6–1

Chapter 6

Fundamentals of Product and Service Costing

Learning Objectives

1. Explain the fundamental themes underlying the design of cost systems.

2. Explain how cost allocation is used in a cost management system.

3. Explain how a basic product costing system works.

4. Understand how overhead cost is allocated to products.

5. Explain the operation of a two-stage allocation system for product costing.

6. Describe the three basic types of product costing systems: job order, process, and operations.

Chapter Overview

I. COST MANAGEMENT SYSTEMS

II. FUNDAMENTAL THEMES UNDERLYING THE DESIGN OF COST SYSTEMS

FOR MANAGERIAL PURPOSES

III. COSTING IN A SINGLE PRODUCT, CONTINUOUS PROCESS INDUSTRY

• Basic Cost Flow Model

• Costing with no Work-in-Process Inventories

• Costing with Ending Work-in-Process Inventories

IV. COSTING IN A MULTIPLE PRODUCT, DISCRETE PROCESS INDUSTRY

• Predetermined Overhead Rates

• Product Costing of Multiple Products

• Choice of the Allocation Base for Predetermined Overhead Rate

• Choosing Among Possible Allocation Bases

V. MULTIPLE ALLOCATION BASES AND TWO-STAGE SYSTEMS

• Choice of Allocation Bases

VI. DIFFERENT COMPANIES, DIFFERENT PRODUCTION AND COSTING SYSTEMS

• Operations Costing: An Illustration

6–3

Chapter Outline

LO 6-1 Explain the fundamental themes underlying the design of cost

systems.

COST MANAGEMENT SYSTEMS

• A cost management system is a system that provides information about the costs of

processes, products, and services used and produced by an organization.

o A well-designed cost management system accumulates and reports costs that are relevant

to the decisions that managers make.

o These costs include those associated with the processes the organization uses to meet

customer needs, to serve the customers, and to comply with regulatory and tax authorities.

• Reasons to Calculate Product or Service Costs

o The purposes of calculating individual product (and service) cost include:

▪ Computing the inventory values and cost of goods sold for the financial statements.

▪ Helping various product managers make decisions regarding pricing, production,

promotion, and so on. (See Business Application box “Importance of Distinguishing

between Production Costs and Overhead Costs.”)

LO 6-2 Explain how cost allocation is used in a cost management system.

• Cost Allocation and Product Costing

o Costs that are common to two or more cost objects are likely to be allocated to those cost

objects on a somewhat arbitrary basis; such cost allocations can result in misleading

information and poor decisions.

• Cost Flow Diagram

o A cost flow diagram provides a graphical representation of the product costing process.

6–4

▪ Exhibit 6.1 illustrates a basic cost flow diagram.

• The cost object is the product.

• The direct materials and direct labor costs are “assigned” directly to the cost

objects; that is, we can observe the link between resources and the cost objects

that consume the resources in an unambiguous way.

• In this example, manufacturing overhead costs are allocated based on direct labor.

FUNDAMENTAL THEMES UNDERLYING THE DESIGN OF COST SYSTEMS FOR

MANAGERIAL PURPOSES

• Questions that need addressing before undertaking the design of a new cost system:

o How will managers use the information the system is designed to provide?

o What type of decisions will be made using the cost information?

o Will the benefits of improved decision making outweigh the costs of implementing the

new cost system?

• The following points relate to designing a new cost system for managerial purposes:

o Cost systems should have a decision focus.

LO 6-3 Explain how a basic product costing system works.

COSTING IN A SINGLE PRODUCT, CONTINUOUS PROCESS INDUSTRY

• Basic Cost Flow Model

o The fundamental framework for recording costs in any type of firm is the cost flow

model, which is the basic inventory equation.

6–5

Beginning balance (BB)

xx

Plus: Transfers in (TI)

xx

Total to account for

xx

o A third way to look at the inventory equation is the inventory T-account:

Inventory account

Beginning balance (BB)

Less: Transfers out (TO)

Plus: Transfers in (TI)

Ending balance (EB)

o The inventory equation applies to physical units and to the costs associated with the units.

• Costing with no Work-in-Process Inventories

o For a single product with a continuous production process, each individual unit of

product can be considered identical to every other one, so there is no need to trace costs

to individual units.

