Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

EXERCISE 6-33 (45 MINUTES)

1.

Variable utility cost per hour

=

400 700

$2,600 $3,800

−

−

=

$4.00

Total utility cost at 700 hours …………………………………………………………….

Fixed cost per month ………………………………………………………………………..

Cost formula:

Monthly utility cost = $1,000 + $4.00 X , where X denotes hours of operation.

2.

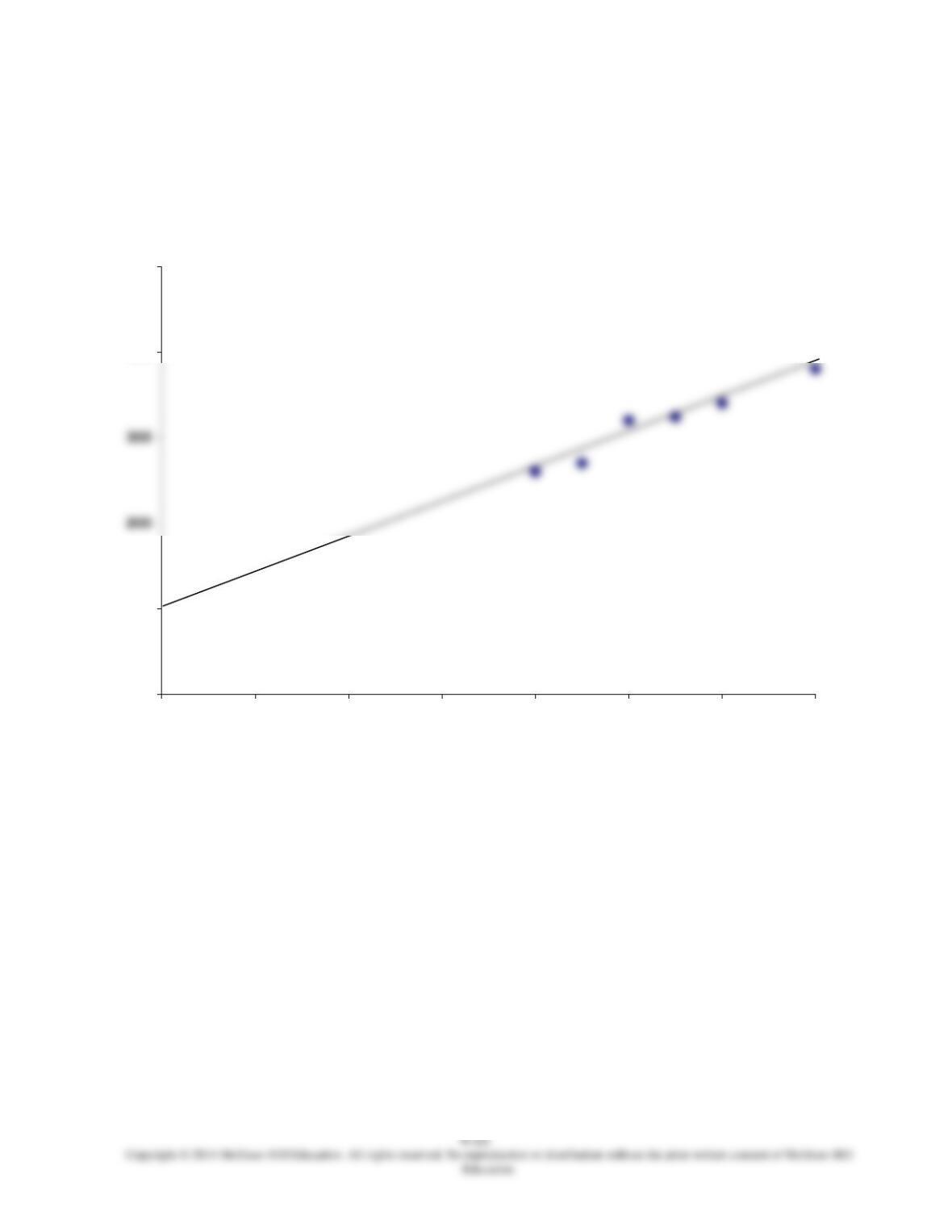

Variable-cost estimate based on the scatter diagram on the next page:

Cost at

……………………………………………………………..

Cost at

……………………………………………………………..

Difference

……………………………………………………………..

Variable cost per hour = $2,500/600 hr. = $4.17 (rounded)

Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

EXERCISE 6-33 (CONTINUED)

Scatter diagram and visually-fit line:

0

1000

4000

5000

0100 200 300 400 500 600 700

Utility cost

per month

Hours of

operation

Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

EXERCISE 6-33 (CONTINUED)

3. Estimation of variable- and fixed-cost components of cost behavior using least-

squares regression:

4.

