794 / ₩

2014.

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 6

QUICK STUDIES

Quick Study 6-1 (10 minutes)

Units in ending inventory

Units stored in basement ................................

1,300

units

Quick Study 6-2 (10 minutes)

Cost ................................................................

$14,000

Plus

Quick Study 6-3 (10 minutes)

Beginning inventory .....................................

10 units @ $60

$ 600

Plus

Quick Study 6-4 (10 minutes)

FIFO—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

320 @ $3.00

= $ 960.00

Quick Study 6-5 (10 minutes)

LIFO—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

320 @ $3.00

= $ 960.00

371

Quick Study 6-6 (10 minutes)

Weighted Average—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

320 @ $3.00

= $ 960.00

1/9

80 @ $3.20

320 @ $3.00

Quick Study 6-7A (10 minutes)

Ending Cost of

FIFO—Periodic Inventory Goods Sold

FIFO

Quick Study 6-8A (10 minutes)

Ending Cost of

LIFO—Periodic Inventory Goods Sold

LIFO

Quick Study 6-9A (10 minutes)

Ending Cost of

Weighted Average—Periodic Inventory Goods Sold

Quick Study 6-10 (25 minutes)

FIFO—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

12/ 7

10 @ $ 6 = $ 60

10 @ $ 6

= $ 60.00

Quick Study 6-11

LIFO—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

12/7

10 @ $ 6 = $ 60

10 @ $ 6

= $ 60

373

Quick Study 6-12

Weighted Average—Perpetual

Quick Study 6-13

Specific Identification—Perpetual

Quick Study 6-14A (10 minutes)

Ending Cost of

FIFO—Periodic Inventory Goods Sold

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

12/7

10 @ $6 = $60

10 @ $6

= $ 60

374

Quick Study 6-15A (10 minutes)

Ending Cost of

LIFO—Periodic Inventory Goods Sold

LIFO

Quick Study 6-16A (10 minutes)

Ending Cost of

Weighted Average—Periodic Inventory Goods Sold

Quick Study 6-17A (10 minutes)

Ending Cost of

Specific Identification—Periodic Inventory Goods Sold

Specific Identification

Quick Study 6-18 (10 minutes)

Quick Study 6-19 (20 minutes)

Per Unit

Total

Total

LCM -

Items

Inventory Items

Units

Cost

Market

Cost

Market

Mountain bikes

11

$600

$550

$ 6,600

$ 6,050

$ 6,050

Quick Study 6-20 (15 minutes)

a. Overstates 2017 cost of goods sold.

Quick Study 6-21 (10 minutes)

Inventory turnover = Cost of goods sold/Average merchandise inventory

376

Quick Study 6-22B (15 minutes)

Goods available for sale

Inventory, January 1 ................................................................

$190,000

Quick Study 6-23 (10 minutes)

a. Both IFRS and U.S. GAAP provide broad and similar guidance on the

accounting for items and costs making up merchandise inventory.

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 6

377

EXERCISES

Exercise 6-1 (10 minutes)

Exercise 6-2 (10 minutes)

Cost of inventory (estate’s contents)

