CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN)

COST-VOLUME-PROFIT ANALYSIS

DISCUSSION QUESTIONS

1. Total variable costs change in proportion to changes in the level of activity. Unit variable costs

remain the same regardless of the level of activity.

2. a. Variable costs

b. Variable costs

3. Total fixed cost remains the same regardless of changes in the level of activity. Fixed cost per unit

decreases as the activity level increases and increases as the activity level decreases.

5. a. No impact on the contribution margin.

b. Operating income would decrease.

8. Austin Company had lower fixed costs and a higher percentage of variable costs to sales than

did Hill Company. Such a situation resulted in a lower break-even point for Austin Company.

9. The individual products are treated as components of one overall enterprise product. These

components are weighted by the sales mix percentages when determining the contribution margin.

Therefore, the sales mix affects the contribution margin and thus the break-even point.

10. Operating leverage measures the relationship between a company’s contribution margin and

operating income. The difference between contribution margin and operating income is fixed

costs. Thus, companies with high fixed costs will normally have a high operating leverage. Low

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

BASIC EXERCISES

BE 20–1 (FIN MAN); BE 6–1 (MAN)

BE 20–2 (FIN MAN); BE 6–2 (MAN)

a.

35% = ($120 – $78) ÷ $120, or ($30,000,000 – $19,500,000) ÷ $30,000,000

b.

$42 per unit = $120 – $78

Sales …………………………………………..

(250,000 units × $120 per unit)

Variable costs ……………………………..

(250,000 units × $78 per unit)

Fixed costs ………………………………….

Operating income ………………………..

BE 20–3 (FIN MAN); BE 6–3 (MAN)

a. 22,000 units = $4,290,000 ÷ ($650 – $455)

b. 21,450 units = $4,290,000 ÷ ($655 – $455)

BE 20–4 (FIN MAN); BE 6–4 (MAN)

BE 20–5 (FIN MAN); BE 6–5 (MAN)

Unit selling price of E [($180 × 0.80) + ($225 × 0.20)] ……………………………….

$ 189.00

Unit variable cost of E [($99 × 0.80) + ($135 × 0.20)] ………………………………..

(106.20)

Unit contribution margin of E ………………………………………………………………..

$ 82.80

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

BE 20–6 (FIN MAN); BE 6–6 (MAN)

BE 20–7 (FIN MAN); BE 6–7 (MAN)

– Sales – Sales at Break Even Point

Margin of safety = Sales

($380,000,000 – $323,000,000) $57,000,000

= = = 15%

$380,000,000 $380,000,000

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

EXERCISES

Ex. 20–1 (FIN MAN); Ex. 6–1 (MAN)

1.

Variable

9.

Mixed

2.

Variable

10.

Mixed

3.

Fixed

11.

Fixed

4.

Fixed

12.

Variable

5.

Variable

13.

Variable

6.

Variable

14.

Variable

7.

Fixed

15.

Variable

Ex. 20–2 (FIN MAN); Ex. 6–2 (MAN)

a.

Cost Graph Three

d.

Cost Graph Two

Ex. 20–3 (FIN MAN); Ex. 6–3 (MAN)

1.

e

4.

f

2.

b

d

Ex. 20–4 (FIN MAN); Ex. 6–4 (MAN)

1. e

2. f

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

Ex. 20–5 (FIN MAN); Ex. 6–5 (MAN)

a.

Variable

g.

Fixed*

b.

Variable

h.

Fixed

d.

Variable

Variable

* The developer salaries are fixed because they are more variable to the number of titles or releases rather

than the number of units sold. For example, a title could sell one copy or a million copies, and the salaries

of the developers would not be affected.

Ex. 20–6 (FIN MAN); Ex. 6–6 (MAN)

Toys produced ………………..

40,000

80,000

120,000

Total costs:

Cost per unit:

Variable cost per unit……..

(a)

$18.00

(g)

$18.00

(m)

$18.00

Fixed cost per unit …………

(b)

15.00

(h)

7.50

(n)

5.00

Total cost per unit ………….

