CHAPTER 6 Accounting for Merchandising Businesses

Appendix 2 Ex. 6-40

20Y6

Cost of Merchandise Sold 150,000

Appendix 2 Ex. 6-41

20Y3

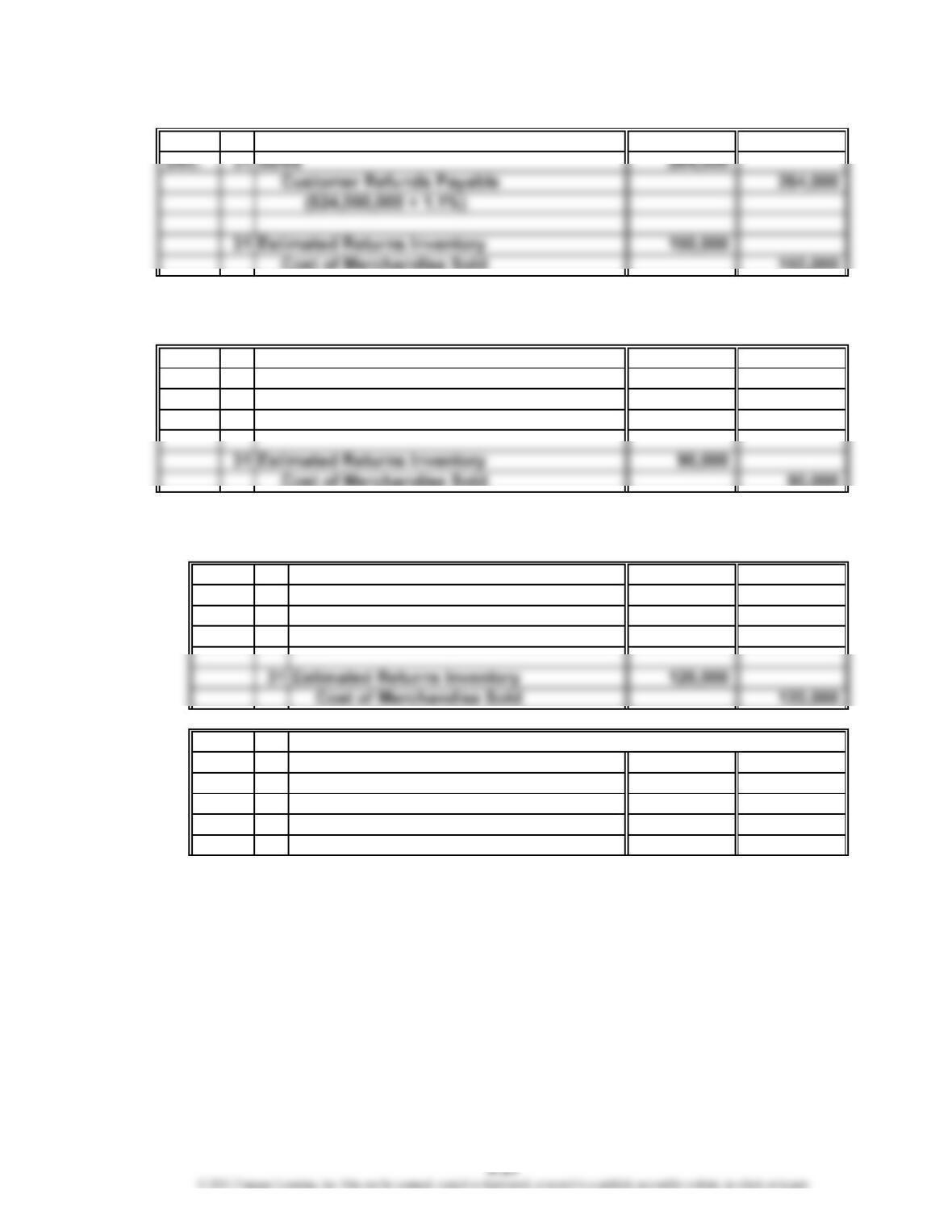

Dec. 31 Sales 140,400

Customer Refunds Payable 140,400

($7,800,000 × 1.8%)

Cost of Merchandise Sold 90,000

Appendix 2 Ex. 6-42

a. 20Y1

Dec. 31 Sales 180,000

Customer Refunds Payable 180,000

($12,000,000 × 1.5%)

b. 20Y2

Feb. 15 Customer Refunds Payable 8,000

Cash 8,000

15 Merchandise Inventory 5,500

Estimated Returns Inventory 5,500

CHAPTER 6 Accounting for Merchandising Businesses

Appendix 3 Ex. 6-43

(a) credit

(b) debit

(c) debit

Appendix 3 Ex. 6-44

Jan. 2 Purchases 18,200

Accounts Payable 18,200

13 Accounts Receivable [$37,300 – ($37,300 × 1%)] 36,927

Sales 36,927

15 Delivery Expense 215

Cash 215

Accounts Receivable 36,927

*[($18,200 – $2,750) × 2%]

Appendix 3 Ex. 6-45

a. Purchases discounts, Purchases returns and allowances

b. Freight in

CHAPTER 6 Accounting for Merchandising Businesses

Appendix 3 Ex. 6-46

a. Cost of merchandise sold:

Merchandise inventory, May 1, 20Y6 $ 380,000

Cost of merchandise purchased:

Purchases $3,800,000

Purchases returns and allowances (150,000)

Purchases discounts (80,000)

b. $2,310,000 ($5,850,000 – $3,540,000)

c. No. Gross profit would be the same if the perpetual inventory system was used.

Appendix 3 Ex. 6-47

Cost of merchandise sold:

Merchandise inventory, November 1 $ 28,000

Cost of merchandise purchased:

Purchases $475,000

Purchases returns and allowances (15,000)

CHAPTER 6 Accounting for Merchandising Businesses

Appendix 3 Ex. 6-48

Cost of merchandise sold:

Merchandise inventory, July 1 $ 190,850

Cost of merchandise purchased:

Purchases $1,126,000

Purchases returns and allowances (46,000)

Purchases discounts (23,000)

Appendix 3 Ex. 6-49

1. The schedule should begin with the June 1, 20Y3, not the May 31, 20Y4,

merchandise inventory.

2. Purchases returns and allowances and purchases discounts should be deducted

from (not added to) purchases.

A corrected schedule would appear as follows:

Cost of merchandise sold:

Merchandise inventory, June 1, 20Y3 $ 91,300

Cost of merchandise purchased:

Purchases $1,110,000

Purchases returns and allowances (55,000)

Purchases discounts (30,000)

