1. Merchandising businesses acquire merchandise for resale to customers. It is the selling of

2. Yes. Gross profit is the excess of sales over cost of merchandise sold. A net loss arises when

4. a. 1% discount allowed if paid within 15 days of date of invoice; entire amount of invoice

5. Sales to customers who use MasterCard or VISA cards are recorded as cash sales.

6. a. A credit memo issued by the seller of merchandise indicates the amount for which the

b

uyer’s account is to be credited (credit to Accounts Receivable) and the reason for the

p

7. a. The buyer

8. Sales, Cost of Merchandise Sold, Merchandise Inventory.

10. Loss from Merchandise Inventory Shrinkage would be debited.

CHAPTER 6

ACCOUNTING FOR MERCHANDISING BUSINESSES

DISCUSSION QUESTIONS

6-1

CHAPTER 6 Accounting for Merchandising Businesses

PE 6–1A

PE 6–1B

PE 6–2A

a. $13,328. Purchase of $18,228 [$18,600 – ($18,600 × 2%)] less the return of

PE 6–2B

PE 6–3A

a. Accounts Receivable [$72,500 – ($72,500 × 2%)] 71,050

Sales 71,050

PE 6–3B

a. Accounts Receivable [$92,500 – ($92,500 × 1%)] 91,575

Sales 91,575

PRACTICE EXERCISES

6-2

CHAPTER 6 Accounting for Merchandising Businesses

PE 6–4A

a. $75,250. Purchase of $89,100 [$90,000 – ($90,000 × 1%)] less return of

PE 6–4B

a. $31,680. Purchase of $35,640 [$36,000 – ($36,000 × 1%)] less return of

PE 6–5A

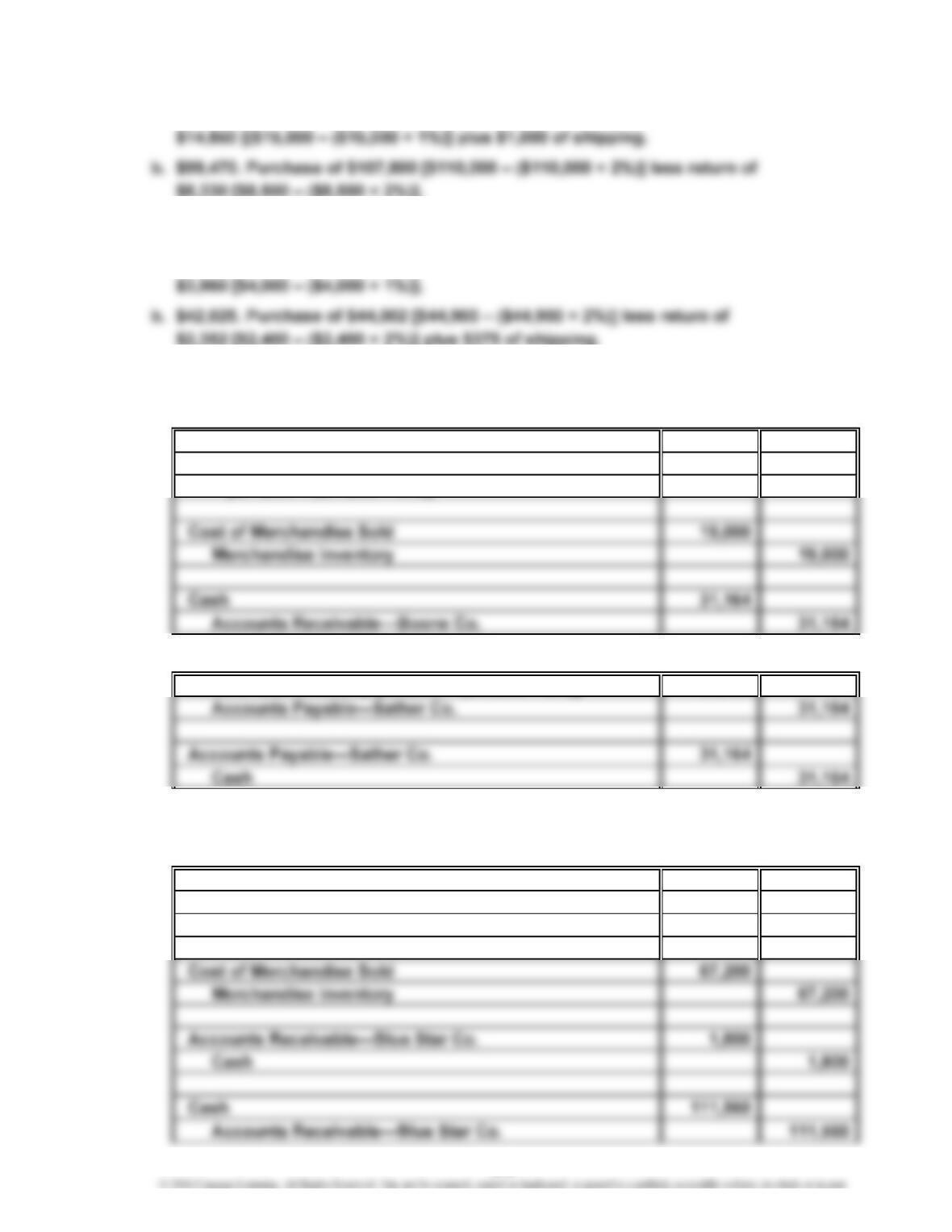

Sather Co. journal entries:

Accounts Receivable—Boone Co. 31,164

Sales 31,164

[$31,800 – ($31,800 × 2%)]

Boone Co. journal entries:

Merchandise Inventory [$31,800 – ($31,800 × 2%)] 31,164

PE 6–5B

Shore Co. journal entries:

Accounts Receivable—Blue Star Co. 109,760

Sales 109,760

[$112,000 – ($112,000 × 2%)]

6-3

CHAPTER 6 Accounting for Merchandising Businesses

PE 6–5B (Continued)

Blue Star Co. journal entries:

