6

Fundamentals of Product and Service Costing

Solutions to Review Questions

6-1.

Cost allocation is the assignment of costs in cost pools to cost objects. The cost objects

6-2.

Cost management systems should satisfy the following criteria:

6-3.

Cost flow diagrams serve two purposes. First, they help describe how a cost

6-4.

A job costing accounting system traces costs to individual units or to specific jobs

6-5.

All three systems assign costs from cost pools to cost objects using a cost allocation

rule. They differ in detail of the cost assignments to individual units.

6-6.

6-7.

6-8.

6-9.

6-10.

The basic cost flow model appears as follows:

Beginning balance + Transfers in – Transfers out = Ending balance

Solutions to Critical Analysis and Discussion Questions

6-11.

Although there may be no one correct way to allocate cost, cost allocation can provide

6-12.

There are three important points to consider:

1. The cost system should meet the needs of the users (the decision makers).

6-13.

The basic cost flow model is as follows:

6-14.

It is sometimes difficult (and frustrating) for managers when the cost accountant says

6-15.

Reasons to agree with approach: If the products are not contributing to company profits,

then the products should be eliminated. This will increase overall company profits.

6-16.

The way the “products” are defined will depend, at least in part, on the decision the

dean is interested in making. They may be defined as degree programs vs. non-degree

programs. They may be the different degree programs. They might be the credit hour

(although it is unlikely you would be able to get much information at this level).

6-17.

Answers will vary. Common answers include the number of students, the number of

credit hours, number of classes, number of class sessions, and so on.

6-18.

6-19.

Although it would be ideal for the cost allocation base to have cause–and-effect relation

with overhead costs, it is unlikely to happen for several reasons. One reason is that

6-20.

The allocation base determines the costs assigned to the cost objects. If these costs are

6-21.

There are many reasons why two companies may have different cost systems. First,

dictate the information needed from the cost system.

6-22.

6-23.

Although it is true that the cost of the product will be the same regardless of the cost

allocation method, it does not mean that cost allocation does not matter. We might be

Solutions to Exercises

6-24. (20 min.) Basic Cost Flow Model: Ralph’s Mini-Mart.

6-25. (20 min.) Basic Cost Flow Model: Generic Electric.

a. $32.0 million = $8.0 million + $13.5 million + (.7 x $15.0 million)

6-26. (20 min.) Basic Cost Flow Model.

Based on the basic formula:

6-27. (20 min.) Basic Cost Flow Model.

Based on the basic formula:

BB

+

TI

–

TO

=

EB

A.

+

–

=

=

=

B.

+

–

=

=

=

+

–

=

=

=

6-28. (20 min.) Basic Cost Flow Model.

Based on the basic formula:

BB

+

TI

–

TO

=

EB

A.

+

–

=

=

=

$31,000

B.

+

$210,000

–

=

=

$30,000 + $210,000 – $22,000

=

$218,000

$102,000

+

–

$815,000

=

=

=

$827,000

Manufacturing overhead ………………..

6-29. (10 min.) Basic Product Costing: Enviro Corporation.

6-30. (10 min.) Basic Product Costing: Sara’s Sodas.

Materials ……………………………………..

$310,000

=

6-31. (15 min.) Basic Product Costing: Sara’s Sodas.

If the cost per liter is $0.43 and 4.5 million liters were produced, the total manufacturing

cost must have been $1,935,000 (= $0.43 x 4.5 million). But total manufacturing cost is

computed as:

6-32. (15 min.) Basic Product Costing: Sara’s Sodas.

a. If the cost per liter is $0.45 and 3.8 million liters were produced, the total

manufacturing cost must have been $1,710,000 (= $0.45 x 3.8 million). But total

manufacturing cost is computed as:

6-33. (10 min.) Basic Product Costing: Big City Bank.

Labor …………………………………………..

$ 35,000

÷ Checks processed ………………………

6-34. (20 min.) Basic Product Costing: Luke’s Lubricants.

Total

a.

Sold

b.

Work-in–

Process,

January 31

Production:

Gallons …………………………………..

900,000

800,000

100,000

Percentage complete ……………….

100%

80%

Equivalent gallons……………………

800,000

Materials ………………………………..

