171

CHAPTER 6

RECEIVABLES AND INVENTORIES

CLASS DISCUSSION QUESTIONS

1. Receivables are normally classified as (1)

accounts receivable, (2) notes receivable, or

(3) other receivables.

2. Transactions in which merchandise is sold

or services are provided on credit generate

accounts receivable.

5. Carter’s should use the direct write-off

method because it is a small business that

has a relatively small number and volume of

accounts receivable.

6. The allowance method

7. Contra asset

8. The accounts receivable and allowance for

doubtful accounts may be reported at a net

9. (1) The percentage rate used is excessive

in relationship to the volume of accounts

written off as uncollectible; hence, the

balance in the allowance is excessive.

(2) A substantial volume of old uncollectible

accounts is still being carried in the ac-

counts receivable account.

10. Manufacturing firms must accumulate the

costs for making product. The costs for mak-

the work-in-process costs are transferred to

the finished goods inventory account. Upon

sale, the finished goods costs are trans-

ferred to cost of goods sold, to be matched

against the revenue from sale. Since

merchandisers only purchase goods for re-

counting for the sale of completed goods is

similar for both types of firms.

11. No, they are not techniques for determining

physical quantities. The terms refer to cost

flow assumptions, which affect the determi-

nation of the cost prices assigned to items in

the inventory.

12. No, the term refers to the flow of costs rather

16. The LIFO reserve is the difference between

the FIFO and LIFO inventory valuation. The

analyst will adjust earnings to what they

would have been under FIFO. This is be-

cause the liquidation of a LIFO reserve

abnormally inflates gross profit and net in-

come.

17. Current Assets

18. Net realizable value (estimated selling price

172

EXERCISES

E6–1

Accounts receivable from the U.S. government are significantly different from receiva-

bles from commercial aircraft carriers such as Delta and United. Thus, Boeing should

E6–2

Due Date Interest Due at Maturity

a. Feb. 20 $450 [$40,000 × 0.09 × (45/360)]

b. May 22 $150 [$9,000 × 0.10 × (60/360)]

E6–3

a. MGM: 17.1% ($101,207,000 ÷ $592,937,000)

b. IBM: 2.2% ($256,000,000 ÷ $11,435,000,000)

c. Casino operations experience greater bad debt risk, since it is difficult to

control the creditworthiness of customers entering the casino. In addition,

individuals who may have adequate creditworthiness could overextend them-

173

E6–4

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accounts

Statement

Cash

+

Receivable

Feb. 14.

Feb. 14.

Operating

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Retained

Statement

Accounts Receivable

=

Earnings

Feb. 14.

Feb. 14.

Income Statement

expense

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Retained

Statement

Accounts Receivable

=

Earnings

Dec. 23.

45,000

45,000

Dec. 23.

Income Statement

Dec. 23.

Bad debt

expense

45,000

174

E6–4, Concluded

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accounts

Statement

Cash

+

Receivable

Operating

45,000

E6–5

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accounts

Statement

Cash

+

Receivable

Jan. 31.

8,000

–8,000

Statement of Cash Flows

Jan. 31.

Operating

8,000

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Allowance for

Statement

Receivable

Jan. 31.

175

E6–5, Concluded

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accounts

Allowance for

Statement

Receivable

–

Doubtful Accounts

Nov. 2.

32,000

–32,000

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Statement

Nov. 2.

Nov. 2.

Operating

32,000

176

E6–6

a.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accounts

Retained

Statement

Receivable

=

Earnings

–11,575

–11,575

Income Statement

Bad debt

expense

–11,575

b.

Balance Sheet

Statement of

+

Stockholders’ Equity

Income

Cash Flows

Accts.