Merchandise Inventory 111,560

PE 6–6A

Nov. 30 Cost of Merchandise Sold 11,600

PE 6–6B

Dec. 31 Cost of Merchandise Sold 23,250

PE 6–7A

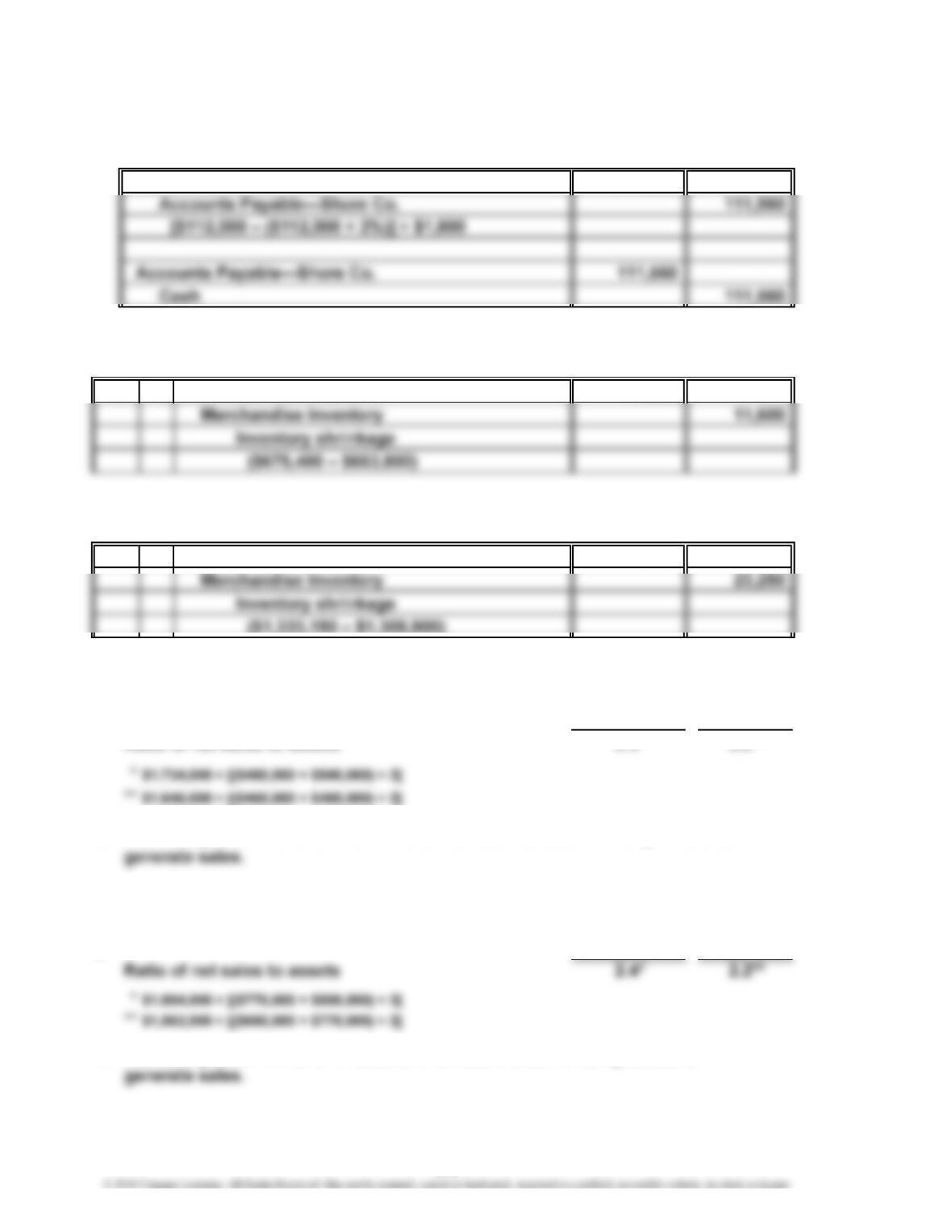

a. 2016 2015

Ratio of net sales to assets 3.4* 3.5**

b. The change from 3.5 to 3.4 indicates an unfavorable trend in using assets to

PE 6–7B

a. 2016 2015

b. The change from 2.2 to 2.4 indicates a favorable trend in using assets to

6-4

CHAPTER 6 Accounting for Merchandising Businesses

Ex. 6–1

a. $1,856,300 ($4,885,000 – $3,028,700)

Ex. 6–2

Ex. 6–3

a. $22,572. Purchase of $28,611 [$28,900 – ($28,900 × 1%)] less return of

Ex. 6–4

The offer of Supplier Two is lower than the offer of Supplier One. Details are as follows:

Supplier One Supplier Two

List price $100,000 $99,750

Ex. 6–5

(2) Paid freight, $300.