CHAPTER 6 Accounting for Merchandising Businesses

Appendix 3 Ex. 6-50

Dec. 31 Merchandise Inventory (December 31) 480,000

Sales 2,220,000

Purchases Discounts 35,000

Purchases Returns and Allowances 45,000

Merchandise Inventory (January 1) 375,000

Purchases 1,760,000

Closing Entries

CHAPTER 6 Accounting for Merchandising Businesses

Prob. 6-1A

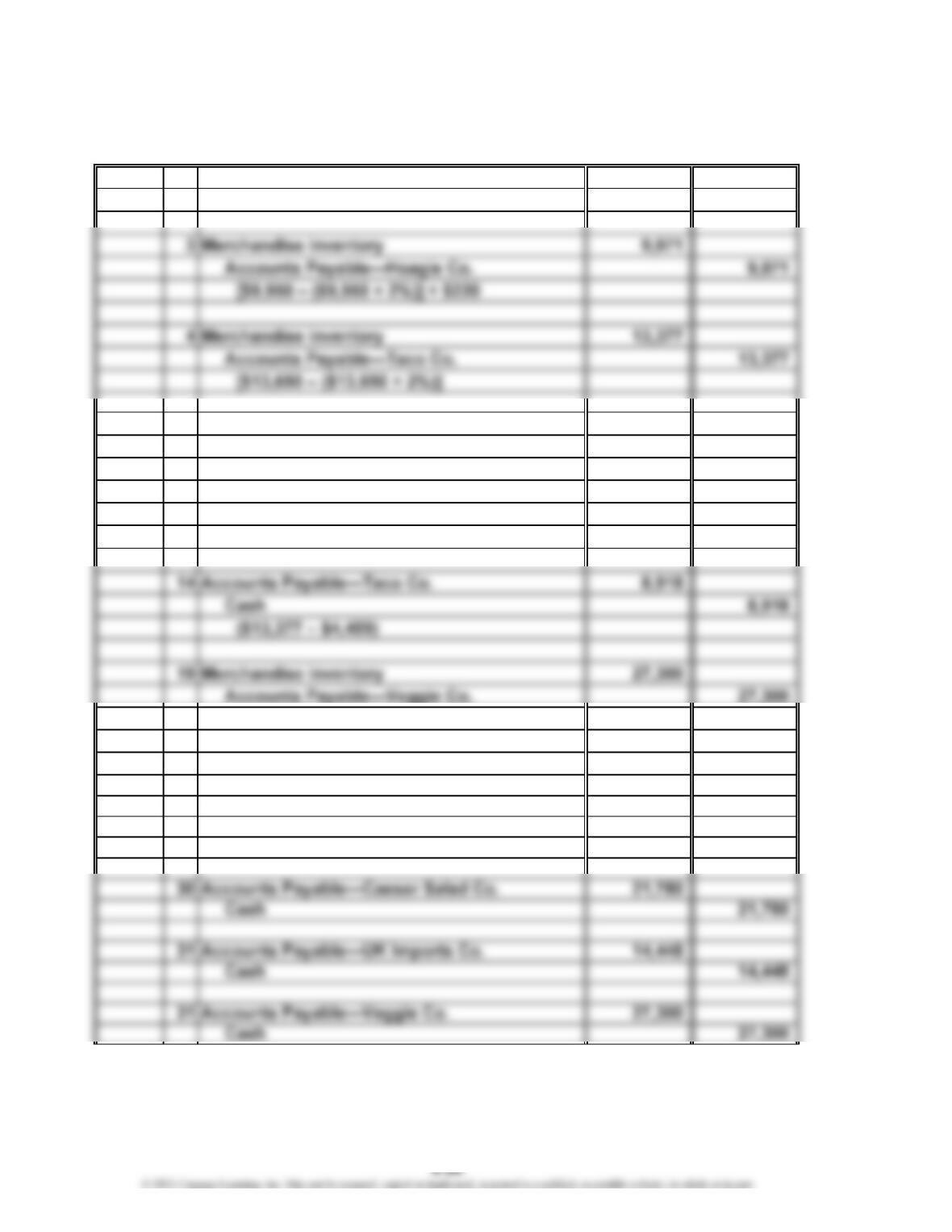

Oct. 1 Merchandise Inventory 14,448

Accounts Payable—UK Imports Co. 14,448

6 Accounts Payable—Taco Co. 4,459

Merchandise Inventory 4,459

[$4,550 – ($4,550 × 2%)]

13 Accounts Payable—Hoagie Co. 9,971

Cash 9,971

19 Merchandise Inventory 400

Cash 400

20 Merchandise Inventory 21,780

Accounts Payable—Caesar Salad Co. 21,780

[$22,000 – ($22,000 × 1%)]

PROBLEMS

CHAPTER 6 Accounting for Merchandising Businesses

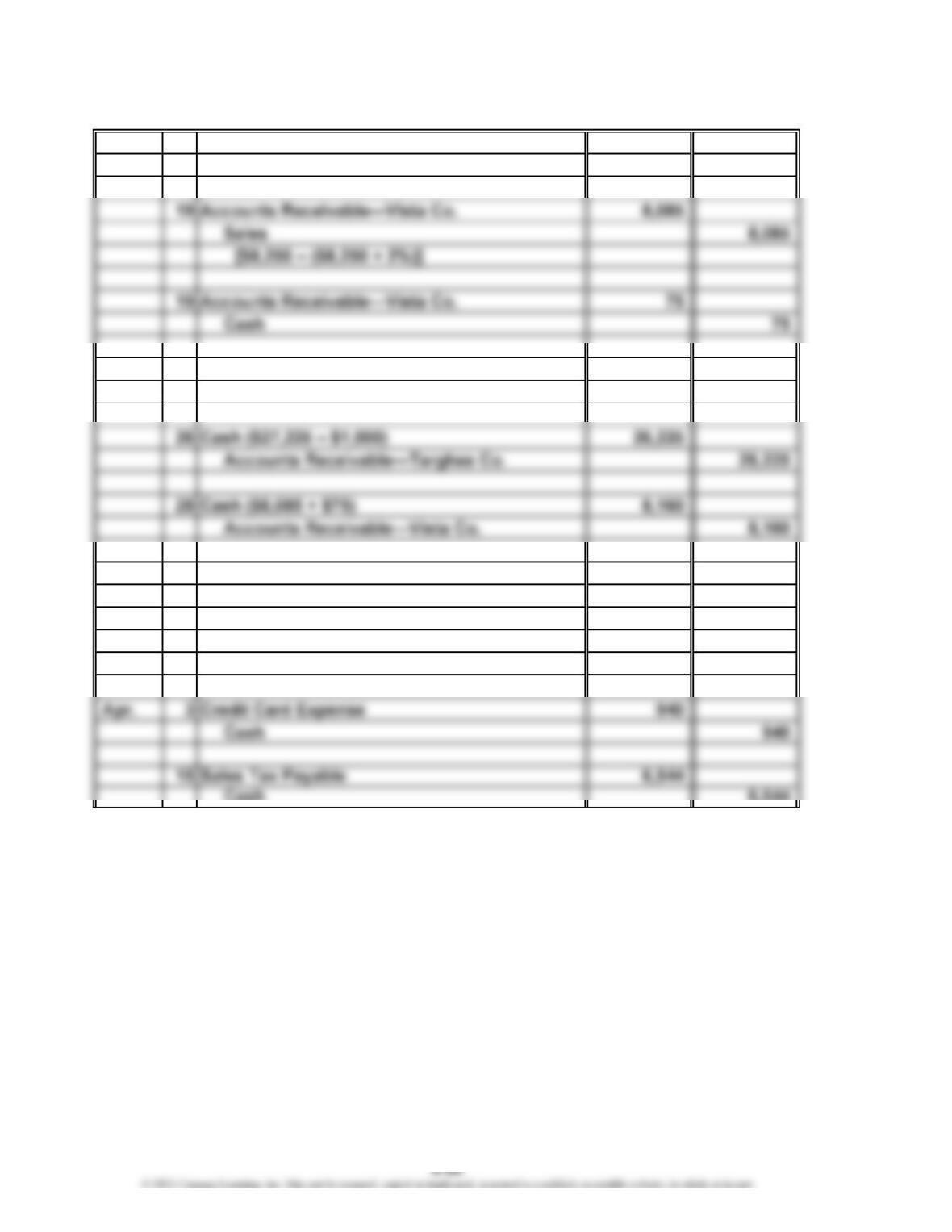

Prob. 6-2A

Mar. 2 Accounts Receivable—Equinox Co. 18,711

Sales 18,711

[$18,900 – ($18,900 × 1%)]

