*PROBLEM 6-8A (Continued)

(b)

Gross profit:

LIFO FIFO

Moving-

Average

Sales $15,690 $15,690 $15,690

*PROBLEM 6-9A

(a) (1) FIFO

Cost of

Date Purchases Goods Sold Balance

(2) MOVING-AVERAGE

Cost of

Date Purchases Goods Sold Balance

(3) LIFO

Cost of

Date Purchases Goods Sold Balance

July 1 (7 @ $ 62) $434 (7 @ $ 62) $434

(b) The highest ending inventory is $213 under the FIFO method.

SOLUTIONS TO PROBLEMS—SET B

PROBLEM 6-1B

(a) Include $1,000 in inventory.

(b) Include $620 in inventory.

(c) Exclude the goods from Sun’s inventory. The consigned goods are

owned by Frederick Inc. No entry is recorded.

PROBLEM 6-2B

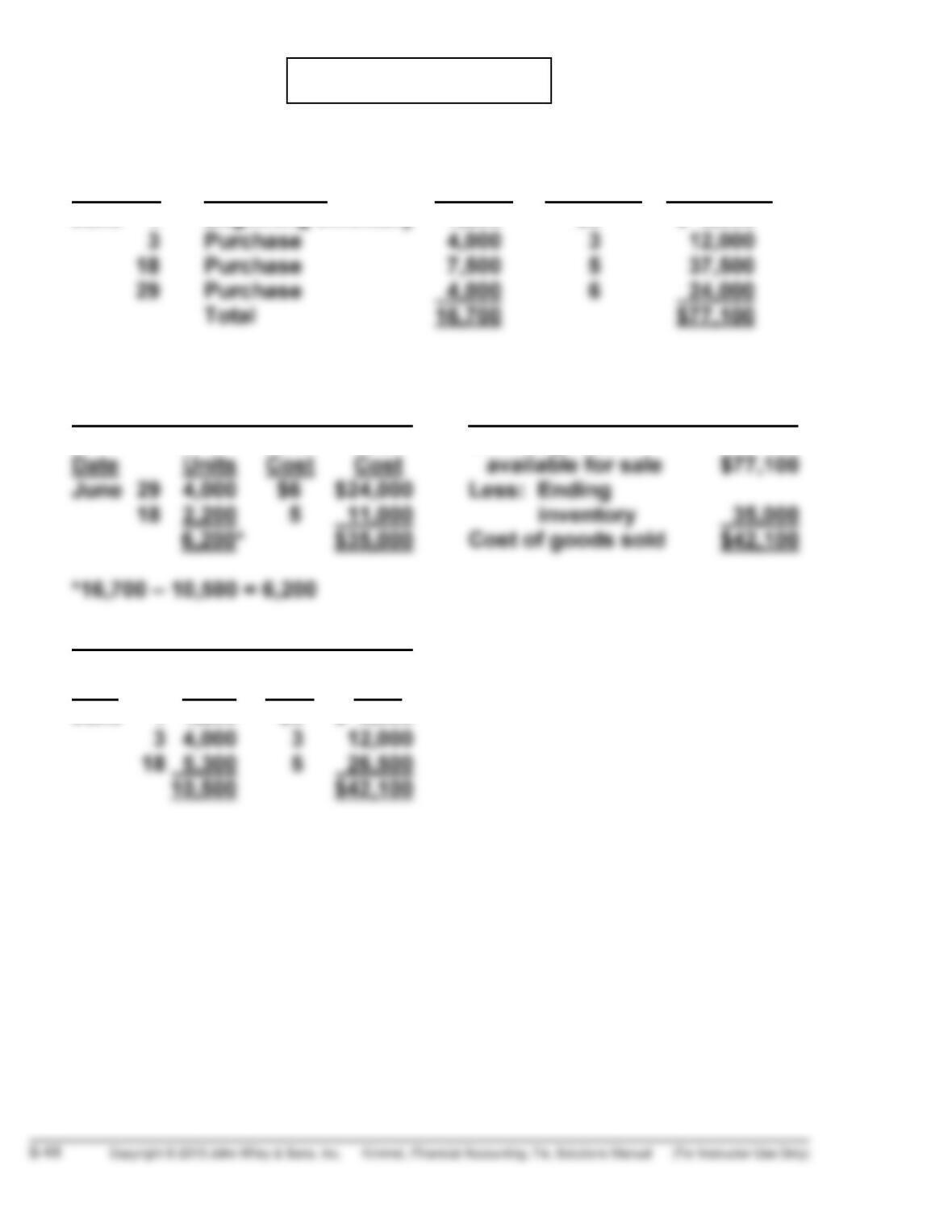

(a) COST OF GOODS AVAILABLE FOR SALE

Date Explanation Units Unit Cost Total Cost

June 1 Beginning inventory 1,200 $3 $ 3,600

(b) FIFO

(1) Ending Inventory (2) Cost of Goods Sold

Unit Total Cost of goods

Proof of Cost of Goods Sold

Unit Total

Date Units Cost Cost

June 1 1,200 $3 $ 3,600

PROBLEM 6-2B (Continued)

