ATS–13

2018

e

d

i

t

i

o

n

PAYROLL

ACCOUNTING

Bieg/Toland

TEST 6

Student INSTRUCTOR’S COPY

Chapter 6 Date

SCORING RECORD

Section Total Points Deductions Score

A 40

B 60

Total 100

Section A—DIRECTIONS: Each of the following statements is either true or false. Unless directed otherwise

by your instructor, indicate your choice in the Answers column by writing “T” for a true answer or “F” for a false

answer. (2 points for each correct answer)

For

Answers Scoring

1. In the garnishment process, federal tax levies take secondary priority to wages withheld for

2. The information needed in preparing a journal entry to record the wages earned, deductions

3. In all computerized payroll systems, there is still the need to manually post from the printed

5. The employer keeps track of each employee’s accumulated wages in the employee’s earnings

6. In calculating overtime premium earnings at one and a half times the regular hourly rate, the

7. When recording the employer’s payroll taxes, a liability account entitled Employers Payroll

8. The payment of the FUTA tax and the FICA taxes by the employer to the IRS is recorded in the

9. In the case of a federal tax levy, the employee will notify the employer of the amount to take

10. FICA Taxes Payable—HI is a liability account in which is recorded the liability of the employer

11. Federal tax levies are not subject to the limits imposed on garnishments under the Consumer

14. In the case of an unclaimed paycheck, the employer can hold the check indefinitely until the

ATS–14 Chapter 6/Achievement Test Solutions

SECTION A (continued)

For

Answers Scoring

15. For the purpose of a federal tax levy, the IRS defines take-home pay as the gross pay less taxes

16. In the case of multiple wage attachments, a garnishment for a student loan has priority over any

17. At the time of depositing FICA taxes and employees’ federal income taxes, the account FICA

18. When union dues that have been withheld from employees’ wages are turned over to the union

19. The employer’s OASDI portion of FICA taxes is included as part of the payroll tax entry, but

Section B—DIRECTIONS: Journalize each of the payroll transactions listed below. Omit the writing of the

description or explanation for each journal entry, and do not skip a line between each entry. Then

p

ost all entries

except the last one to the appropriate general ledger accounts. (8 points for each correct journal entry and ½

p

oint

for each correct account balance)

The journal page and the ledger accounts to be used in this section are supplied on the following pages. The balances

listed in the general ledger accounts for Cash, FUTA Taxes Payable, SUTA Taxes Payable, Employees SIT Payable,

Wages and Salaries, and Payroll Taxes are the results of all payroll transactions for the first quarter, not including

the last pay of the quarter. The balances in FICA Taxes Payable—OASDI, FICA Taxes Payable—HI, and Employ-

ees FIT Payable are the amounts due from the March 15 payroll.