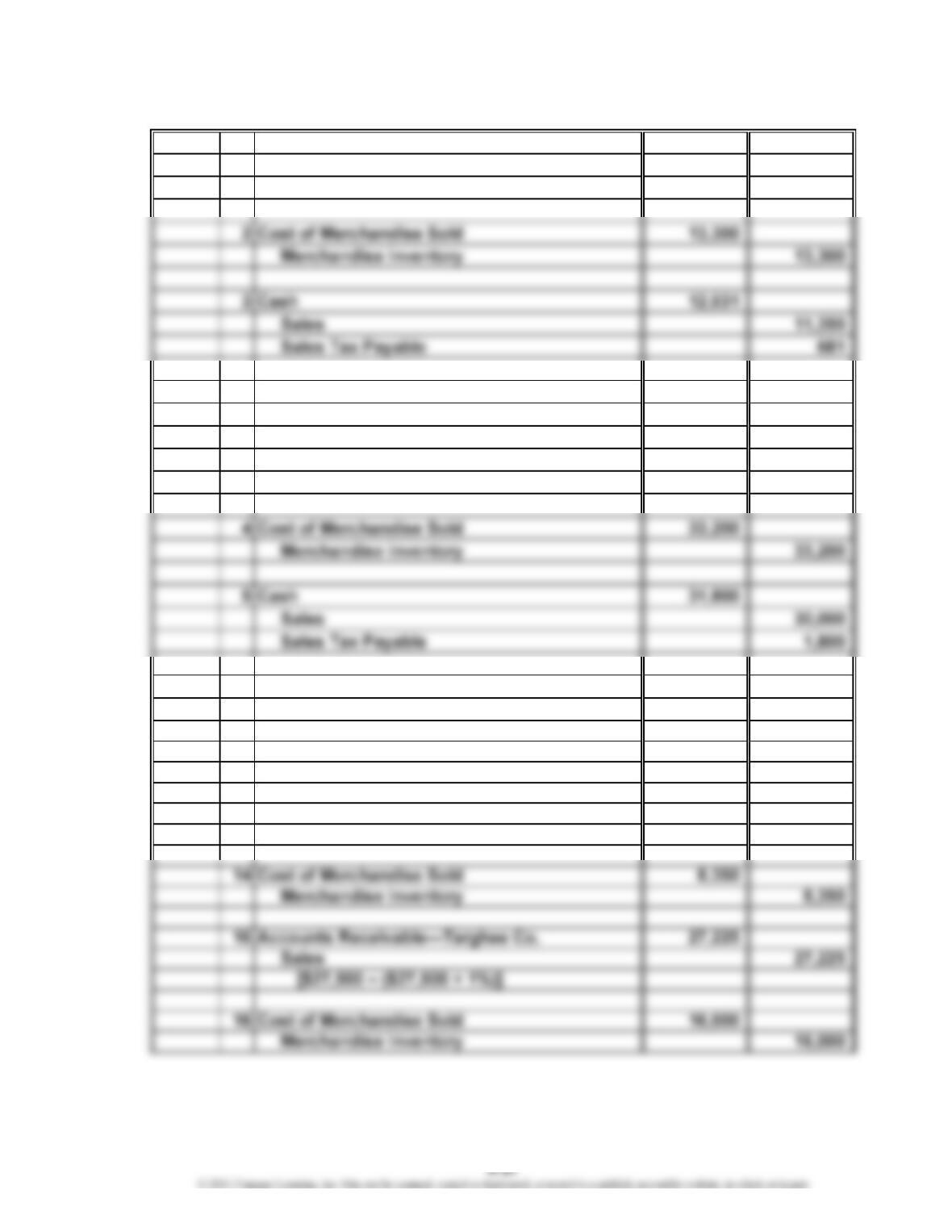

3 Cost of Merchandise Sold 7,000

Merchandise Inventory 7,000

4 Accounts Receivable—Empire Co. 55,400

Sales 55,400

5 Cost of Merchandise Sold 19,400

Merchandise Inventory 19,400

12 Cash 18,711

Accounts Receivable—Equinox Co. 18,711

14 Cash 13,700

Sales 13,700

CHAPTER 6 Accounting for Merchandising Businesses

Prob. 6-2A (Concluded)

Mar. 18 Customer Refunds Payable 1,000

Accounts Receivable—Targhee Co. 1,000

19 Cost of Merchandise Sold 5,000

Merchandise Inventory 5,000

31 Cash 55,400

Accounts Receivable—Empire Co. 55,400

31 Delivery Expense 5,600

Cash 5,600

Cash 6,544

CHAPTER 6 Accounting for Merchandising Businesses

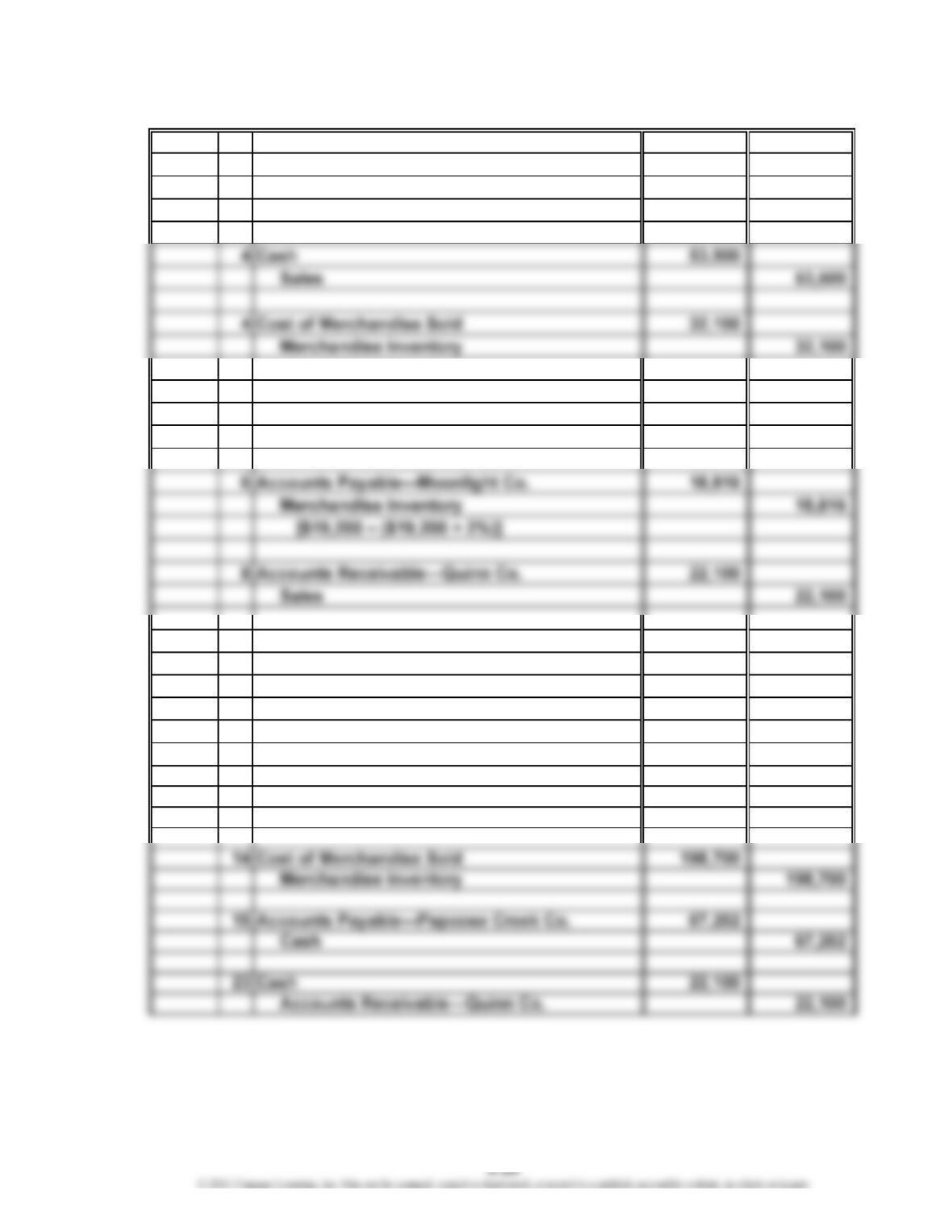

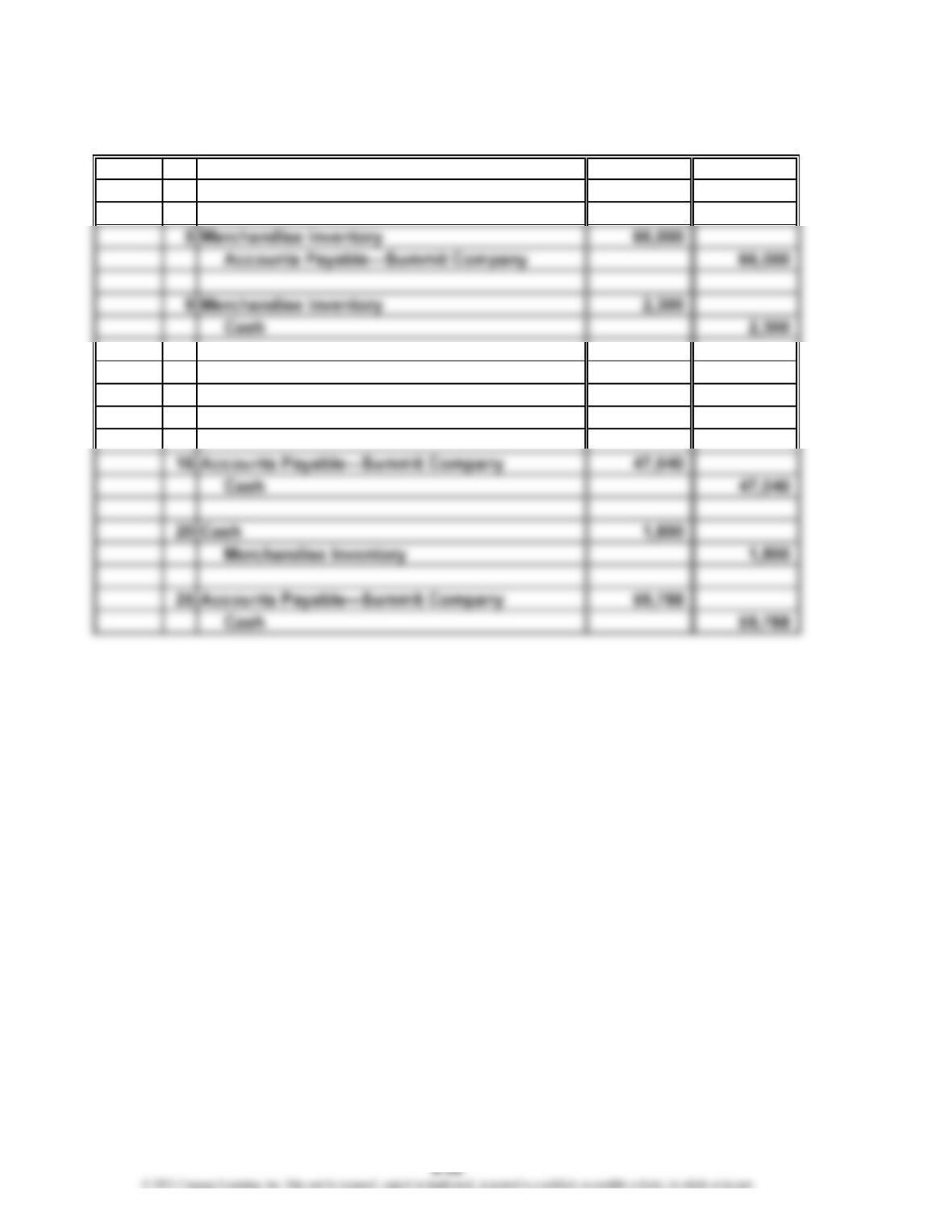

Prob. 6-3A

Nov. 3 Merchandise Inventory 88,200

Accounts Payable—Moonlight Co. 88,200

[$120,000 – ($120,000 × 25%)] = $90,000

[$90,000 – ($90,000 × 2%)]