LIFO

(1) Ending Inventory (2) Cost of Goods Sold

Unit Total Cost of goods

Date Units Cost Cost available for sale $77,100

June 1 1,200 $3 $ 3,600 Less: Ending

Proof of Cost of Goods Sold

Unit Total

Date Units Cost Cost

June 29 4,000 $6 $24,000

AVERAGE-COST

(1) Ending Inventory (2) Cost of Goods Sold

Cost of goods

$77,100 ÷ 16,700 = $4.617 available for sale $77,100

Less: Ending

(c) (1) As shown in (b), due to rising prices, FIFO produces the highest

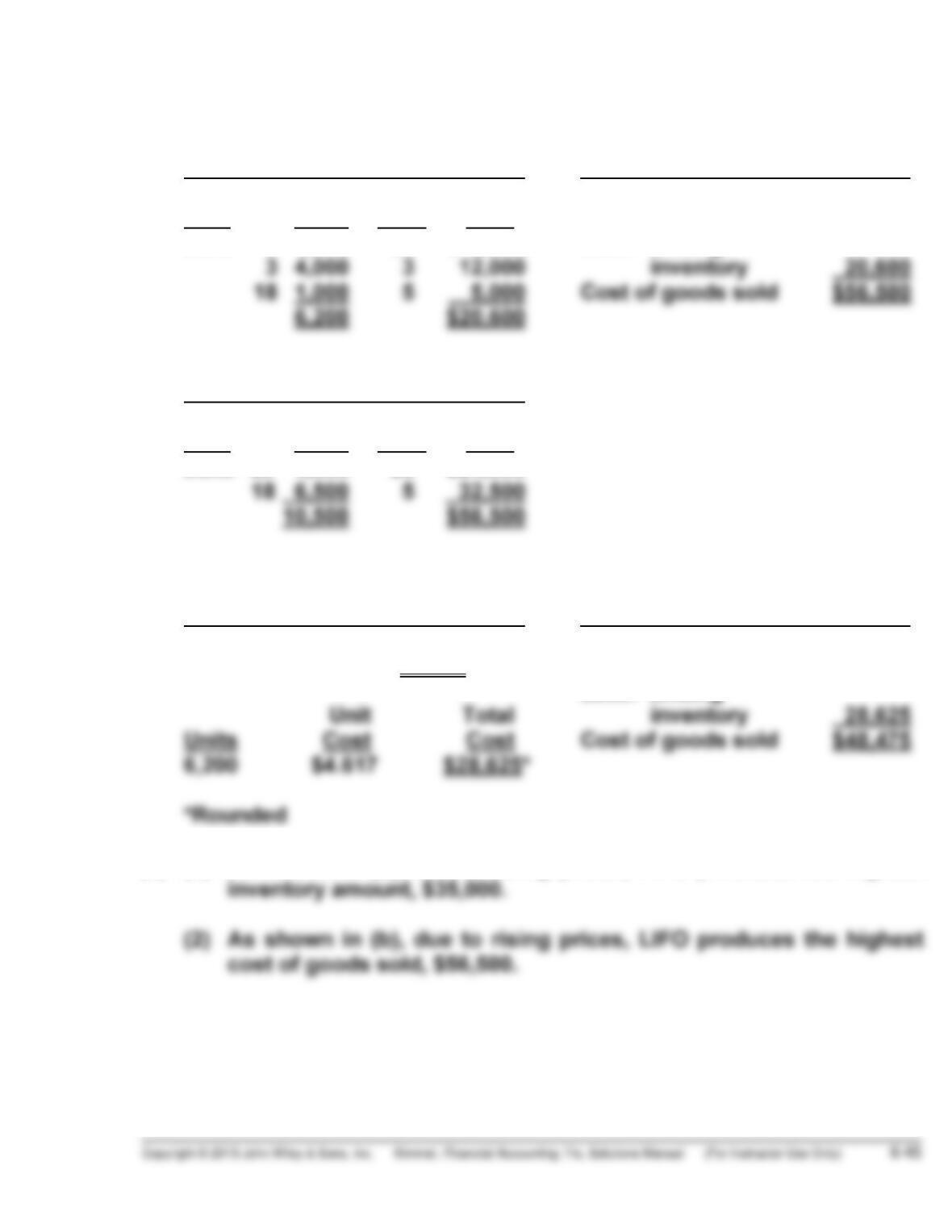

PROBLEM 6-3B

(a) COST OF GOODS AVAILABLE FOR SALE

Date Explanation Units Unit Cost Total Cost

Jan. 1 Beginning inventory 200 $ 6 $ 1,200

(b) FIFO

(1) Ending Inventory (2) Cost of Goods Sold

Date Units

Unit

Cost

Total

Cost

Cost of goods

available for sale $18,900

Nov. 30 350 $10 $3,500 Less: Ending

Proof of Cost of Goods Sold

Date Units

Unit

Cost

Total

Cost

Jan. 1 200 $6 $ 1,200

PROBLEM 6-3B (Continued)

LIFO

(1) Ending Inventory (2) Cost of Goods Sold

Date Units

Unit

Cost

Total

Cost

Cost of goods

available for sale $18,900

Jan. 1 200 $6 $1,200 Less: Ending

Proof of Cost of Goods Sold

Date Units

Unit

Cost

Total

Cost

Nov. 30 350 $10 $ 3,500

AVERAGE-COST

(1) Ending Inventory (2) Cost of Goods Sold

Cost of goods

(c) Due to rising prices, LIFO results in the lowest inventory amount for

PROBLEM 6-4B

(a) WEIGEL INC.