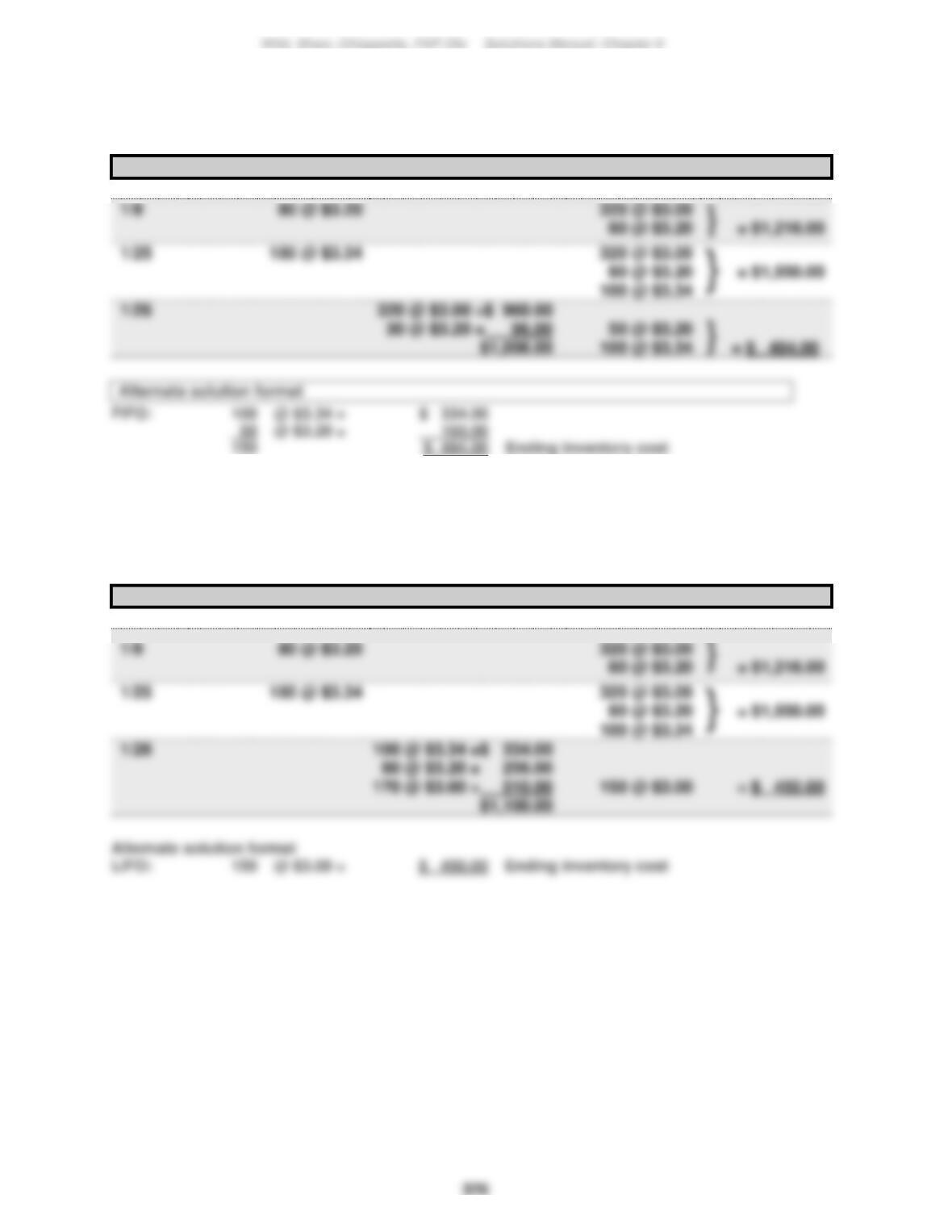

Exercise 6-3 (45 minutes)

a. Specific identification

Ending inventory—180 units from January 30, 5 units from January 20, and 15

units from beginning inventory

Ending Cost of

Specific Identification Inventory Goods Sold

378

Exercise 6-3 (continued)

b. Weighted Average—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

140 @ $6.00

= $ 840.00

c. FIFO—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

140 @ $6.00

= $ 840.00

d. LIFO—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

140 @ $6.00

= $ 840.00

379

Exercise 6-3 (Concluded)

Alternate Solution Format for FIFO and LIFO Perpetual

Ending Cost of

Computations Inventory Goods Sold

c. FIFO

(180 x $4.50) + (20 x $5.00) ............................................... $ 910.00