Statement

Doubtful Accounts

E6–7

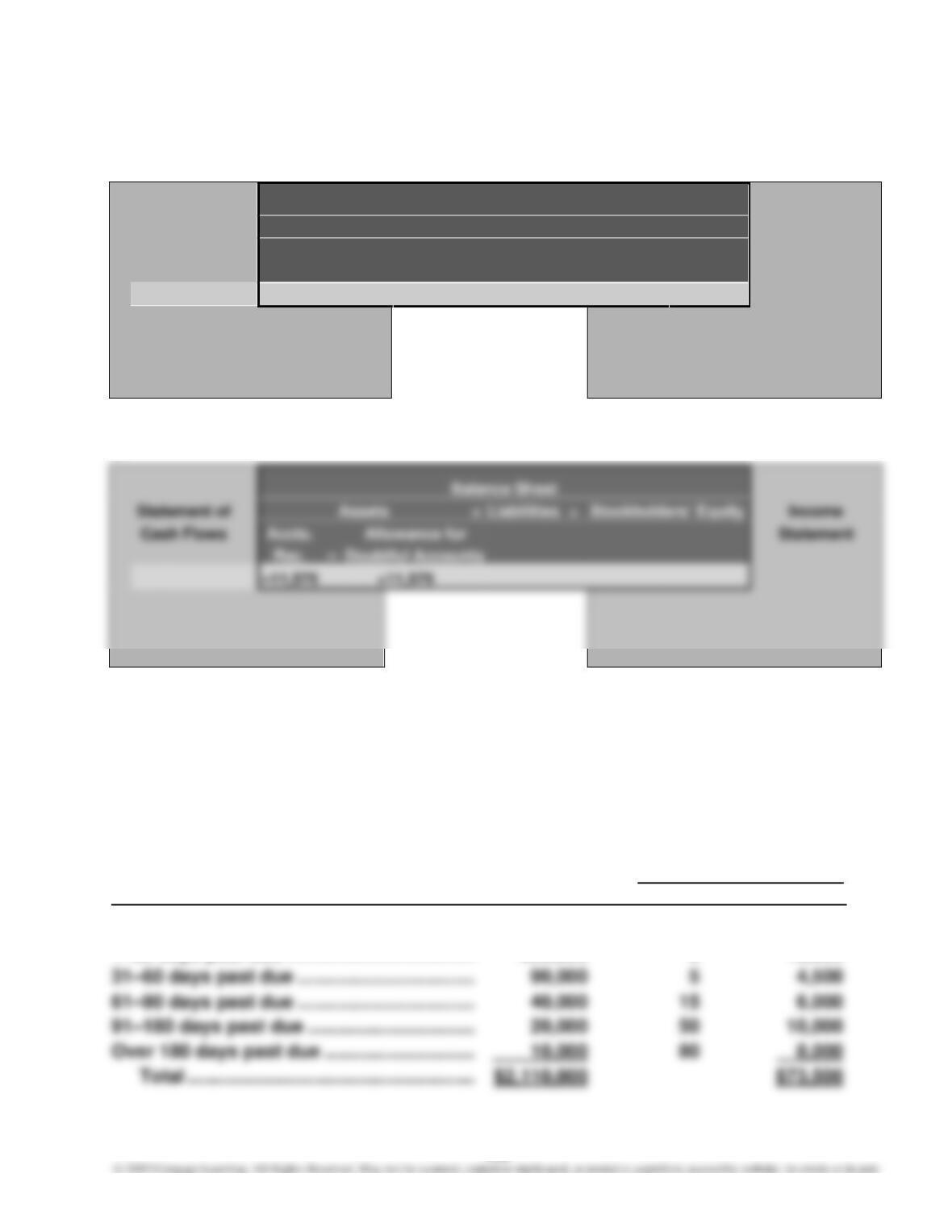

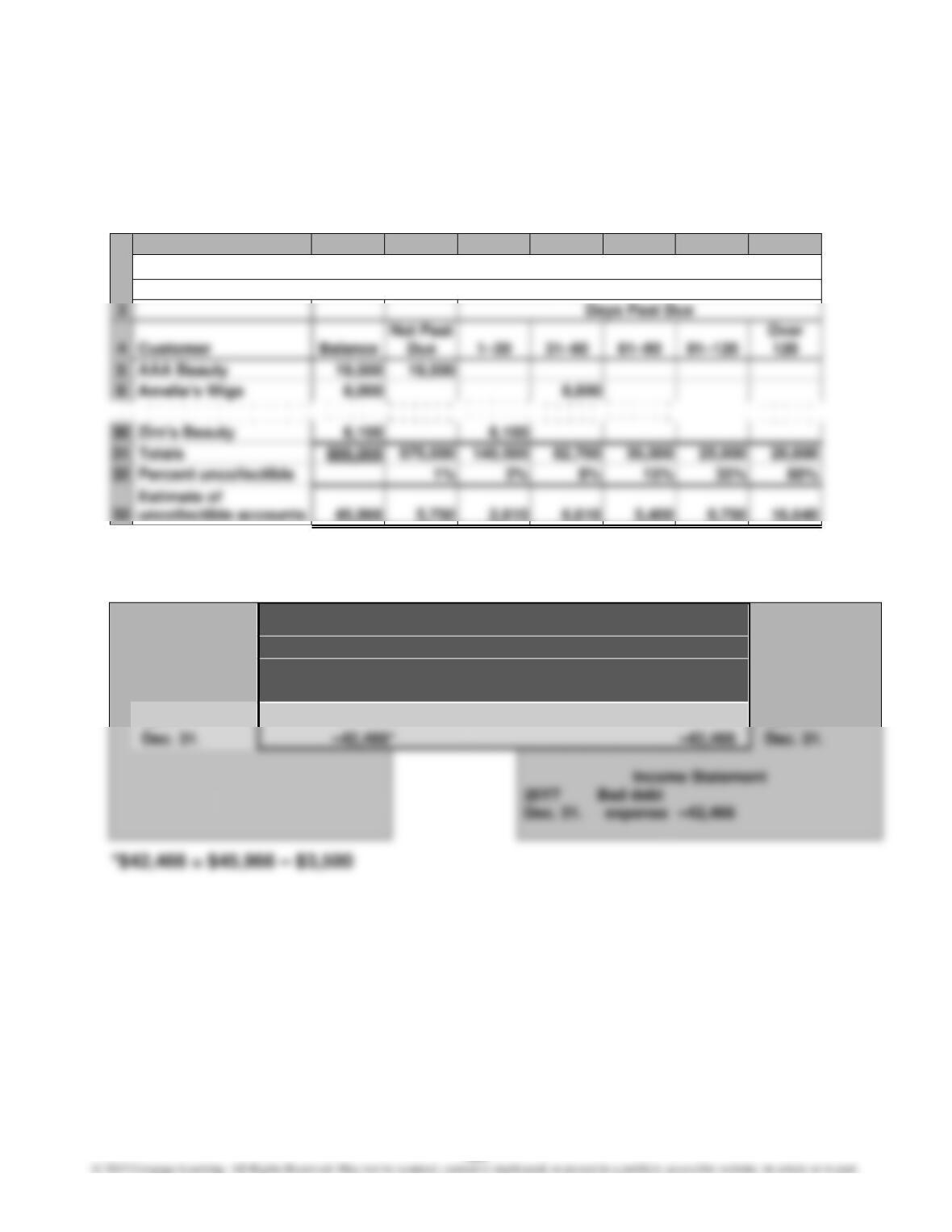

Estimated balance of Allowance for Doubtful Accounts: $73,500

Computed as shown below.