EXERCISES

6-5

CHAPTER 6 Accounting for Merchandising Businesses

Ex. 6–6

a. Merchandise Inventory [$75,000 – ($75,000 × 2%)] 73,500

Accounts Payable 73,500

Ex. 6–7

a. Merchandise Inventory [$48,000 – ($48,000 × 1%)] 47,520

Accounts Payable—Atlas Co. 47,520

b. Accounts Payable—Atlas Co. 47,520

Cash 47,520

6-6

CHAPTER 6 Accounting for Merchandising Businesses

Ex. 6–8

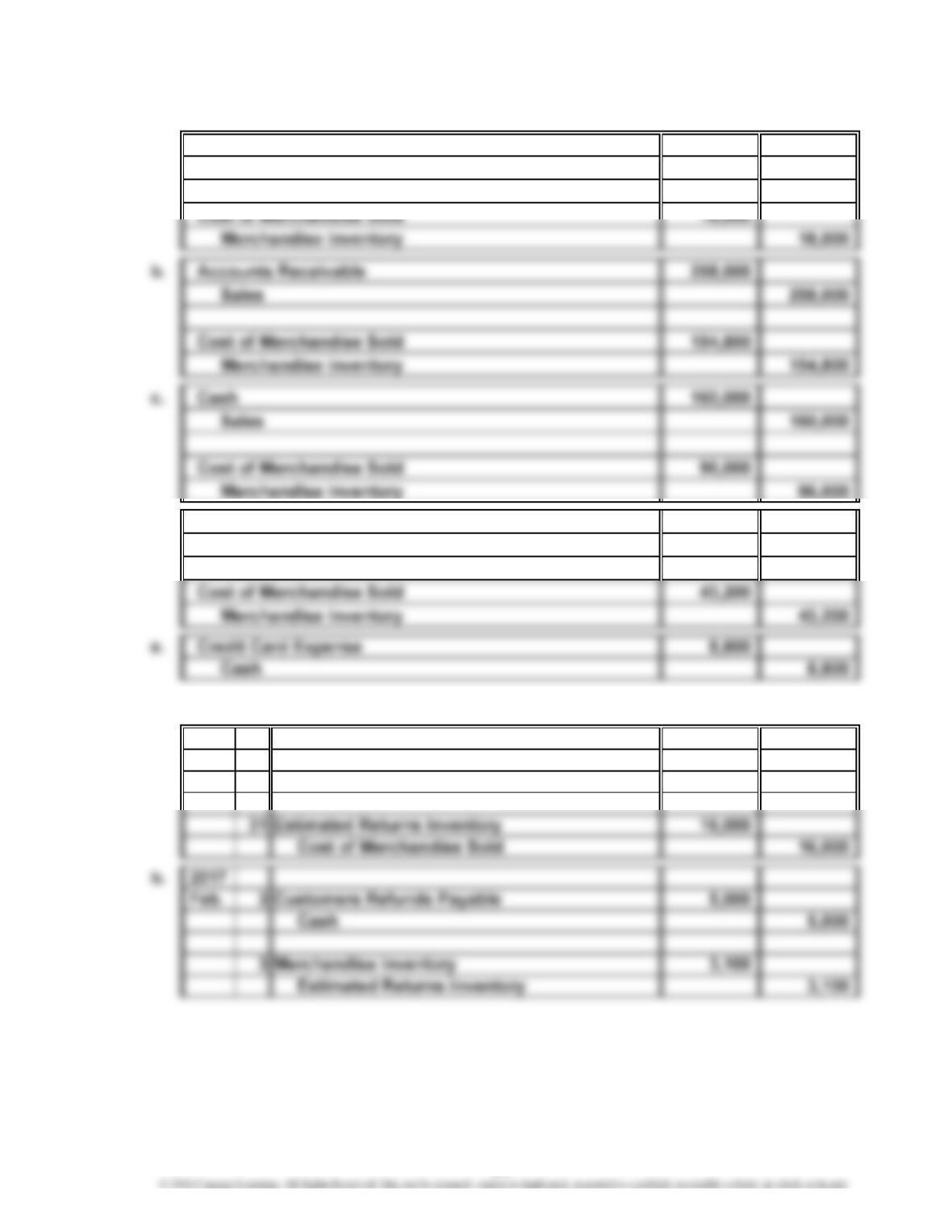

a. Cash 30,000

Sales 30,000

d. Cash 72,000

Sales 72,000

Ex. 6–9

a. 2016

Dec. 31 Sales ($1,800,000 × 1.5%) 27,000

Customer Refunds Payable 27,000

6-7

CHAPTER 6 Accounting for Merchandising Businesses

Ex. 6–10

a. $27,440 [$28,000 – ($28,000 × 2%)]

b. Customers Refunds Payable 27,440

Cash 27,440

Ex. 6–11

(2) Recorded the cost of the merchandise sold and reduced the merchandise

inventory account, $25,200.

(4) Updated the merchandise inventory account for the cost of the merchandise

Ex. 6–12

a. $55,370 [$56,500 – ($56,500 × 2%)]

Ex. 6–13

a. $22,500 ($27,000 – $4,500)

b. $15,763. Purchase of $18,228 [$18,600 – ($18,600 × 2%)] less return of

$2,940 [$3,000 – ($3,000 × 2%)] plus freight of $475.