Labor ……………………………………

Manufacturing overhead …………..

294,000

Total cost incurred …………………..

Cost per equivalent gallon …………..

6-35. (20 min.) Basic Product Costing—Ethical Issues: Old Tyme Soda.

a. and b.

Total

a.

Sold

b.

Work-in–

Process,

November 30

Production:

Costs:

6-36. (15 min.) Process Costing: Sanchez & Company.

Total

Transferred

to Finished

Goods

Work-in–

Process,

January 31

Production:

Costs:

6-37. (15 min.) Process Costing: Graham Petroleum.

Total

Shipped

Work-in–

Process,

May 31

Production:

28.0

16.8

Costs:

6-38. (15 min.) Process Costing: Joplin Corporation.

Total

Completed

Work-in–

Process,

November 30

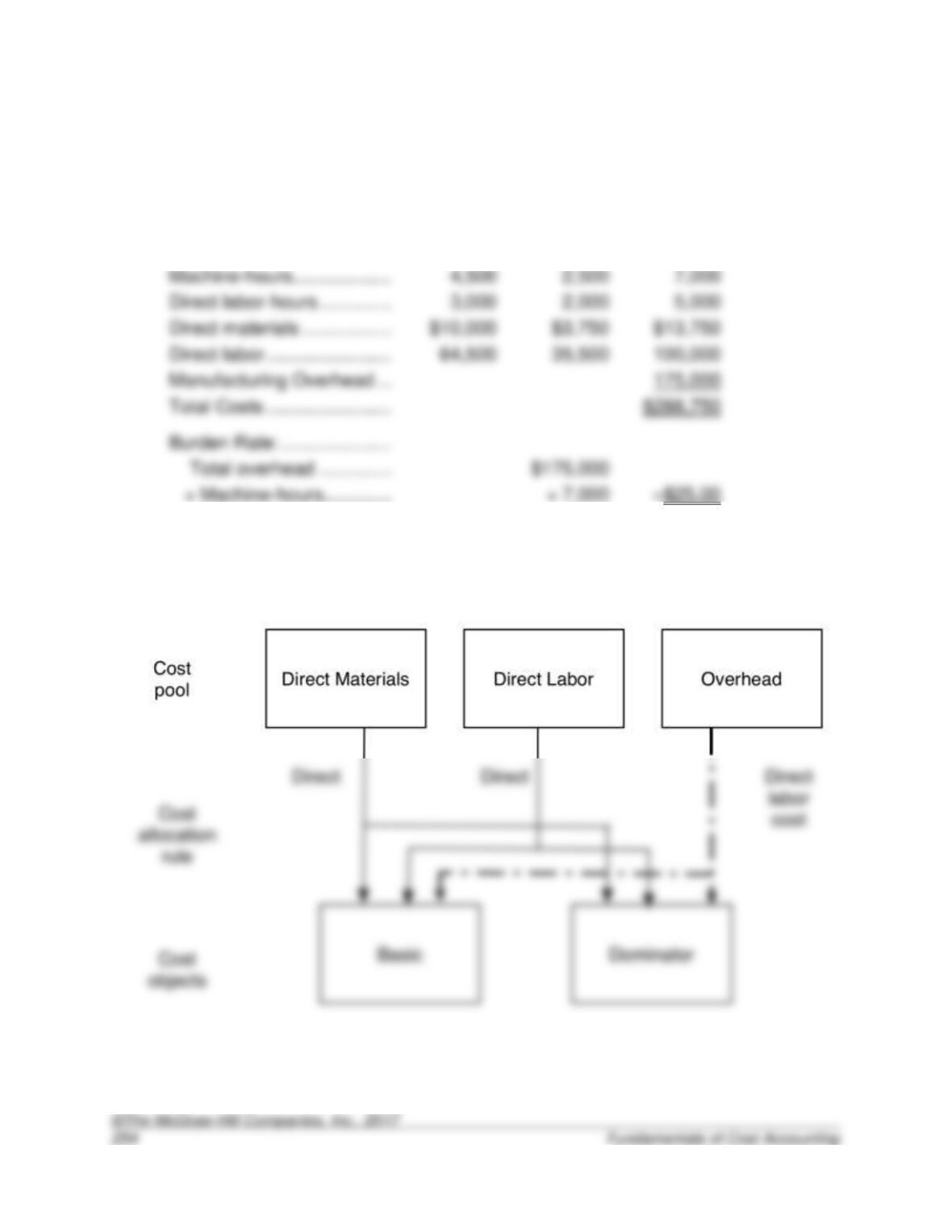

6-39. (15 Minutes) Predetermined Overhead Rates: Tiger Furnishings.