▪ When there are no work-in-process inventories, the cost assigned to each unit of

output produced can be calculated as:

Total manufacturing costs (materials, labor, and overhead) for the period

Total quantity of output for the period

• Example 1: In April, Baxter Paints started and completed production of 100,000

gallons of white paint. Total manufacturing costs incurred in April were

$1,000,000. There were no beginning and ending work-in-process inventories.

The following T-account shows the relations in terms of the physical units.

Beginning balance

Plus: Transfers in

Less: Transfers out

Ending balance

Beginning balance

Plus: Transfers in

1,000,000

Less: Transfers out

1,000,000

Ending balance

Less: Transfers out (TO)

xx

Ending balance (EB)

xx

6–6

• Costing with Ending Work-in-Process Inventories

o When ending work-in-process inventory is present, the denominator of the unit-cost

calculation requires modification.

▪ Since the ending work-in–process inventory is partially completed, the “equivalent”

unit of production must be calculated for the ending work-in-process inventory and

added to the number of units completed to determine the total quantity of output for a

period.

• Example 2: (Continued from Example 1): In May, Baxter Paints incurred a total

of $990,000 manufacturing white paint. The accountant prepared the following T-

account in physical units.

Inventory account – White Paint (gallons)

Beginning balance

0

Plus: Transfers in

110,000

Less: Transfers out

90,000

Ending balance

20,000

(50% complete)

For the 20,000 gallons of paint in process at the end of May, they were on average

50 percent complete and was equivalent to 10,000 gallons of finished paint (=

20,000 gallons × 50%). Total quantity of output for May became 100,000 gallons

(= 90,000 gallons completed and transferred out + 10,000 equivalent gallons).

Each gallon of white paint was assigned a cost of $9.90 (= $990,000 ÷ 100,000

gallons). The $990,000 total manufacturing costs incurred were allocated to two

cost objects:

Inventory account – White Paint (gallons)

Beginning balance

0

Plus: Transfers in

990,000

Less: Transfers out

Ending balance

99,000

6–7

See Demonstration Problem 1

COSTING IN A MULTIPLE PRODUCT, DISCRETE PROCESS INDUSTRY

• When a firm manufactures multiple-products using a manufacturing process that takes place

in a series of discrete steps that differ in detail depending on the product, the benefits of more

detailed costing often outweigh the costs.

o The cost flow diagram in Exhibit 6.3 describes the problem of taking costs from the three

basic cost pools (direct materials, direct labor, and manufacturing overhead) and

allocating them to the cost objects (various products).

▪ Direct costs (direct materials and direct labor) can be directly traced or assigned to the

products at relatively low cost. Work orders, inventory requisitions, and skilled

workers’ time spent are specific to the individual products.

▪ A problem arises, however, with manufacturing overhead. By definition, these costs

cannot be identified directly (for a reasonable cost) with individual units of product. If

they could be, they would be included in either direct materials or direct labor.

Therefore: we need to identify one or more allocation bases to use to allocate the

manufacturing overhead to the various products.

LO 6-4 Understand how overhead cost is allocated to products.

• Predetermined Overhead Rates

o A predetermined overhead rate represents the cost per unit of the allocation base used

to charge manufacturing overhead to products.

6–8

▪ Example 3: Grange Boats makes two products, C-20 and C-27 sailboats, and uses

direct labor hours to allocate manufacturing overhead to products. For next January,

the budget data indicate that 10 C-27s and 30 C-20s will be produced using 2,000 and

3,000 direct labor hours, respectively. The total manufacturing overhead is expected