(c)

$33.00

(i)

$25.50

(o)

$23.00

Supporting calculations:

a. $18.00 ($720,000 ÷ 40,000 units)

b. $15.00 ($600,000 ÷ 40,000 units)

h. $7.50 ($600,000 ÷ 80,000 units)

I. $25.50 ($18.00 + $7.50)

j. $2,160,000 ($18.00 × 120,000 units)

k. $600,000 (fixed costs do not change with volume)

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

Ex. 20–7 (FIN MAN); Ex. 6–7 (MAN)

a.

Difference in Total Costs

Variable Cost per Unit = Difference in Units Produced

40,000units

The fixed cost can be determined by subtracting the estimated total variable

cost from the total cost at either the highest or lowest level of production, as

follows:

Total Cost = (Variable Cost per Unit × Units Produced) + Fixed Costs

Highest level:

$32,120,000 = ($175.50 × 120,000 units) + Fixed Costs

b. Total Cost = (Variable Cost per Unit × Units Produced) + Fixed Costs

Total cost for 115,000 units:

Variable cost:

Units …………………………………………………

115,000

Variable cost per unit …………………………

× $175.50

Total variable cost ……………………………..

Fixed costs ………………………………………..

Total cost …………………………………………..

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

Ex. 20–8 (FIN MAN); Ex. 6–8 (MAN)

Variable Cost per

–

Difference in Total Costs

=Difference in Gross Ton Miles

Gross-Ton Mile

The fixed costs can be determined by subtracting the estimated total variable

cost from the total cost at either the highest or lowest level of gross-ton mile,

as follows:

Total Cost = (Variable Cost per Gross-Ton Mile × Gross-Ton Miles) + Fixed Costs

Highest level:

$40,312,500 = ($1.75 × 12,750,000 gross-ton miles) + Fixed Costs

Ex. 20–9 (FIN MAN); Ex. 6–9 (MAN)

a.

Sales ………………………….

$112,900,000

Variable costs …………….

(66,611,000)

Contribution margin ……

$ 46,289,000

Contribution

Sales – Variable Costs

=Sales

Contribution margin ratio ………………………………………….

Contribution margin ………………………………………………….

Fixed costs ………………………………………………………………

Operating income ……………………………………………………..

Margin Ratio

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

Ex. 20–10 (FIN MAN); Ex. 6–10 (MAN)

a.

Sales (in millions) ………………………………………………………………………….

$15,295.0

Contribution margin (in millions) ……………………………………………………

Variable costs (in millions):

b.

Sales – Variales Costs

Contribution Margin Ratio = Sales

$5,310.1 million

= = 34.7%

$15,295.0 million

the computation.

Ex. 20–11 (FIN MAN); Ex. 6–11 (MAN)

a.

–Fixed Costs

Break Even Sales (units) = Units Contribution Margin

$27,600,000

= = 80,000units

$1,150 – $805

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

Ex. 20–12 (FIN MAN); Ex. 6–12 (MAN)

Total Cost

(in millions)

Variable Cost

Percentage

Variable Cost

(in millions)

Cost of goods sold ……………………….

$17,803.00

×

75%

=

$13,352.25

Selling, general, and

administrative expenses …………….

$14,439.00

×

50%

=

$7,219.50

(in millions)

(in millions)

(in millions)

Number of

Barrels

(in millions)

Per-Barrel

Amount

Total Amount

(in millions)

Sales ……………………………………………

$45,517.00

÷

500

=

$91.03

Variable cost of goods sold ………….

$13,352.25

÷

500

=

26.70

Variable selling, general, and

administrative expenses …………….

$7,219.50

÷

500

=

14.44

The variable costs per unit are determined by multiplying the total amount of each cost by

the variable cost percentage (75% for cost of goods sold and 50% for selling, general, and

administrative expenses), then dividing by the number of barrels.

b.

–––

$11,670.25 + $400.00

Break Even Sales (units) = $91.03 $26.70 $14.44

= 241.9 million barrels

Ex. 20–13 (FIN MAN); Ex. 6–13 (MAN)

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

Ex. 20–14 (FIN MAN); Ex. 6–14 (MAN)

–Fixed Costs

Break Even Sales (units)= Units Contribution Margin

Ex. 20–15 (FIN MAN); Ex. 6–15 (MAN)

The cost of the promotional campaign is the fixed cost in this analysis because

we’re trying to determine the break-even adoption rate of the campaign.