Predetermined overhead rate = $35.00 per direct labor hour.

Basic

Dominator

Total

Units produced ………………….

1,000

250

1,250

7,000

Direct labor-hours ………………

3,000

2,000

5,000

Direct materials …………………

Direct labor ……………………….

Burden Rate: …………………….

6-40. (15 Minutes) Predetermined Overhead Rates: Tiger Furnishings.

Predetermined overhead rate = 175% of direct labor cost.

Basic

Dominator

Total

Units produced ………………….

1,000

250

1,250

7,000

Direct labor-hours ………………

3,000

2,000

5,000

Direct materials …………………

Direct labor ……………………….

Manufacturing overhead ……..

Burden Rate: …………………….

6-41. (15 Minutes) Predetermined Overhead Rates: Tiger Furnishings.

Predetermined overhead rate = $25.00 per machine-hour.

Basic

Dominator

Total

Units produced ………………

1,000

250

1,250

7,000

Direct labor-hours …………..

3,000

2,000

5,000

Direct materials ……………..

Direct labor ……………………

6-42. (20 Minutes) Predetermined Overhead Rates: Tiger Furnishings.

6-43. (30 Minutes) Operations Costing: Howrley-David, Inc.

The unit costs are:

Fatboy: …………

$4,000

Screamer: …….

$5,000

Fatboy

Screamer

Total

Number of units …………………….

2,000

4,000

6,000

Materials cost per unit ……………

$2,000

$3,000

Costs …………………………..………

Conversion costs:

Conversion cost per unit in plant ……………………

$2,000 per unit.

(@ $2,000 per unit) ……………….

$12,000,000

Material cost …………………………

Total cost …………………………..…

Number of units …………………….

6-44. (30 Minutes) Operations Costing: S. Lee Enterprises.

The unit costs are:

SL1: …………….

$2,200

SL2: …………….

$2,700

SL1

SL2

Total

Number of units …………………….

1,300

1,800

3,100

Materials cost per unit ……………

$900

$1,400

Costs …………………………..………

Conversion costs:

Conversion cost per unit in plant ……………………

$1,300 per unit.

(@ $1,300 per unit) ……………….

Material cost …………………………

1,170,000

2,520,000

Total cost …………………………..…

Number of units …………………….

6-45. (30 Minutes) Operations Costing: Organic Grounds.

The unit costs are:

Star: …………….

$10.60

Bucks: ………….

$12.60

Star

Bucks

Total

Number of pounds …………………

5,000

20,000

25,000

Materials cost per pound ………..

Costs …………………………………..

Conversion costs:

Cost per pound in plant ………….

$6.60 per pound.

(@ $6.60 per pound) ……………..

Material cost …………………………

Total cost ……………………………..

