6-12

1.

Cost of goods available for sale

=

Cost of

goods sold

+

Ending

inventory

Beginning

inventory

and

purchases

Number

of units

x

Unit

cost

=

Total

Cost

+

2.

Cost of goods available for sale

=

Cost of

goods sold

+

Ending

inventory

Beginning

inventory

and

purchases

Number

of units

x

Unit

cost

=

Total

Cost

+

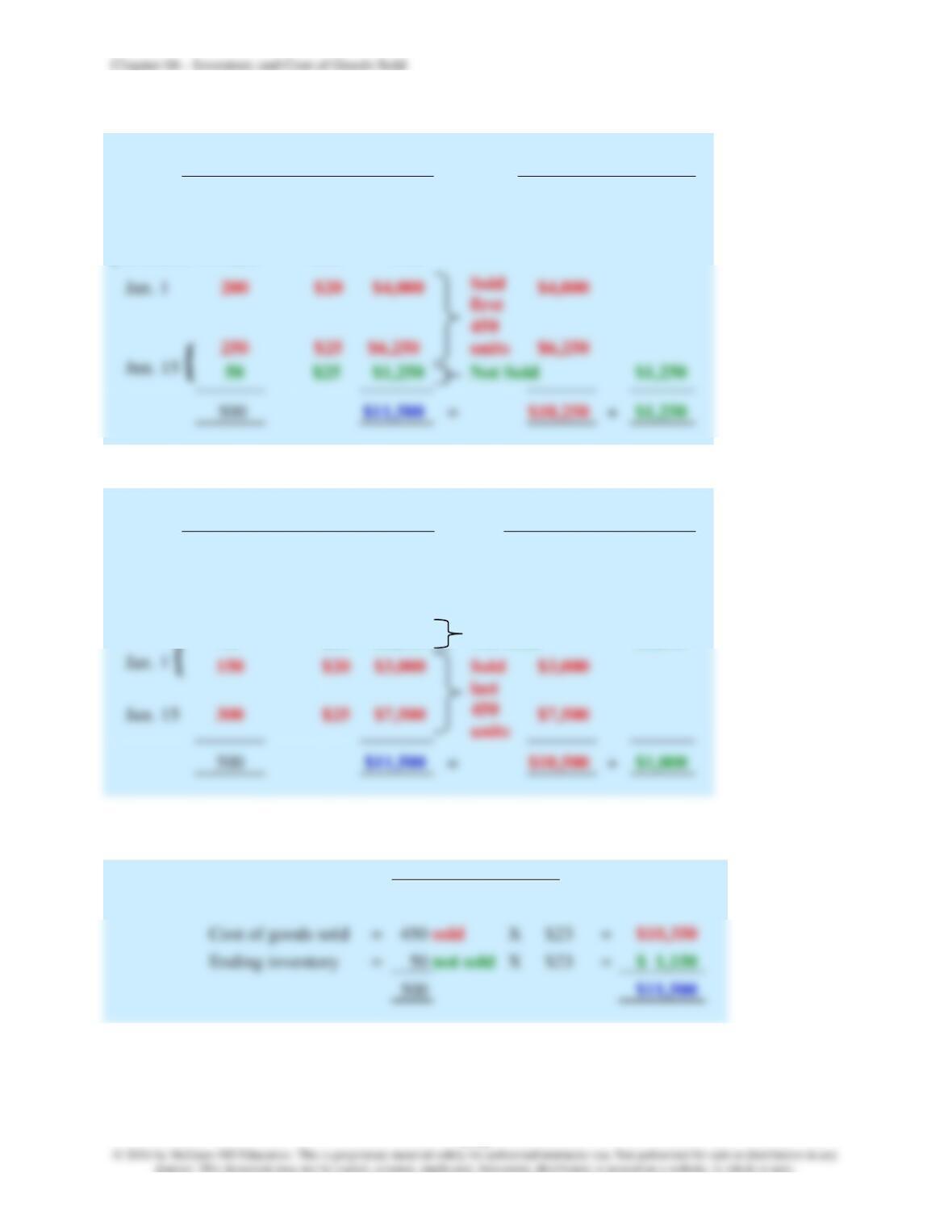

50

$20

$1,000

Not Sold

$1,000

3.