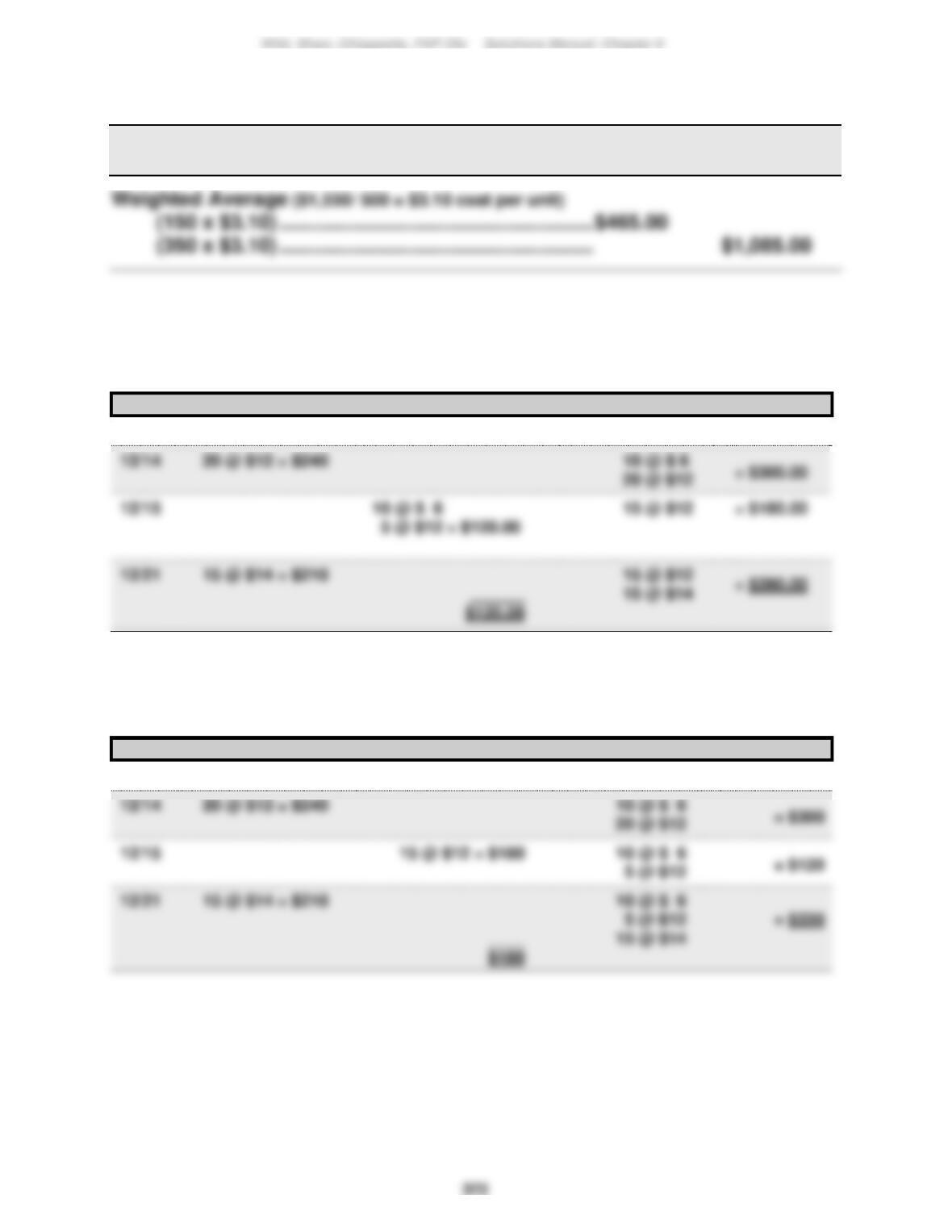

Exercise 6-4 (20 minutes)

LAKER COMPANY

Income Statements

For Month Ended January 31

Specific

Identification

Weighted

Average

FIFO

LIFO

Sales ......................................

$2,700.00

$2,700.00

$2,700.00

$2,700.00

(180 units x $15 price)

380

Exercise 6-5A (35 minutes)

Ending Cost of

Periodic Inventory Computations Inventory Goods Sold

a. Specific Identification—Periodic

b. Weighted Average—Periodic

381

Exercise 6-6 (20 minutes)

LAKER COMPANY

Income Statements

For Month Ended January 31

Specific

Identification

Weighted

Average

FIFO

LIFO

Sales ......................................