Number of pounds …………………

Conversion cost

Solutions to Problems

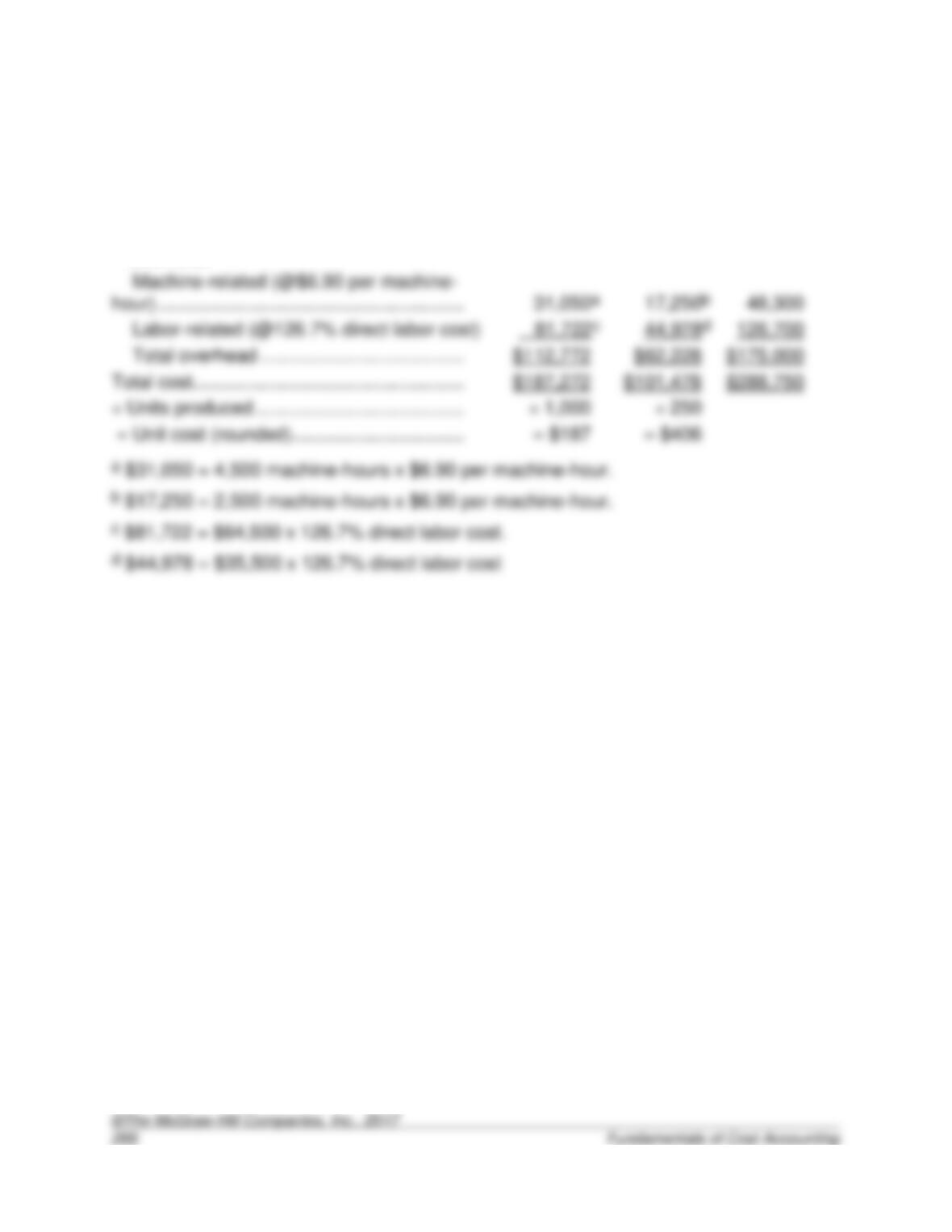

6-46. (30 Minutes) Product Costing: Tiger Furnishings.

The unit costs are: Basic: $187.38 (rounded) and Dominator: $405.50

Basic

Dominator

Total

Direct materials ……………………………………………………

$10,000

$3,750

$13,750

Direct labor ………………………………………………………….

64,500

35,500

100,000

62,125

Total costs …………………………………………………………..

Units produced …………………………………………………….

6-47. (30 Minutes) Product Costing: Tiger Furnishings.

The unit costs are: Basic: $187 and Dominator: $407

Basic

Dominator

Total

Direct materials ………………………………………………

$ 10,000

$3,750

$13,750

Direct labor …………………………………………………….

64,500

35,500

100,000

Total costs ……………………………………………………..

Units produced ……………………………………………….

6-48. (30 Minutes) Product Costing—Ethical Issues: Tiger Furnishings.

a. The unit costs are different because the two products use the machine hours and

direct labor costs in different proportions. The Basic model is more machine

6-49. (30 Minutes) Two-Stage Allocation and Product Costing: Donovan &

Parents.