6-8

CHAPTER 6 Accounting for Merchandising Businesses

Ex. 6–14

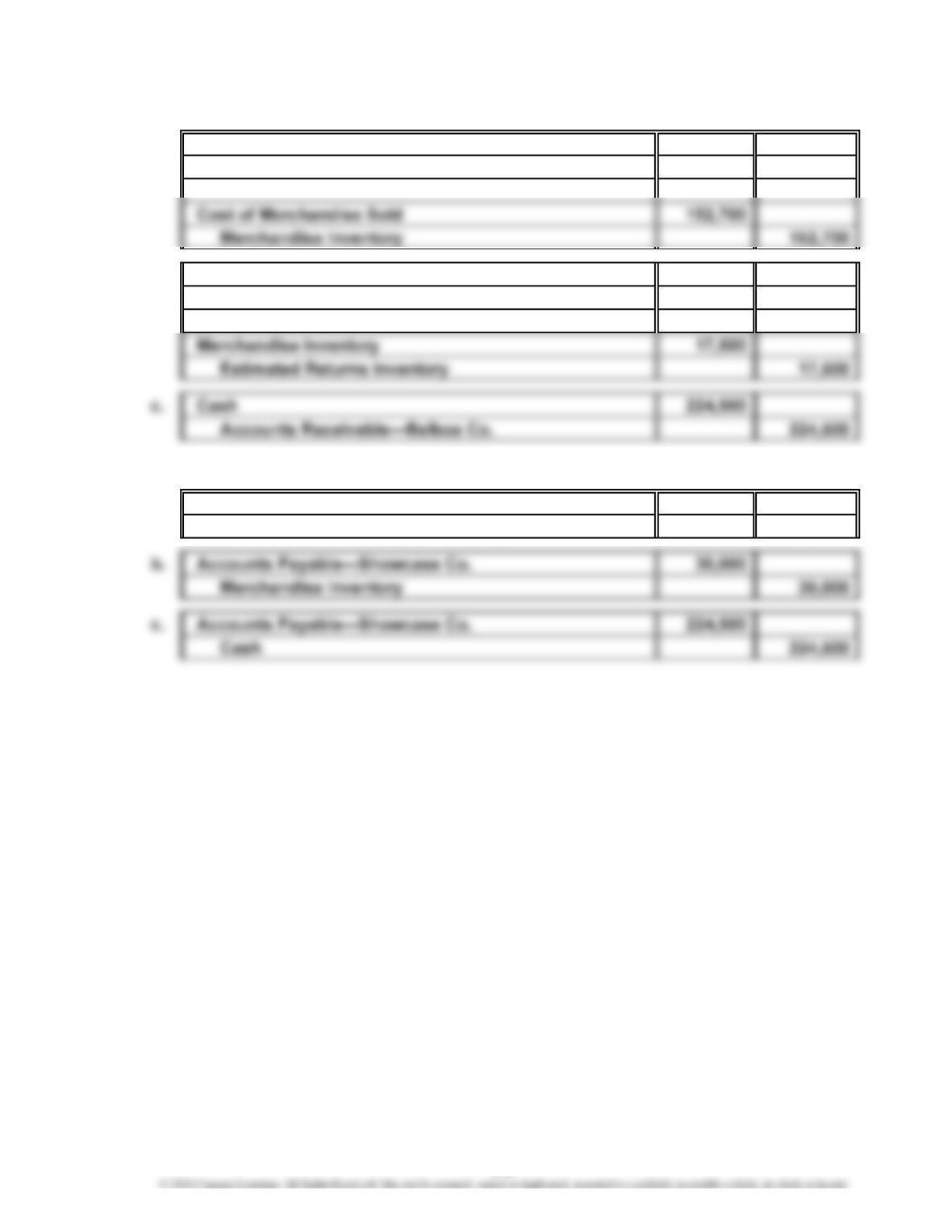

a. Accounts Receivable—Balboa Co. 254,500

Sales 254,500

b. Customer Refunds Payable 30,000

Accounts Receivable—Balboa Co. 30,000

Ex. 6–15

a. Merchandise Inventory 254,500

Accounts Payable—Showcase Co. 254,500

6-9

CHAPTER 6 Accounting for Merchandising Businesses

Ex. 6–16

Balance Sheet Accounts Income Statement Accounts

100 Assets 400 Revenues

110 Cash 410 Sales

112 Accounts Receivable 500 Expenses

200 Liabilities 532 Depreciation Expense—

210 Accounts Payable Office Equipment

Note: The order and number of some of the accounts within subclassifications is