5 Merchandise Inventory 67,202

Accounts Payable—Papoose Creek Co. 67,202

[$67,400 – ($67,400 × 2%) + $1,150]

8 Cost of Merchandise Sold 13,000

Merchandise Inventory 13,000

13 Accounts Payable—Moonlight Co. 69,384

Cash 69,384

($88,200 – $18,816)

14 Cash 335,000

Sales 335,000

CHAPTER 6 Accounting for Merchandising Businesses

Prob. 6-3A (Concluded)

Nov. 24 Accounts Receivable—Rabel Co. 79,992

Sales 79,992

[$80,800 – ($80,800 × 1%)]

CHAPTER 6 Accounting for Merchandising Businesses

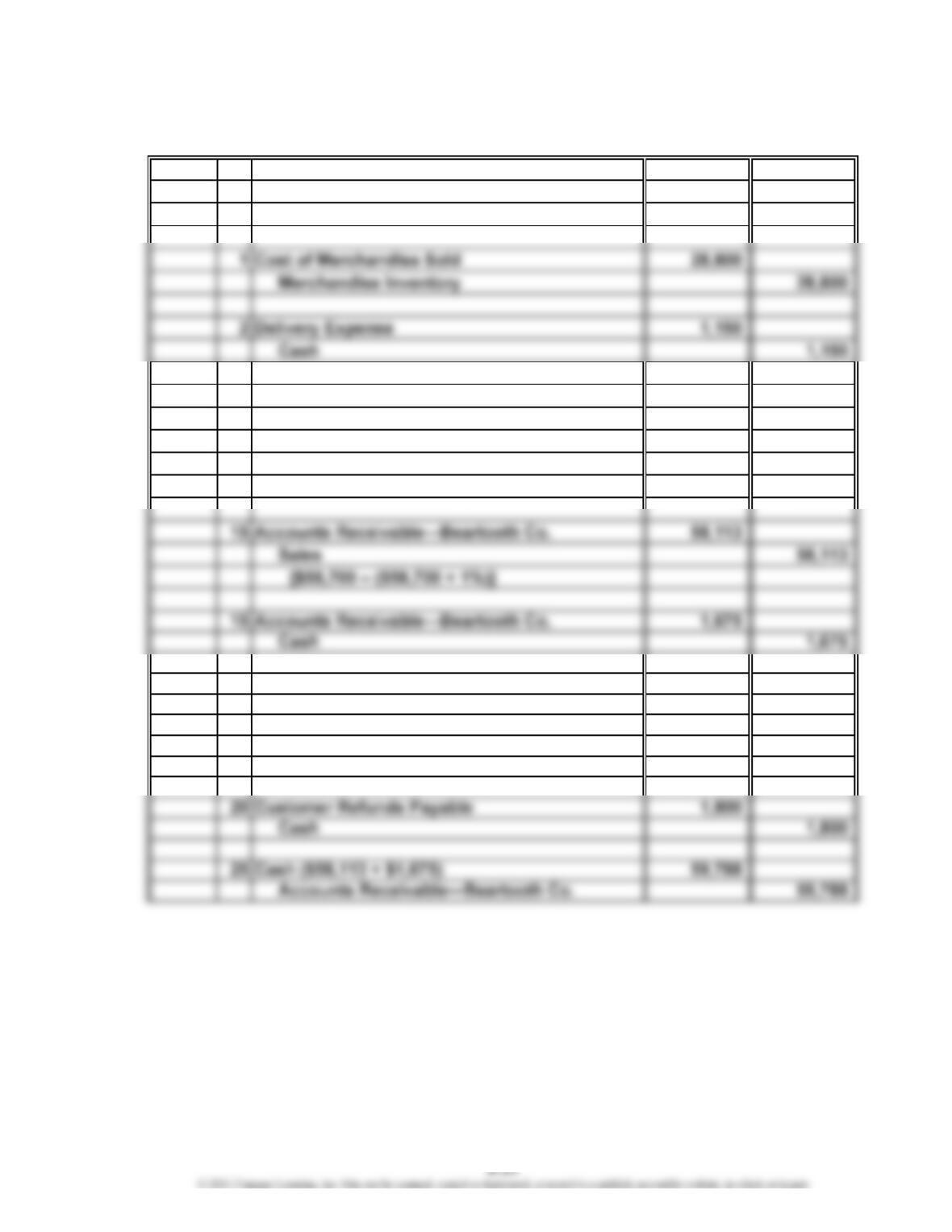

Prob. 6-4A

1.

Aug. 1 Accounts Receivable—Beartooth Co. 47,040

Sales 47,040

[$48,000 – ($48,000 × 2%)]

5 Accounts Receivable—Beartooth Co. 66,000

Sales 66,000

5 Cost of Merchandise Sold 40,000

Merchandise Inventory 40,000

15 Cost of Merchandise Sold 35,000

Merchandise Inventory 35,000

16 Cash 47,040

Accounts Receivable—Beartooth Co. 47,040

CHAPTER 6 Accounting for Merchandising Businesses

Prob. 6-4A (Concluded)

2.

Aug. 1 Merchandise Inventory 47,040

Accounts Payable—Summit Company 47,040

15 Merchandise Inventory 59,788

Accounts Payable—Summit Company 59,788

{[$58,700 – ($58,700 × 1%)] + $1,675}

CHAPTER 6 Accounting for Merchandising Businesses

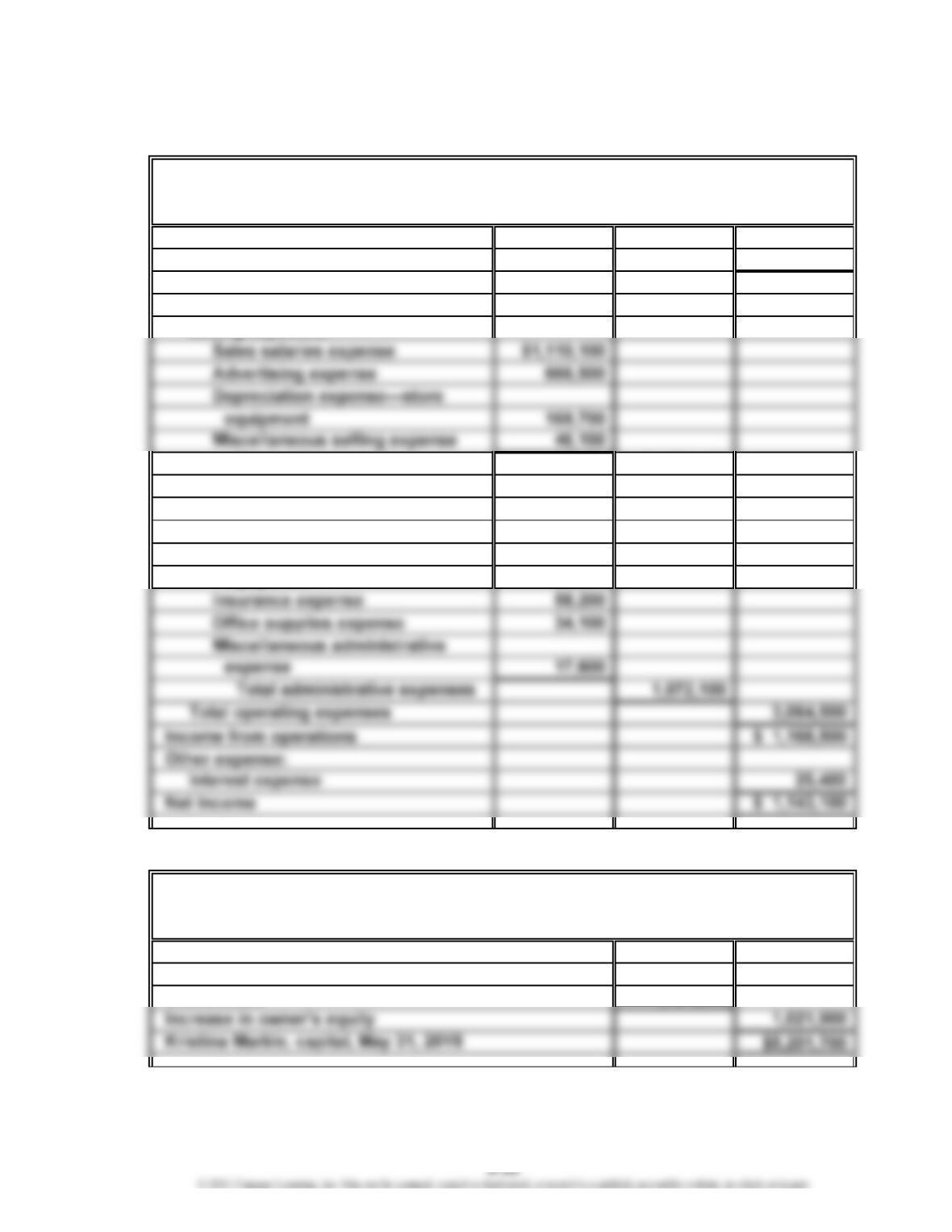

Prob. 6-5A

1.