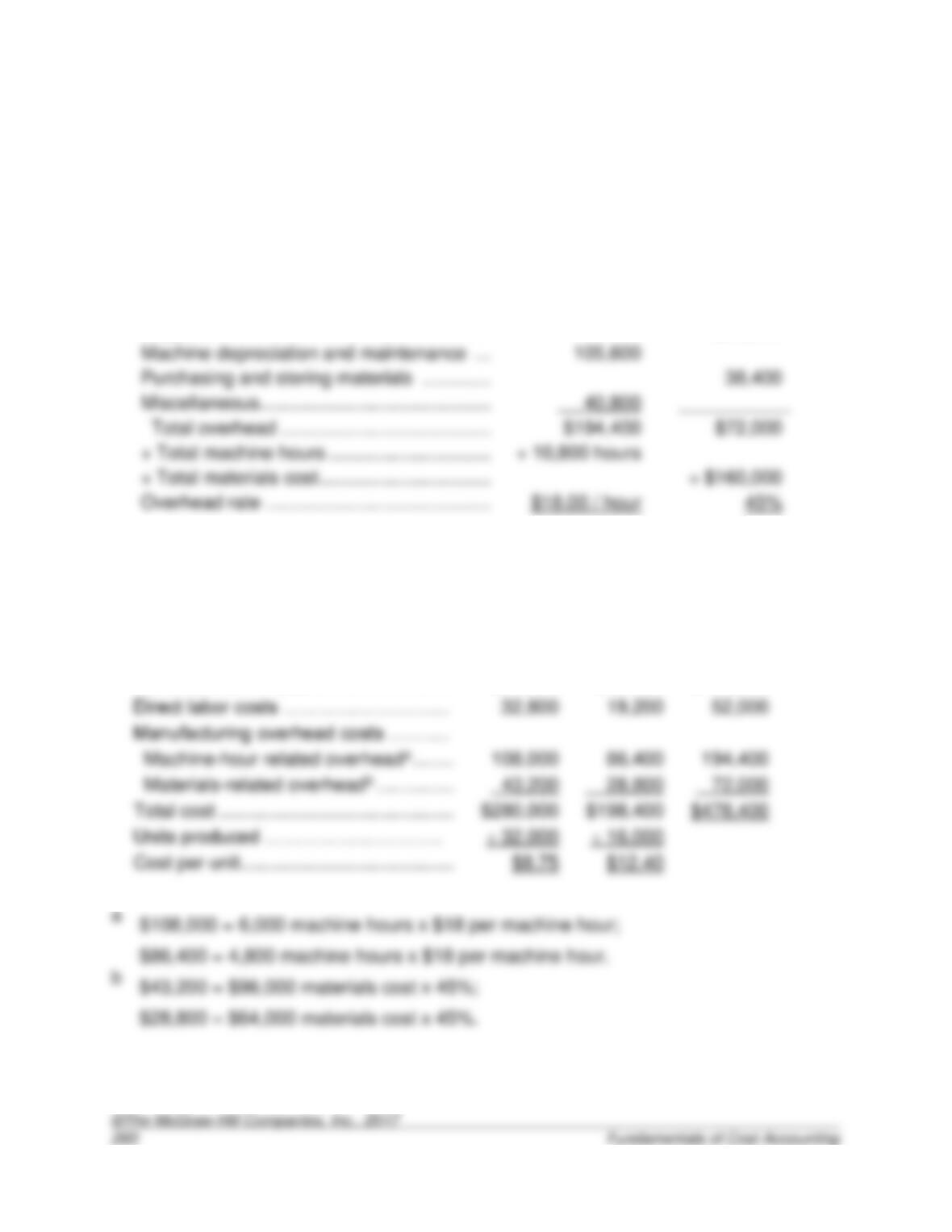

a. The overhead rates are $18 per machine hour and 45% of direct-materials cost.

Account

Machine-Hour

Related

Materials

Related

Utilities …………………………. ……………..

$ 48,000

Supplies …………………………………………….

$33,600

38,400

Miscellaneous ……………………………………..

_____________________________________

÷ Total materials cost …………………………...

b. The cost per unit of output is $8.75 for jerseys and $12.40 for shorts.

Jerseys

Shorts

Total

Machine hours used …………………………………….

6,000

4,800

10,800

Direct materials costs ………………….

$96,000

$64,000

$160,000

Direct labor costs ………………………

Manufacturing overhead costs ……….

86,400

Total cost …………………………………………………..

Units produced ………………………..

Cost per unit ……………………………………………….