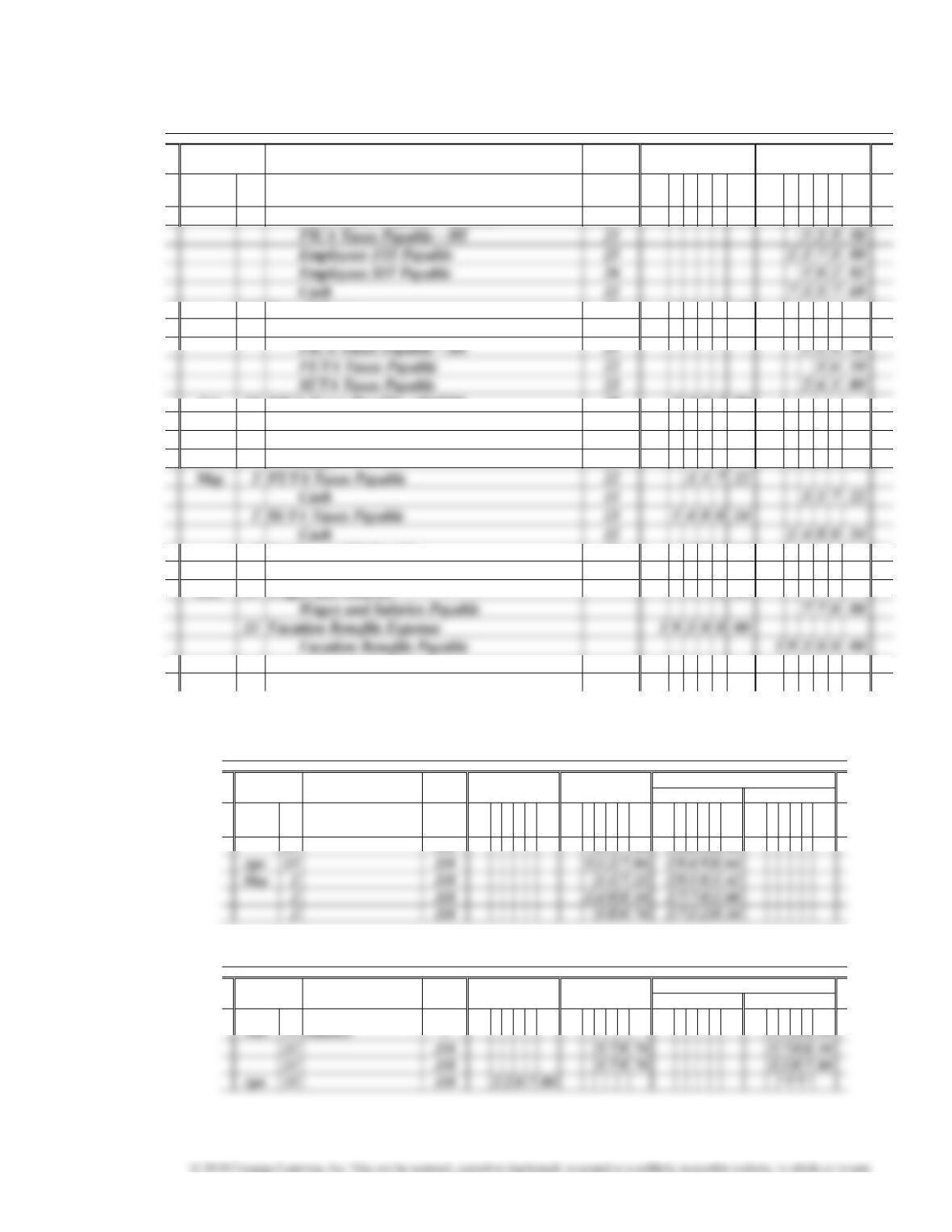

March 31, 20–: Paid total wages of $9,350.00. These are the wages for the last semimonthly pay of March. All of

this amount is taxable under FICA (OASDI and HI). In addition, withhold $1,175 for federal income taxes and

$102.03 for state income taxes. These are the only deductions made from the employees’ wages.

March 31, 20–: Record the employer’s payroll taxes for the last pay in March. All of the earnings are taxable under

FICA (OASDI and HI), FUTA (0.6%), and SUTA (2.8%).

April 15, 20–: Made a deposit to remove the liability for the FICA taxes and the employees’ federal income taxes

withheld on the two March payrolls.

May 2, 20–: Made the deposit to remove the liability for FUTA taxes for the first quarter of 20–.

May 2, 20–: Filed the state unemployment contributions return for the first quarter of 20– and paid the total amount

owed for the quarter to the state unemployment compensation fund.

May 2, 20–: Filed the state income tax return for the first quarter of 20– and paid the total amount owed for the

quarter to the state income tax bureau.

December 31, 20–: In July 20–, the company changed from a semimonthly pay system to a weekly pay system.

The employees were paid every Friday through the rest of 20–. Record the adjusting entry for wages accrued at the

end of December ($770) but not paid until the first Friday in January. Do not post this entry.

December 31, 20–: The company has determined that employees have earned $19,300 in unused vacation time.

Record the adjusting entry to put this expense on the books. Do not post this entry.