Estimated

Uncollectible Accounts

Age Interval Balance Percent Amount

Not past due ……………………………………….. $1,350,000 2% $27,000

1–30 days past due ……………………………… 600,000 3 18,000

E6–8

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

– Allowance for

Retained

Statement

Doubtful Accounts

=

Earnings

E6–9

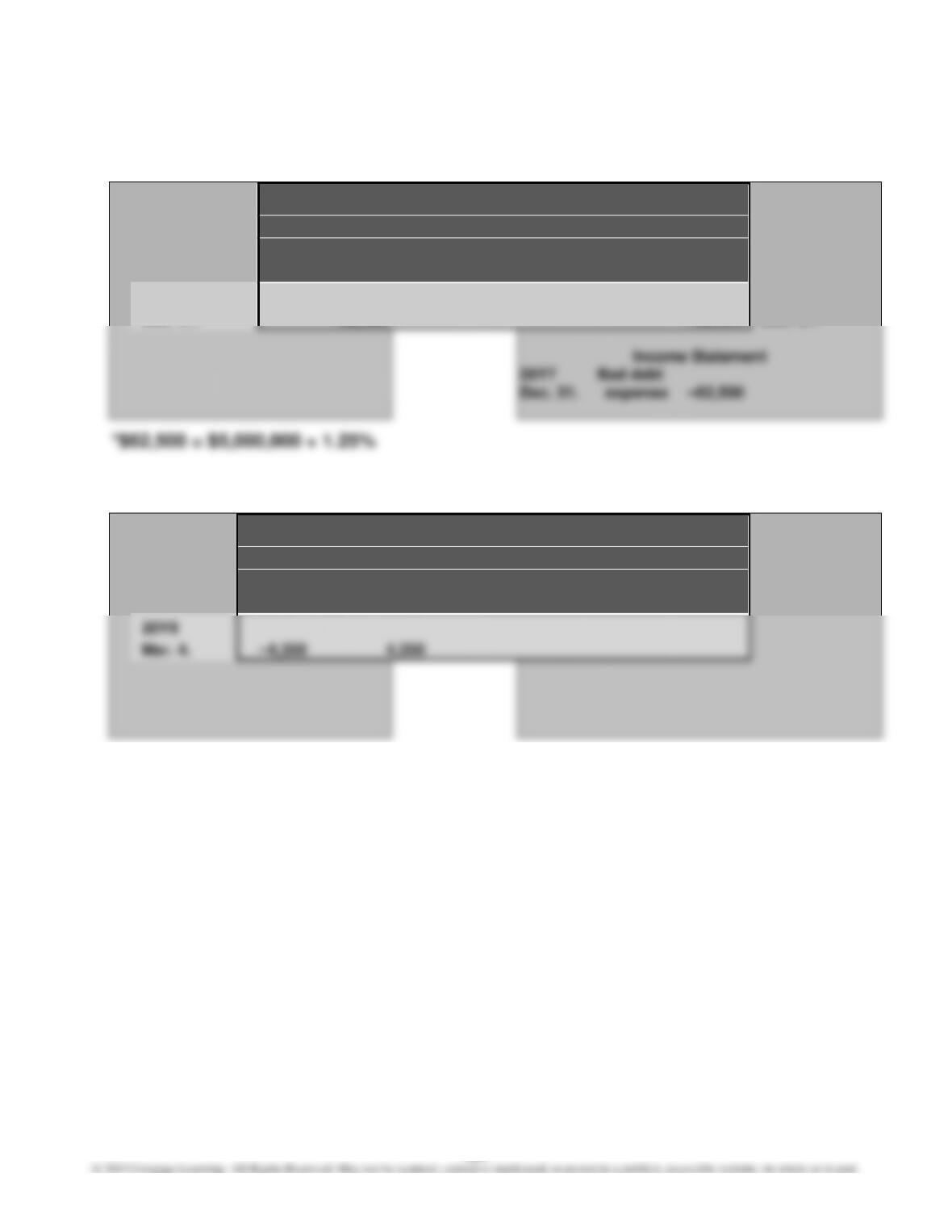

a. $108,000 ($21,600,000 × 0.005) c. $162,000 ($21,600,000 × 0.0075)

b. $125,000 ($145,000 – $20,000) d. $148,000 ($130,000 + $18,000)

E6–10

E6–11

E6–12

a. The three different inventories accumulate manufacturing costs as the product is

being produced. Costs flow through these accounts until the product is sold, and

the cost is matched on the income statement as cost of goods sold, shown as fol-

E6–13

a. The asset categories reflect the life cycle of a film. The initial “In development”

costs are associated with efforts to develop a new film. These costs would include

b. The description above sounds similar to a manufacturing firm. Raw materials (in

development) are transferred to work in process (in process), then to finished

goods (completed). Thus, the reclassification of costs through different asset cat-

egories as the film becomes more complete is similar to a manufacturing firm.

E6–14

a. $148,500 (90 units at $1,650)