Weighted-average unit cost

=

$11,500

=

$23

500

Cost of goods sold

=

X

$23

=

Ending inventory

=

X

$23

=

500

Chapter 06 – Inventory and Cost of Goods Sold

6-13

Problem #2

A company accounts for its inventory using FIFO with a perpetual system. At the beginning of

March, the company has inventory of $40,000.

Required:

Record the following transactions for the company for the month of March:

1. On March 7, the company purchases additional inventory for $65,000 on account, terms 3/10,

n/30.

2. On March 7, the company purchases additional inventory for $65,000 on account, terms 3/10,

n/30.

3. On March 10, inventory that cost $5,000 arrived damaged and was returned for a full refund.

4. On March 16, the company makes full payment for inventory purchased on March 7,

excluding inventory returned and the discount received.

5. During the month of March, revenue from inventory sales totals $85,000. All sales are for

cash. The cost of inventory sold is $35,000.

Solution:

1.

Inventory 65,000

6-14

Problem #3

J-Lo Fashions provides year-round specialty jeans. At December 31, the company’s records

show the following amounts in ending inventory for each item.

Inventory items

Quantity

Cost

Per unit

Market

per unit

Fall jeans

50

$100

$ 70

Winter jeans

200

120

140

Spring jeans

300

150

180

Required:

1. Determine ending inventory using the lower of cost and net realizable value.

2. Record any necessary year-end adjustment associated with the lower of cost and net realizable

value.

Solution:

1.

Inventory items

Quantity

Cost

per unit

NRV

per unit

Per unit lower

of cost or NRV

Total lower

of cost or

NRV

Fall jeans

50

$100

$ 70

➔

$ 70

$ 3,500

Winter jeans

140

➔

Spring jeans

180

➔

$72,500

2.

December 31

Debit

Credit

Cost of Goods Sold

Chapter 06 – Inventory and Cost of Goods Sold

6-15

Key Points by Learning Objective

LO6-1 Trace the flow of inventory costs from manufacturing companies to merchandising

companies.

LO6-2 Understand how cost of goods sold is reported in a multiple-step income statement.

Inventory is a current asset reported in the balance sheet and represents the cost of inventory not

yet sold at the end of the period. Cost of goods sold is an expense reported in the income

statement and represents the cost of inventory sold.

LO6-3 Determine the cost of goods sold and ending inventory using different inventory cost

methods.

LO6-4 Explain the financial statement effects and tax effects of inventory cost methods.

Generally, FIFO more closely resembles the actual physical flow of inventory. When inventory

LO6-5 Record inventory transactions using a perpetual inventory system.

The perpetual inventory system maintains a continual—or perpetual—record of inventory

purchased and sold. When companies purchase inventory using a perpetual inventory system,

Chapter 06 – Inventory and Cost of Goods Sold

6-16

LO6-6 Apply the lower of cost and net realizable value rule for inventories.

We report inventory at the lower of cost and net realizable value; that is, at cost (specific

Analysis

LO6-7 Analyze management of inventory using the inventory turnover ratio and gross

profit ratio.

The inventory turnover ratio indicates the number of times the firm sells, or turns over, its

Appendixes

LO6-8 Record inventory transactions using a periodic inventory system.

Using the periodic inventory system, we record purchases of inventory, freight-in, purchase

LO6-9 Determine the financial statement effects of inventory errors.

In the current year, inventory errors affect the amounts reported for inventory and retained

Chapter 06 – Inventory and Cost of Goods Sold

6-17

Common Mistakes

Common Mistake

Many students find it surprising that companies are allowed to report inventory costs using

assumed amounts rather than actual amounts. Nearly all companies sell their actual inventory in

a FIFO manner, but they are allowed to report it as if they sold it in a LIFO manner. Later, we’ll

see why that’s advantageous.

Common Mistake

In calculating the weighted-average unit cost, be sure to use a weighted average of the unit cost

instead of the simple average. In the example above, there are three unit costs: $7, $9, and $11. A

simple average of these amounts is $9 [= (7 + 9 + 11) ÷ 3]. The simple average, though, fails to

Common Mistake

FIFO and LIFO describe more directly the calculation of cost of goods sold, rather than ending

inventory. For example, FIFO (first-in, first-out) directly suggests which inventory units are

assumed sold (the first ones in) and therefore used to calculate cost of goods sold. It is implicit

under FIFO that the inventory units not sold are the last ones in and are used to calculate ending

inventory.