Chapter 6/Achievement Test Solutions ATS–15

JOURNAL PAGE 18

POST

DATE DESCRIPTION REF. DEBIT CREDIT

20–

Mar. 31 Wages and Salaries 51 9 3 5 0 00

FICA Taxes Payable—OASDI 20 5 7 9 70

31 Payroll Taxes 52 1 0 3 3 18

FICA Taxes Payable—OASDI 20 5 7 9 70

Apr. 15 FICA Taxes Payable—OASDI 20 2 2 8 7 80

FICA Taxes Payable—HI 21 5 3 5 06

Employees FIT Payable 25 2 3 0 5 00

Cash 11 5127 86

2 Employees SIT Payable 26 5 8 0 74

Cash 11 58074

Dec. 31 Wages and Salaries 7 7 0 00

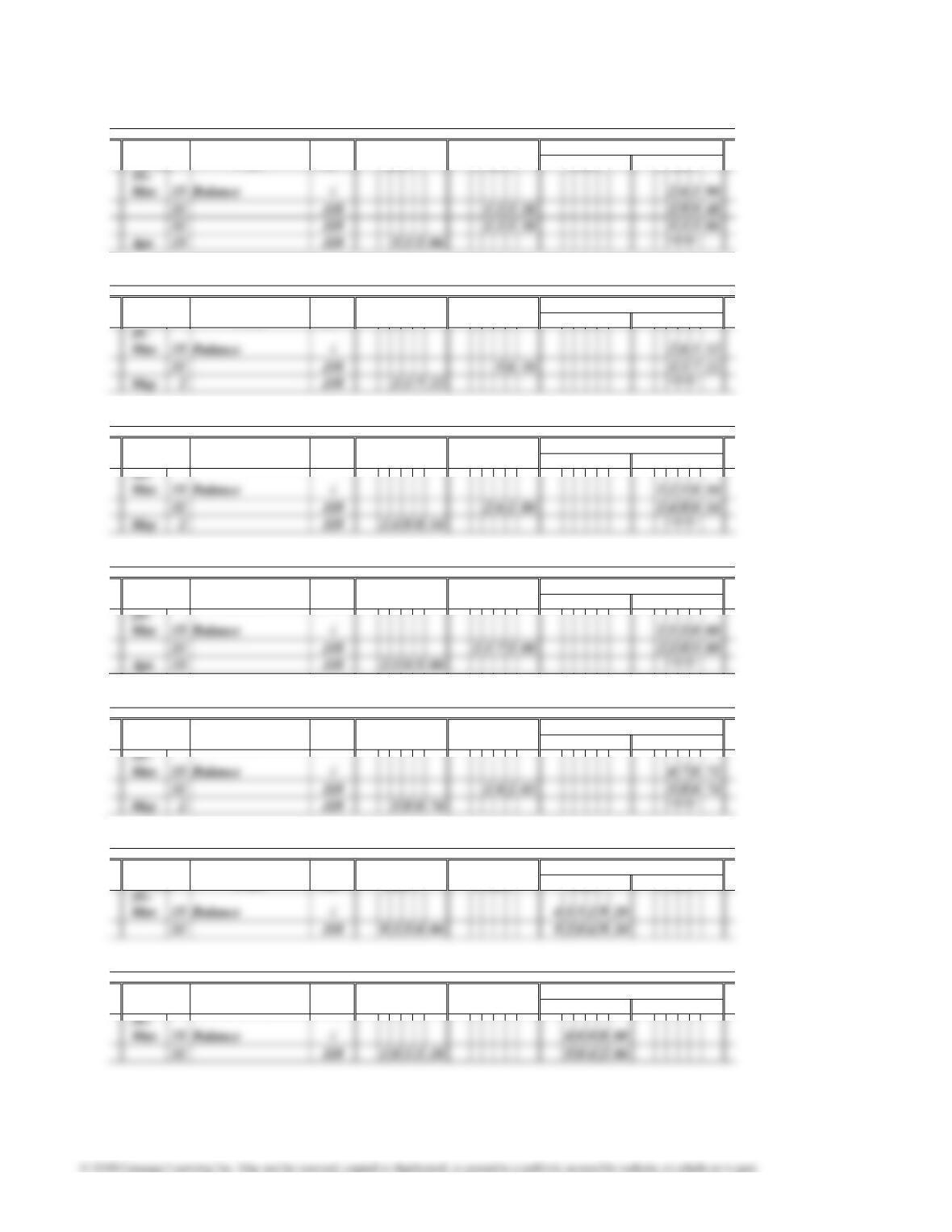

GENERAL LEDGER

ACCOUNT CASH ACCOUNT 11

POST BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

20–

Mar. 31 Balance

√

4 1 9 8 4 19

ACCOUNT FICA TAXES PAYABLE

—

OASDI ACCOUNT 20

POST BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

20–

ATS–16 Chapter 6/Achievement Test Solutions

ACCOUNT FICA TAXES PAYABLE

—

HI ACCOUNT 21

POST BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

ACCOUNT FUTA TAXES PAYABLE ACCOUNT 22

POST BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

ACCOUNT SUTA TAXES PAYABLE ACCOUNT 23

POST BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

ACCOUNT EMPLOYEES FIT PAYABLE ACCOUNT 25

POST BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

ACCOUNT EMPLOYEES SIT PAYABLE ACCOUNT 26

POST BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

ACCOUNT WAGES AND SALARIES ACCOUNT 51

POST BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT

ACCOUNT PAYROLL TAXES ACCOUNT 52

POST BALANCE

DATE ITEM REF. DEBIT CREDIT DEBIT CREDIT