$12.40

6-50. (30 Minutes) Two-Stage Allocation and Product Costing: Owl-Eye

Radiologists.

a. The overhead rates are $46 per equipment hour and $50 per direct labor hour.

Account

Equipment-

Hour Related

Direct-Labor

Hour Related

Utilities …………………………. ………………..

$ 4,800

Supplies ……………………………………………….

$12,600

Miscellaneous ………………………………………..

_____________________________________

÷ Total labor hours ………………………………….

b. The costs per patient are $114.75 per hospital patient hour and $29.44 per other

patient.

Hospital

Patients

Other

Patients

Total

Equipment hours used …………………………………

240

120

360

Direct labor-hours ……………………………………….

480

180

660

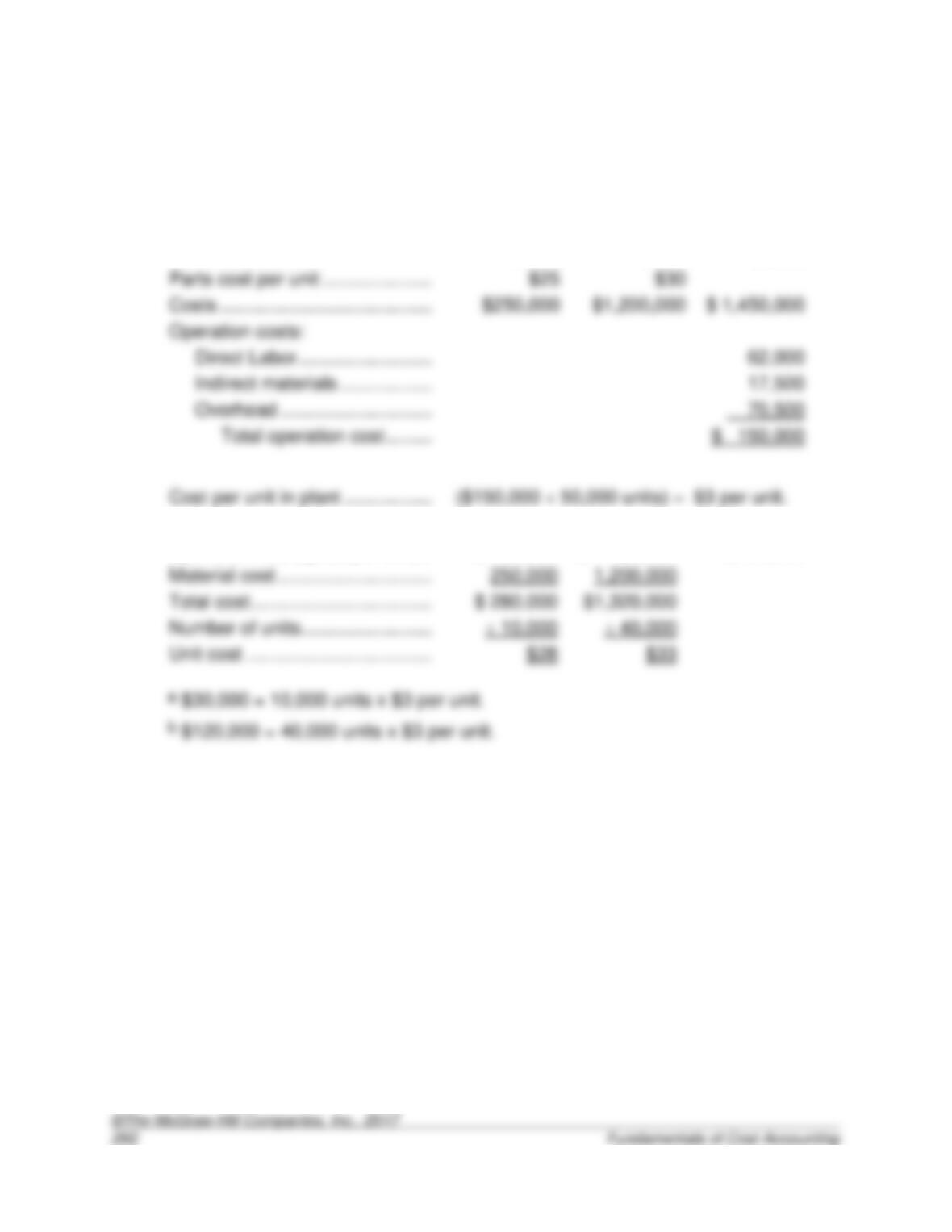

6-51. (30 Minutes) Operations Costing: Vermont Instruments.

