Continuing Cookie Chronicle 1

Continuing Cookie Chronicle

(Note: This is a continuation of the Cookie Chronicle from Chapters 1 through 5.)

CCC6 Natalie is busy establishing both divisions of her business (cookie classes and mixer sales) and

completing her business degree. Her goals for the next 11 months are to sell one mixer per month and to

give two to three classes per week.

The cost of the fine European mixers is expected to increase. Natalie has just negotiated new terms

with Kzinski that include shipping costs in the negotiated purchase price (mixers will be shipped FOB

destination), but the supplier cannot guarantee the invoice price. Natalie has decided to use a periodic

inventory system and now must choose a cost flow assumption for her mixer inventory.

The following transactions occur in February to May 2015.

Feb. 2 Natalie buys two deluxe mixers on account from Kzinski Supply Co. for $1,150 ($575 each),

FOB destination, terms n/30.

16 She sells one deluxe mixer for $1,100 cash.

25 She pays the amount owed to Kzinski.

Mar. 2 She buys one deluxe mixer on account from Kzinski Supply Co. for $592, FOB destination,

terms n/30.

30 Natalie sells two deluxe mixers for a total of $2,200 cash.

31 She pays the amount owed to Kzinski.

Apr. 1 She buys two deluxe mixers on account from Kzinski Supply Co. for $1,172 ($586 each), FOB

destination, terms n/30.

13 She sells three deluxe mixers for a total of $3,300 cash.

30 Natalie pays the amount owed to Kzinski.

May 4 She buys three deluxe mixers on account from Kzinski Supply Co. for $1,800 ($600 each),

FOB destination, terms n/30.

27 She sells one deluxe mixer for $1,100 cash.

Instructions

(a) Prepare journal entries for each of the transactions.

(b) Determine the cost of goods available for sale. Recall from Chapter 5 that at the end of January,

Cookie Creations had three mixers on hand at a cost of $570 each.

(c) Calculate (i) ending inventory, (ii) cost of goods sold, (iii) gross profit, and (iv) gross profit rate

under each of the following methods: LIFO, FIFO, and average cost. (Round average unit cost to

three decimal places.)

(d) Natalie is thinking of getting a bank loan. If this is the only factor Natalie has to consider in

choosing an inventory cost flow assumption, which cost flow assumption would you recommend

that Natalie use? Why?

(a)

Feb. 2

Purchases ………………………………………..

1,150

Accounts Payable ………………………

1,150

Cash ………………………………………………..

1,100

Sales Revenue…………………………...

1,100

Accounts Payable ……………………………..

1,150

Cash ………………………………………….

1,150

Mar. 2

Purchases ………………………………………..

Accounts Payable ………………………

Cash ………………………………………………..

2,200

Sales Revenue…………………………...

2,200

Accounts Payable ……………………………..

Cash ………………………………………….

Apr. 1

Purchases ………………………………………..

1,172

Accounts Payable ………………………

1,172

Cash ………………………………………………..

3,300

Sales Revenue…………………………...

3,300

30

Accounts Payable ……………………………..

1,172

Cash ………………………………………….

1,172

May 4

Purchases ………………………………………..

1,800

Accounts Payable ………………………

1,800

Cash ………………………………………………..

1,100

Sales Revenue…………………………...

1,100

(b) COST OF GOODS AVAILABLE FOR SALE

Date

Explanation

Units

Unit Cost

Total Cost

Feb.

1

Beginning Inventory

3

$570

$1,710

Feb.

