387

Exercise 6-15A (20 minutes)

Periodic Inventory

Ending

Inventory

Cost of

Goods Sold

a. Specific Identification

(50 x $2.80) + (10 x $2.00) ……………………………….

$160.00

(60 x $2.54)…………………………………………………….

(22 x $2.00) + (38 x 2.30) …………………………………

(60 x $3.00)…………………………………………………….

Exercise 6-16B (20 minutes)

At Cost

At Retail

Goods available for sale

Beginning inventory ……………………………………………

$ 63,800

$128,400

Cost of goods purchased ……………………………………

Goods available for sale ……………………………………..

$178,860

$ 65,200

388

Exercise 6-17B (20 minutes)

Goods available for sale

Inventory, January 1 ……………………………………………..

$ 225,000

Net sales ……………………………………………………………….

Estimated cost of goods sold

Exercise 6-18 (15 minutes)

1. Samsung generally applies the (weighted) average cost assumption when

2. Under IFRS, Samsung would reverse inventory valuation losses if

inventory values increased in subsequent periods. Specifically, it would

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 6

389

PROBLEM SET A

Problem 6-1A (40 minutes)

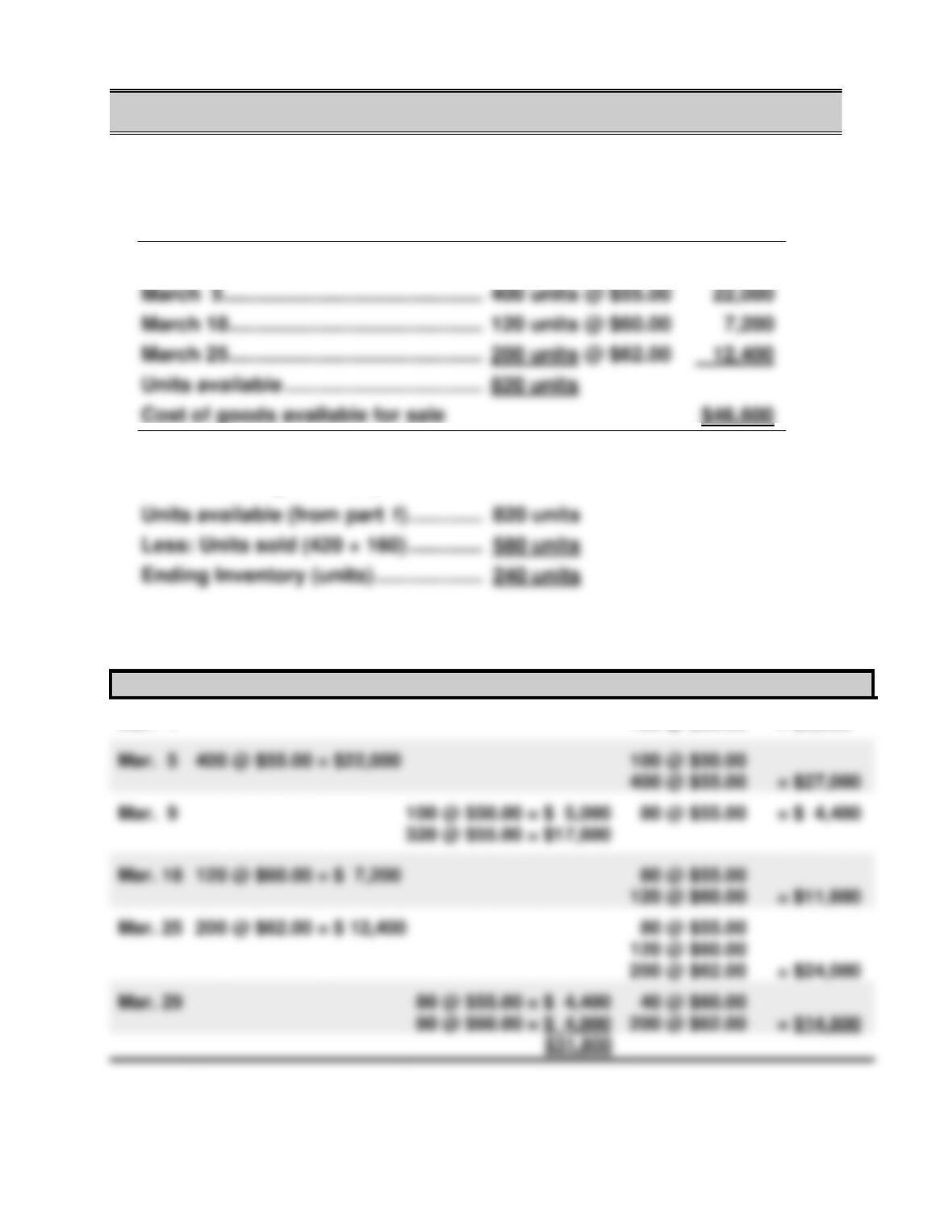

1. Compute cost of goods available for sale and units available for sale

Beginning inventory ………………………

100 units @ $50.00

$ 5,000

2. Units in ending inventory

Units available (from part 1) ……………………….