The break-even number of subscribers necessary to cover the fixed cost of the

promotion would be computed as follows:

–Fixed Costs

Break Even = Contribution Margin per Units

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

Ex. 20–16 (FIN MAN); Ex. 6–16 (MAN)

a.

–

Fixed Costs

Break Even= Revenue per Accounts – Variable Costs per Account

1 Fixed costs (in millions):

Cost of revenue ……………………………………………

$14,958

×

30%

=

$ 4,487.4

Selling, general, and administrative expenses

7,994

×

70%

=

5,595.8

Depreciation and amortization ……………………..

8,150

×

100%

=

8,150.0

Total fixed costs…………………………………………..

$18,233.2

Cost of revenue ……………………………………………

$14,958

70%

=

Selling, general, and administrative expenses

7,994

30%

=

Divided by number of accounts…………………….

Variable cost per account (rounded) ……………..

b.

–Fixed Cost

Break Even= Revenue per Account – Variable Cost per Account

60.0X – $12,870.0 =$18,233.2million

60.0X =$31,103.2

X =$518.4(rounded)

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

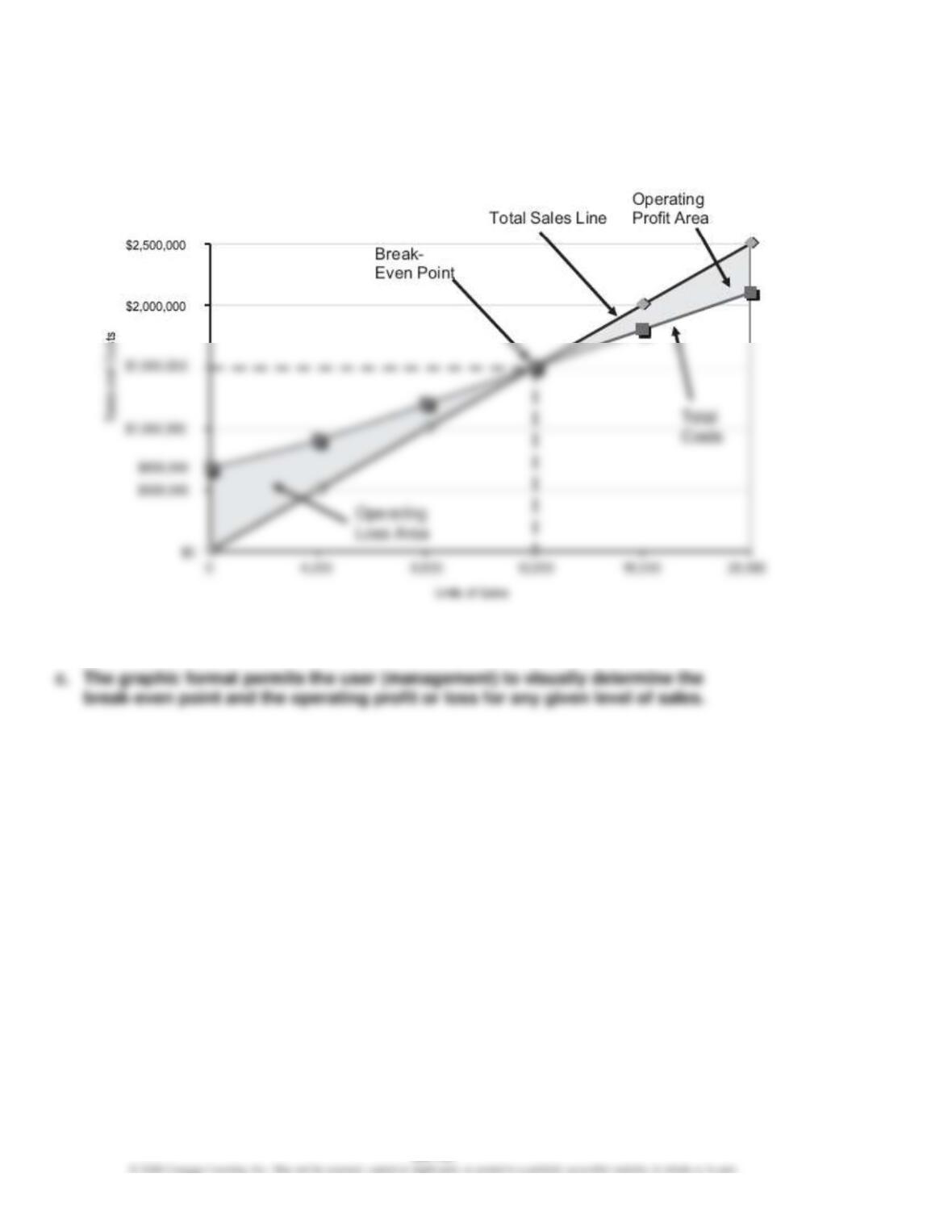

Ex. 20–17 (FIN MAN); Ex. 6–17 (MAN)

a.