$2,700.00

$2,700.00

$2,700.00

$2,700.00

382

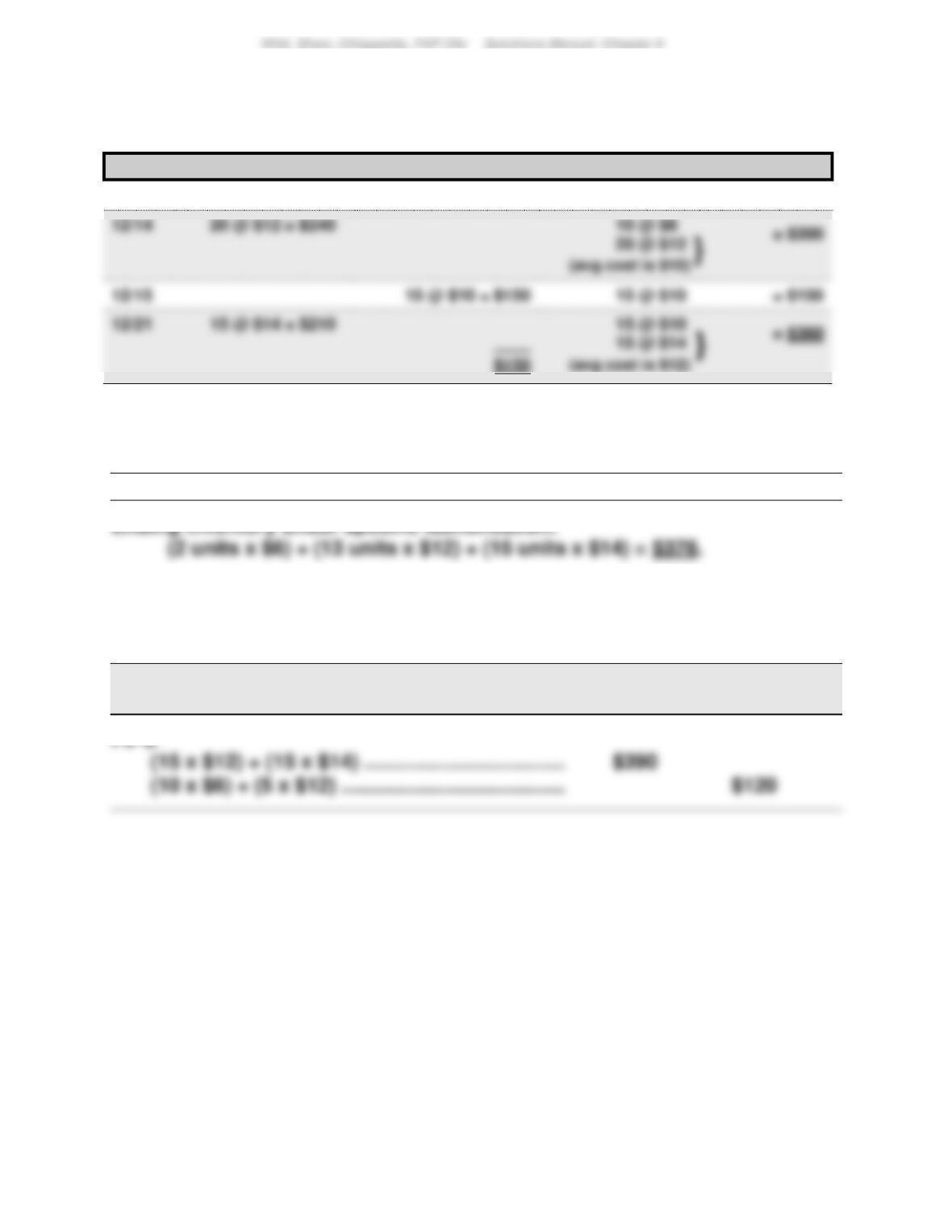

Exercise 6-7 (20 minutes)

