CHAPTER 6 Inventories

Prob. 6–2B (Concluded)

2. Total sales………………………………………………………………………… $525,250

*

CHAPTER 6 Inventories

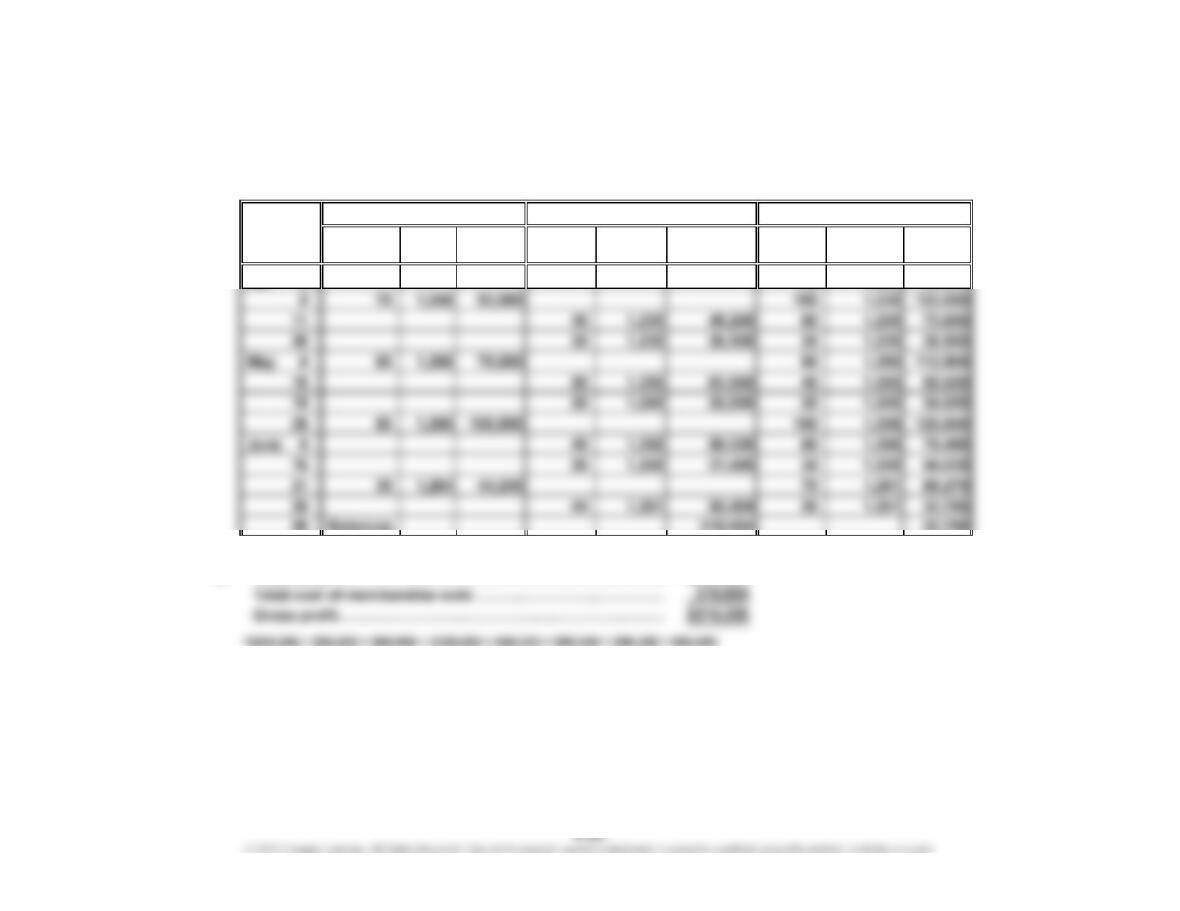

Prob. 6–3B

1.