somewhat arbitrary, as in accounts 115–117, accounts 520–524, and accounts

6-10

CHAPTER 6 Accounting for Merchandising Businesses

Ex. 6–17

a. At the time of sale

Ex. 6–18

a. Accounts Receivable 65,940

Sales 62,800

b. Sales Tax Payable 39,650

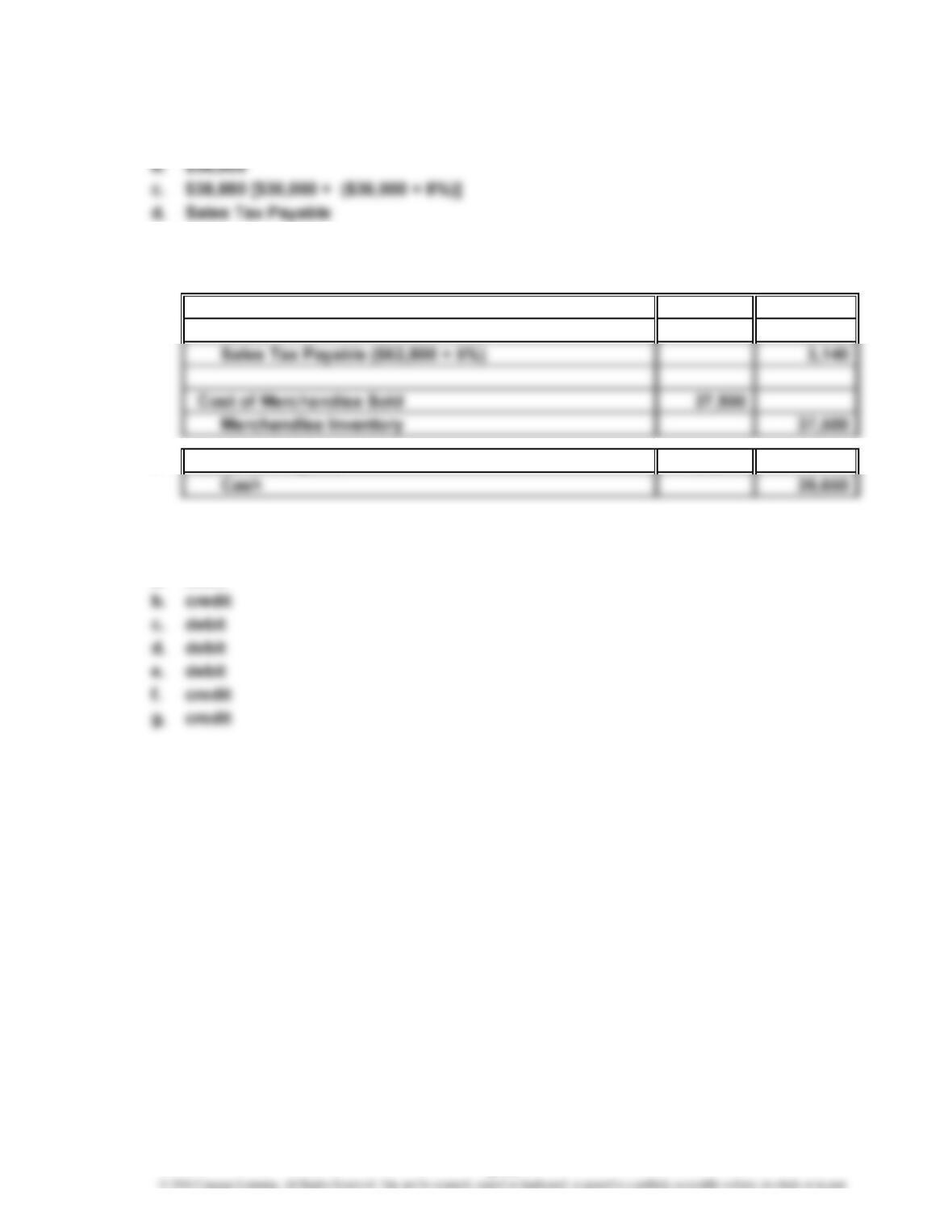

Ex. 6–19

a. debit

6-11

CHAPTER 6 Accounting for Merchandising Businesses

Ex. 6–20

a. Gross profit: $10,165,000 ($25,565,000 – $15,400,000)

b. No, there could be other income and expense items that could affect the

Ex. 6–21

a. Selling expense, (1), (2), (7), (8)

Ex. 6–22

a. $379,900 ($463,400 – $83,500)

6-12

CHAPTER 6 Accounting for Merchandising Businesses

Ex. 6–23

a.