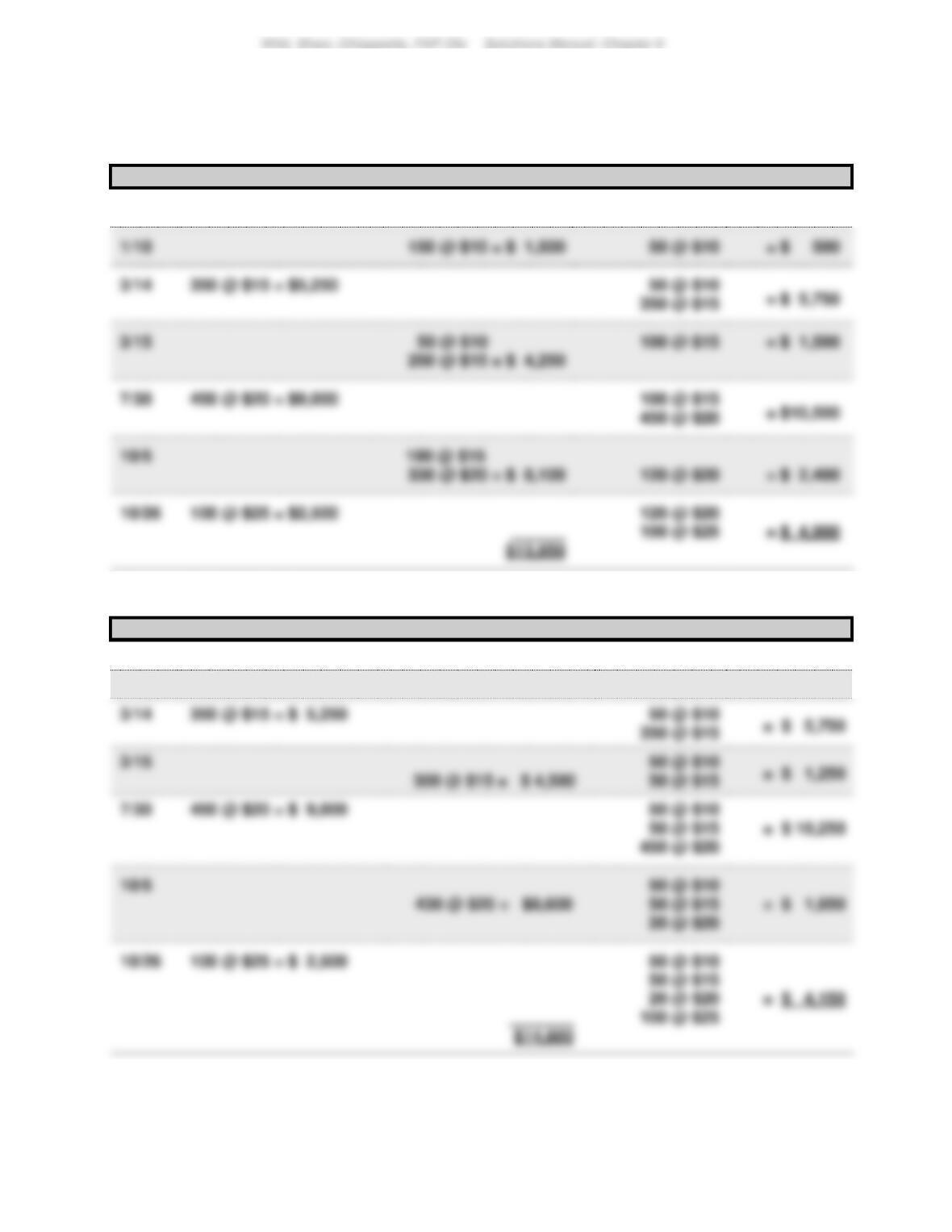

a. FIFO—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

200 @ $10

= $ 2,000

b. LIFO—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

200 @ $10

= $ 2,000

1/10

150 @ $10 = $ 1,500

50 @ $10

= $ 500

383

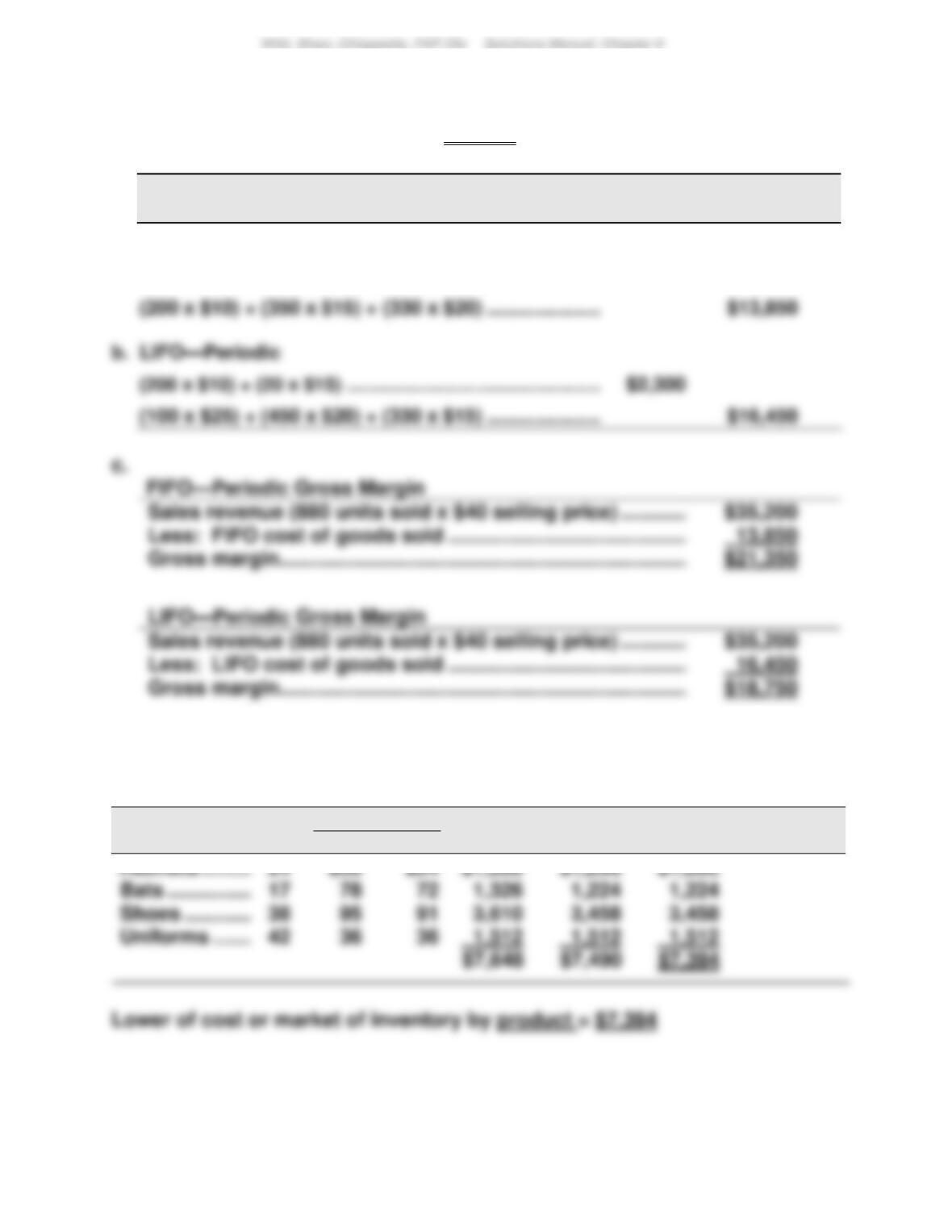

Exercise 6-7 (Concluded)