b. $114,480 [(54 units × $1,200) + (36 units × $1,380)] = $64,800 + $49,680

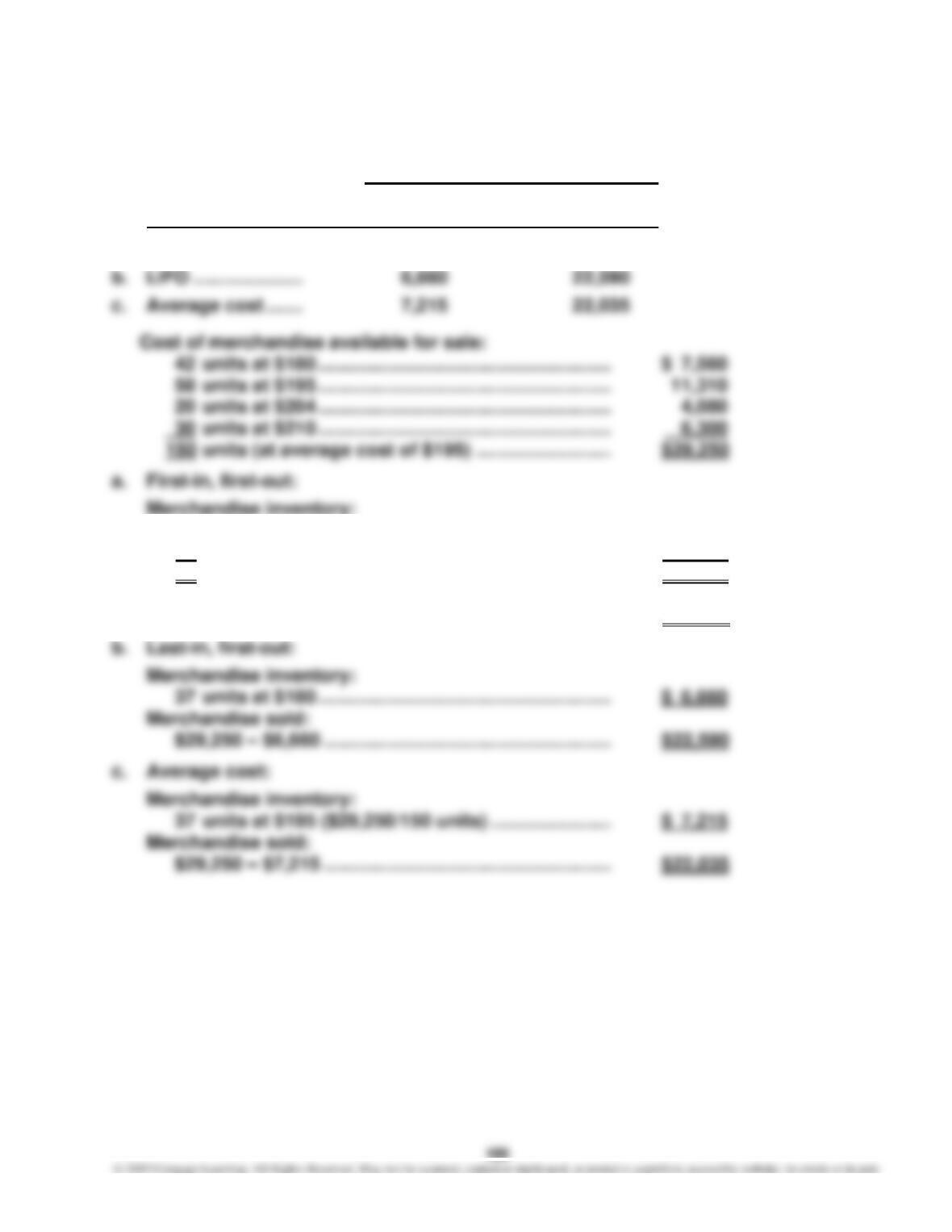

E6–15

Cost

Merchandise Merchandise

Inventory Method Inventory Sold

a. FIFO ………………… $7,728 $21,522

30 units at $210 ……………………………………………….. $ 6,300

7 units at $204 ……………………………………………….. 1,428

37 units …………………………………………………………… $ 7,728

Merchandise sold:

$29,250 – $7,728 ………………………………………………. $21,522

E6–16

1. a. FIFO inventory > (greater than) LIFO inventory

2. In periods of rising prices, the income shown on the company’s tax return would

be lower than if FIFO were used; thus, there is a tax advantage of using LIFO.

E6–17

2. The allowance for doubtful accounts should be deducted from accounts receiva-

ble.

A corrected partial balance sheet would be as follows:

ZABEL COMPANY

E6–18

A

B

C

D

E

F

G

1

Unit

Unit

Total

2

Inventory

Cost

Market

3

Commodity

Quantity

Price

Price

Cost

Market

LCM

4

Buffalo

35

$115

$120

$ 4,025

$ 4,200

$ 4,025

5

Dakota

67

90

75

6,030

5,025

5,025

6

Frontier

8

2,400

2,240

2,240

7

Midwest

83

3,320

2,490

2,490

8

Rainbow

9,000

9,400

9,000

E6–19

The merchandise inventory would appear in the Current Assets section, as follows:

183

PROBLEMS

P6–1

1.

A

B

C

D

E

F

G

H

1

Aging-of-Receivables Schedule

2

December 31, 20Y7

3

4

Balance

6,616

2.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

– Allowance for

Retained

Statement

Doubtful Accounts

=

Earnings

20Y7

20Y7

184

P6–1, Continued

3.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

– Allowance for

Retained

Statement

Doubtful Accounts

=

Earnings

20Y7

Dec. 31.

–62,500*

–62,500

20Y7

Dec. 31.

Dec. 31.

4.

Balance Sheet

Statement of

Assets

=

Liabilities

+

Stockholders’ Equity

Income

Cash Flows

Accounts

Allowance for

Statement

Receivable

–

Doubtful Accounts