3a. FIFO perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Mar. 1

100 @ $50.00 = $5,000

320 @ $55.00 = $17,600

400 units @ $55.00

120 units @ $60.00

200 units @ $62.00

Units available ……………………………….

820 units

390

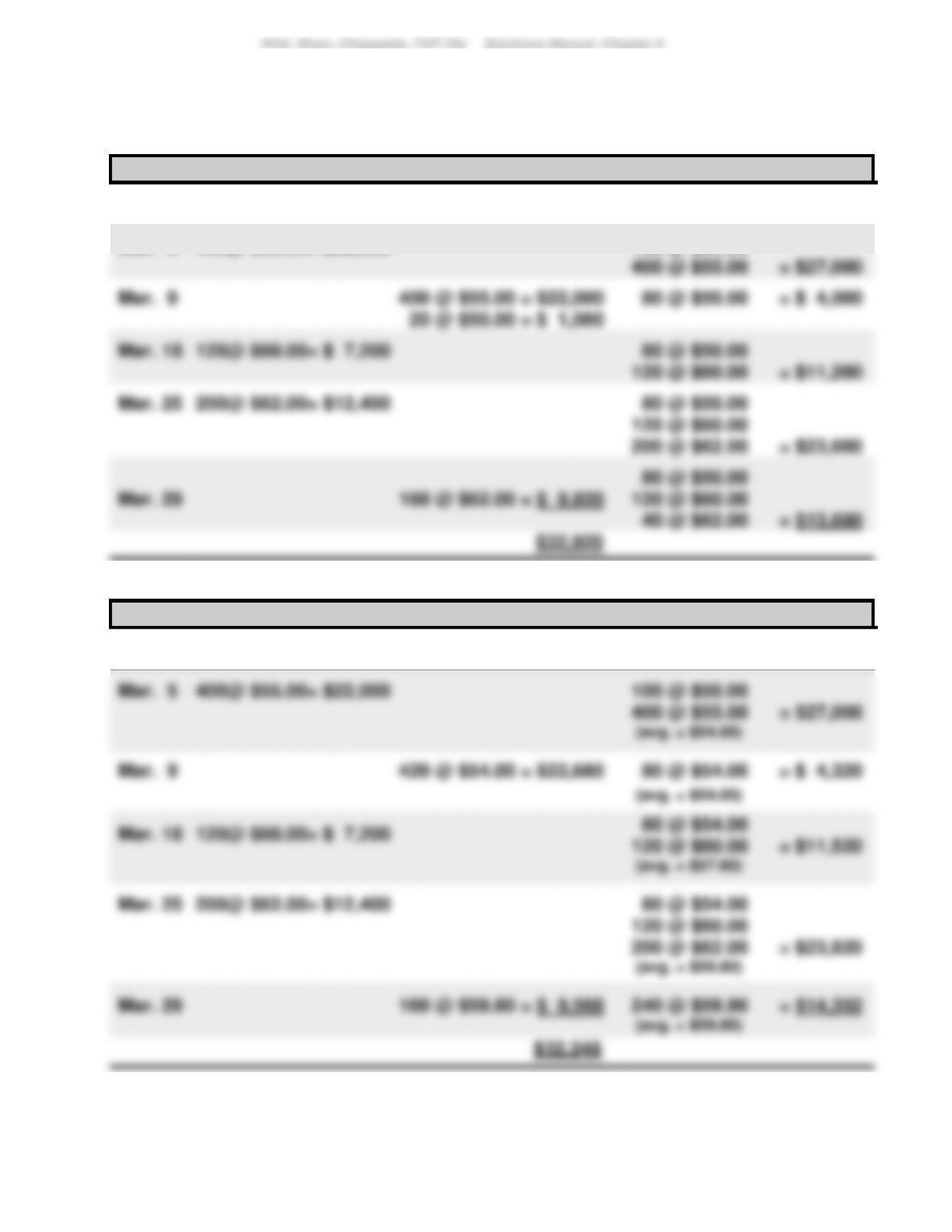

Problem 6-1A (Continued)

3b. LIFO perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Mar. 1

100 @ $50.00 = $ 5,000

Mar. 5

400@ $55.00= $22,000

Mar. 9

400 @ $55.00 = $22,000

Mar. 18

120@ $60.00= $ 7,200

120 @ $60.00

Mar. 29

160 @ $62.00 = $ 9,920

120 @ $60.00

100 @ $50.00

3c. Weighted Average perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Mar. 1