Unit Total Total Total

Quantity Cost Cost Quantity Unit Cost Cost Quantity Unit Cost Cost

Apr. 3 25 1,200 30,000

2. Total sales…………………………………………………………

…

$525,250

3. $32,786 (26 units × $1,261)

Cost of Merchandise Sold Inventory

Date

2016

Purchases

*

CHAPTER 6 Inventories

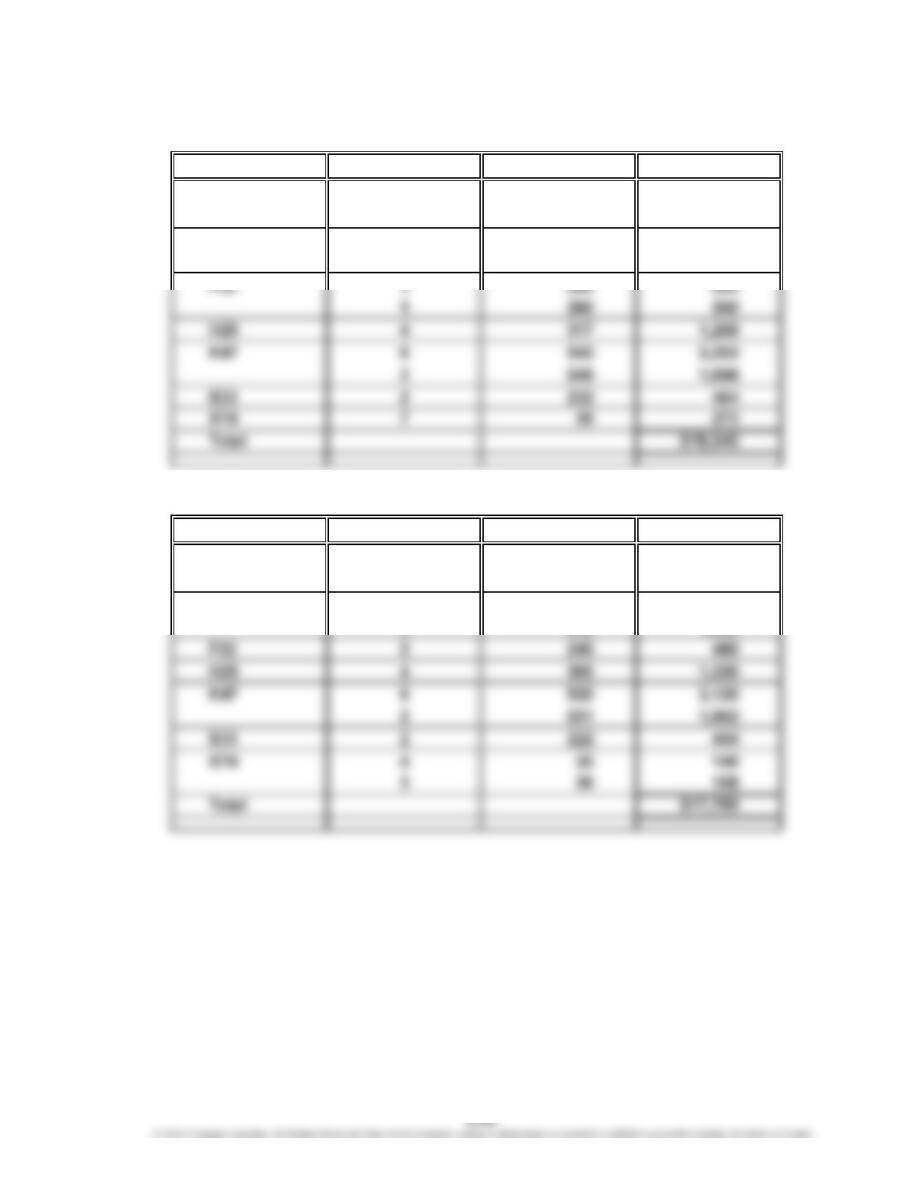

Prob. 6–4B

1. First-In, First-Out Method

Merchandise inventory, June 30, 2016…………………………………

…

$ 32,864

Cost of merchandise sold………………………………………..………

…

310,776

2. Last-In, First-Out Method

Merchandise inventory, June 30, 2016…………………………………

…

$ 31,240

Cost of merchandise sold…………………………………….…………

…

312,400

Supporting computations

…

…

…

CHAPTER 6 Inventories

Prob. 6–4B (Continued)

3. Weighted Average Cost Method

Merchandise inventory, June 30, 2016……………………

…

$ 32,500

Cost of merchandise sold……………………………………

…

311,140

Supporting computations

Weighted Average Unit Cost Units Available for Sale

Total Cost of Merchandise Available for Sale

=

…

CHAPTER 6 Inventories

Prob. 6–4B (Concluded)