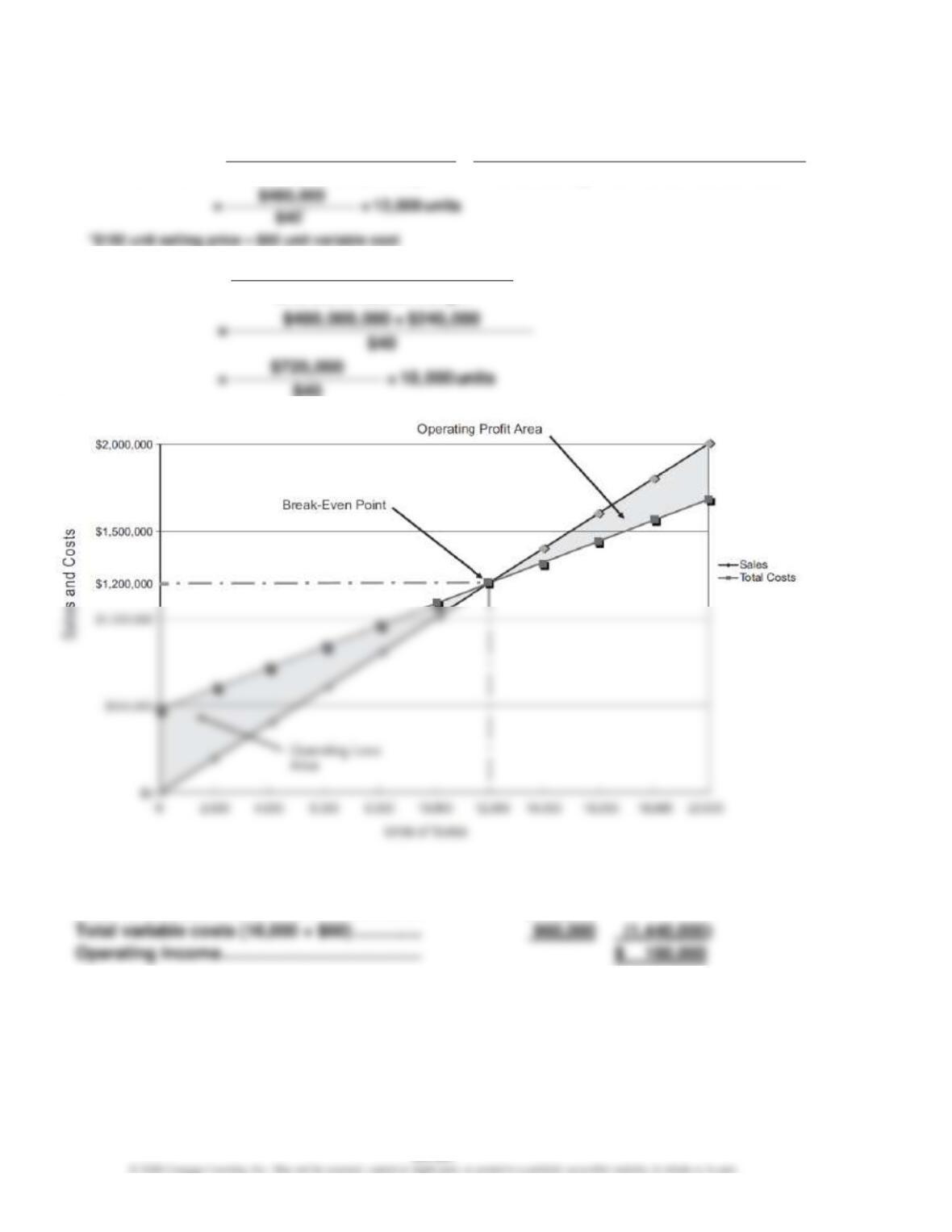

b. $1,500,000 (the intersection of the total sales line and the total costs line)