Cost predictions at 300 hours of operation:

(a)

High-low method:

=

$1,000 + ($4.00)(300) = $2,200

(b)

Visually-fitted line:

=

$2,190

(c)

Regression:

=

$1,002 + ($4.04)(300) = $2,214

5. Calculation of R2:

Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

EXERCISE 6-33 (CONTINUED)

The following alternative approach to calculating the regression parameters is not a

requirement in the problem.

Least-square regression using manual calculations:

(a)

Tabulation of data:

Month

Dependent

Variable

(cost)

Y

Independent

Variable

(hours)

X

X2

XY

January …………………..

3,240

550

302,500

1,782,000

February …………………

3,400

600

360,000

2,040,000

March ……………………..

3,800

700

490,000

2,660,000

April ……………………….

3,200

500

250,000

1,600,000

May ………………………..

2,700

450

202,500

1,215,000

June ……………………….

(b)

Calculation of parameters:

a

=

))(( )(

))(( ))((

2

2

XXXn

XYXXY

−

−

=

(c)

Cost formula:

$1,002 + $4.04X, where X denotes hours of operation.

Variable utility cost

=

$4.04 per hour of operation

Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

EXERCISE 6-34 (45 MINUTES)

The following alternative approach to calculating the regression parameters and R2 is not a

requirement in the problem.

Least-square regression using manual calculations:

(a)

Tabulation of data:

Month

Dependent

Variable

(cost in

thousands)

Y

Independent

Variable

(thousands

of

passengers)

X

X2

XY

July ………………………..

54

16

256

864

August ……………………

54

17

289

918

September ………………

57

16

256

912

October …………………..

60

18

324

November ……………….

54

15

225

810

December ……………….

17

Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

EXERCISE 6-34 (CONTINUED)

(b)

Calculation of parameters:

a

=

))(( )(

))(( ))((

2

2

XXXn

XYXXY

−

−

(c)

Cost formula:

Calculation and interpretation of R2 using manual calculations:

(a)

Formula for calculation:

2

2

2

)(

)‘ (

1

YY

YY

R

−

−

−=

Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

EXERCISE 6-34 (CONTINUED)

(b)

Tabulation of data:*

Month

Y

X

Predicted Cost (in

thousands)

Based on

Regression

Line Y’

[( Y – Y’)2]†

[(Y –

Y

)2]†

July …………….

54

16

55.176

1.383

4.000

August ………..

54

17

56.812

7.907

4.000

September …..

57

16

55.176

3.327

1.000

October ……….

60

18

58.448

2.409

November ……

54

15

53.540

4.000

December ……

57

17

56.812

=

($29,000 + $1,636X)/$1,000

(c)

Calculation of R2:

(d)

Interpretation of R2:

The coefficient of determination, R2, is a measure of the goodness of fit of the

least-squares regression line. An R2 of .49 means that 49% of the variability of

Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

SOLUTIONS TO PROBLEMS

PROBLEM 6-35 (20 MINUTES)

Note that j was not used.

PROBLEM 6-36 (15 MINUTES)

An appropriate activity measure for the school would be hours of instruction. The costs are

classified as follows:

Variable

Variable

Semivariable (or mixed)*

Fixed

Fixed

Fixed

Fixed

Semivariable (or mixed)

Fixed

Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

6-29

PROBLEM 6-37 (25 MINUTES)

1.

Variable maintenance cost per hour of service

=

310 525

990,2$710,4$

−

−

=

$8.00

Total maintenance cost at 310 hours of service ………………………………….

Fixed maintenance cost per month ……………………………………………………

Cost formula:

Monthly maintenance cost = $510 + $8.00X, where X denotes hours of

maintenance service.

3.

Cost prediction at 600 hours of activity:

Maintenance cost = $510 + ($8.00)(600) = $5,310

4.

Variable cost per hour [from requirement (2)] …………………………………….

$8.00

Fixed cost per hour at 610 hours of activity ($510/610) ……………………….

$ .84*

*Rounded.

Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

PROBLEM 6-38 (25 MINUTES)

1. Straight-line depreciation—committed fixed

The per-ton mining labor/fringe benefit cost is constant at both volume levels

presented, which is characteristic of a variable cost.

Royalties have both a variable and a fixed component, making it a semivariable

(mixed) cost.

Variable royalty cost = difference in cost difference in tons

Fixed royalty cost:

June

(2,700 tons)

December

(1,400 tons)

Total royalty cost……………………….

Less: Variable cost at $65 per ton…..

Fixed royalty cost………………………

2. Total cost for 1,700 tons:

Depreciation……………………………………………

$ 30,000

Charitable contributions…………………………….