Sales $13,746,000

Cost of merchandise sold 9,513,000

Gross profit $ 4,233,000

Expenses:

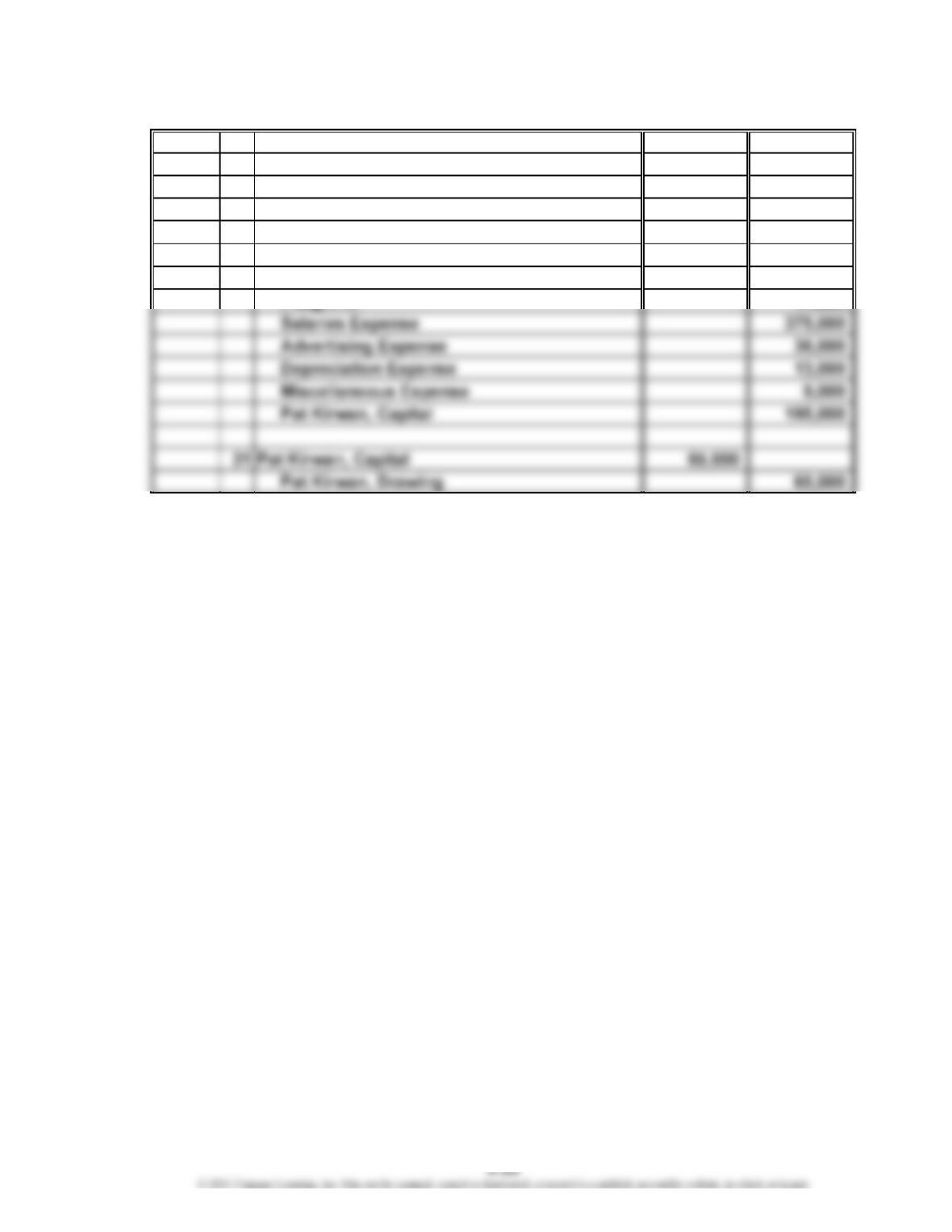

Selling expenses:

Total selling expenses $1,992,400

Administrative expenses:

Office salaries expense $ 787,700

Rent expense 113,900

Depreciation expense—office

equipment 60,600

2.

Kristina Marble, capital, June 1, 20Y7 $4,179,800

Net income for the year $1,143,100

Withdrawals (121,200)

Druid Hills Co.

Statement of Owner’s Equity

For the Year Ended May 31, 20Y8

Druid Hills Co.

Income Statement

For the Year Ended May 31, 20Y8

CHAPTER 6 Accounting for Merchandising Businesses

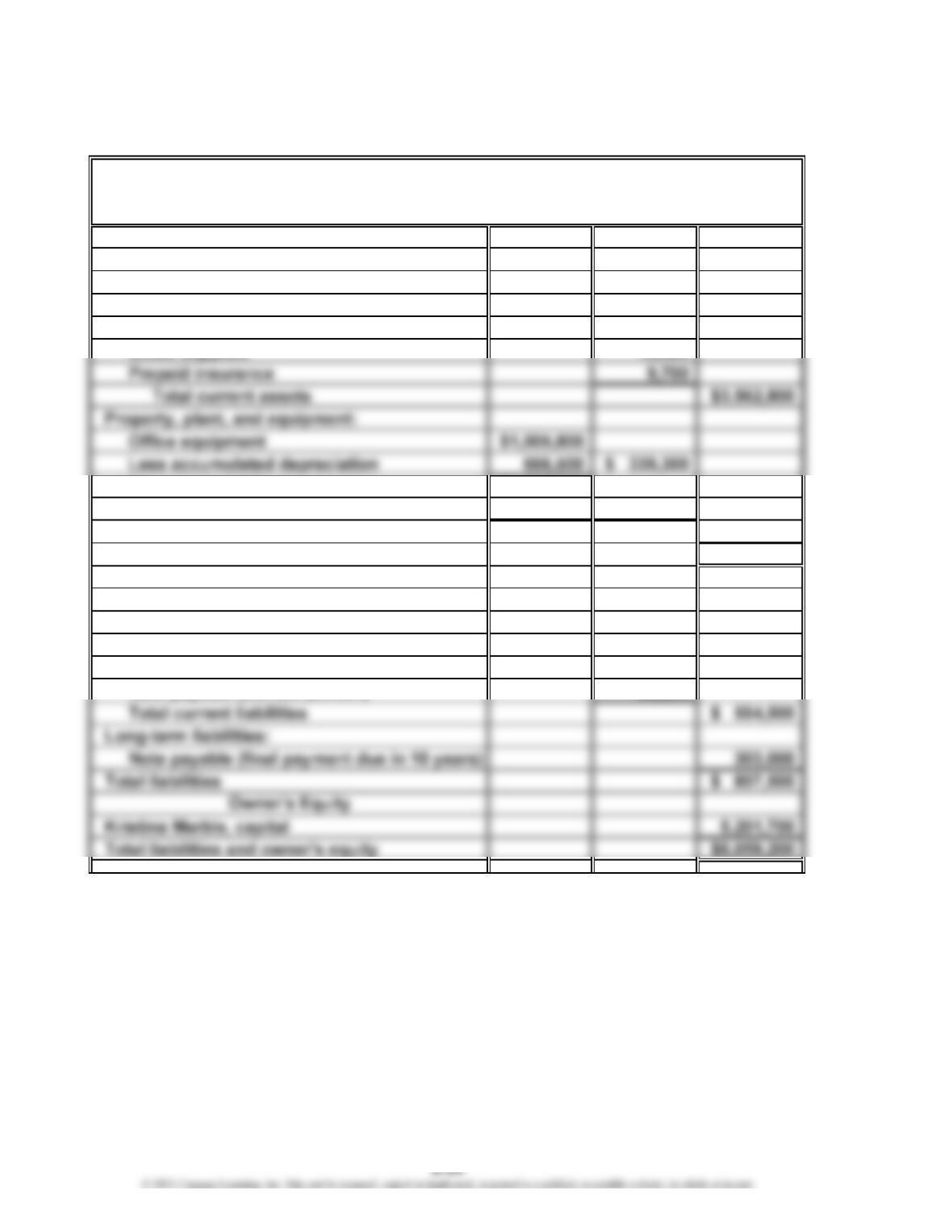

Prob. 6-5A (Concluded)

3.