Alternate Solution Format

Ending Cost of

Inventory Goods Sold

a. FIFO

(100 x $25) + (120 x $20) ......................................................... $4,900

FIFO Gross Margin

Sales revenue (880 units sold x $40 selling price) .........................

$35,200

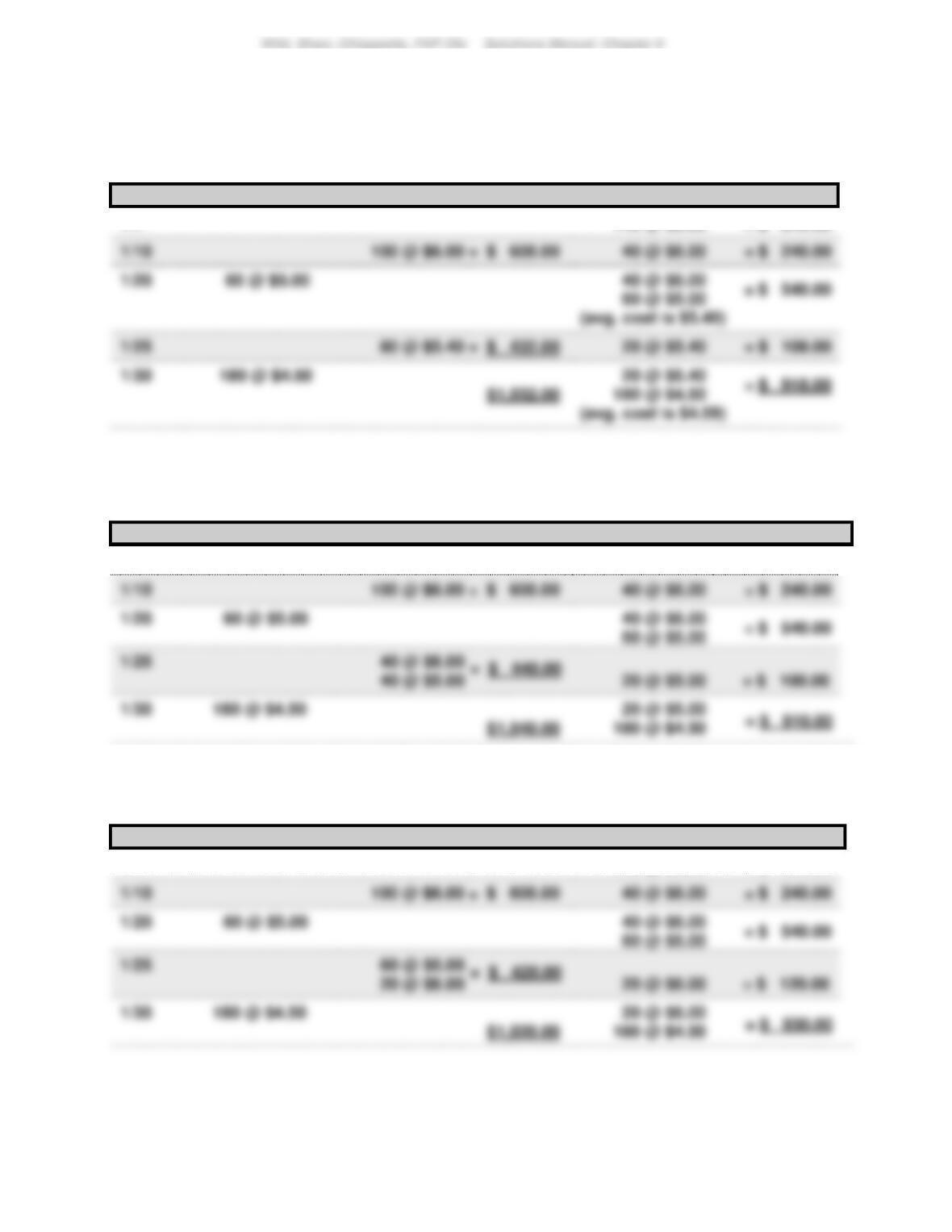

Exercise 6-8 (15 minutes)

a. Specific Identification method—Cost of goods sold

Cost of goods available for sale .............................................

