CHAPTER 6

SOLUTIONS TO PROBLEMS: SET B

PROBLEM 6-1B

(a) The goods should not be included in inventory as they were shipped

FOB shipping point and shipped February 26. Title to the goods

transfers to the customer February 26. Weber should have recorded

the transaction in the Sales and Accounts Receivable accounts.

(b) The amount should not be included in inventory as they were shipped

FOB destination and not received until March 2. The seller still owns

the inventory. No entry is recorded.

(c) Include $500 in inventory.

(d) Include $400 in inventory.

PROBLEM 6-2B

(a)

COST OF GOODS AVAILABLE FOR SALE

Date

Explanation

Units

Unit Cost

Total Cost

March 1

Beginning Inventory

1,500

$ 7

$ 10,500

5

Purchase

3,000

8

24,000

Purchase

4,500

Purchase

4,000

40,000

Purchase

Total

$142,500

(b)

FIFO

(1)

Ending Inventory

(2)

Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

Cost of goods

available for sale

$142,500

March 26

$11

$27,500

inventory

37,500

1,000

$37,500

Cost of goods sold

$105,000

Proof of Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

March 1

1,500

$ 7

$ 10,500

5

8

4,500

9

PROBLEM 6-2B (Continued)

LIFO

(1)

Ending Inventory

(2)

Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

Cost of goods

available for sale

$142,500

March 1

1,500

$10,500

inventory

26,500

5

2,000

8

3,500

$26,500

Cost of goods sold

$116,000

Proof of Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

March 26

2,500

$11

$27,500

4,000

4,500

5

8

12,000

AVERAGE-COST

(1)

Ending Inventory

(2)

Cost of Goods Sold

$142,500 ÷ 15,500 = $9.194

Cost of goods

available for sale

Cost

inventory

Cost of goods sold

(c) (1) As shown in (b) above, FIFO produces the highest inventory amount,

$37,500.

PROBLEM 6-3B

(a)

COST OF GOODS AVAILABLE FOR SALE

Date

Explanation

Units

Unit Cost

Total Cost

1/1

Beginning Inventory

400

$ 8

$ 3,200

2/20

Purchase

5/5

Purchase

8/12

Purchase

12/8

Purchase

Total

$19,300

(b)

FIFO

(1)

Ending Inventory

(2)

Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

Cost of goods

available for sale

$19,300

12/8

$12

$2,400

Less: Ending

inventory

5,700

8/12

$5,700

Cost of goods sold

$13,600

Proof of Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

1/1

$ 8

2/20

9

5/5

500

5,000

1,500

PROBLEM 6-3B (Continued)

(b)

LIFO

(1)

Ending Inventory

(2)

Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

Cost of goods

available for sale

$19,300

1/1

400

$8

$3,200

inventory

4,100

2/20

100

9

500

$4,100

Cost of goods sold

Less: Ending

Proof of Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

12/8

200

$12

$ 2,400

8/12

300

5/5

500

10

2/20

500

1,500

$15,200

AVERAGE-COST

(1)

Ending Inventory

(2)

Cost of Goods Sold

$19,300 ÷ 2,000 = $9.65

Cost of goods

available for sale

$19,300

Units

inventory

Cost of goods sold

(c) (1) LIFO results in the lowest inventory amount for the balance sheet,

$4,100.

PROBLEM 6-4B

(a) Patel CO.

Condensed Income Statement

For the Year Ended December 31, 2017

FIFO

LIFO

Sales revenue ……………………………………… $865,000 $865,000

Cost of goods sold

Beginning inventory ……………………… 32,000 32,000

Cost of goods sold ……………………….. 553,600 568,800

Gross profit ………………………………………… 311,400 296,200

(b) (1) The FIFO method produces the most meaningful inventory amount

for the balance sheet because the units are costed at the most

recent purchase prices.

(2) The LIFO method produces the most meaningful net income because

the costs of the most recent purchases are matched against sales.