The unit costs are:

Fin-X: ……

$28

Sci-X: ……

$33

Fin-X

Sci-X

Total

Number of units …………………….

10,000

40,000

50,000

Parts cost per unit …………………

Costs …………………………………..

Operation costs:

62,000

Cost per unit in plant ……………..

($150,000 ÷ 50,000 units) =

$3 per unit.

Operation cost (@ $3 per unit) ..

$ 30,000a

$ 120,000b

$150,000

Material cost …………………………

Total cost ……………………………..

Number of units …………………….

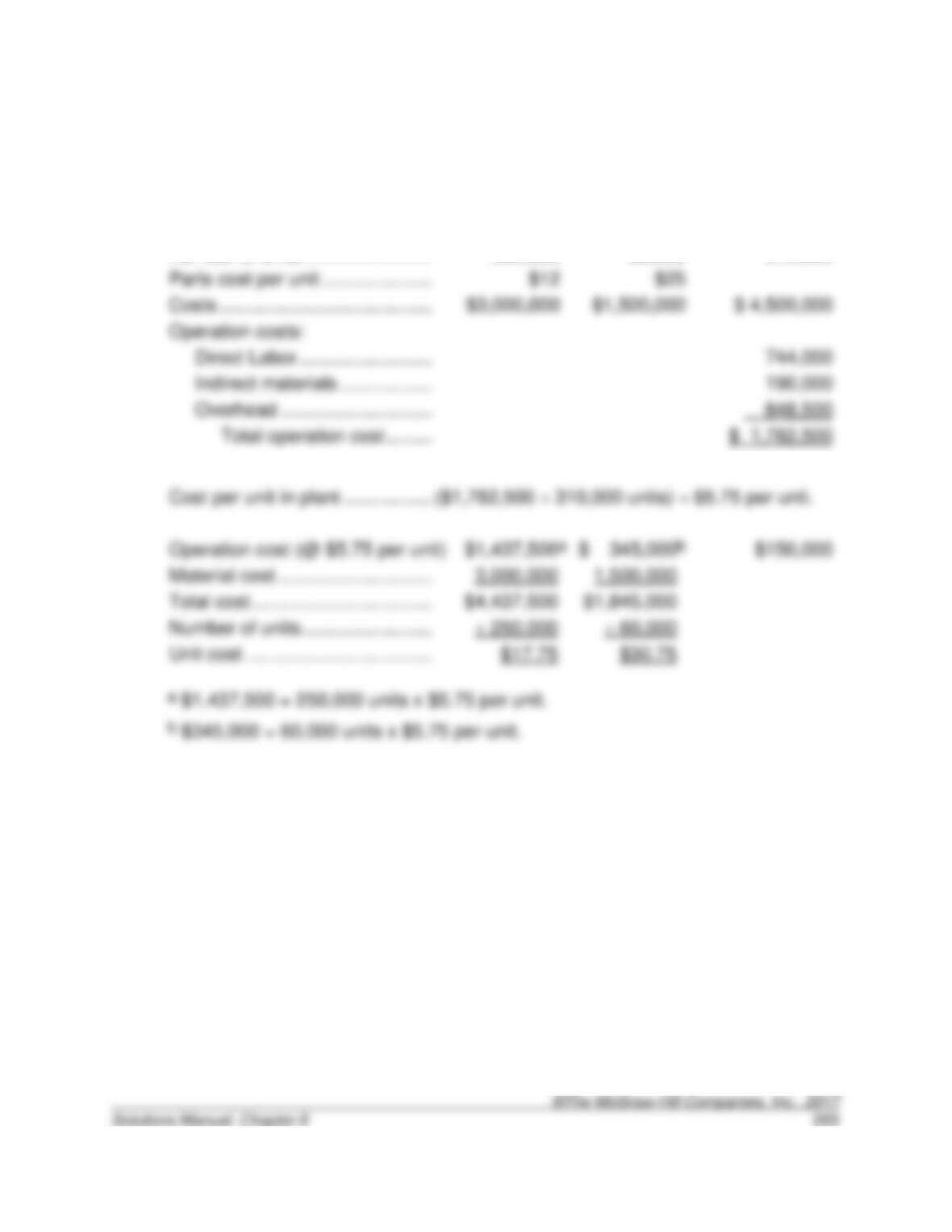

6-52. (30 Minutes) Operation Costing: DiDonato Supplies.