$18,750

Ending inventory under specific identification

384

Exercise 6-9A (20 minutes)

Cost of goods available for sale = $18,750 (given in Exercise 6-7)

Ending Cost of

Periodic Inventory System Inventory Goods Sold

a. FIFO—Periodic

(100 x $25) + (120 x $20) ............................................ $4,900

Exercise 6-10 (15 minutes)

Per Unit

Total

Total

LCM Applied

to Items

Inventory Items

Units

Cost

Market

Cost

Market

385

Exercise 6-11 (20 minutes)

1. a. LIFO ratio computations

LIFO current ratio (2017) = $220/$200 = 1.1

b. FIFO ratio computations

2. The use of LIFO versus FIFO for Cruz markedly impacts the ratios computed.

Specifically, LIFO makes Cruz appear worse in comparison to FIFO numbers

on the current ratio (1.1 vs. 1.5) but better on inventory turnover (5.5 vs. 3.8)

Exercise 6-12 (25 minutes)

2. Reported income figures

Year 2016

Year 2017

Year 2018

Sales ..................................

$850,000

$850,000

$850,000

Cost of goods sold

Exercise 6-13 (20 minutes)

2016 Inventory turnover 2016 Days' Sales in Inventory

2017 Inventory turnover 2017 Days' Sales in Inventory

Exercise 6-14A (20 minutes)