PROBLEM 6-5B

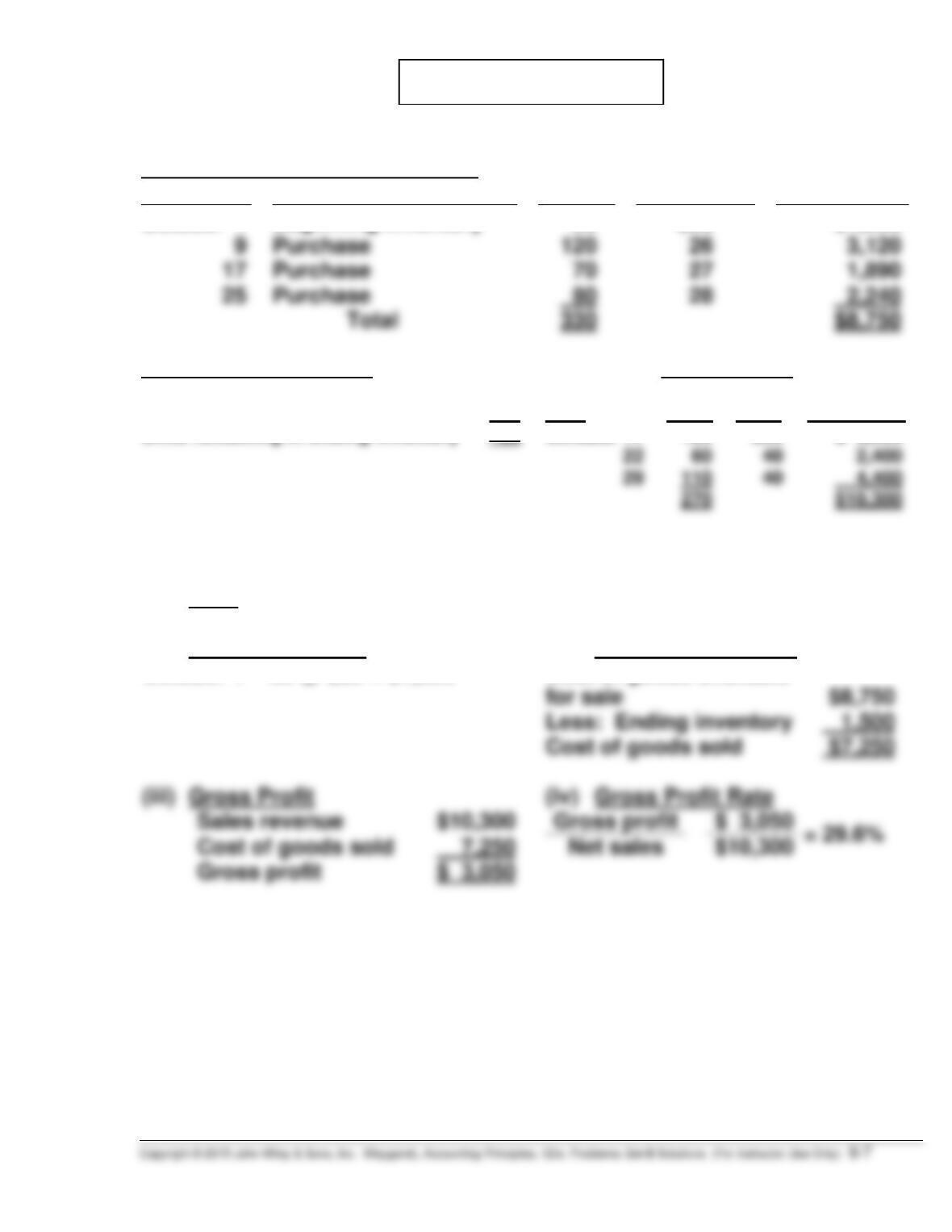

Cost of Goods Available for Sale

Date

Explanation

Units

Unit Cost

Total Cost

October 1

Beginning Inventory

60

$25

$1,500

9

Purchase

120

26

3,120

Purchase

70

Purchase

28

330

Ending Inventory in Units:

Sales Revenue

Units available for sale

330

Unit

Sales (100 + 60 + 110)

270

Date

Units

Price

Total Sales

Units remaining in ending inventory

60

October 11

100

$35

$ 3,500

2,400

110

270

(a)

(1)

LIFO

(i)

Ending Inventory

(ii)

Cost of Goods Sold

October 1

60 @ $25 = $1,500

Cost of goods available

for sale

$8,750

Less: Ending inventory

1,500

Cost of goods sold

(iii)

Gross Profit

(iv)

Gross Profit Rate

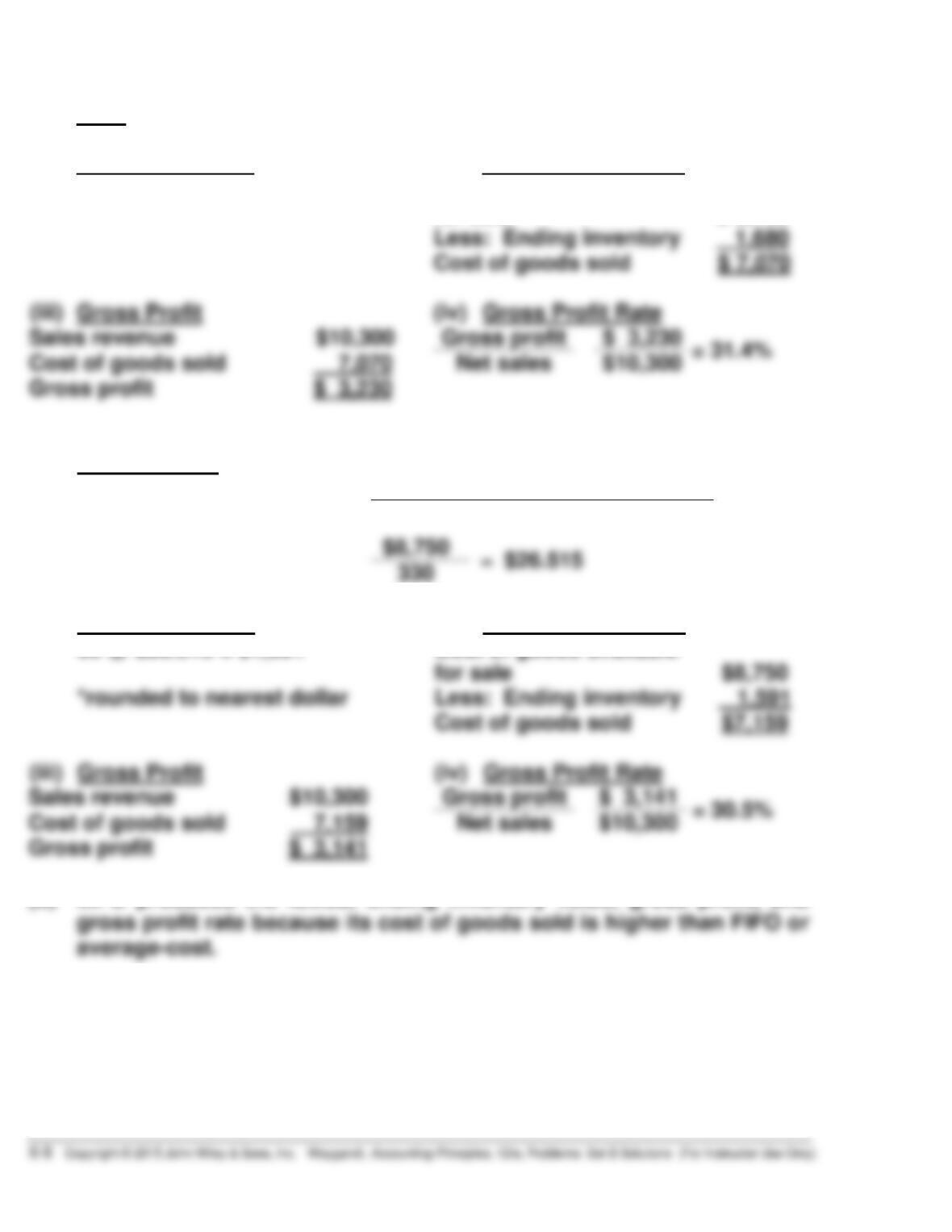

PROBLEM 6-5B (Continued)