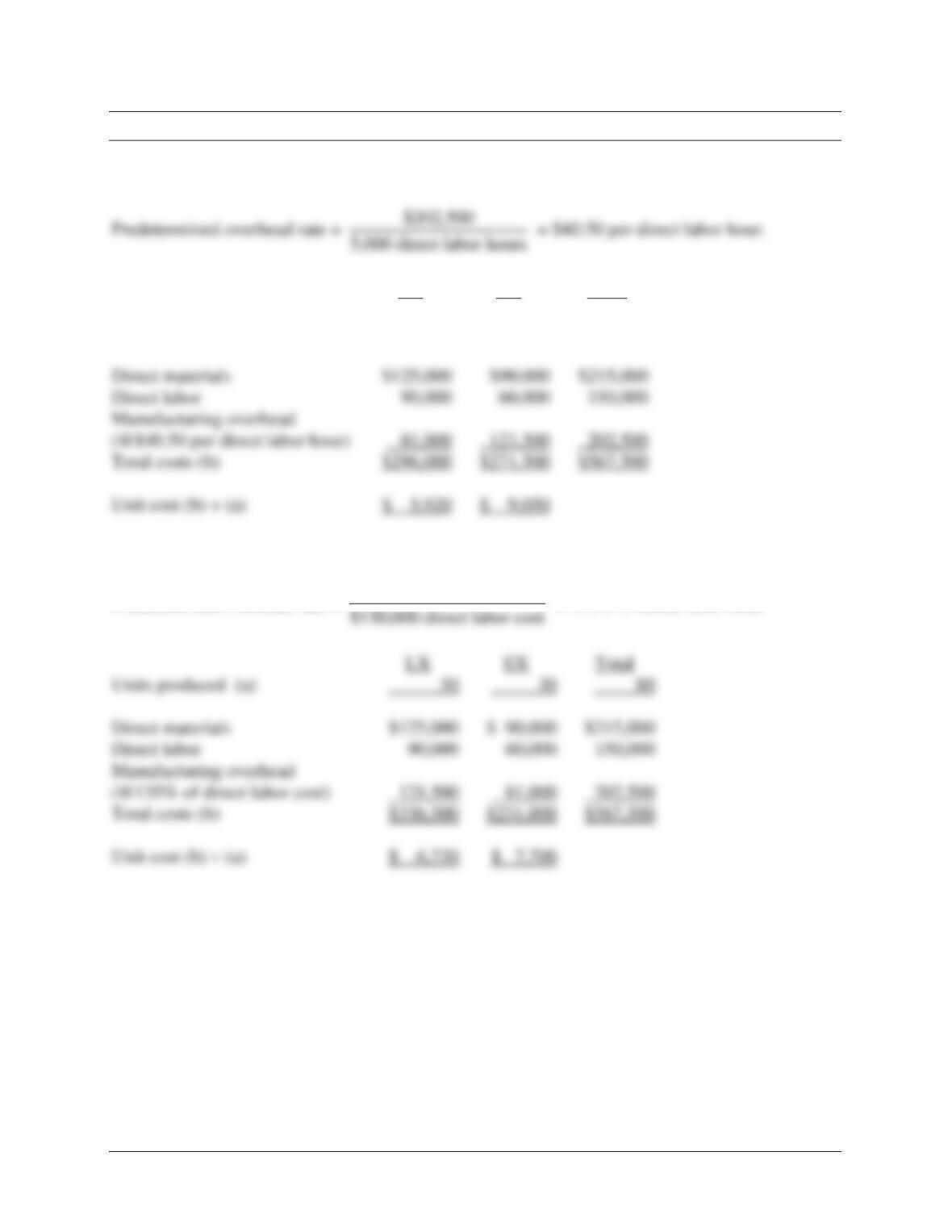

to be $180,000. The predetermined overhead rate can be calculated as:

Predetermined overhead rate =

$180,000

(2,000 + 3,000) direct labor hours

• Product Costing of Multiple Products

o The cost assigned to each unit of output produced in a multiple-product, discrete process

firm can be calculated as:

Total manufacturing costs (materials, labor, and overhead) for a product

Total quantity of output for a product

o The product costs are estimates, not actual results.

▪ They are useful for decisions about future pricing and whether to continue making a

particular product.

6–9

• Choice of the Allocation Base for Predetermined Overhead Rate

o There are at least two reasons why a particular allocation base is chosen:

o Using direct labor dollars instead of direct labor hours as the allocation base changes the

unit cost (as illustrated below).

▪ Example 5 (Continued from Examples 3 and 4): If Grange Boats selects instead direct

labor cost as the allocation base, then the predetermined overhead rate can be

calculated as:

See Demonstration Problem 2

• Choosing Among Possible Allocation Bases

o The choice of possible allocation bases, though arbitrary, could have important

implications for decision making.

6–10

▪ Cost estimation methods can be applied to aid in making the choice.

• The overhead accounts can be analyzed to determine which allocation base seems

to be more highly related to overhead.

LO 6-5 Explain the operation of a two-stage allocation system for product

costing.

MULTIPLE ALLOCATION BASES AND TWO-STAGE SYSTEMS

• Exhibit 6.7 provides more detail on the components of manufacturing overhead at Grange

Boats.