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

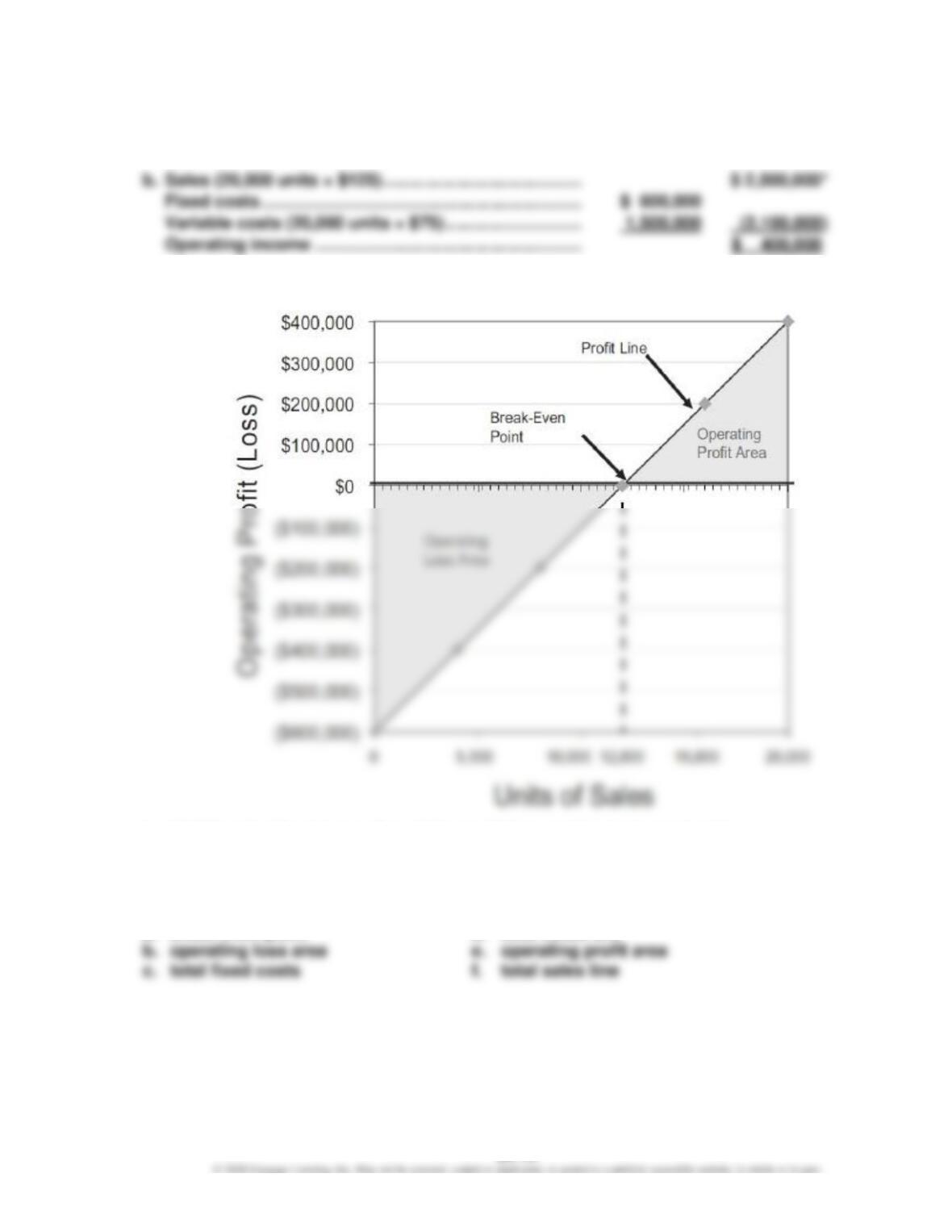

Ex. 20–18 (FIN MAN); Ex. 6–18 (MAN)

a. $600,000 (total fixed costs)

* 20,000 units = $2,500,000 maximum sales ÷ $125 unit selling price

c.

d. 12,000 units (the intersection of the profit line and the horizontal axis)

Ex. 20–19 (FIN MAN); Ex. 6–19 (MAN)

Cost-volume-profit chart

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

Ex. 20–20 (FIN MAN); Ex. 6–20 (MAN)

Profit-volume chart

a. break-even point

b. total fixed costs

f. operating profit area

Ex. 20–21 (FIN MAN); Ex. 6–21 (MAN)

a.