Condensed Income Statements

For the Year Ended December 31, 2014

FIFO LIFO

Sales………………………………………………………………….. $900,000 $900,000

Cost of goods sold

Beginning inventory …………………………………….. 16,000 16,000

Cost of goods purchased …………………………….. 470,500 470,500

(b) Answers to questions:

(1) The FIFO method produces the most meaningful inventory amount

(2) The LIFO method produces the most meaningful net income

(3) The FIFO method is most likely to approximate actual physical

(4) There will be $1,650 additional cash available under LIFO because

PROBLEM 6-4B (Continued)

(5) The illusionary gross profit is $5,500 ($456,050 – $450,550) under

FIFO. Under LIFO, Weigel Inc. has recovered the current

replacement cost of the units ($449,450), whereas under FIFO, it

has only recovered the earlier costs ($443,950). This means that

under FIFO, the company must reinvest $5,500 of the gross profit to

replace the units used.

Answer in business-letter form:

The LIFO method produces the most meaningful net income

because the costs of the most recent purchases are matched

against sales. There will be $1,650 additional cash available under

PROBLEM 6-5B

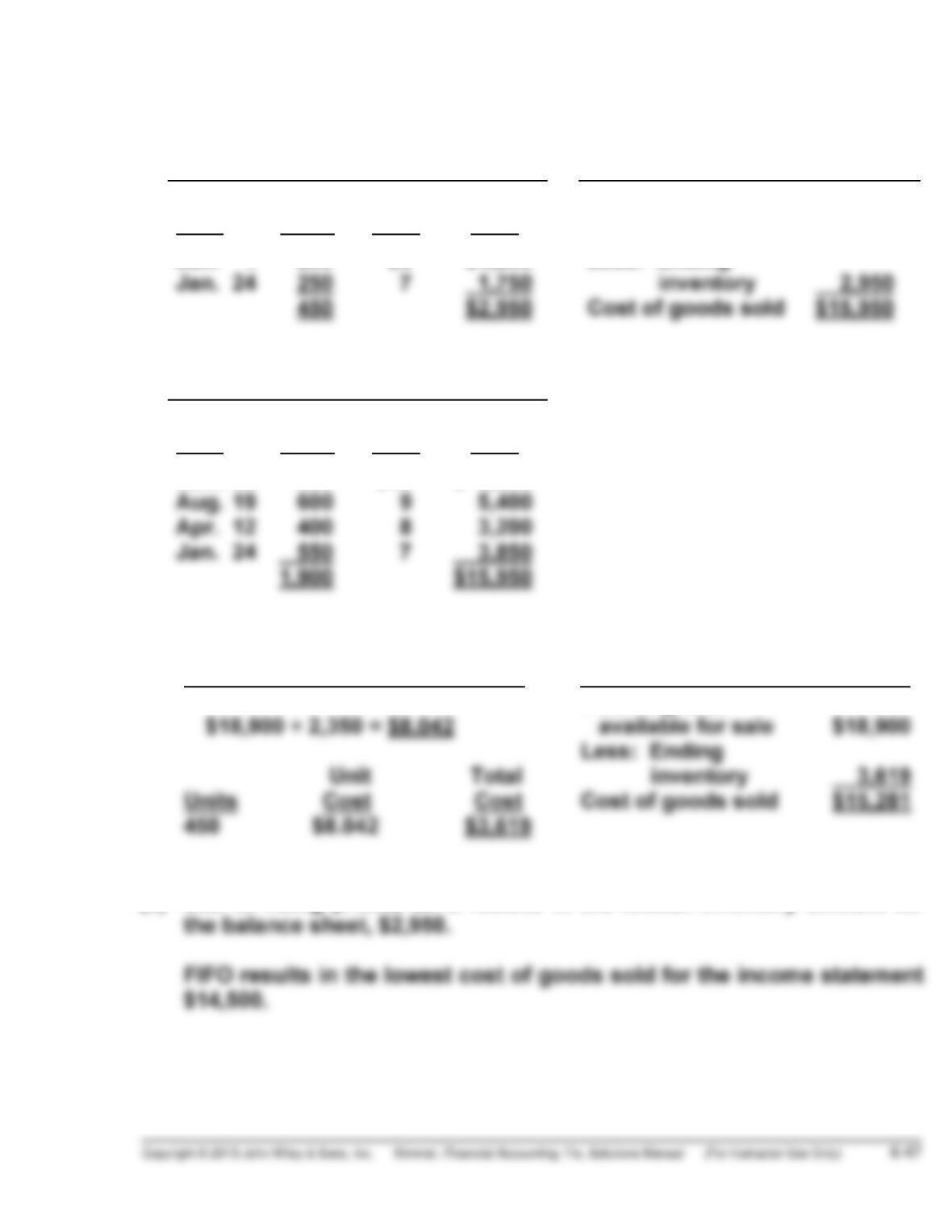

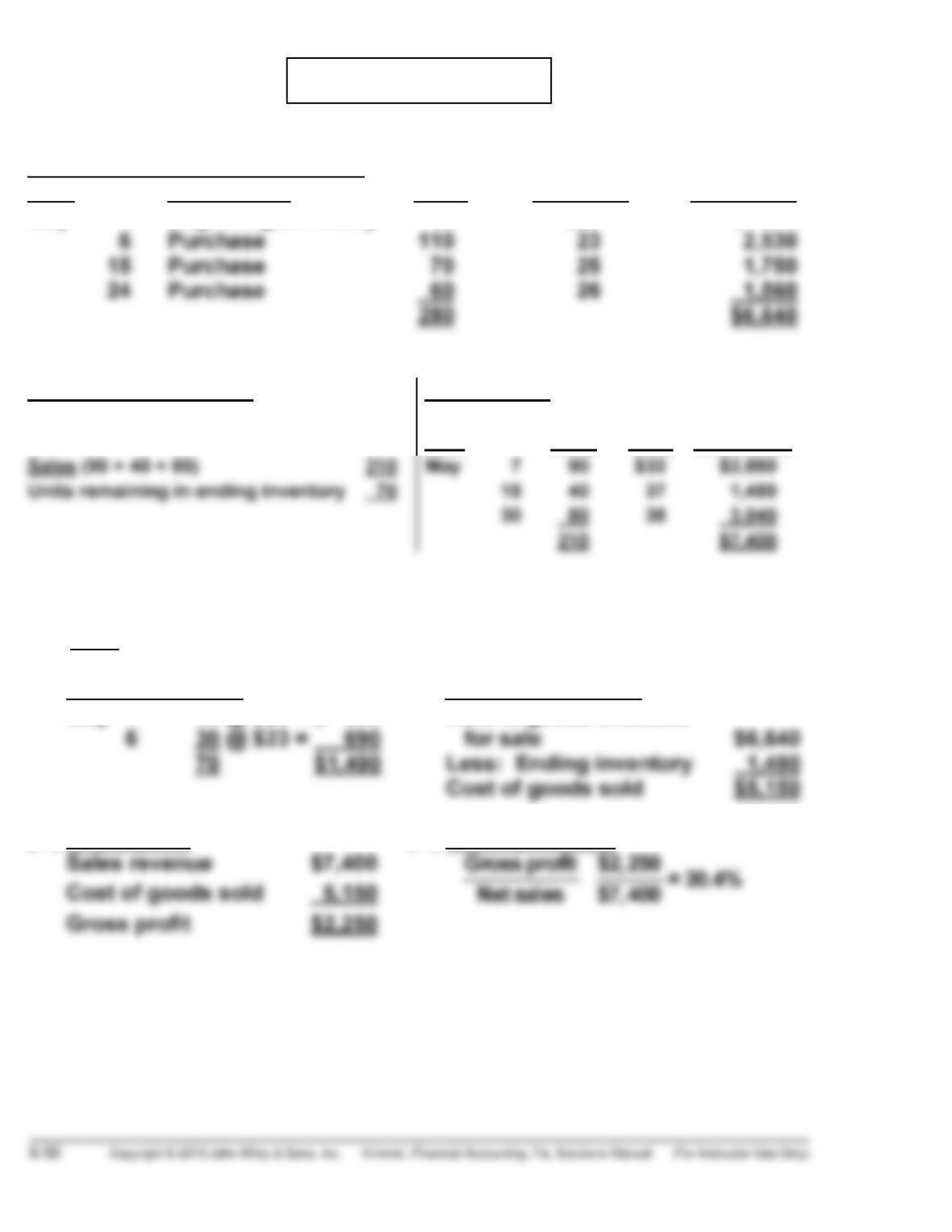

Cost of Goods Available for Sale

Date Explanation Units Unit Cost Total Cost

May 1 Beginning inventory 40 $20 $ 800

Ending Inventory in Units Sales revenue

Units available for sale 280

Date Units

Unit

Price Total Sales

(a)

(1) LIFO

(i) Ending inventory (ii) Cost of goods sold

May 1 40 @ $20 = $ 800

Cost of goods available

(iii) Gross profit (iv) Gross profit rate

PROBLEM 6-5B (Continued)

(2) FIFO

(i) Ending inventory (ii) Cost of goods sold

May 24 60 @ $26 = $1,560

Cost of goods available

$6,640

(iii) Gross profit (iv) Gross profit rate

Sales revenue $7,400 Gross profit

(3) Average-Cost

Weighted-average cost per unit: cost of goods available for sale

units available for sale

(i) Ending inventory (ii) Cost of goods sold

70 @ $23.714 = $1,660* Cost of goods available

for sale

$6,640

(b) LIFO produces the lowest ending inventory value, gross profit, and

PROBLEM 6-6B

(a) (1) To maximize gross profit, Limex Watches should sell the watches

with the lowest cost.