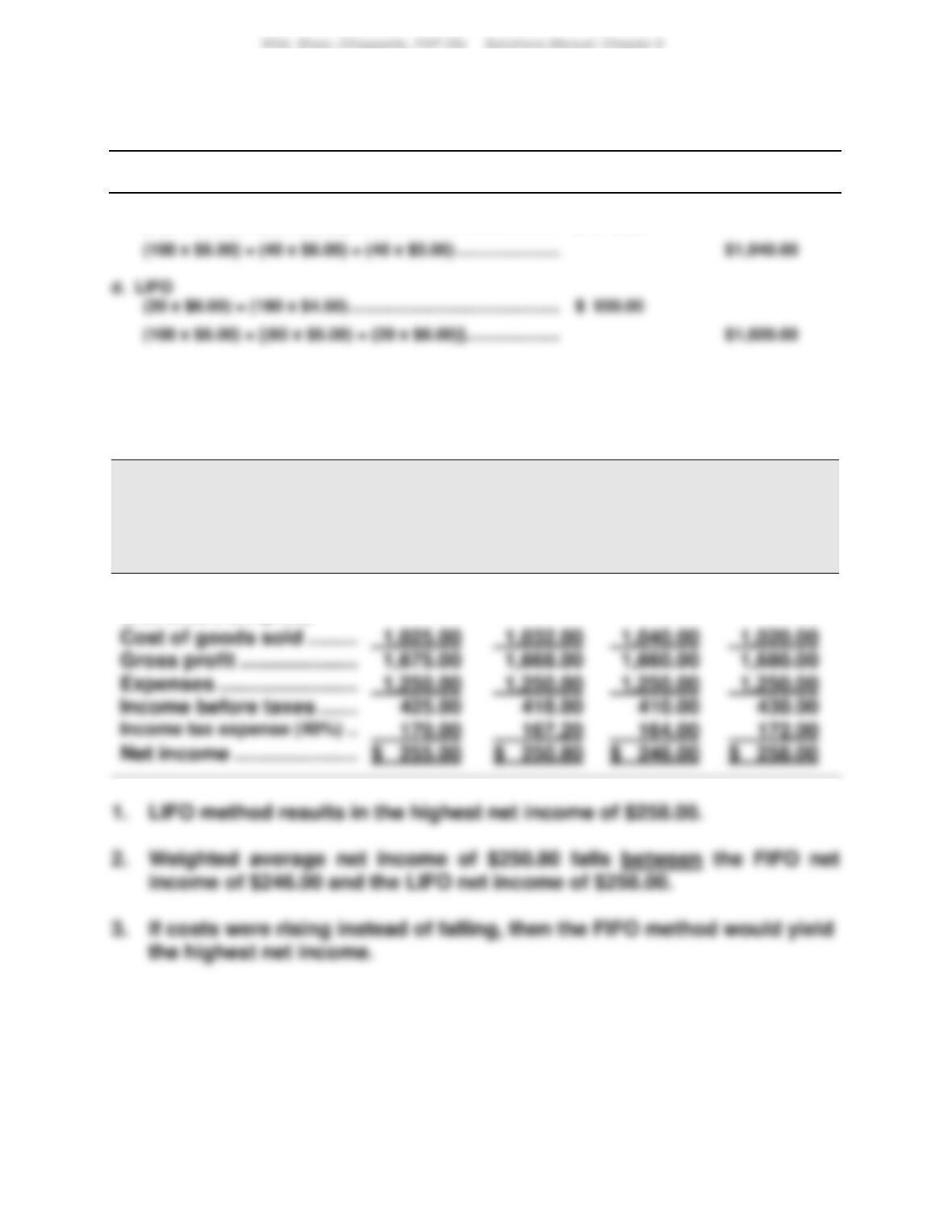

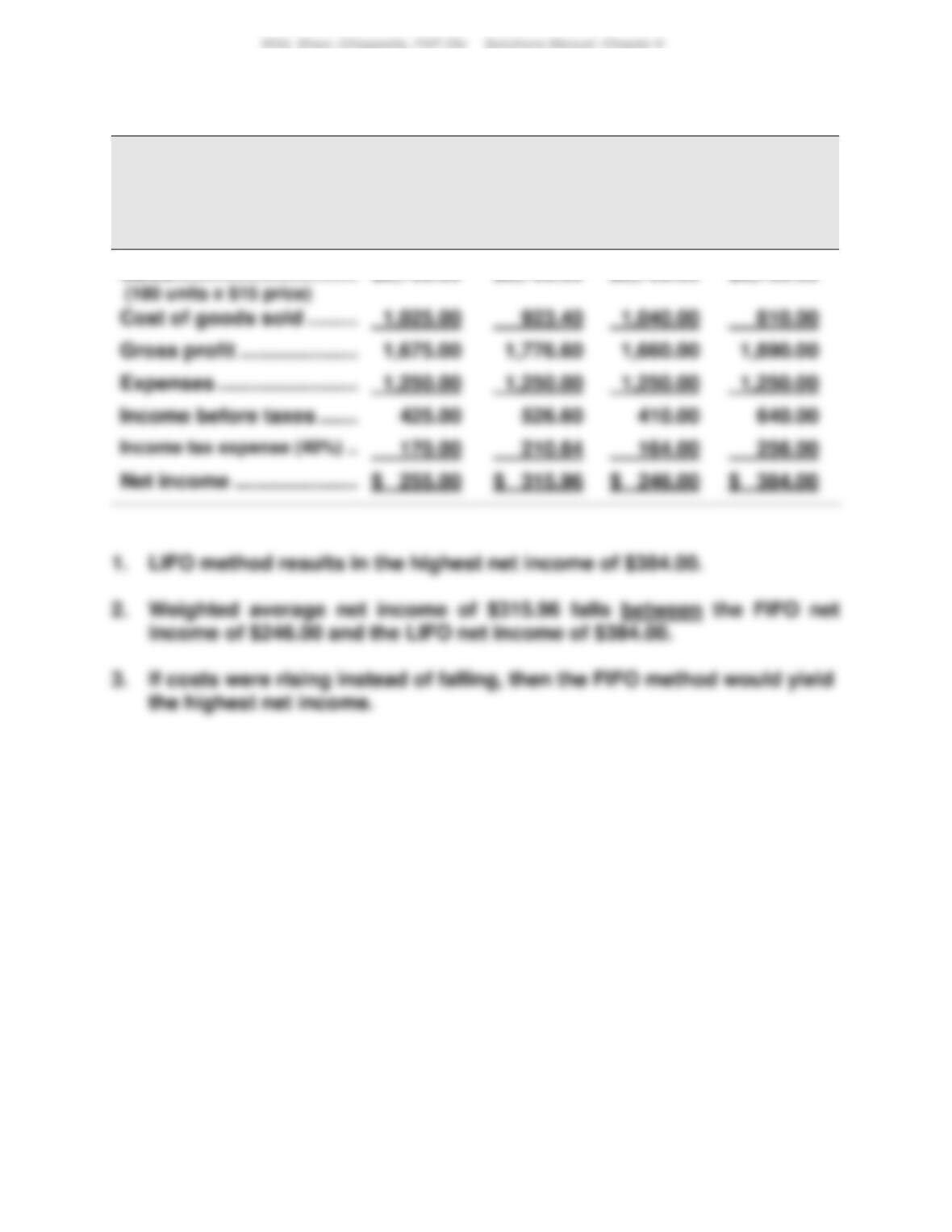

Ending

Inventory

Cost of

Goods Sold

a. Specific identification

(50 x $2.90) + (50 x $2.80) + (50 x $2.50) .............

$410.00