4. Weighted

FIFO LIFO Average

CHAPTER 6 Inventories

Prob. 6–5B

1. First-In, First-Out Method

Model Quantity Unit Cost Total Cost

C55 3 $1,070 $ 3,210

1 1,060 1,060

D11 6 675 4,050

5 666 3,330

2. Last-In, First-Out Method

Model Quantity Unit Cost Total Cost

C55 3 $1,040 $ 3,120

1 1,054 1,054

D11 9 639 5,751

2 645 1,290

CHAPTER 6 Inventories

Prob. 6–5B (Concluded)

3. Weighted Average Cost Method

Quantity Unit Cost*Total Cost

4 $1,056 $ 4,224

11 654 7,194

2 252 504

4 311 1,244

*Computations of unit costs:

C55: $1,056 = [(3 × $1,040) + (3 × $1,054) + (3 × $1,060) + (3 × $1,070)] ÷ (3 + 3 + 3 + 3)

D11: $654 = [(9 × $639) + (7 × $645) + (6 × $666) + (6 × $675)] ÷ (9 + 7 + 6 + 6)

F32: $252 = [(5 × $240) + (3 × $260) + (1 × $260) + (1 × $280)] ÷ (5 + 3 + 1 + 1)

4. a. During periods of rising prices, the LIFO method will result in a lower cost