Common Mistake

amount generated over a period) with a balance sheet item (an amount at a particular date), the

balance sheet item needs to be converted to an amount over the same period. This is done by

Many students use ending inventory rather than average inventory in calculating the inventory

turnover ratio. Generally, when you calculate a ratio that includes an income statement item (an

Chapter 06 – Inventory and Cost of Goods Sold

6-18

Decision Points

Question

Accounting Information

Analysis

When comparing

inventory amounts

between two

companies, does the

choice of inventory

method matter?

The LIFO difference

reported in the notes to the

financial statements

When inventory costs are rising, FIFO

results in a higher reported inventory.

The LIFO difference can be used to

compare inventory of two companies

if one uses FIFO and the other uses

LIFO.

Question

Accounting Information

Analysis

Is the company

effectively managing

its inventory?

Inventory turnover ratio

and average days in inventory

Question

Accounting Information

Analysis

For how much is a

company able to sell a

product above its

cost?

Gross profit and net sales

The ratio of gross profit to net sales

indicates how much inventory sales

exceeds inventory costs for each $1 of

sales.

A high inventory turnover ratio (or

low average days in inventory)

generally indicates that the company’s

Chapter 06 – Inventory and Cost of Goods Sold

6-19

Career Corner

Career Corner

Many career opportunities are available in tax accounting. Because tax laws constantly change

and are complex, tax accountants provide services to their clients not only through income tax

statement preparation but also by formulating tax strategies to minimize tax payments. The

choice of LIFO versus FIFO is one such example.

Chapter 06 – Inventory and Cost of Goods Sold

6-20

Ethical Dilemma

Ethical Dilemma

Diamond Computers, which is owned and operated by Dale Diamond, manufactures and sells

different types of computers. The company has reported profits every year since its inception in

2002 and has applied for a bank loan near the end of 2018 to upgrade manufacturing facilities.

These upgrades should significantly boost future productivity and profitability.

In preparing the financial statements for the year, the chief accountant, Sandy Walters,

mentions to Dale that approximately $80,000 of computer inventory has become obsolete and a

write-down of inventory should be recorded in 2018.

Dale understands that the write-down would result in a net loss being reported for company

operations in 2018. This could jeopardize the company’s application for the bank loan, which

would lead to employee layoffs. Dale is a very kind, older gentleman who cares little for his

personal wealth but who is deeply devoted to his employees’ well-being. He truly believes the

loan is necessary for the company’s sustained viability. Dale suggests Sandy wait until 2019 to

write down the inventory so that profitable financial statements can be presented to the bank this

year.

Explain how failing to record the write-down in 2018 inflates profit in that year. How would

this type of financial accounting manipulation potentially harm the bank? Can Sandy justify the

manipulation based on Dale’s kind heart for his employees?

Key Issues

• Writing off inventory reduces net income and total assets in the year of the write-off. By

delaying the write-off, the company shifts profits from the following year to the current

year, overstating current performance.

• Proper reporting vs. the long-term care of the company and its employees

Option 1: Wait to book the write-off

• Booking the write-off could be very damaging to the long-term health of the company

and its employees. Missing out on the loan could damage the profitability of future years,

leading to layoffs.

• Dale should be commended for his attentiveness to his employees’ careers.

• Accounting rules can be bent a little to help the company and employees, and five years

from now, it will not matter whether the write-off was booked in 2018 or 2019.

• As an employee, Sandy should do whatever her boss asks her to do. Any responsibility

for wrongdoing would fall on Dale.

Chapter 06 – Inventory and Cost of Goods Sold

6-21

Option 2: Book the write-off now

• The company is in the situation they are in concerning the obsolete inventory because of

business decisions and circumstances over the past few years. Bad decision making

should not be corrected via creative accounting.

• Despite the possible increased productivity that would be generated from the loan that

will fund upgrades, there is no guarantee that these increases will lead to enough profits

to offset the write-off if postponed to 2019. Then the company will be in a similar

situation a year later.

• Sandy should realize that her responsibility is to present accurate financial statements, not

please Dale’s good intentions. If this write-off is postponed and then later discovered by

auditors, then she has lost her credibility and may personally lose her own job despite

saving the job of many others.