Sale Date Cost o

f

goods sold Sales Revenue

July 5 180 @ $420 $ 75,600 180 @ $700 $126,000

(2) To minimize gross profit, Limex Watches should sell the watches

with the highest cost.

Sale Date Cost of goods sold Sales Revenue

July 5 180 @ $450 $ 81,000 180 @ $700 $126,000

(b) FIFO

Cost of goods available for sale

July 1 Beginning inventory 220 @ $420 $ 92,400

PROBLEM 6-6B (Continued)

Cost of goods available for sale $350,400

(c) LIFO

Cost of goods available for sale $350,400

(from part b)

(d) The choice of inventory method depends on the company’s objectives.

Since the watches are marked and coded, the company could use

specific identification. This could, however, result in “earnings manage-

PROBLEM 6-7B

(a) 2014

Inventory

$130, 460

(b) Current

$54, 243

(c) 2014

Current assets using LIFO $54,243

(d) The current ratio was slightly higher in (c) compared to (b) because

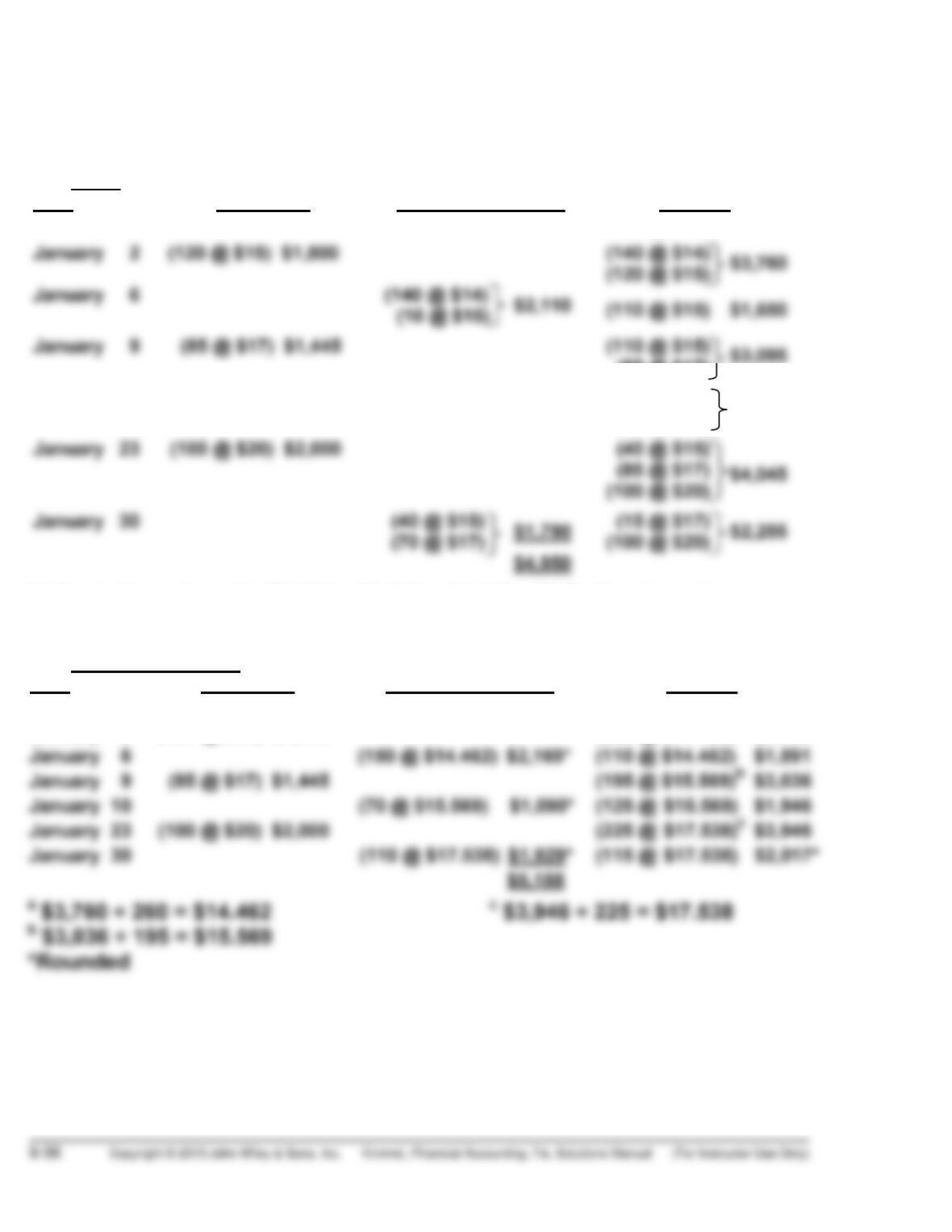

*PROBLEM 6-8B

(a)