Units Selling Price of E = ($90 × 40%) + ($105 × 60%)

= $36 + $63 = $99

b. 6,200 units of baseball bats (15,500 units × 40%)

9,300 units of baseball gloves (15,500 units × 60%)

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

Ex. 20–22 (FIN MAN); Ex. 6–22 (MAN)

a.

Unit contribution margin of overall product (E):

Unit selling price of E [(10% × $800) + (90% × $300)] …………………..

$ 350

Break-even sales (units) of overall product:

–Fixed Costs

Break Even Sales(units)= Unit Contribution Margin

$13,680

= = 60 seats(tickets)

$228per seat

Ex. 20–23 (FIN MAN); Ex. 6–23 (MAN)

a. (1) Margin of Safety (dollars) = Sales – Sales at Break-Even Point

= $1,200,000 – $960,000 = $240,000

(2)

– Sales – Sales at Break Even Point

Margin of Safety (percentage) = Sales

= $240,000 ÷ $1,200,000 = 20%

b. The break-even point (S) is determined as follows:

Break-Even Sales (dollars) = Total Fixed Costs + Total Variable Costs (at Break-Even)

Break-Even Sales (dollars) = Total Fixed Costs + 80% Break-Even Sales (dollars)

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

Ex. 20–24 (FIN MAN); Ex. 6–24 (MAN)

If 420,000 units are sold and sales at the break-even point are 472,500 units, there is no

margin of safety.

Ex. 20–25 (FIN MAN); Ex. 6–25 (MAN)

Bryant Inc.:

Contribution Margin

Operating Leverage = Operating Income

$750,000

= =2.5

$300,000

b. Beck Inc.’s operating income would increase by 100% (5.0 × 20%), or $100,000

(100% × $100,000), and Bryant Inc.’s operating income would increase by 50%

(2.5 × 20%), or $150,000 (50% × $300,000).

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

PROBLEMS

Prob. 20–1A (FIN MAN); Prob. 6–1A (MAN)

Fixed

Variable

Mixed

Cost

Cost

Cost

Cost

a.

X

X

c.

X

d.

X

e.

X

f.

X

g.

X

h.

X

i.

X

j.

X

k.

X

l.

X

X

X

X

p.

X

X

s.