• A close inspection of the components of manufacturing overhead may reveal that more than

one factor is driving the resource consumption during production. If this is the case, we can

use two or more allocation bases to allocate manufacturing overhead to the products.

o The approach is referred to as a two-stage cost allocation. The process has two-steps:

6–11

o An alternative view is shown below.

Direct costs:

Direct materials

Direct labor

Assigned to

Cost

objects:

o Example 6 (Continued from Examples 3 and 4): An analysis of Grange Boats’ January

budget data shows that the total machine-related overhead is $72,000 and there are 4,000

machine hours (1,000 machine hours for C-27s and 3,000 machine hours for C-20s), so

the machine-related overhead rate is $18 per machine hour (= $72,000 ÷ 4,000 machine

hours).

The total labor-related overhead is $108,000 and the direct labor costs are $150,000

($72,000 for C-27s and $78,000 for C-20s), so the labor-related overhead rate is 72% of

direct labor cost (= $108,000 ÷ $150,000 direct labor cost).

Manufacturing

overhead

First stage

allocation

Cost pools

Second stage

allocation

6–12

• Choice of Allocation Bases

o In a two-stage allocation system:

▪ Allocation bases still have to be chosen that best reflect the relation between overhead

incurred and activity.

LO 6-6 Describe the three basic types of product costing systems: job order,

process, and operations.

DIFFERENT COMPANIES, DIFFERENT PRODUCTION AND COSTING SYSTEMS

• Different companies have different production and costing systems.

o The two production processes that sit at the opposite end of the production spectrum can

be described as discrete (such as boat building) and continuous (such as paint

manufacturing), respectively.

6–13

▪ Process costing is an accounting system used when identical units are produced

through a series of uniform production steps.

▪ Continuous flow processing is a system that generally mass-produces a single,

homogeneous output in a continuing process.

• Process systems are used in manufacturing chemicals, grinding flour, and refining

oil.

• Operations Costing: An Illustration

o The design of the cost system is fundamentally the same.

6–14

Matching

A.

Continuous flow processing

F.

Operation costing

B.

Cost management system

G.

Predetermined overhead rate

C.

Job

H.

Process costing

D.

Job costing

I.

Two-stage cost allocation

E.

Operation

_____ 1. A system that provides information about the costs of processes, products, and

services used and produced by an organization.

_____ 2. Represents the cost per unit of the allocation base used to charge manufacturing

overhead to products and is calculated from the budgeted data.

_____ 3. The process of first allocating costs to intermediate cost pools and then to the

individual cost objects using different allocation bases.

_____ 4. Units of a product that are easily distinguishable from other units.

_____ 5. A system that generally mass-produces a single, homogeneous output in a continuing

process.

_____ 6. A standardized method or technique of making a product that is repetitively

performed.

_____ 7. An accounting system used when identical units are produced through a series of

uniform production steps.

_____ 8. A hybrid costing system often used in manufacturing goods that have some common

characteristics plus some individual characteristics.

_____ 9. An accounting system that traces costs to individual units or to specific jobs, contracts,

or batches of goods.

6–15

Matching Answers

1. B

Multiple Choice

1. Which of the following statements is correct?

a. A cost flow diagram is helpful by providing a graphical representation of the product

costing process.

b. Manufacturing overhead can be directly traced to products.

c. The cost system should be tailored to the needs of accountants.

d. The benefits of accurate cost information always outweigh the costs of the information

system.

2. Which of the following statements about the design of the cost systems is correct?

a. Cost systems should have a decision focus.

b. Different cost information is used for different purposes.

c. Cost information for managerial purposes must meet the cost-benefit test.

d. All of the above.

3. In June, 30,000 bushels of corn are 70% completed in the ending work-in-process inventory.

What are the equivalent units of production?

a. 18,000 bushels

b. 19,500 bushels

c. 21,000 bushels

d. 24,000 bushels

Use the following information to answers questions 4 through 7:

Company B produces two products, P1 and P2, at its two departments: Machining and Assembly.

The accountant tries to allocate overhead costs to the two products.