Cost of goods available for sale:

Inventory

Purchases

140 units @ $14 $1,960

January 2 120 units @ $15 1,800

Sales:

Date

January 6 150 @ $30 $ 4,500

(1) LIFO

Date Purchases Cost of goods sold Balance

January 1 (140 @ $14) $1,960

(140 @ $14)

*PROBLEM 6-8B (Continued)

(i) Cost of goods sold: $7,205 – $1,625 = $5,580. (ii) Ending inventory = $1,625.

(iii) Gross profit = $11,570 – $5,580 = $5,990.

(2) FIFO

Date Purchases Cost of goods sold Balance

January 1 (140 @ $14) $1,960

(85 @ $17) $3,095

January 10 (70 @ $15) $1,050 (40 @ $15)

(85 @ $17) $2,045

(i) Cost of goods sold: $7,205 – $2,255 = $4,950. (ii) Ending inventory =

$2,255. (iii) Gross profit = $11,570 – $4,950 = $6,620.

(3) Moving-Average:

Date Purchases Cost of goods sold Balance

January 1 (140 @ $14) $1,960

January 2 (120 @ $15) $1,800 (260 @ $14.462)a $3,760

*PROBLEM 6-8B (Continued)

(i) Cost of goods sold: $7,205 – $2,017 = $5,188. (ii) Ending inventory = $2,017.

(iii) Gross profit = $11,570 – $5,188 = $6,382.

(b)

Gross profit:

LIFO FIFO

Moving-

Average

Sales $11,570 $11,570 $11,570

In a period of rising costs, the LIFO cost flow assumption results in the

highest cost of goods sold and lowest gross profit. FIFO gives the lowest

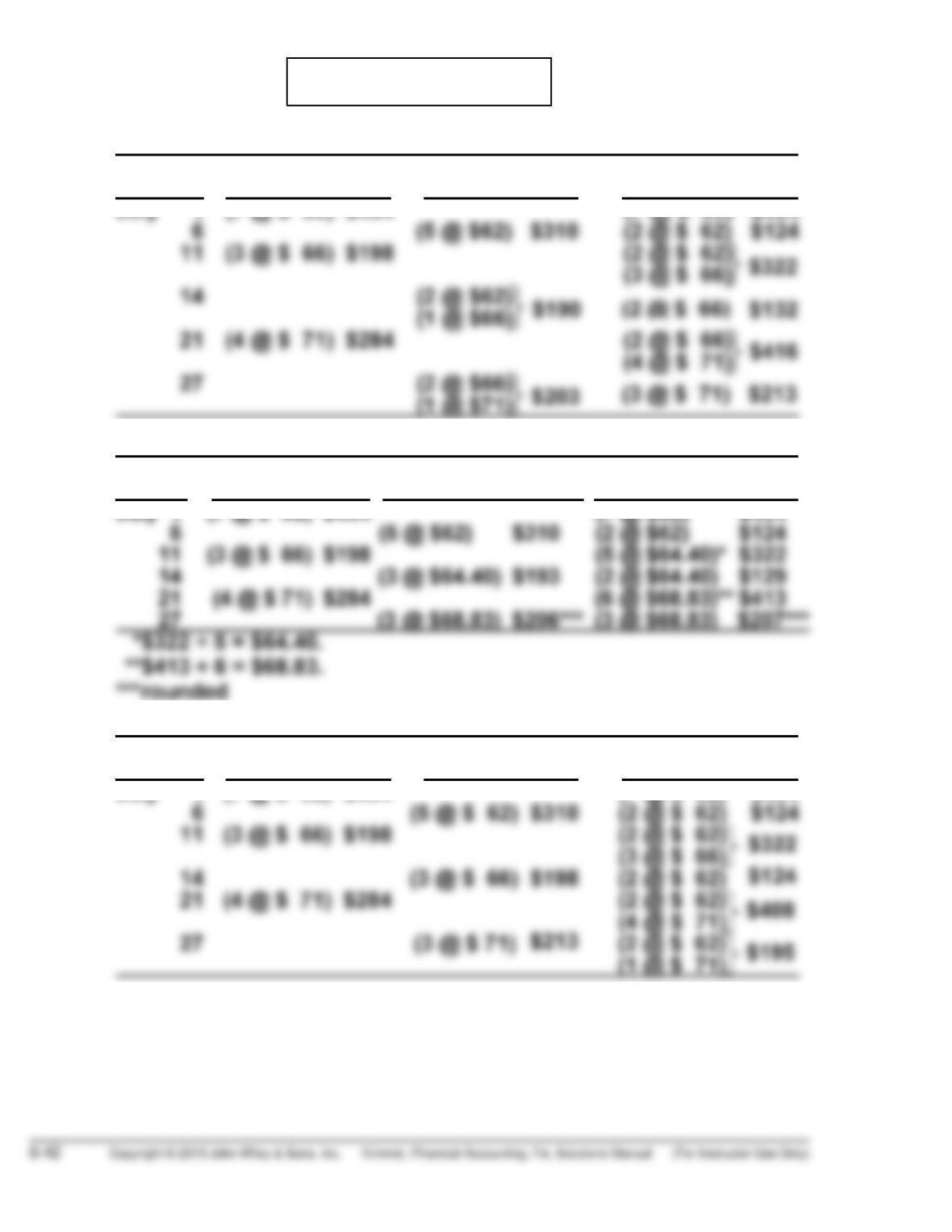

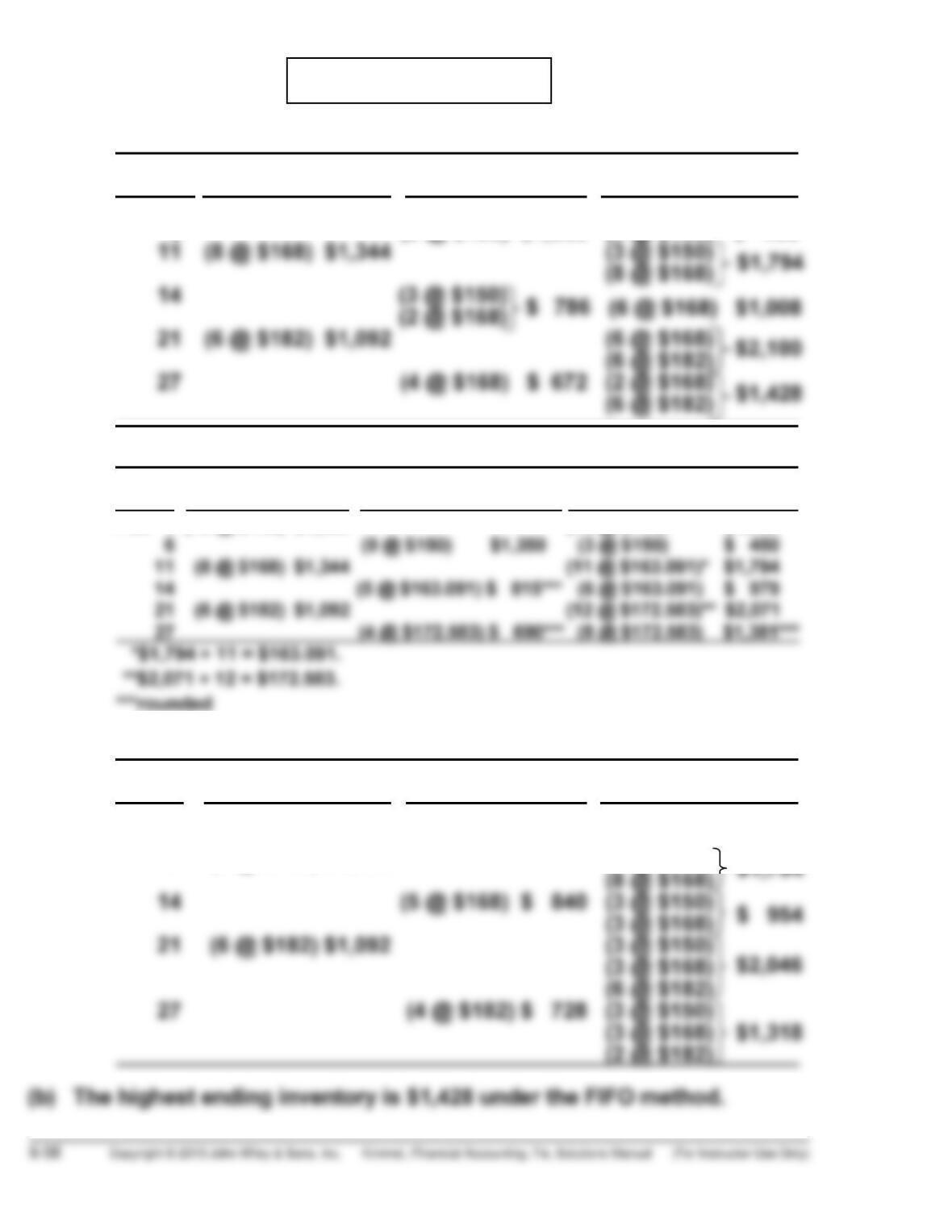

*PROBLEM 6-9B

(a) (1) FIFO

Cost of

Date Purchases Goods Sold Balance

Feb. 1 (12 @ $150) $1,800 (12 @ $150) $1,800

6 (9 @ $150) $1,350 (3 @ $150) $ 450

(2) MOVING-AVERAGE

Cost of

Date Purchases Goods Sold Balance

Feb. 1 (12 @ $150) $1,800 (12 @ $150) $1,800

(3) LIFO

Cost of

Date Purchases Goods Sold Balance

Feb. 1 (12 @ $150) $1,800 (12 @ $150) $1,800

6 (9 @ $150) $1,350 (3 @ $150) $ 450

11 (8 @ $168) $1,344 (3 @ $150)

COMPREHENSIVE PROBLEM SOLUTION

(a) Dec. 3 Inventory (4,000 X $0.72)……………………….