H29

Model

C55

D11

F32

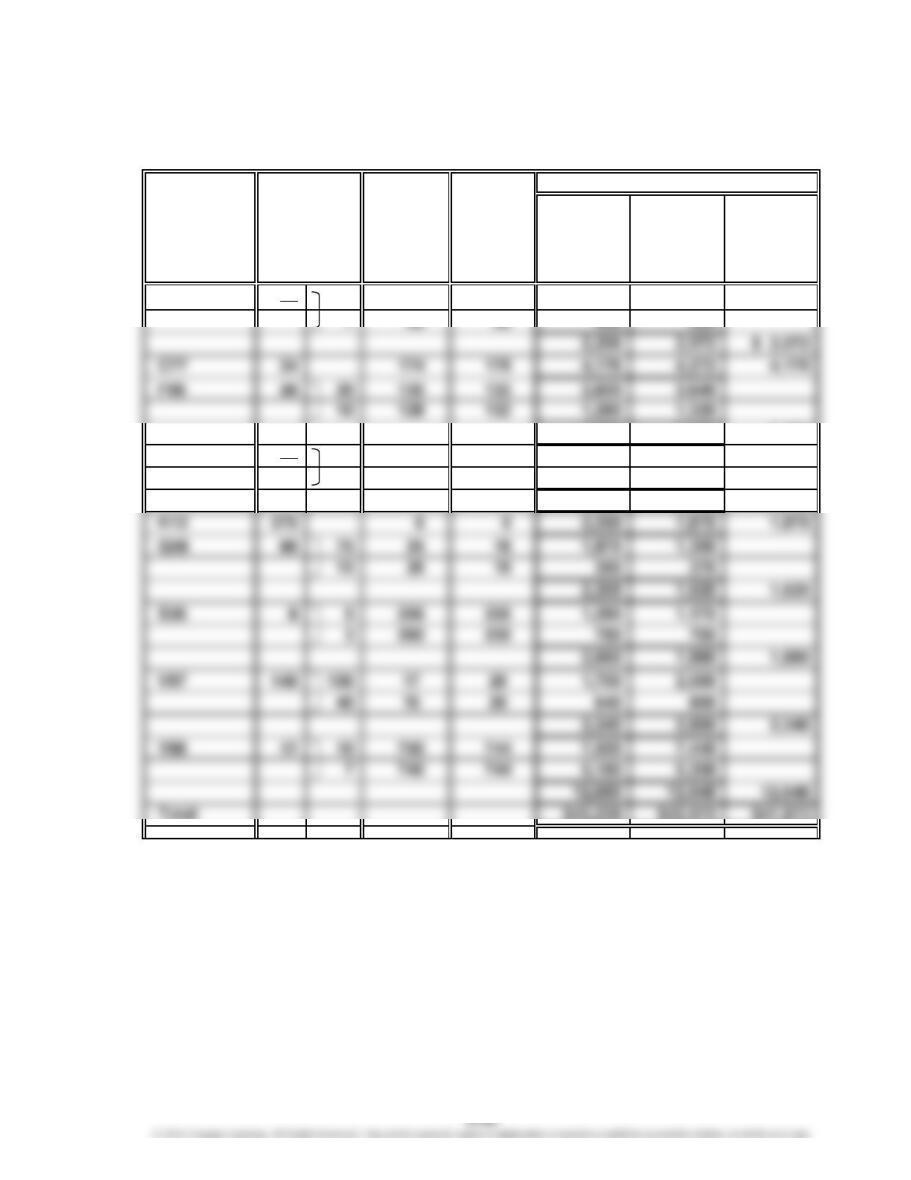

CHAPTER 6 Inventories

Prob. 6–6B

Market

Value per

Cost Unit (Net

per Realizable

Commodity Unit Value) Cost Market LCM

A54 37 30 $ 60 $ 56 $ 1,800 $ 1,680

3,880 3,960 3,880

H83 21 6 547 545 3,282 3,270

15 540 545 8,100 8,175

11,382 11,445 11,382

Quantity

Inventory Sheet

December 31, 2016

Inventory

Total

CHAPTER 6 Inventories

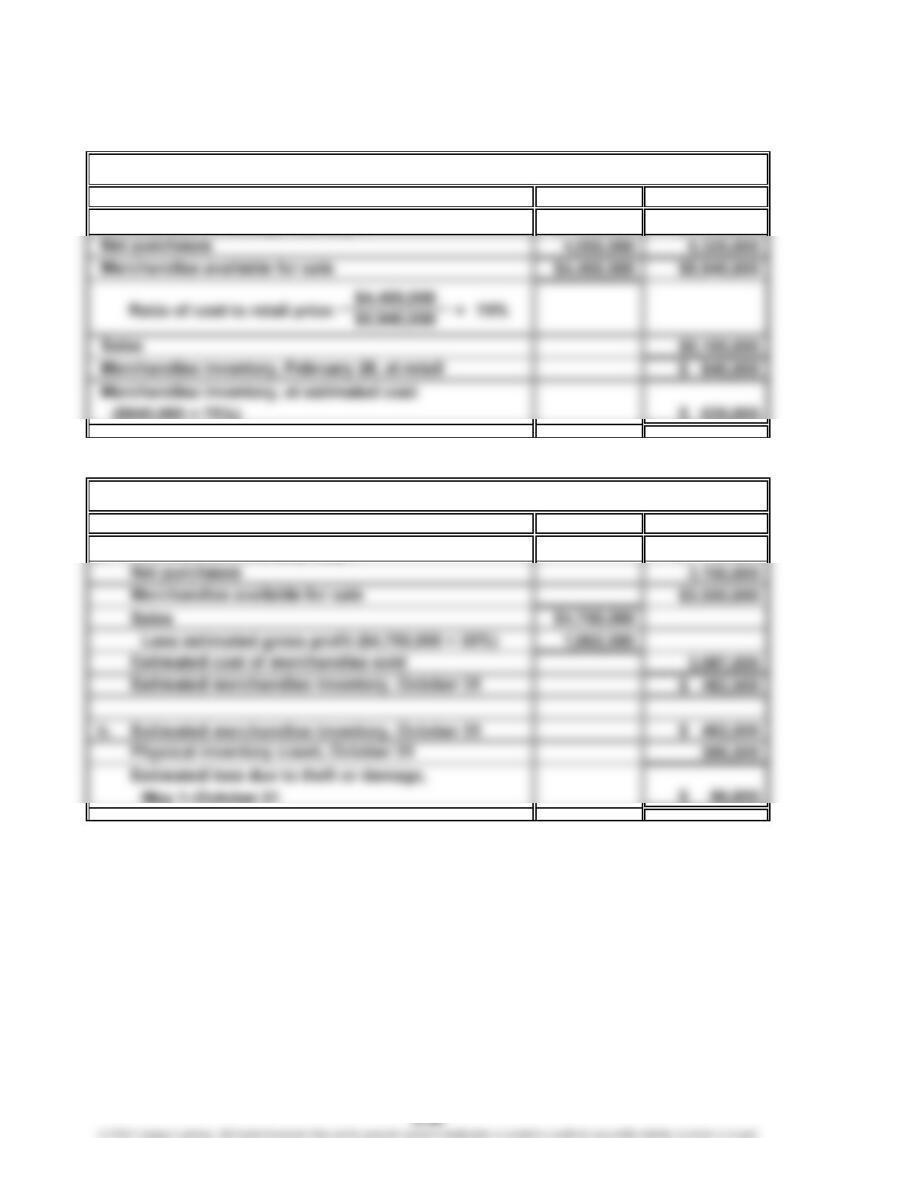

Prob. 6–7B

1.