—-

Mining labor/fringe benefits at $225 per ton…….

Royalties:

49,000

Trucking and hauling………………………………..

$852,000

Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

PROBLEM 6-38 (CONTINUED)

3. Hauling 1,400 tons is not particularly cost effective. Lone Mountain Extraction will

4. A committed fixed cost results from an entity’s ownership or use of facilities and its

In times of severe economic difficulties, a company’s management will often

operations that may be difficult to overturn when economic conditions rebound.

5. Lone Mountain Extraction uses a calendar year for tax-reporting purposes. At year-

end, it may have ample funds available and decide to make donations to charitable

Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

PROBLEM 6-39 (25 MINUTES)

1. Machine supplies: $153,000 34,000 direct-labor hours = $4.50 per hour

2. Plant maintenance cost:

April

(23,000

hours)

June

(34,000

hours)

* Excludes supervisory labor cost

Variable maintenance cost = difference in cost difference in direct-labor hours

Fixed maintenance cost:

April

(23,000

hours)

Total maintenance cost ……………………….

Less: Variable cost at $13.50 per hour …

Fixed maintenance cost ………………………

June

(34,000

hours)

Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

PROBLEM 6-39 (CONTINUED)

3. Manufacturing overhead at 29,500 labor hours:

Machine supplies at $4.50 per hour ……………

$132,750

Depreciation …………………………………………….

22,500

Plant maintenance cost:

Supervisory labor …………………………………….

$933,000

4. A fixed cost remains constant when a change occurs in the cost driver (or activity

Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

PROBLEM 6-40 (40 MINUTES)