100 @ $50.00 = $ 5,000

Mar. 5

400@ $55.00= $22,000

100 @ $50.00

391

Problem 6-1A (Concluded)

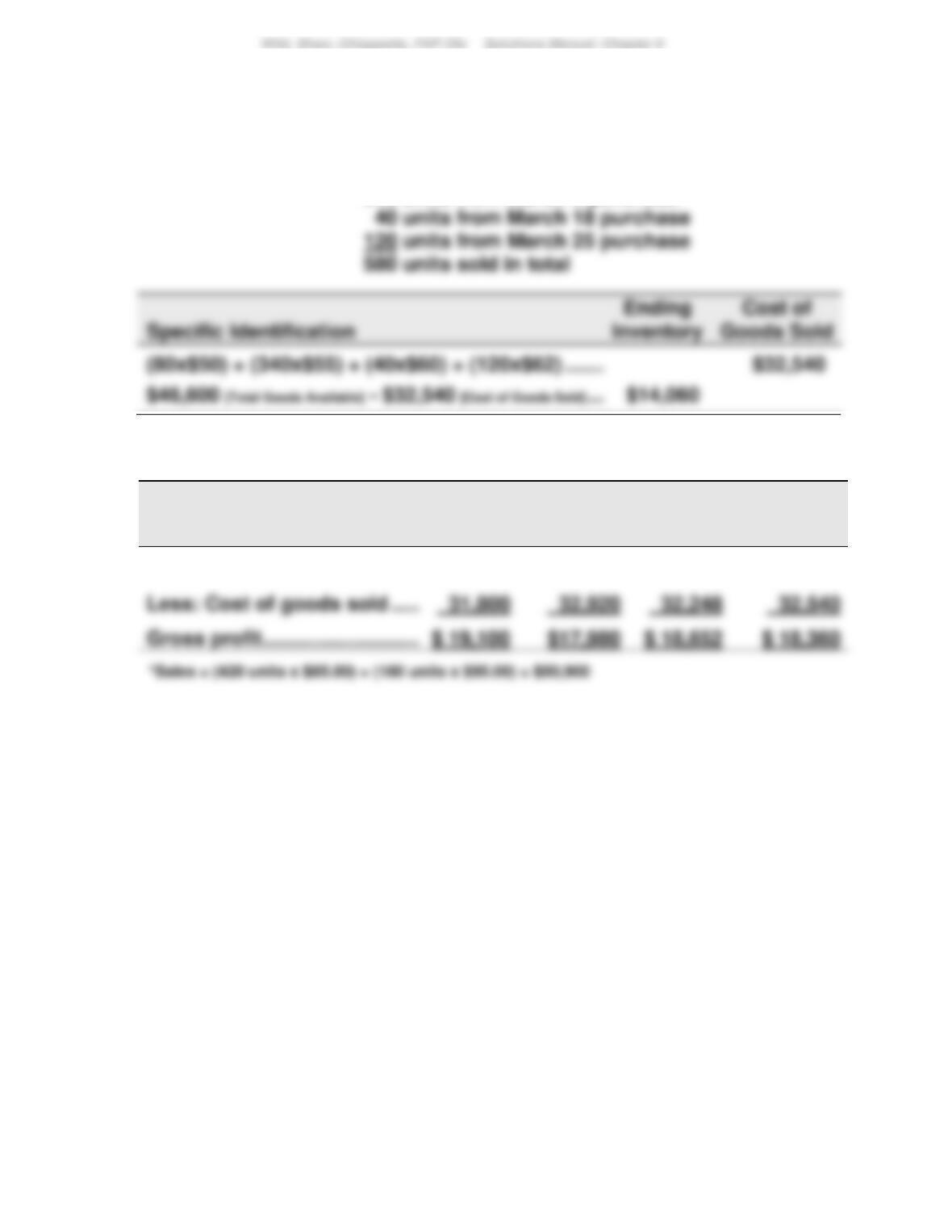

3d. Specific Identification

Cost of goods sold— 80 units from beginning inventory

340 units from March 5 purchase

4.

FIFO

LIFO

Weighted

Average

Specific

Identifi-

cation

Sales* ………………………………..

$50,900

$50,900

$50,900

$50,900

392

Problem 6-2A (40 minutes)

1. Compute cost of goods available for sale and units available for sale

Beginning inventory ………………………

100 units @ $50.00

$ 5,000

2. Units in ending inventory

3.

Periodic Inventory

Ending

Inventory

Cost of

Goods Sold

a. FIFO

(200 x $62.00) + (40 x $60.00) ………………………….

$14,800.00

(100 x $50.00) + (400 x $55.00) + (80 x $60.00) …

$31,800.00

(100 x $50.00) + (140 x $55.00) ……………………….