Cost Retail

Merchandise inventory, February 1 $ 400,000 $ 615,000

2.

Cost

a. Merchandise inventory, May 1 $ 400,000

JAFFE CO.

CORONADO CO.

CHAPTER 6 Inventories

CP 6–1

Because the title to merchandise shipped FOB shipping point passes to the buyer whe

n

CP 6–2

In developing a response to Paula’s concerns, you should probably first emphasize

the practical need for an assumption concerning the flow of cost of goods purchased

and sold. That is, when identical goods are frequently purchased, it may not be

practical to specifically identify each item of inventory. If all the identical goods were

CASES & PROJECTS

CHAPTER 6 Inventories

CP 6–3

1. a. First-in, first-out method:

8,000 units at $48.00………………………………………………

…

$ 384,000

8,000 units at $44.85………………………………………………

…

358,800

12,800 units at $43.50………………………………………………

…

556,800

2. Weighted Average

FIFO LIFO Cost

Sales……………………………………… $10,000,000 $10,000,000 $10,000,000

3. a. The LIFO method is often viewed as the best basis for reflecting income

from operations. This is because the LIFO method matches the most current

cost of merchandise purchases against current sales. The matching of

current costs with current sales results in a gross profit amount that many

…

…

…

CHAPTER 6 Inventories

CP 6–3 (Continued)

While the LIFO method is often viewed as the best method for matching

revenues and expenses, the FIFO method is often consistent with the

physical movement of merchandise in a business because most businesses

tend to dispose of commodities in the order of their acquisition. To the extent

physical flow of goods concepts equally.

b. The FIFO method provides the best reflection of the replacement cost of the

ending inventory for the balance sheet. This is because the amount reported

on the balance sheet for merchandise inventory will be assigned costs from

the most recent purchases. For most businesses, these costs will reflect

CHAPTER 6 Inventories

CP 6–3 (Concluded)

d. The advantages of the perpetual inventory system include the following:

(1) A perpetual inventory system provides an effective means of control

(2) A perpetual inventory system provides an accurate method for

determining inventories used in the preparation of interim statements.

(3) A perpetual inventory system provides an aid for maintaining inventories

at optimum levels. Frequent review of the perpetual inventory records

helps management in the timely reordering of merchandise so that loss of

April 31,000 units 16,000 units 15,000 units 15,000 units 16,000 units

May 33,000 16,000 17,000 32,000 20,000

It appears that during April through July, the company ordered inventory

without regard to the accumulation of excess inventory. A perpetual

inventory system might have prevented this excess accumulation from

occurring.

Increase

Month Purchases

(Decrease) in

Sales Inventor

y

End of Month Sales

Inventory at Next Month’s

CHAPTER 6 Inventories

CP 6–4

Cost of Goods Sold

Average Inventory

Dell

$48,260 $48,260

($1,301 + $1,404) ÷ 2 $1,352.5

b. Dell builds its computers primarily to a customer order, called a build-to-order

strategy. Customers place their orders on the Internet. Dell then builds and

a.

35.7Inventory Turnover = = =

=

Inventory Turnover

CHAPTER 6 Inventories

CP 6–5

Inventory

Turnover

0.81

8.34

Computations:

Tiffany Co.

Cost of Goods Sold

Average Inventory

Amazon.com

Cost of Goods Sold

Average Inventory

$45,971

($4,992 + $6,031) ÷ 2

= = 8.34

Inventory Turnover

a. Number of Days’

Sales in Inventory

=Inventory Turnover

Tiffany Co. 452.34

43.76

Amazon.com

=

CHAPTER 6 Inventories

CP 6–6

a. Costco Walmart JCPenney

1. Cost of merchandise sold………………

…

$86,823 $335,127 $11,042

Merchandise inventory, beginning……

…

$ 6,638 $ 36,437 $ 3,213

2. Average merchandise inventory

1. Average merchandise inventory

[from part (a)]…………………………… $6,867.0 $38,575.5 $3,064.5

…

sold (COMS ÷ 365)……………………

…

$ 237.9 $ 918.2 $ 30.3

Number of day’s sales in inventory…

…

28.9 42.0 101.3

c. Both the inventory turnover ratio and the number of day’s sales in inventory

reflect the merchandising approaches of the three companies.

Costco is a club warehouse. Its approach is to hold only mass appeal items that

are sold quickly off the shelf. Most items are sold in bulk quantities at very