Overhead

P1

P2

Total

Machining

$300,000

1,200 machine hours

800 machine hours

2,000 machine hours

Assembly

150,000

600 labor hours

900 labor hours

1,500 labor hours

Total

$450,000

4. If the accountant decides to allocate overhead based on machine hours, what is P2’s share of

the total overhead costs?

a. $180,000

b. $200,000

c. $220,000

d. $240,000

5. If the accountant decides to allocate overhead based on labor hours, what is P1’s share of the

total overhead costs?

a. $180,000

b. $200,000

c. $220,000

d. $240,000

6–17

6. If the accountant chooses machine hours for Machining and labor hours for Assembly as

allocation bases, what is the overhead rate at Machining?

a. $100 per labor hour

b. $140 per labor hour

c. $120 per machine hour

d. $150 per machine hour

7. If the accountant chooses machine hours for Machining and labor hours for Assembly as

allocation bases, what is P1’s share of the total overhead costs?

a. $180,000

b. $240,000

c. $270,000

d. $300,000

8. For a two-stage allocation system:

a. The first stage is the most difficult to accomplish.

b. Cost pools ideally consist of homogeneous cost items.

c. Exactly two overhead rates are required.

d. The allocation bases bear no relationship with the overhead costs.

9. Which of the following statements is not correct?

a. Jobs are indistinguishable from each other.

b. Companies that produce customized products use job costing methods.

c. Companies that generally mass-produce a single, homogeneous output in a continuing

process adopt the continuous flow processing.

d. Operation is a standardized method of making a product.

10. Operations costing:

a. Is a hybrid costing system.

b. Is suitable when different products use the same production process and different

materials for input.

c. Combines features from both job and process costing.

d. All of the above.

11. Job order system and process system are similar in the sense that:

a. Both use the same inventory costing method.

b. Both keep track of prime costs, but not overhead items.

c. Both use the same manufacturing technique.

d. Both require inputs of direct materials, direct labor, and overhead.

12. The basic inventory equation can be represented by:

a. BB + TI = TO + EB.

b. BB – TI = TO + EB.

c. BB + EB = TI + TO.

d. BB + TO – TI = EB.