Current assets:

Cash $ 290,800

Accounts receivable 1,170,600

Merchandise inventory 2,075,300

Store equipment $4,362,700

Less accumulated depreciation 2,205,600 2,157,100

Total property, plant, and equipment 2,496,400

Total assets $6,059,200

Current liabilities:

Accounts payable $ 395,100

Customer refunds payable 48,500

Salaries payable 50,300

4. The multiple-step form of income statement contains various sections for revenues

and expenses, with intermediate balances, and concludes with net income. In the

single-step form, the total of all expenses is deducted from the total of all revenues.

There are no intermediate balances.

Druid Hills Co.

Balance Sheet

May 31, 20Y8

Assets

Liabilities

CHAPTER 6 Accounting for Merchandising Businesses

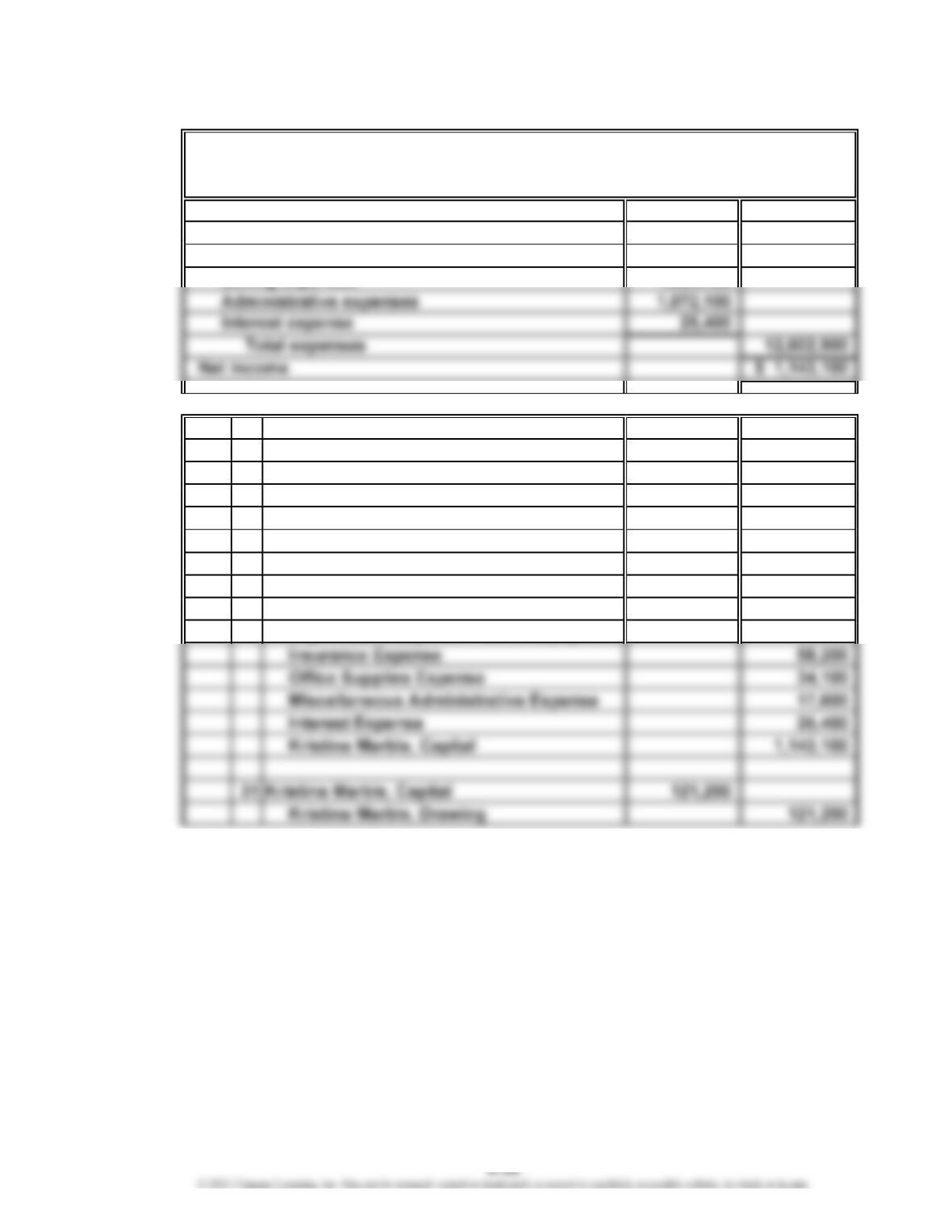

Prob. 6-6A

1.

Sales $13,746,000

Expenses:

Cost of merchandise sold $9,513,000

2. 20Y8

May 31 Sales 13,746,000

Cost of Merchandise Sold 9,513,000

Sales Salaries Expense 1,110,100

Advertising Expense 666,500

Depreciation Expense—Store Equipment 169,700

Miscellaneous Selling Expense 46,100

Office Salaries Expense 787,700

Rent Expense 113,900

Depreciation Expense—Office Equipment 60,600

Closing Entries

Druid Hills Co.

