Chapter 6 – Weygandt Managerial 7e

Challenge Exercises Solutions

Solution

CE6-1

(a)

(1) Booth Company

CVP Income Statement

For the year ended December 31, 2017

Sales (75,000 units x $25/unit)……………………………………… $1,875,000

(2) Booth Company

CVP Income Statement

For the year ended December 31, 2017

Sales (78,000 units x $23/unit)…………………………………….…$1,794,000

Variable Costs (78,000 units x $12/unit…………………………………936,000

(b) Booth Company

CVP Income Statement

For the year ended December 31, 2017

Sales (67,500 units x $28/unit)…………………………………………$1,890,000

Variable Costs (67,500 units x $17.25/unit…………………….……….1,164,375

(c) Booth Company

CVP Income Statement

For the year ended December 31, 2017

Sales (75,000 units x $28/unit)………………………… ………………$2,100,000

Variable Costs (75,000 units x $17.75/unit………….…………………..1,331,250

Solution

CE 6-2

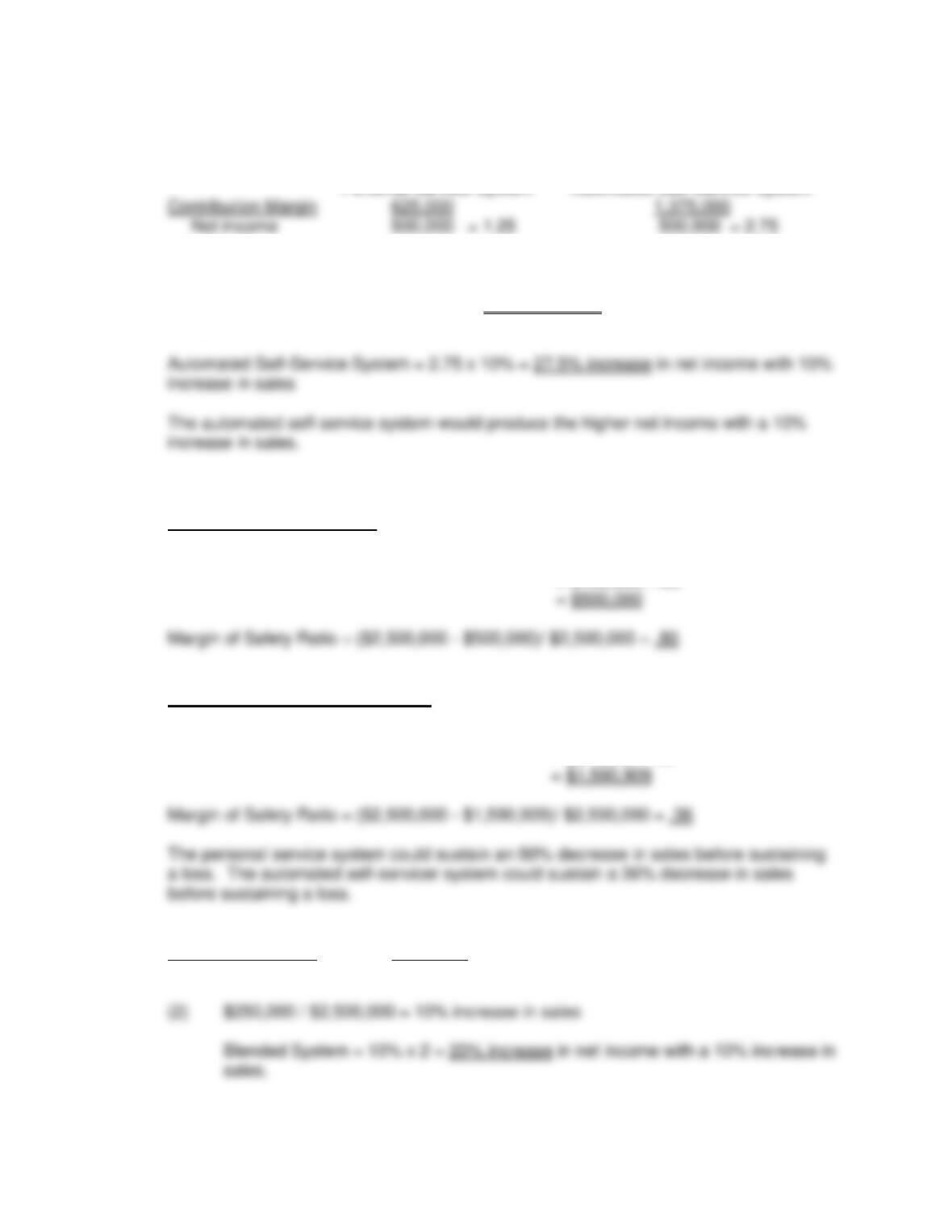

(a) Operating leverage = Contribution margin / Net income

Personal Service System Automated Self-Service System

(b) Increase in sales = $250,000/$2,500,000 = 10% increase

Personal Service System = 1.25 x 10% = 12.5% increase in net income with 10%

increase in sales

(c) Margin of safety ratio = (Actual sales – Break-even sales) / Actual sales

Personal Service System:

Break even = Fixed Costs / Contribution margin ratio = $125,000 / ($625,000 / $2,500,000)

= $125,000 / .25

Automated Self-Service System:

Break even = Fixed Costs / Contribution margin ratio = $875,000 / ($1,375,000 / $2,500,000)

= $875,000 / .55

(d) (1) Blended System

Contribution Margin 1,000,000

Net income 500,000 = 2.00 operating leverage

CE 6-2 solution (continued)

(3)

Break even = Fixed Costs / Contribution margin ratio = $500,000 / ($1,000,000 / $2,500,000)

= $500,000 / .40

= $1,250,000