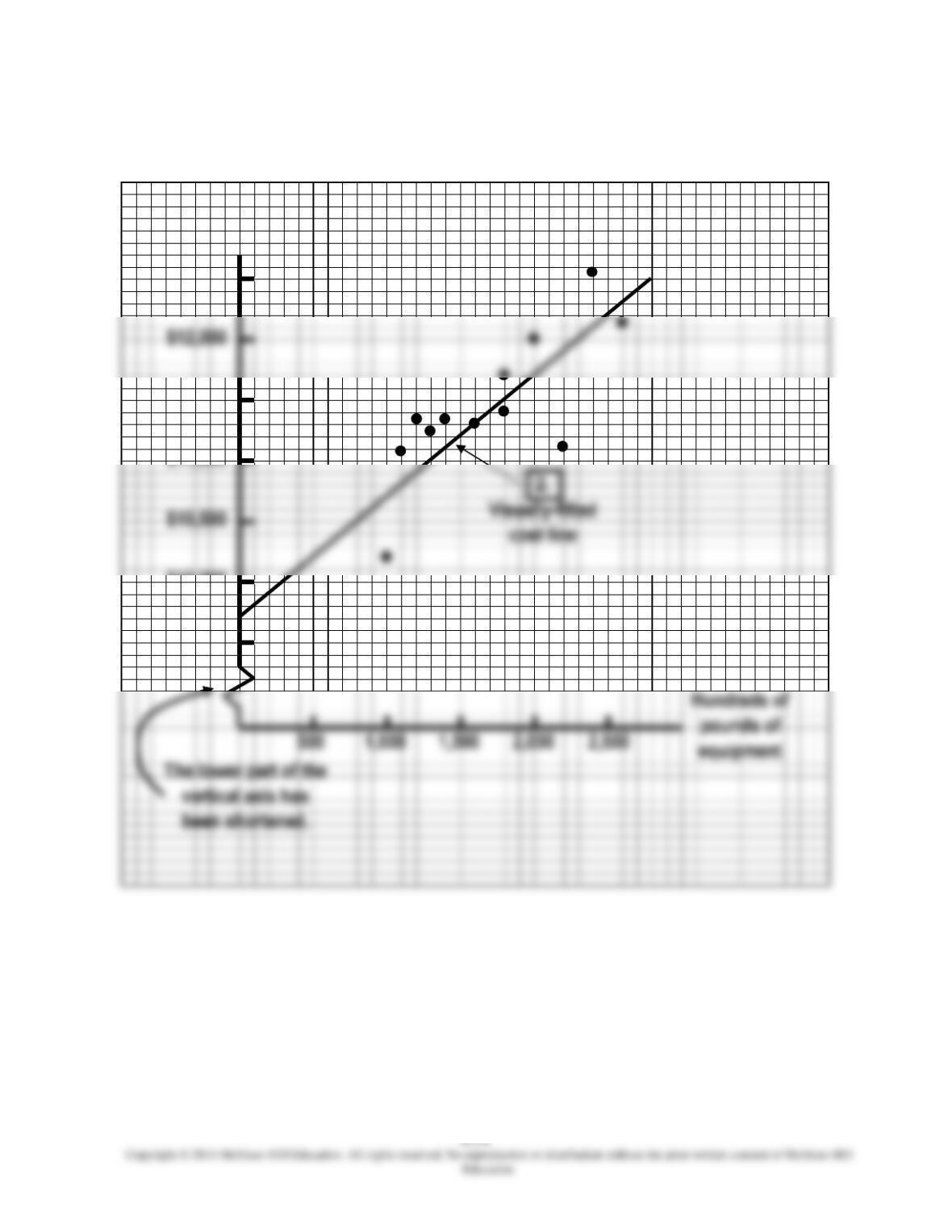

1.

Material-handling costs

$10,500

$11,000

$10,000

$9,500

$11,500

$12,500

$12,000

Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

PROBLEM 6-40 (CONTINUED)

2.

See graph for requirement (1).

3.

The estimate of the fixed cost is the intercept on the vertical axis.

Fixed-cost component = $9,700

To estimate the variable-cost component, choose any two points on the visually-fitted

cost line. For example, choose the following points:

Activity

Cost

0 ………………………………………………………………………………….

2,000 ……………………………………………………………………………

Then proceed as follows to estimate the variable-cost component:

=

$1.00

*Pounds (in hundreds) of equipment loaded or unloaded

4.

Cost equation:

Total material-handling cost = $9,700 + $1.00X, where X denotes the number pounds

(in hundreds) of equipment loaded or unloaded during the month.

Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

PROBLEM 6-40 (CONTINUED)

5.

High-low method:

=

$1.20

*Pounds (in hundreds) of equipment loaded or unloaded

Total cost at 2,600 units of activity ……………………………………………………..

$12,120

Fixed cost …………………………………………………………………………………………

$ 9,000

Cost equation based on high-low method:

Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

PROBLEM 6-40 (CONTINUED)

6.

Memorandum

Date:

Today

To:

President, Nantucket Marine Supply

From:

I.M. Student

Subject:

Material-handling cost estimates

On the basis of a scatter diagram and visually-fitted cost line, the Material-Handling

Department’s monthly cost behavior was estimated as follows:

Material-handling cost per month = $9,700 + $1.00 unit of activity

A unit of activity is defined in this department as 100 pounds of equipment loaded or

unloaded at the loading dock.

Using the high-low method, the following cost estimate was obtained:

Material-handling cost per month = $9,000 + $1.20 unit of activity

In this case, the two data points used by the high-low method do not appear to be

representative of the entire set of data.

7.

Predicted Material-Handling Costs

Using Visually-Fit

Cost Line*

Using

High-Low Method

$11,950 = $9,700 + ($1.00)(2,250)

*This method is preferable, because it uses all of the data

Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

PROBLEM 6-41 (45 MINUTES)

1. Estimation of variable and fixed components of cost behavior using least-squares

regression:

2.

Total monthly cost = $9,943 + $.89 per unit of activity

Least-squares regression equation:

3.

Cost prediction:

4.

The cost predictions differ because the cost formulas differ under the three cost–

estimation methods. The high-low method, while objective, uses only two data points.

Ten observations are excluded.

Therefore, least-squares regression is the preferred method of cost estimation.

5. Calculation of R2:

Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

The following alternative approach to calculating the regression parameters is not a

requirement in the problem.

Least-squares regression using manual calculations:

(a)

Tabulation of data:

Month

Dependent

Variable

(cost in

thousands)

Y

Independent

Variable

(units of

activity in

thousands)

X

X2

XY

January …………………..

11.70

1.8

3.24

21.060

February …………………

11.30

1.6

2.56

18.080

March ……………………..

11.25

1.3

1.69

14.625

April ……………………….

10.20

1.0

1.00

10.200

May ………………………..

11.10

2.2

4.84

24.420

June ……………………….

12.55

2.4

5.76

30.120

July ………………………..

12.00

2.0

4.00

24.000

August ……………………

11.40

1.8

3.24

20.520

12.12

2.6

6.76

31.512

October …………………..

11.05

1.1

1.21

12.155

November ……………….

11.35

1.2

1.44

13.620

December ……………….

(b)

Calculation of parameters:

a

=

))(( )(

))(( ))((

2

2

XXXn

XYXXY

−

−

Chapter 06 – Activity Analysis, Cost Behavior, and Cost Estimation

PROBLEM 6-41 (CONTINUED)

(c)

Fixed- and variable-cost components:

Monthly fixed cost = $9,943*

Variable cost = $.89 per unit of activity (rounded)†

*The intercept parameter (a) computed above is the cost per month in thousands.