$12,700.00

c. Weighted average ($46,600/820 = $56.83)

(240 x $56.83) ………………………………………………..

$13,639.20

(20 x $50)+(60 x $55)+(80 x $60)+(80 x $62) ……..

$14,060.00

393

Problem 6-2A (Concluded)

4.

FIFO

LIFO

Weighted

Average

Specific

Identifi-

cation

Sales* ………………………………..

$50,900.00

$50,900.00

$50,900.00

$50,900.00

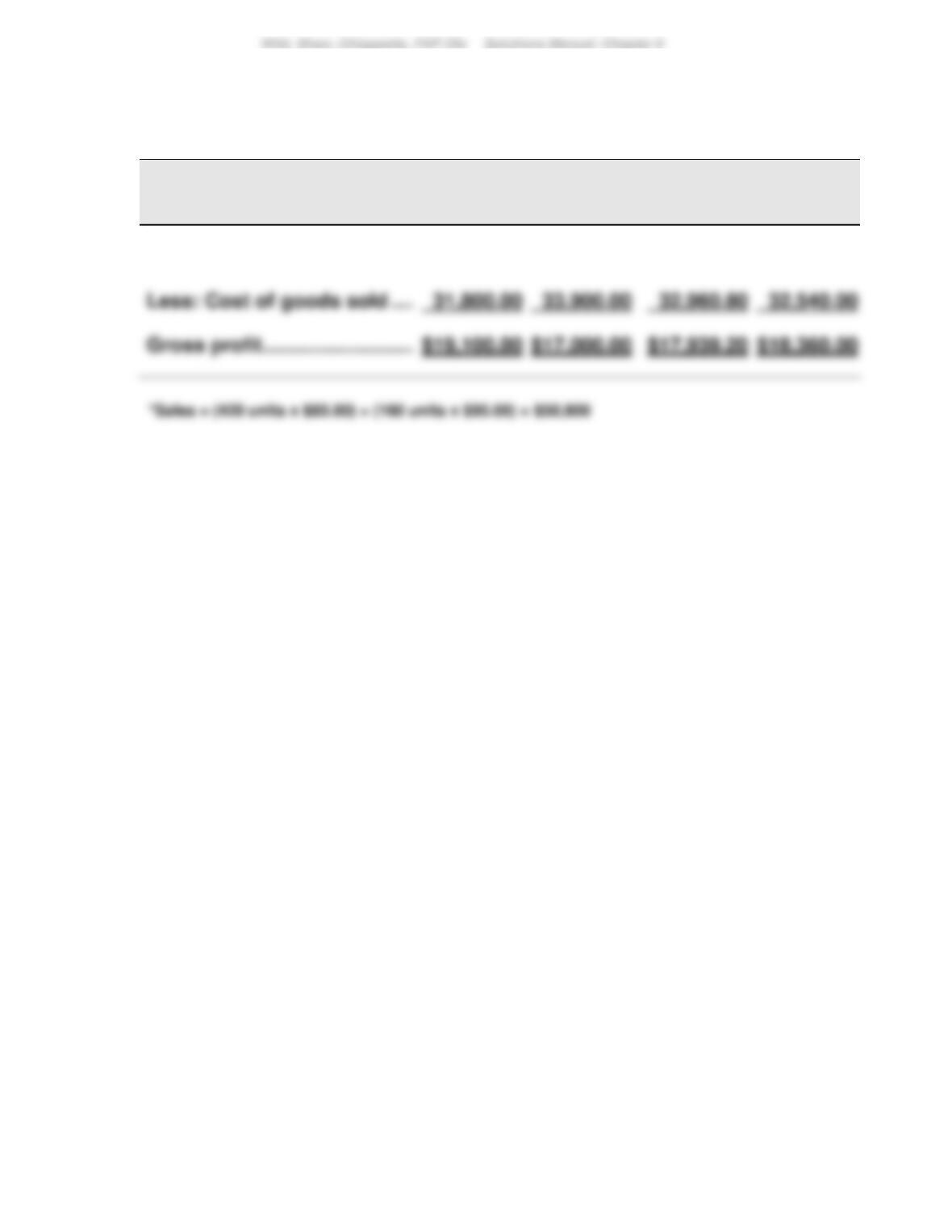

Less: Cost of goods sold ……

394

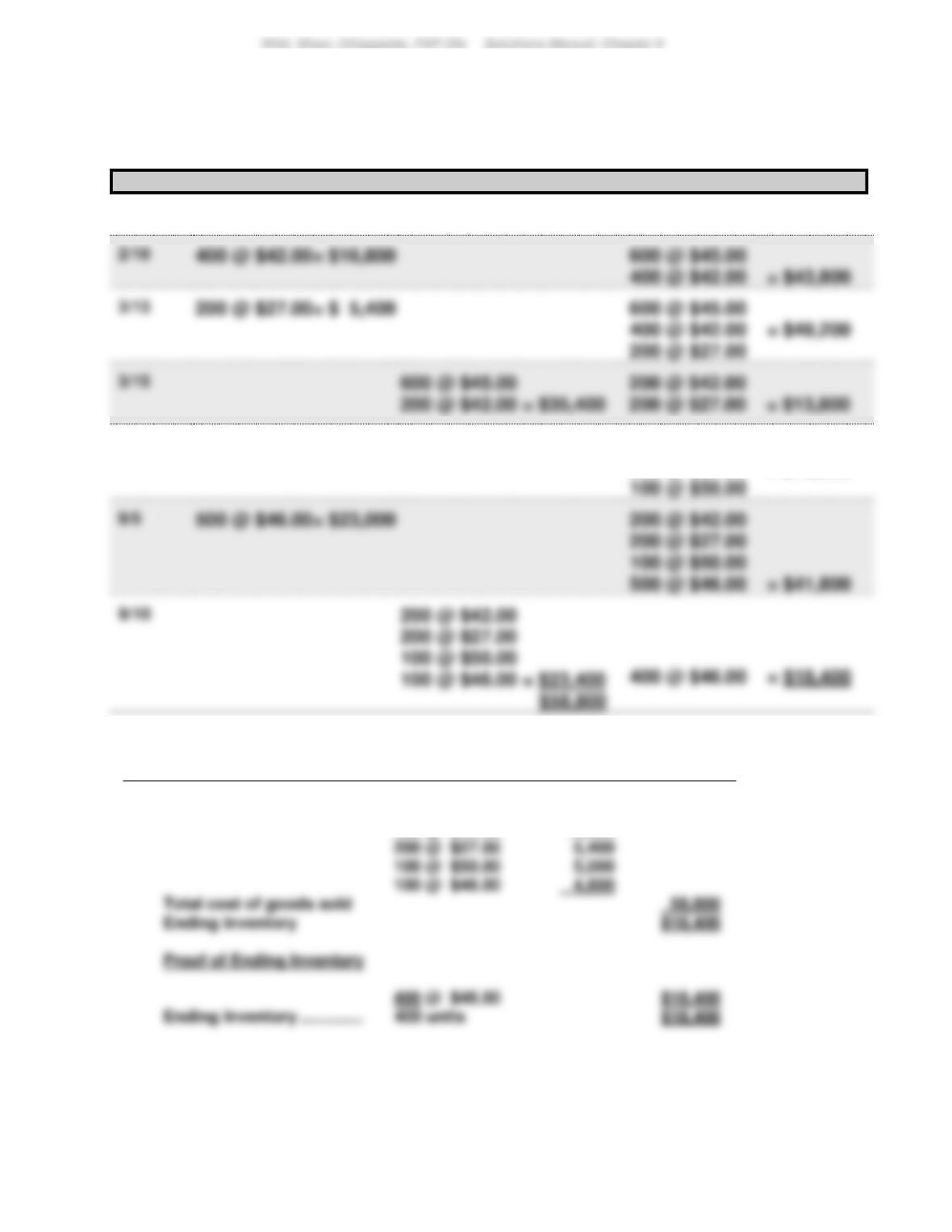

Problem 6-3A (40 minutes)

1. Calculate cost of goods available for sale and units available for sale

Beginning inventory ………………………

600 units @ $45.00

$27,000

400 units @ $42.00

200 units @ $27.00

Aug. 21 ………………………………………….

100 units @ $50.00

500 units @ $46.00

2. Units in ending inventory

Units available (from part 1) ……………………….

1,800

395

Problem 6-3A (Continued)

3a. FIFO perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

600 @ $45.00 = $27,000

600 @ $45.00

3/13

200 @ $27.00= $ 5,400

600 @ $45.00

400 @ $42.00 = $49,200

200 @ $42.00 = $35,400

200 @ $27.00 = $13,800

8/21

100 @ $50.00= $ 5,000

200 @ $27.00

100 @ $50.00

200 @ $42.00

200 @ $27.00 = $18,800

FIFO Alternate Solution Format

Cost of goods available for sale

$77,200

Less: Cost of sales

600 @ $45.00

$27,000

400 @ $42.00

16,800

200 @ $27.00

100 @ $50.00

100 @ $46.00

Ending Inventory

$18,400

Proof of Ending Inventory

$18,400

396

Problem 6-3A (Continued)