Income Statement

For the Year Ended May 31, 20Y8

CHAPTER 6 Accounting for Merchandising Businesses

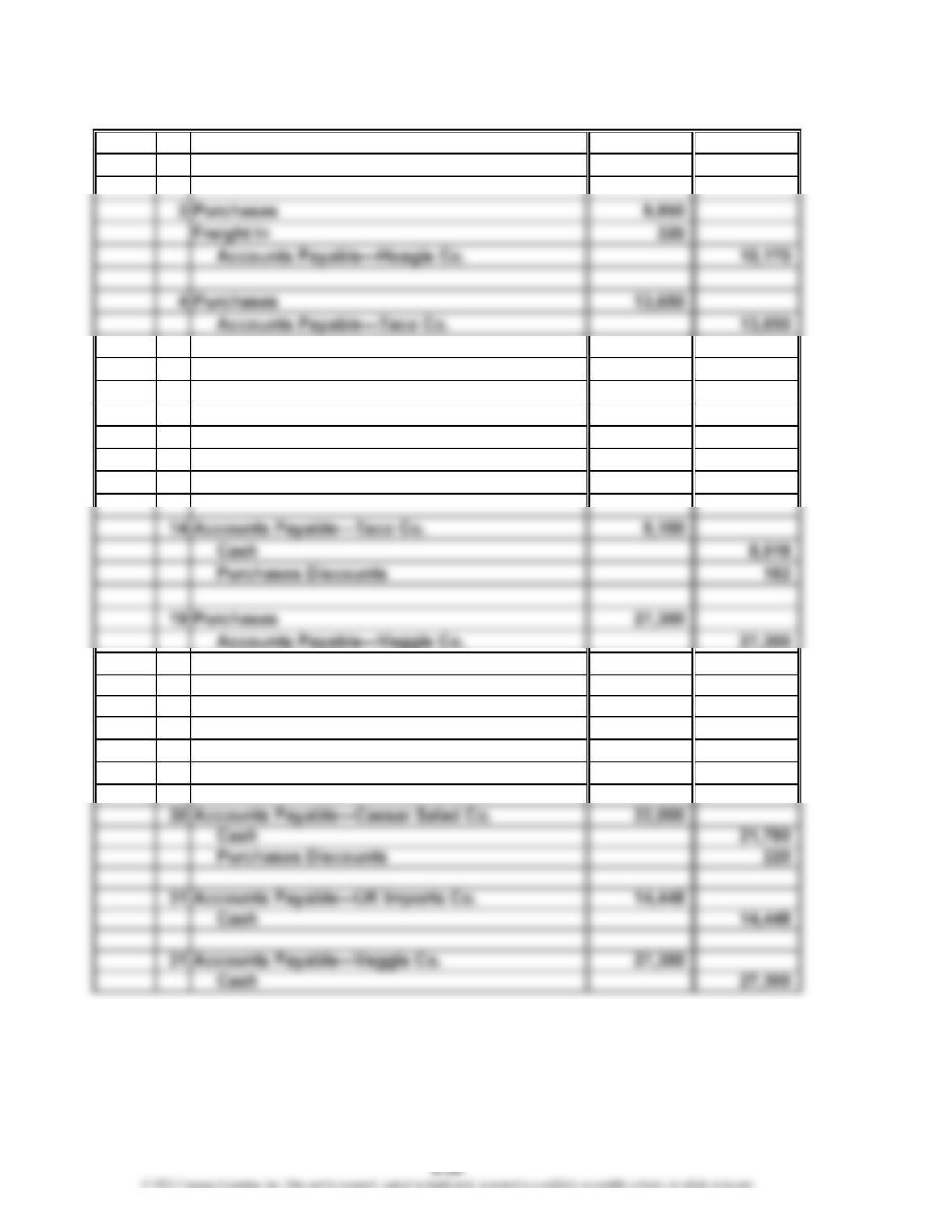

Appendix 3 Prob. 6-7A

Oct. 1 Purchases 14,448

Accounts Payable—UK Imports Co. 14,448

6 Accounts Payable—Taco Co. 4,550

Purchases Returns and Allowances 4,550

13 Accounts Payable—Hoagie Co. 10,170

Cash 9,971

Purchases Discounts ($9,950 × 2%) 199

19 Freight In 400

Cash 400

20 Purchases 22,000

Accounts Payable—Caesar Salad Co. 22,000

CHAPTER 6 Accounting for Merchandising Businesses

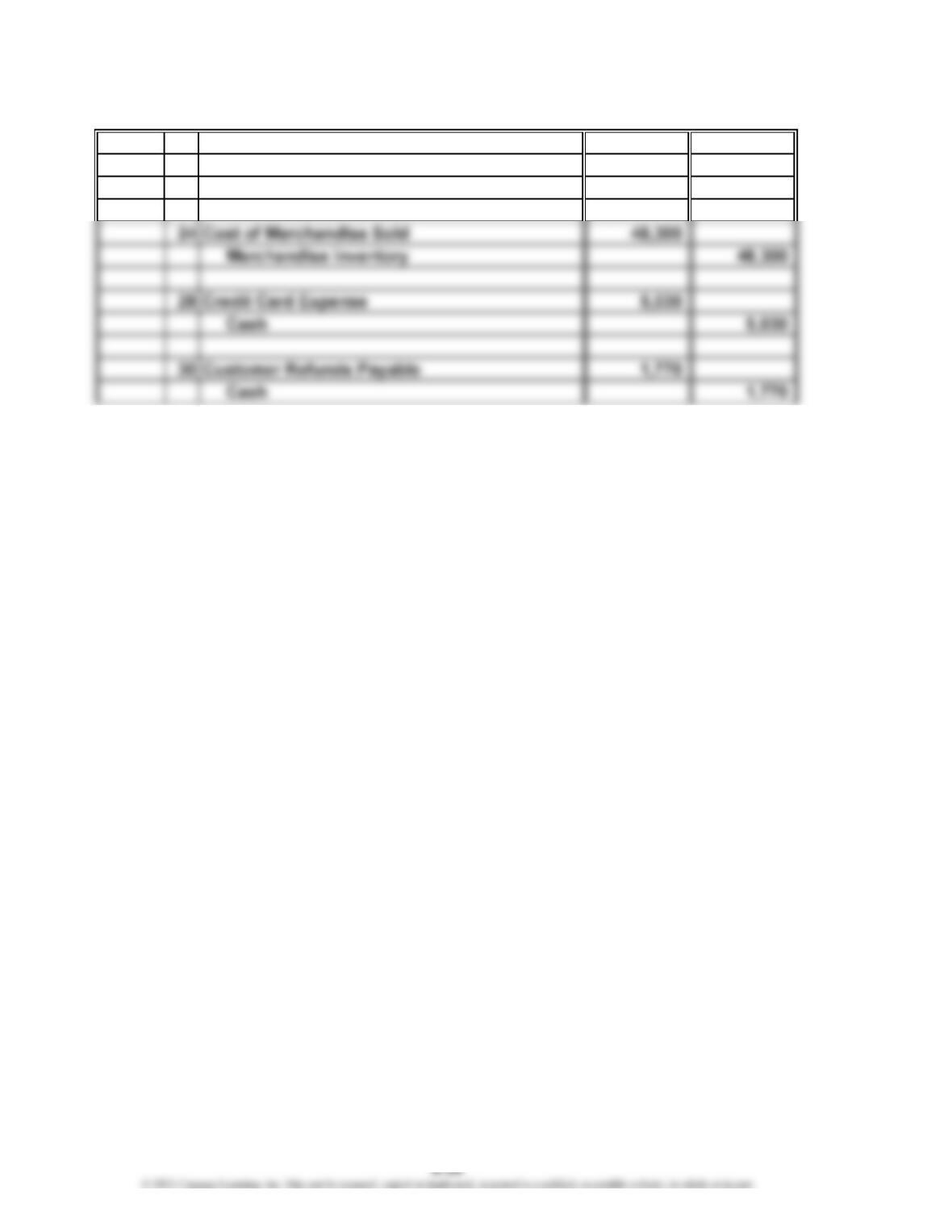

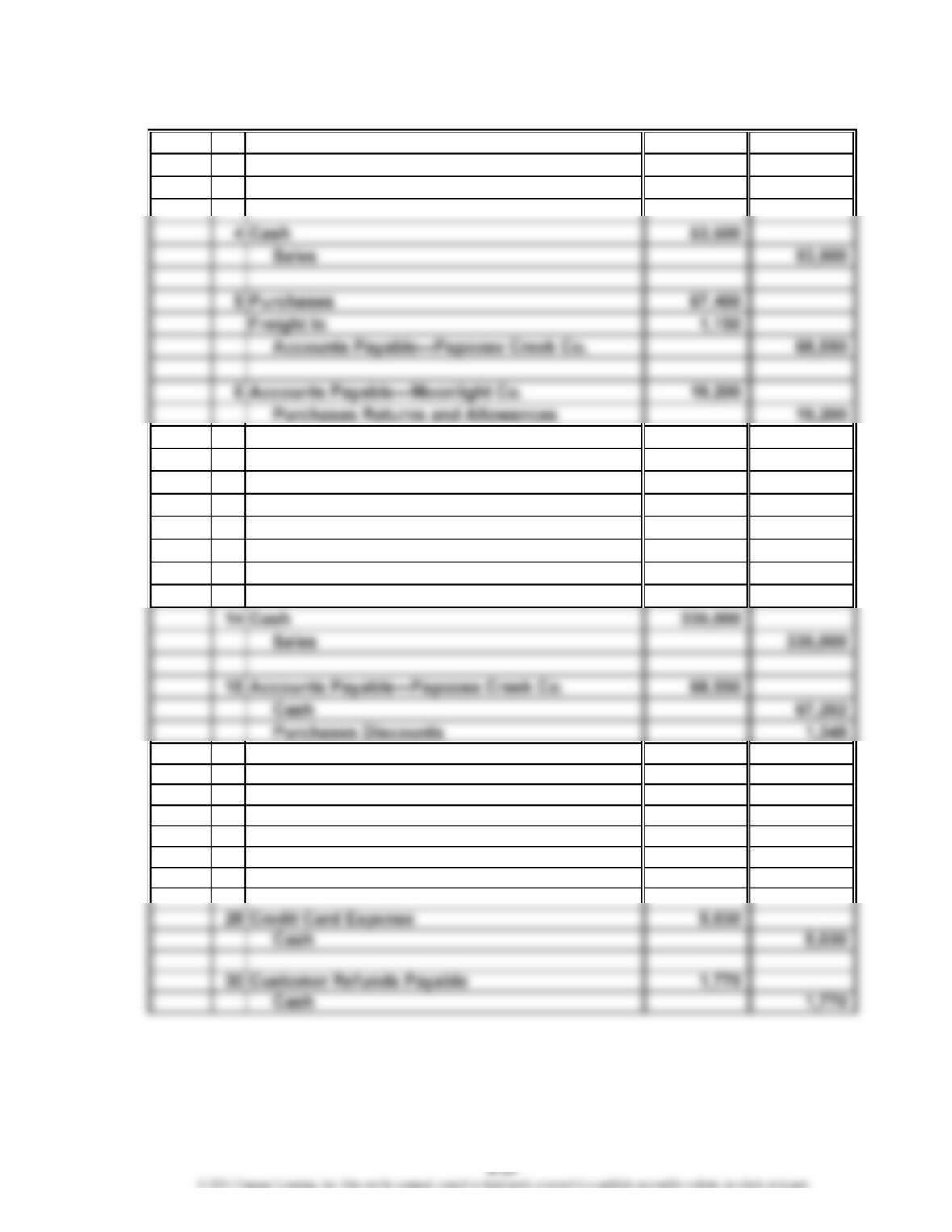

Appendix 3 Prob. 6-8A

Nov. 3 Purchases 90,000

Accounts Payable—Moonlight Co. 90,000

[$120,000 – ($120,000 × 25%)]

8 Accounts Receivable—Quinn Co. 22,100

Sales 22,100

13 Accounts Payable—Moonlight Co. 70,800

Cash 69,384

Purchases Discounts 1,416

23 Cash 22,100

Accounts Receivable—Quinn Co. 22,100

24 Accounts Receivable—Rabel Co. 79,992

Sales 79,992

[$80,800 – ($80,800 × 1%)]