The unit costs are:

Basic: ……

$17.75

Laser: ……

$30.75

Basic

Laser

Total

Number of units …………………….

250,000

60,000

310,000

Parts cost per unit …………………

Costs …………………………………..

Operation costs:

744,000

Cost per unit in plant ……………..

$5.75 per unit.

Operation cost (@ $5.75 per unit) ………………….

$150,000

Material cost …………………………

Total cost ……………………………..

Number of units …………………….

6-53. (45 Minutes) Account Analysis, Two-Stage Allocation, and Product

Costing: Tiger Furnishings.

a. Cost Flow Diagram

Overhead

6-53. (continued)

b.

Basic

$187

Dominator

$406

Basic

Dominator

Total

Units Produced …………………………………….

1,000

250

1,250

Machine hours ……………………………………..

7,000

Direct labor hours …………………………………

3,000

2,000

5,000

Direct materials…………………………………….

$ 13,750

Direct labor ………………………………………….

64,500

Manufacturing Overhead

Machine-hour

related

Direct labor

cost related

Utilities ……………………………………………

$1,800

$0

$1,800

Supplies ………………………………………….

0

5,000

5,000

Training ………………………………………….

0

10,600

10,600

Supervision ……………………………………..

0

25,800

Machine depreciation ……………………….

32,100

Plant depreciation …………………………….

14,400

Miscellaneous ………………………………….

0

85,300

Total ………………………………………….

Burden Rates

Machine hour rate …………………………….

$6.90

Direct labor cost rate ………………………..

6-53. (continued)

Product Costing

Direct material …………………………………..

$ 10,000

$ 3,750

$ 13,750

Direct labor ……………………………………….

64,500

35,500

100,000

Overhead

Solutions to Integrative Cases

6-54. (45 Minutes) Product Costing, Cost Estimation, and Decision Making: Dolan

Products.

a. To determine product costs and margins, first calculate the Year 1 overhead rate:

Overhead rate

=

Total overhead

÷

Total direct labor hours

=

÷

=

÷

=

$25 per direct labor hour

Red

Yellow

Green

Direct materials ………………………….

$70.00

$50.00

$30.00

Direct labor (@$20)……………………..

Manufacturing overhead (@$25) …..

The product margins are:

Red

Yellow

Green

Price …………………………………………

$150.00

$100.00

$75.00

Product cost ……………………………….

160.00

6-54. (continued)

b. To determine product costs and margins, first calculate the Year 2 overhead rate:

Overhead rate

=

Total overhead

÷

Total direct labor hours

=

÷

(10,000 x 1.0 + 20,000 x 0.5)

=

÷

=

$32.50 per direct labor hour

Green

Direct materials ………………………………..

Direct labor (@$20) …………………………..

Manufacturing overhead (@$32.50) …….

The product margins are:

Yellow

Green

Price …………………………………………

Product cost ……………………………….

6-54. (continued)

c. Dolan should not drop Yellow.

The problem is that some of the manufacturing overhead is fixed and when a

We can use the high-low method from Chapter 5 to estimate the fixed overhead

component and the variable overhead rate. We only have two observations, so

these serve as the high and low observations.

Variable cost =

Cost at highest activity – cost at lowest activity

Highest activity – lowest activity

$750,000 – $650,000

Fixed costs

=

Total costs – variable costs

=

$750,000 – ($10.00 x 30,000)

Fixed costs

=

$650,000 – ($10.00 x 20,000)

6-55. (45 Minutes) Product Costing and Decision Making: Brunswick Parts.

This problem is designed to get students to understand the effect that cost systems

a.

The reported product costs include direct materials, direct labor, and manufacturing

overhead.

b.

Based on the reported product costs, it appears that Fredericton is the plant where