3b. LIFO perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

600 @ $45.00 = $27,000

400 @ $42.00= $16,800

600 @ $45.00

400 @ $42.00 = $43,800

400 @ $42.00 = $49,200

200 @ $27.00

200 @ $45.00 = $31,200

8/21

100 @ $50.00= $ 5,000

400 @ $45.00

100 @ $50.00 = $23,000

100 @ $50.00

500 @ $46.00 = $46,000

9/10

500 @ $46.00

LIFO alternate solution format

Cost of goods available for sale

$77,200

Less: Cost of sales

500 @ $46

$23,000

100 @ 50

5,000

200 @ 27

5,400

400 @ 42

200 @ 45

Cost of Goods Sold

Ending Inventory

$18,000

Proof of Ending Inventory

397

Problem 6-3A (Continued)

3c. Weighted Average

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

600 @ $45.00 = $27,000

2/10

400 @ $42.00= $16,800

8/21

100 @ $50.00= $ 5,000

400 @ $41.00

100 @ $50.00

600 @ $45.00

Problem 6-3A (Continued)

3d. Specific Identification

Cost of goods available for sale ……………….

$77,200

Less: Cost of Goods Sold

600 @ $45.00 ……………………………….

$27,000

300 @ $42.00 ……………………………….

200 @ $27.00 ……………………………….

250 @ $46.00 ……………………………….

Total cost of goods sold …………………………..

4.

FIFO

LIFO

Specific

Identifi-

cation

Weighted

Average

5. Montoure’s manager would likely prefer the FIFO method since this

1,400

Problem 6-4A (40 minutes)

1. Calculate cost of goods available for sale and units available for sale

Beginning inventory ………………………

600 units @ $45.00

$27,000

400 units @ $42.00

200 units @ $27.00

Aug. 21 ………………………………………….

100 units @ $50.00

500 units @ $46.00

2. Units in ending inventory

Units available (from part 1) ……………………….

1,800

Problem 6-4A (Concluded)

3.

Periodic Inventory

Ending

Inventory

Cost of

Goods Sold

a. FIFO

(400 x $46.00)…………………………………………………….

$18,400.00

b. LIFO

(400 x $45.00)……………………………………………………

$18,000.00

c. Weighted average ($77,200/1,800 = $42.89 [rounded])

(400 x $42.89)…………………………………………………….

$17,156.00

d. Specific identification

(100 x $42.00) + (50 x $50.00) + (250 x $46.00) …….

$18,200.00

4.

FIFO

LIFO

Specific

Identifi-

cation

Weighted

Average

Sales (1,400 x $75) ……………..

$105,000

$105,000

$105,000

$105,000

5. The manager would likely prefer the FIFO method since this methods’

Problem 6-5A (50 minutes)

Per Unit

Total

Total

LCM Applied

to Items

Inventory Items

Units

Cost

Market

Cost

Market

Car audio equipment:

Speakers…………………

345

$ 90

$ 98

$ 31,050

$ 33,810

$ 31,050

Stereos ……………………

260

111

Amplifiers ……………….

326

Subwoofers …………….

204

10,608

Security equipment:

Alarms …………………….

480

150

Locks………………………

291

Cameras …………………

212

310

65,720

68,264

Tripods ……………………

185

Stabilizers ……………….

170

16,490

17,850

2.

Dec 31

Cost of Goods Sold ……………………………………………..

19,723

402

Problem 6-6A (35 minutes)

Part 1

(a)

Cost of goods sold

2016

2017

2018

Reported …………………………………

$ 615,000

$ 957,000

$ 780,000

Adjustments: 12/31/2016 error ……

+ 20,000

– 20,000

Corrected ……………………………….

$ 559,000

$1,033,000

$ 760,000

Net income

2016

2017

2018

Reported …………………………………

$ 230,000

$ 285,000

$ 241,000

– 20,000

+ 20,000

Corrected ……………………………….

$ 286,000

$ 209,000

$ 261,000

(c)

Total current assets

2016

2017

2018

Reported …………………………………

$1,255,000

$1,365,000

$1,200,000

Adjustments: 12/31/2016 error ……

– 20,000

Corrected ……………………………….

$1,311,000

$1,345,000

$1,200,000

2016

2017

2018

Reported …………………………………

$1,387,000

$1,530,000

$1,242,000

Adjustments: 12/31/2016 error ……

_________

– 20,000

Part 2

Total net income for the combined three-year period ($756,000) is not affected

Part 3

The understatement of inventory by $56,000 results in an overstatement of cost of

403

Problem 6-7AA (25 minutes)

Part 1

Number and total cost of units available for sale

23,000 units in beginning inventory @ $15 …………………….. $ 345,000

Part 2

a. FIFO periodic

Total cost of 150,000 units available for sale ……………….

$3,150,000

Less ending inventory on a FIFO basis

b. LIFO periodic

Total cost of 150,000 units available for sale ……………….