X

X

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

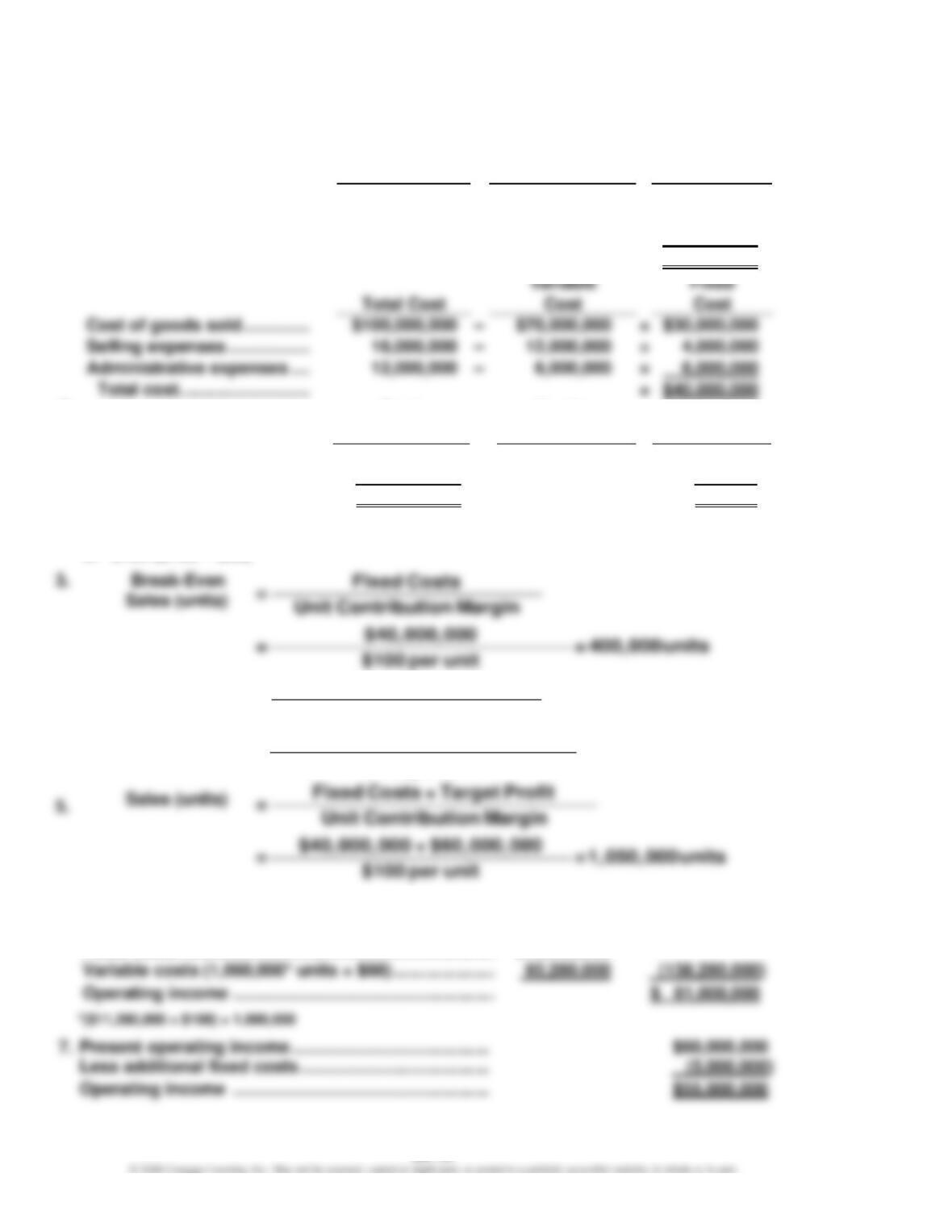

Prob. 20–2A (FIN MAN); Prob. 6–2A (MAN)

1.

Variable

Variable

Total Cost

Cost Percentage

Cost

Cost of goods sold …………..

$100,000,000

×

70%

=

$70,000,000

Selling expenses ……………..

16,000,000

×

75%

=

12,000,000

Administrative expenses ….

12,000,000

×

50%

=

6,000,000

Total variable cost …………

$88,000,000

Cost of goods sold …………..

$100,000,000

=

$30,000,000

Selling expenses ……………..

16,000,000

=

Administrative expenses ….

12,000,000

=

Total cost ………………………

=

$40,000,000

2.

Total

Number

Amount

of Units

Per Unit

Sales ………………………………

$188,000,000

÷

1,000,000

=

$188.00

Variable costs ………………….

(88,000,000)

÷

1,000,000

=

(88.00)

Contribution margin …………

$100,000,000

$100.00

a. $88 ($88,000,000 ÷ 1,000,000 units)

4.

Fixed Costs

= Unit Contribution Margin

$40,000,000 + $5,000,000

=$1 = 450,000units

00 per unit

Break-Even

Sales (units)

6.

Sales ($188,000,000 + $11,280,000) ………………………

$ 199,280,000

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

Prob. 20–2A (FIN MAN); Prob. 6–2A (MAN) (Concluded)

8. In favor of the proposal is the possibility of increasing operating income

from $60,000,000 to $61,000,000. However, there are many points against the

proposal, including:

• The break-even point increases by 50,000 units (from 400,000 to 450,000).

CHAPTER 20 (FIN MAN); CHAPTER 6 (MAN) Cost-Volume-Profit Analysis

Prob. 20–3A (FIN MAN); Prob. 6–3A (MAN)

1.

Break-Even

–

Total Fixed Costs Total Fixed Costs

==

Units Contribution Margin Units Selling Price Units Variable Cost

Sales (units)

2.

Fixed Costs + Target Profit

Sales (units) = Unit Contribution Margin

$40

3.

4. Sales (16,000 × $100) ……………………………..

$ 1,600,000

Total fixed costs …………………………………….

$480,000