CHAPTER 6 Accounting for Merchandising Businesses

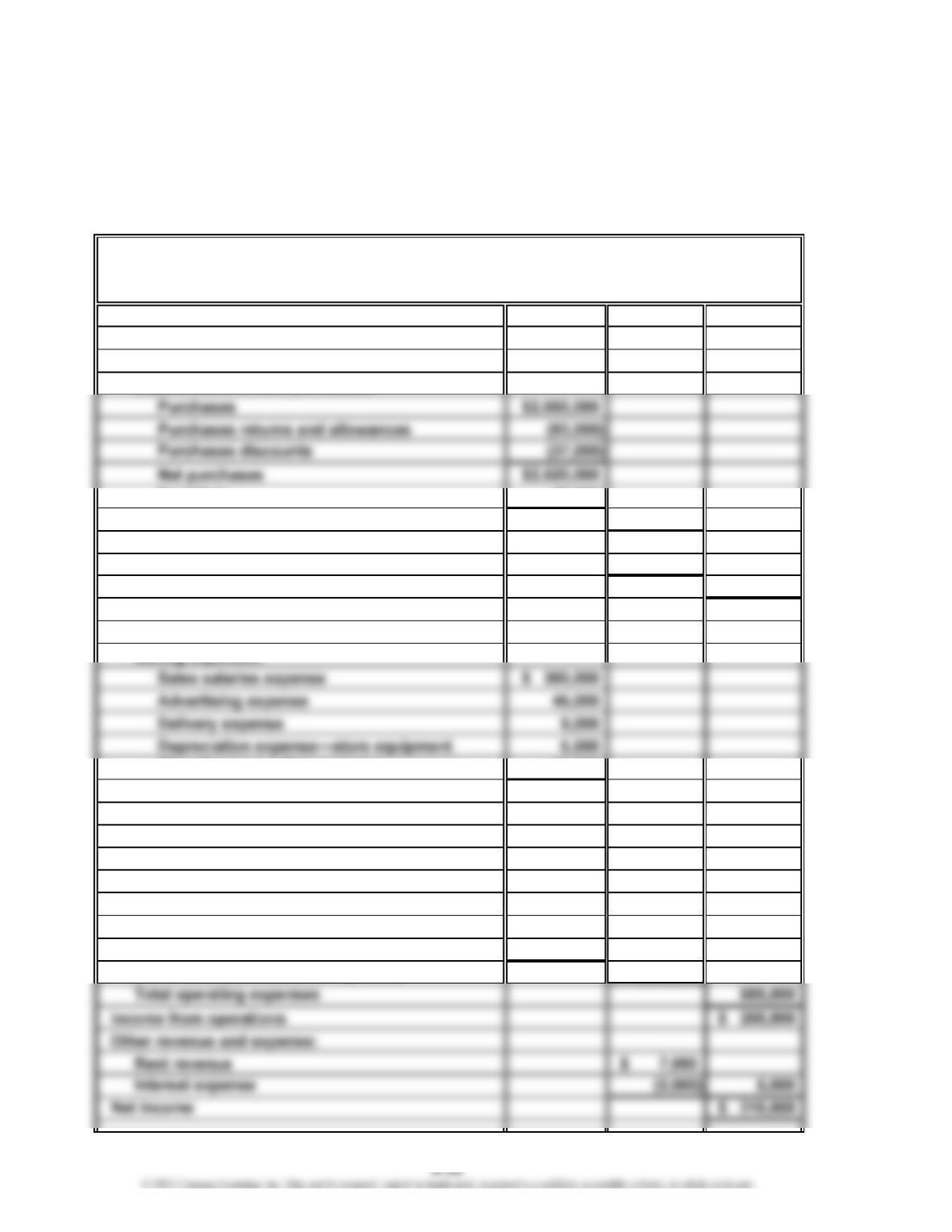

Appendix 3 Prob. 6-9A

1. Wyman Company uses a periodic inventory system because it maintains accounts

for purchases, purchases returns and allowances, purchases discounts, and

freight in.

2.

Sales $3,280,000

Cost of merchandise sold:

Merchandise inventory, January 1, 20Y6 $ 257,000

Cost of merchandise purchased:

Freight in 48,000

Total cost of merchandise purchased 2,568,000

Merchandise available for sale $2,825,000

Merchandise inventory, December 31, 20Y6 (335,000)

Cost of merchandise sold 2,490,000

Gross profit $ 790,000

Expenses:

Miscellaneous selling expense 12,000

Total selling expenses $ 372,000

Administrative expenses:

Office salaries expense $ 175,000

Rent expense 28,000

Insurance expense 3,000

Office supplies expense 2,000

Depreciation expense—office equipment 1,500

Miscellaneous administrative expense 3,500

Total administrative expenses 213,000

Wyman Company

Income Statement

For the Year Ended December 31, 20Y6

CHAPTER 6 Accounting for Merchandising Businesses

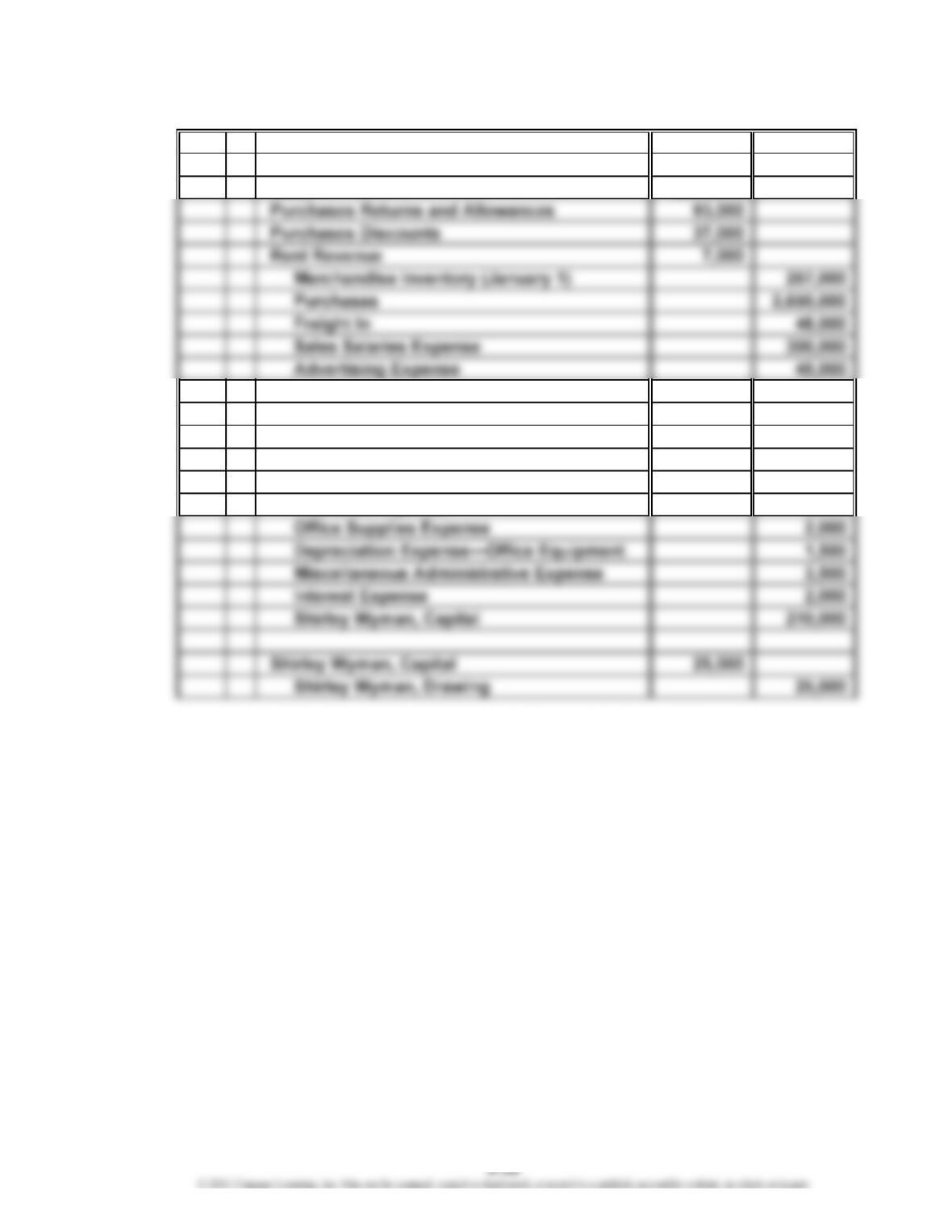

Appendix 3 Prob. 6-9A (Concluded)

3.

Dec. 31 Merchandise Inventory (December 31) 335,000

Sales 3,280,000

Delivery Expense 9,000

Depreciation Expense—Store Equipment 6,000

Miscellaneous Selling Expense 12,000

Office Salaries Expense 175,000

Rent Expense 28,000

Insurance Expense 3,000

4. $210,000, the same net income as under the periodic inventory system

Closing Entries

CHAPTER 6 Accounting for Merchandising Businesses

Prob. 6-1B

Mar. 1 Merchandise Inventory 43,035

Accounts Payable—Haas Co. 43,035

[$43,250 – ($43,250 × 2%)] + $650

13 Merchandise Inventory 15,239

Accounts Payable—Jost Co. 15,239

[$15,550 – ($15,550 × 2%)]

14 Accounts Payable—Jost Co. 3,675

Merchandise Inventory 3,675

[$3,750 – ($3,750 × 2%)]

19 Merchandise Inventory 6,370

Accounts Payable—Bickle Co. 6,370

[$6,500 – ($6,500 × 2%)]

23 Accounts Payable—Jost Co. ($15,239 – $3,675) 11,564

Cash 11,564