$3,150,000

Less ending inventory on a LIFO basis

c. Weighted average periodic

Total cost of 150,000 units available for sale ……………….

$3,150,000

404

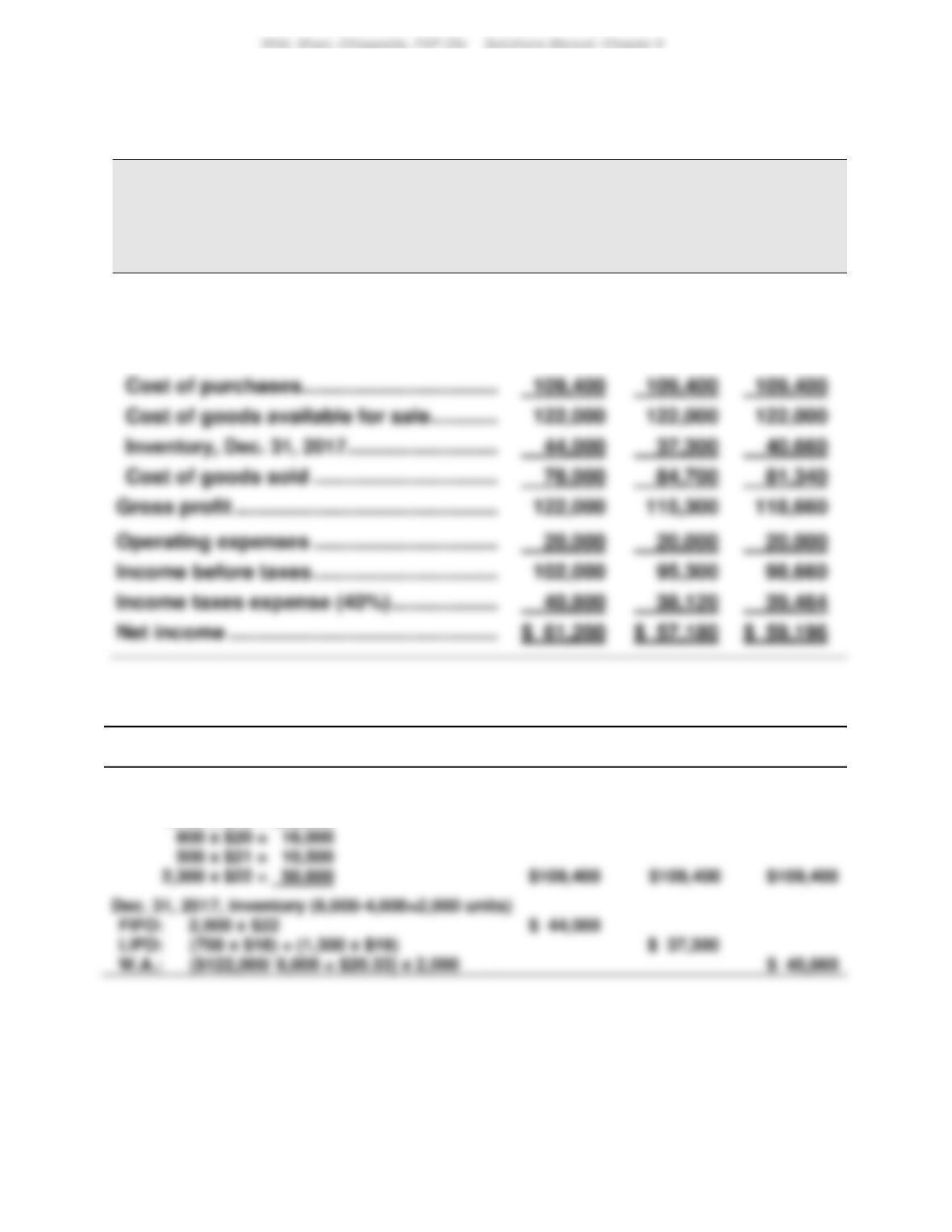

Problem 6-8AA (50 minutes)

Part 1

QP CORP.

Income Statements Comparing FIFO, LIFO, and Weighted Average

For Year Ended December 31, 2017

FIFO

LIFO

Weighted

Average

Sales ……………………………………………………..

$200,000

$200,000

$200,000

Cost of goods sold

Inventory, Dec. 31, 2016 ………………………..

12,600

12,600

12,600

109,400

109,400

109,400

44,000

37,300

40,660

20,000

20,000

20,000

40,800

38,120

39,464

Supporting calculations

FIFO

LIFO

Weighted

Average

Dec. 31, 2016, inventory (700 x $18). …………….