Accounts Payable ………………………….

2,880

2,880

22 Accounts Receivable (2,000 X $0.95) ……..

Sales Revenue ……………………………….

Cost of Goods Sold (2,000 X $0.72) ……….

Inventory ……………………………………….

1,900

1,440

1,900

1,440

COMPREHENSIVE PROBLEM SOLUTION (Continued)

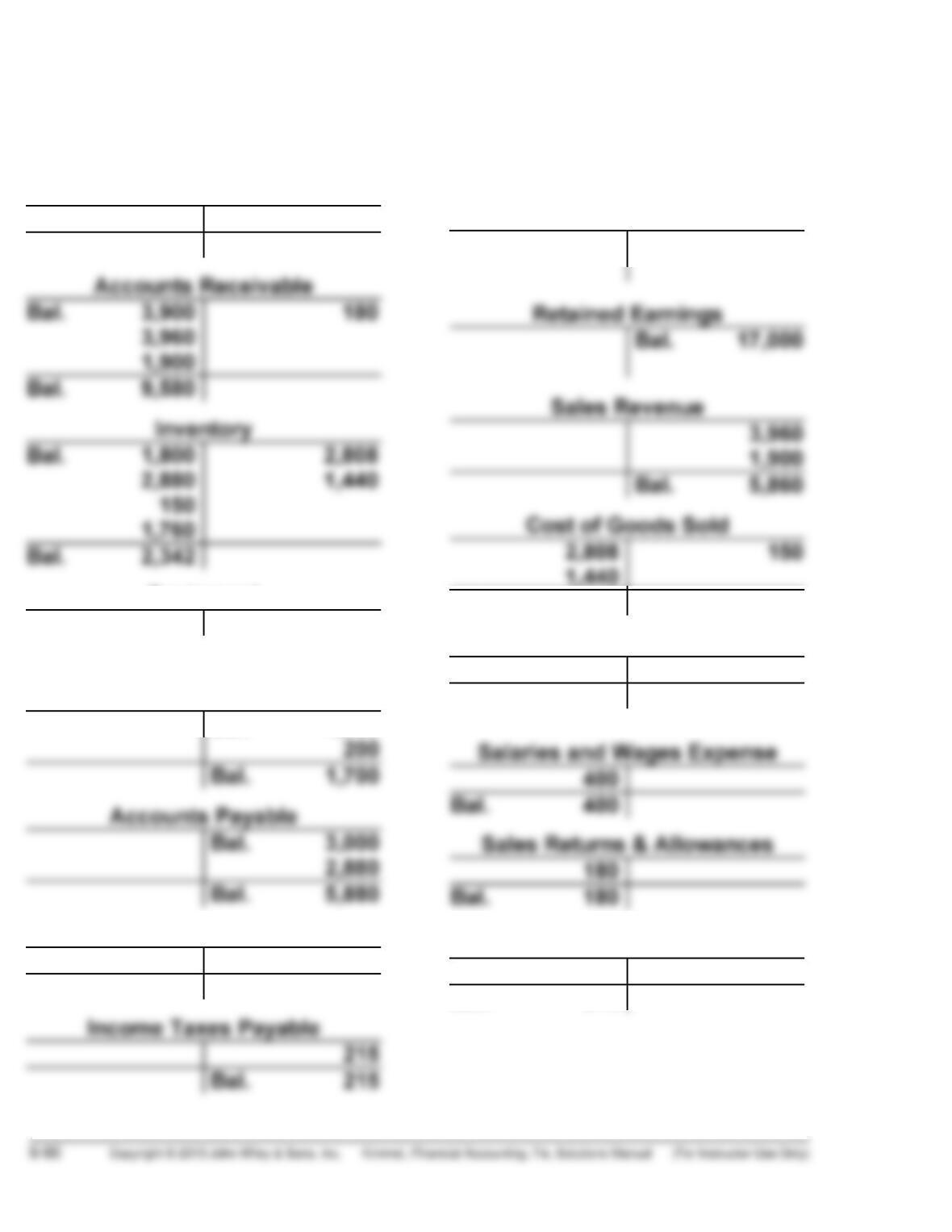

(b) General Ledger

Cash

Bal. 4,800 1,760

Bal. 3,040

Equipment

Bal. 21,000

Accumulated

Depreciation—Equipment

Bal. 1,500

Salaries and Wages Payable

400

Bal. 400

Common Stock

Bal. 10,000

Bal. 4,098

Depreciation Expense

200

Bal. 200

Income Tax Expense

215

Bal. 215