6–18

Multiple Choice Answers

6–19

Demonstration Problem 1

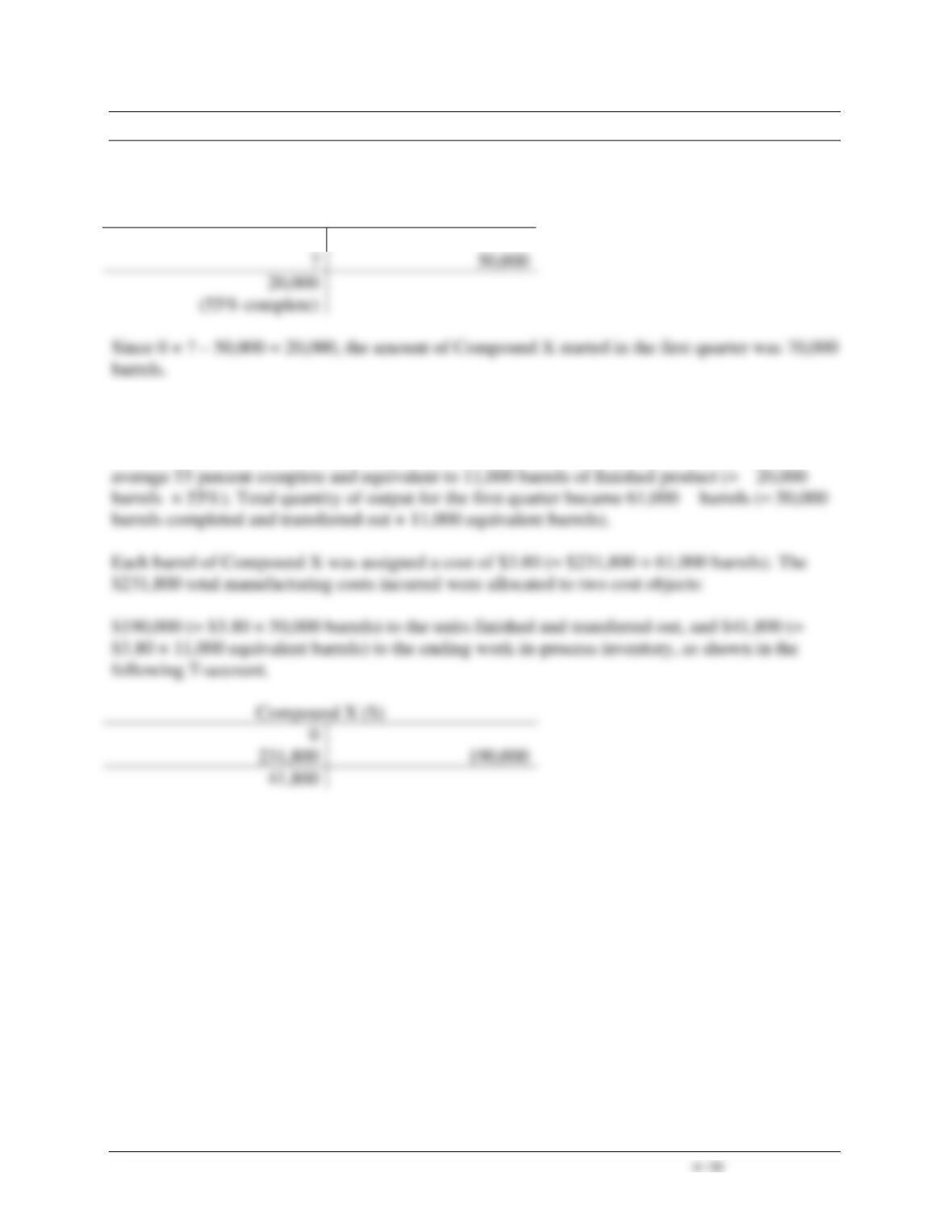

In the first quarter of operation, the Blending Department of ChemUSA produced 50,000 barrels

of Compound X and left 20,000 barrels in ending work-in-process inventory which was, on

average, 55 percent completed. A total of $231,800 was incurred in that period. There was no

beginning work-in-process inventory.

Required:

1. Determine the amount of Compound X started in the first quarter.

2. Compute the cost of Compound X transferred to finished goods and the amount of work-in–

process inventory as of the end of the first quarter.

Demonstration Problem 1 – Solution

Part 1

Compound X (barrels)

0

0

Part 2

For the 20,000 barrels of Compound X in process at the end of the first quarter, they were on

6–21

Demonstration Problem 2

Capable Golf Cart, Inc. (CGC) manufactures two models of golf cart: LX and EX. The budget

data for next month is available.

LX

EX

Total

Units produced

50

30

80

Direct labor hours

2,000

3,000

5,000

Machine hours

1,500

1,200

2,700

Direct materials

$125,000

$90,000

$215,000

Direct labor

90,000

60,000

150,000

Manufacturing overhead

202,500

Total

$567,500

Required:

1. Compute the reported unit cost for each product if direct labor hours are used as the

allocation base.

2. Compute the reported unit cost for each product if direct labor costs are used as the allocation

base.

3. Compute the reported unit cost for each product if machine hours are used as the allocation

base.

6–22

Demonstration Problem 2 – Solution

Part 1

LX

EX

Total

Units produced (a)

50

30

80

Direct labor hours

2,000

3,000

5,000

Direct materials

$90,000

Direct labor

150,000

(@$40.50 per direct labor hour)

Total costs (b)

Unit cost (b) ÷ (a)

Part 2

Predetermined overhead rate =

LX

EX

Total

Units produced (a)

80

Direct materials

Direct labor

150,000

(@135% of direct labor cost)

Total costs (b)

Unit cost (b) ÷ (a)

$202,500

= 135% of direct labor cost.

Demonstration Problem 2 – Solution, continued

Part 3

Predetermined overhead rate =

$202,500

2,700 machine hours

= $75 per machine hour.

6–24

Demonstration Problem 3

Jim is a florist who runs Bountiful Flower Shop as a sole owner. During the third week of June,

he received two orders for flower bouquets that required same operations but different

flower/basket combinations. Orders 471 and 472 were for a wedding hall and a business

conference, respectively. The following information was available.

Order 471

Order 472

Total

Number of bouquets

120

90

210

Flowers

$1,800

$1,080

$2,880

Baskets

600

360

960

Supplies

240

90

330

Total costs of materials

$2,640

$1,530

$4,170

Direct labor in operation

$ 630

Overhead in operation

1,155

Total costs in operation

$1,785

Required:

Determine the total cost and unit cost for Orders 471 and 472.

6–25

Demonstration Problem 3 – Solution

The costs of materials can be assigned directly to the two orders. Because the time and the effort

required to put together each bouquet is essentially the same, Jim could allocate the operation

costs based on the number of units (bouquets) assembled. That is,