$ 12,600

$ 12,600

$ 12,600

Purchases

1,700 x $19 = $32,300

800 x $20 = 16,000

500 x $21 = 10,500

Dec. 31, 2017, inventory (6,000-4,000=2,000 units)

(700 x $18) + (1,300 x $19)

($122,000/ 6,000 = $20.33) x 2,000

405

Problem 6-8AA (Concluded)

Part 2

If QP Corp. had been experiencing declining costs in the acquisition of

inventory, we would observe the opposite results in our comparisons.

Part 3

Advantages

LIFO: Given the cost trends in the problem, the advantage of using LIFO is

406

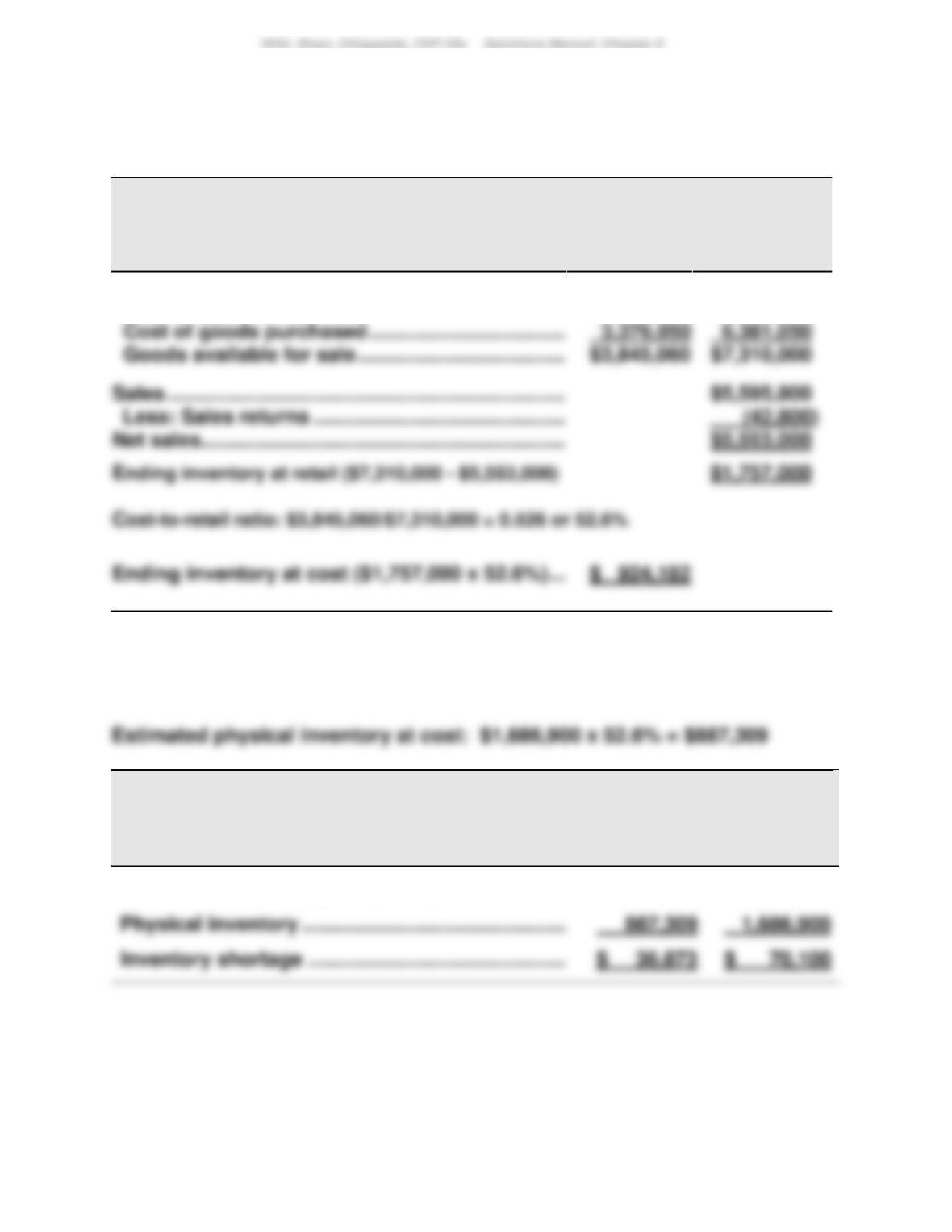

Problem 6-9AB (25 minutes)

Part 1

ALASKA COMPANY

Estimated Inventory

December 31

At Cost

At Retail

Goods available for sale

Beginning inventory……………………………………..

$ 469,010

$ 928,950

Cost of goods purchased ……………………………..

6,381,050

Less: Sales returns ………………………………………

Net sales ………………………………………………………..

Part 2

ALASKA COMPANY

Inventory Shortage

December 31

At Cost

At Retail

Estimated inventory (from part 1) ……………………….

$ 924,182

$ 1,757,000