2

Purchase

2

2

1

1

2

May 4

Purchase

Total

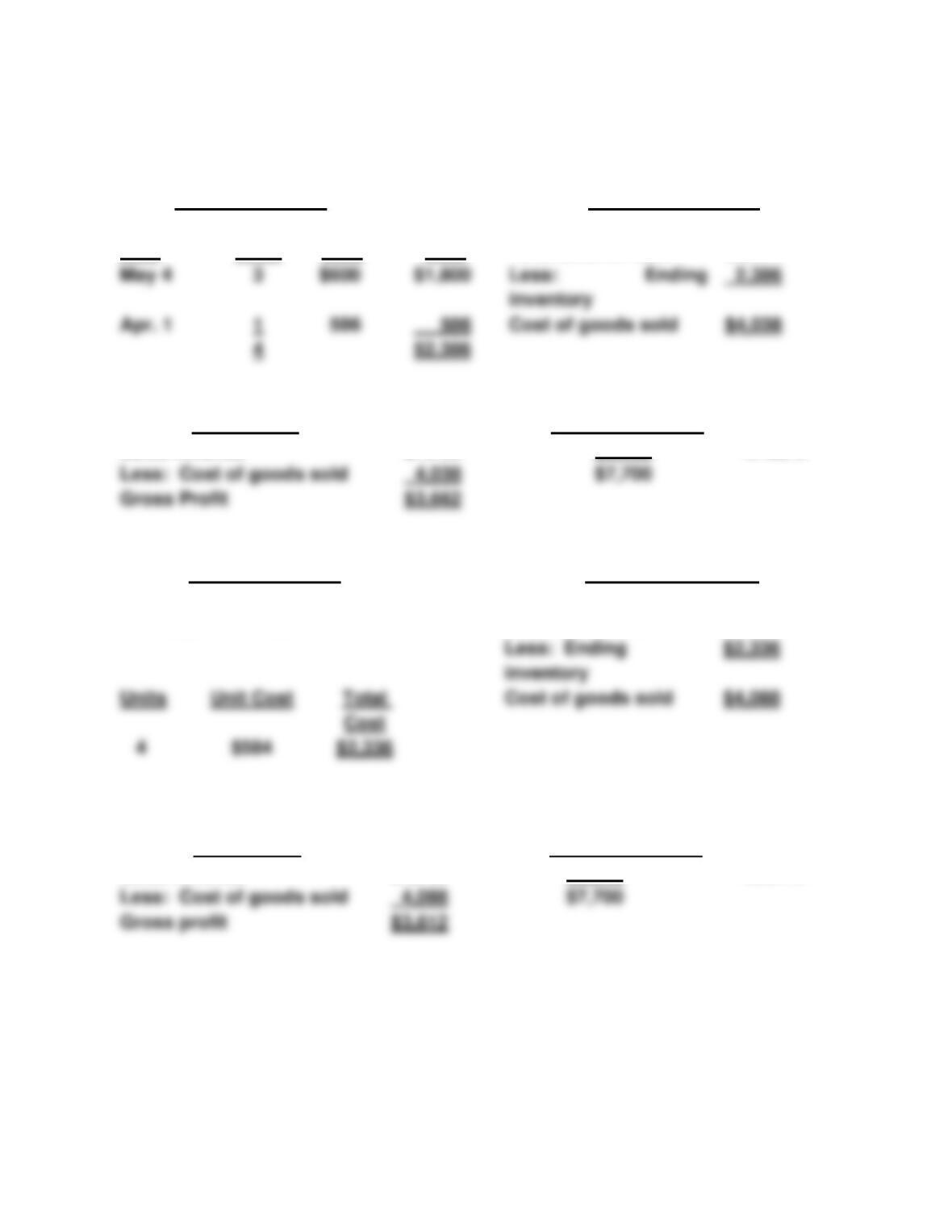

(c)

LIFO

Ending Inventory

Cost of Goods sold

Date

Units

Unit

Cost

Total

Cost

Cost of goods

available for sale

$6,424

Feb. 1

3

Less: Ending inventory

Feb. 2

1

Cost of goods sold

$4,139

Gross Profit

Gross Profit Rate

Sales revenue

$7,700*

$3,561

46.25%

Less: Cost of goods

sold

$7,700

Gross profit

$3,561

CONTINUING COOKIE CHRONICLE (Continued)

FIFO

Ending Inventory

Cost of Goods sold

Date

Units

Unit

Cost

Total

Cost

Cost of goods

available for sale

$6,424

May 4

Less: Ending

inventory

Apr. 1

Cost of goods sold

$4,038

Gross Profit

Gross Profit Rate

Sales revenue

$7,700

$3,662

47.56%

Less: Cost of goods sold

Gross Profit

Average Cost

Ending Inventory

Cost of Goods Sold

$6,424/11 = $584

Cost of goods

available for sale

$6,424

Less: Ending

inventory

$2,336

$2,336

Gross Profit

Gross Profit Rate

Sales revenue

$7,700

$3,612

46.91%

Less: Cost of goods sold

Gross profit

$3,612

(d) It shouldn’t actually matter which cost flow assumption Natalie

chooses for the purpose of the bank loan. Bankers should be able