Sales $6,410,000

Cost of merchandise sold 3,800,000

Gross profit $2,610,000

b. The major advantage of the multiple-step form of income statement is that

PRESTIGE FURNISHINGS COMPANY

Income Statement

For the Year Ended October 31, 2016

6-13

CHAPTER 6 Accounting for Merchandising Businesses

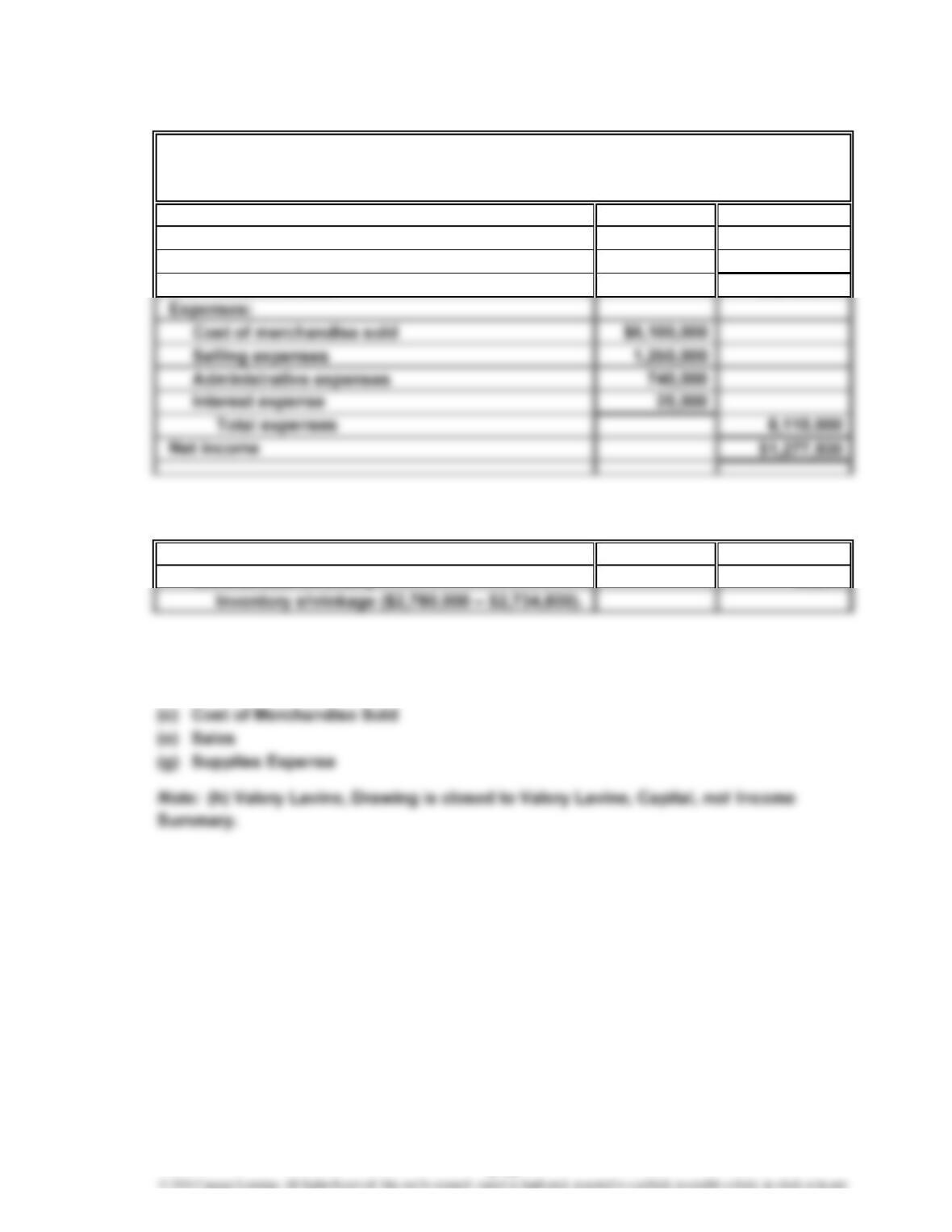

Ex. 6–24

2. Deducting the total expenses from gross profit would yield income from

operations (or operating income).

4. The final amount on the income statement should be labeled net income, not

gross profit.

A correct income statement would be as follows:

Sales $8,595,000

Cost of merchandise sold 6,110,000

Gross profit $2,485,000

Expenses:

CURBSTONE COMPANY

Income Statement

For the Year Ended August 31, 2016

6-14

CHAPTER 6 Accounting for Merchandising Businesses

Ex. 6–25

Revenues:

Sales $9,332,500

Rent revenue 60,000

Total revenues $9,392,500

Ex. 6–26

Cost of Merchandise Sold 45,200

Merchandise Inventory 45,200

Ex. 6–27

(b) Advertising Expense

CUSTOM WIRE & TUBING COMPANY

Income Statement

For the Year Ended April 30, 2016

6-15

CHAPTER 6 Accounting for Merchandising Businesses

Ex. 6–28

2016

Oct. 31 Sales 6,410,000

Income Summary 6,410,000

31 Income Summary 5,065,000

Cost of Merchandise Sold 3,800,000

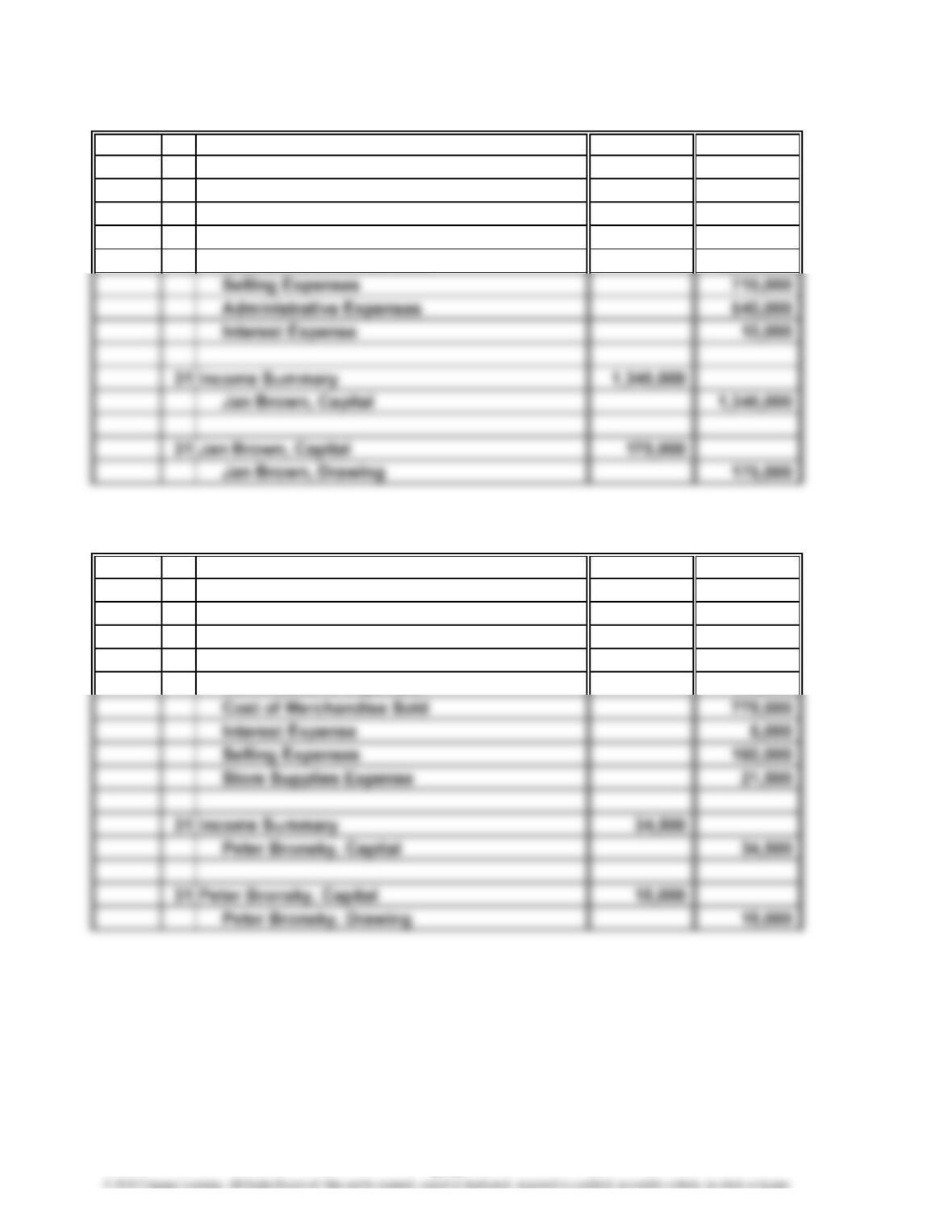

Ex. 6–29

2016

July 31 Sales 1,437,000

Income Summary 1,437,000

31 Income Summary 1,402,500

Administrative Expenses 440,000

Closing Entries

Closing Entries

6-16

CHAPTER 6 Accounting for Merchandising Businesses

Ex. 6–30

a. Year 2: 1.75 {$70,395 ÷ [($40,518 + $40,125) ÷ 2]}

Ex. 6–31

a. 3.85 {$90,374 ÷ [($23,476 + $23,505) ÷ 2]}

b. Although Kroger and Tiffany are both retail stores, Tiffany sells jewelry using a

much longer operating cycle than Kroger uses selling groceries. Thus, Kroger is

6-17

CHAPTER 6 Accounting for Merchandising Businesses

Ex. 6–32

(a) credit

Ex. 6–33

Jan. 2 Purchases 18,200

Accounts Payable 18,200

13 Accounts Receivable [$37,300 – ($37,300 × 1%)] 36,927

Sales 36,927

15 Delivery Expense 215

6-18

CHAPTER 6 Accounting for Merchandising Businesses

Ex. 6–35

a. Cost of merchandise sold:

Merchandise inventory, May 1, 2015 $ 380,000

Purchases $3,800,000

Less: Purchases returns and

Ex. 6–36

Cost of merchandise sold:

Merchandise inventory, November 1 $ 28,000

Purchases $475,000

Less: Purchases returns and

allowances $15,000

6-19

CHAPTER 6 Accounting for Merchandising Businesses

Ex. 6–37

Cost of merchandise sold:

Merchandise inventory, July 1 $ 190,850

Purchases $1,126,000

Less: Purchases returns and

allowances $46,000

Ex. 6–38

2. Purchases returns and allowances and purchases discounts should be deducted

from (not added to) purchases.

4. Freight in should be added to net purchases to yield cost of merchandise

purchased.

A correct cost of merchandise sold section is as follows:

Cost of merchandise sold:

Merchandise inventory, June 1, 2015 $ 91,300

Purchases $1,110,000

Less: Purchases returns and

6-20