(2)

FIFO

(i)

Ending Inventory

(ii)

Cost of Goods Sold

October 25

60 @ $28 = $1,680

Cost of goods available

for sale

$ 8,750

Less: Ending inventory

Cost of goods sold

(iii)

Gross Profit

(iv)

Gross Profit Rate

Sales revenue

$10,300

Cost of goods sold

Gross profit

$ 3,230

(3)

Average-Cost

Weighted-average cost per unit:

cost of goods available for sale

units available for sale

330

(i)

Ending Inventory

(ii)

Cost of Goods Sold

for sale

*rounded to nearest dollar

Less: Ending inventory

Cost of goods sold

(iii)

Gross Profit

(iv)

Gross Profit Rate

Sales revenue

Cost of goods sold

$10,300

Gross profit

60 @ $26.515 = $1,591*

Cost of goods available

(b) LIFO produces the lowest ending inventory value, gross profit, and

gross profit rate because its cost of goods sold is higher than FIFO or

average-cost.

PROBLEM 6-6B

(a) (1) To maximize gross profit, Princess Diamonds should sell the

diamonds with the lowest cost.

Sale Date

Cost of Goods Sold

Sales Revenue

March 5

150 @ $300

$ 45,000

180 @ $600

$108,000

March 25

170 @ $360

$204,400

580

$368,000

(2) To minimize gross profit, Princess Diamonds should sell the diamonds

with the highest cost.

Sale Date

Cost of Goods Sold

Sales Revenue

March 5

180 @ $360

$ 64,800

180 @ $600

$108,000

March 25

350 @ $380

400 @ $650

9,000

$214,000

580

$368,000

(b) FIFO

Cost of goods available for sale

March 1

Beginning inventory

150 @ $300

$ 45,000

3

Purchase

200 @ $360

72,000

Ending inventory

PROBLEM 6-6B (Continued)

Goods available for sale

$250,000

Cost of goods sold

$204,400

(c) LIFO

Cost of goods available for sale

$250,000

(from part b)

Cost of goods sold

$214,000

(d) The choice of inventory method depends on the company’s objectives.

Since the diamonds are marked and coded, the company could use specific

identification. This could, however, result in “earnings management” by

PROBLEM 6-7B

(a) Chelsea INC.

Condensed Income Statement

For the Year Ended December 31, 2017

FIFO

LIFO

Sales revenue ……………………………………. $665,000 $665,000

Cost of goods sold

Beginning inventory……………………… 35,000 35,000

Cost of goods purchased ……………… 504,500 504,500

Cost of goods available for sale ……. 539,500 539,500

Ending inventory ………………………….. 133,500a 115,000b

(b) Answers to questions:

(1) The FIFO method produces the most meaningful inventory amount

for the balance sheet because the units are costed at the most

recent purchase prices.

6-12 Copyright © 2015 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 12/e, Problems: Set B Solutions (For Instructor Use Only)

PROBLEM 6-7B (Continued)

(5) The illusionary gross profit is $18,500 or ($259,000 – $240,500). Under

LIFO, Chelsea Inc. has recovered the current replacement cost of

the units ($424,500), whereas under FIFO, it has only recovered

the earlier costs ($406,000). This means that under FIFO the

company must reinvest $18,500 of the gross profit to replace the

units used.

Answer in business letter form:

Dear Chelsea Inc.

The LIFO method produces the most meaningful net income because

the costs of the most recent purchases are matched against sales.

There will be $5,180 additional cash available under LIFO because

income taxes are $30,940 under LIFO and $36,120 under FIFO.

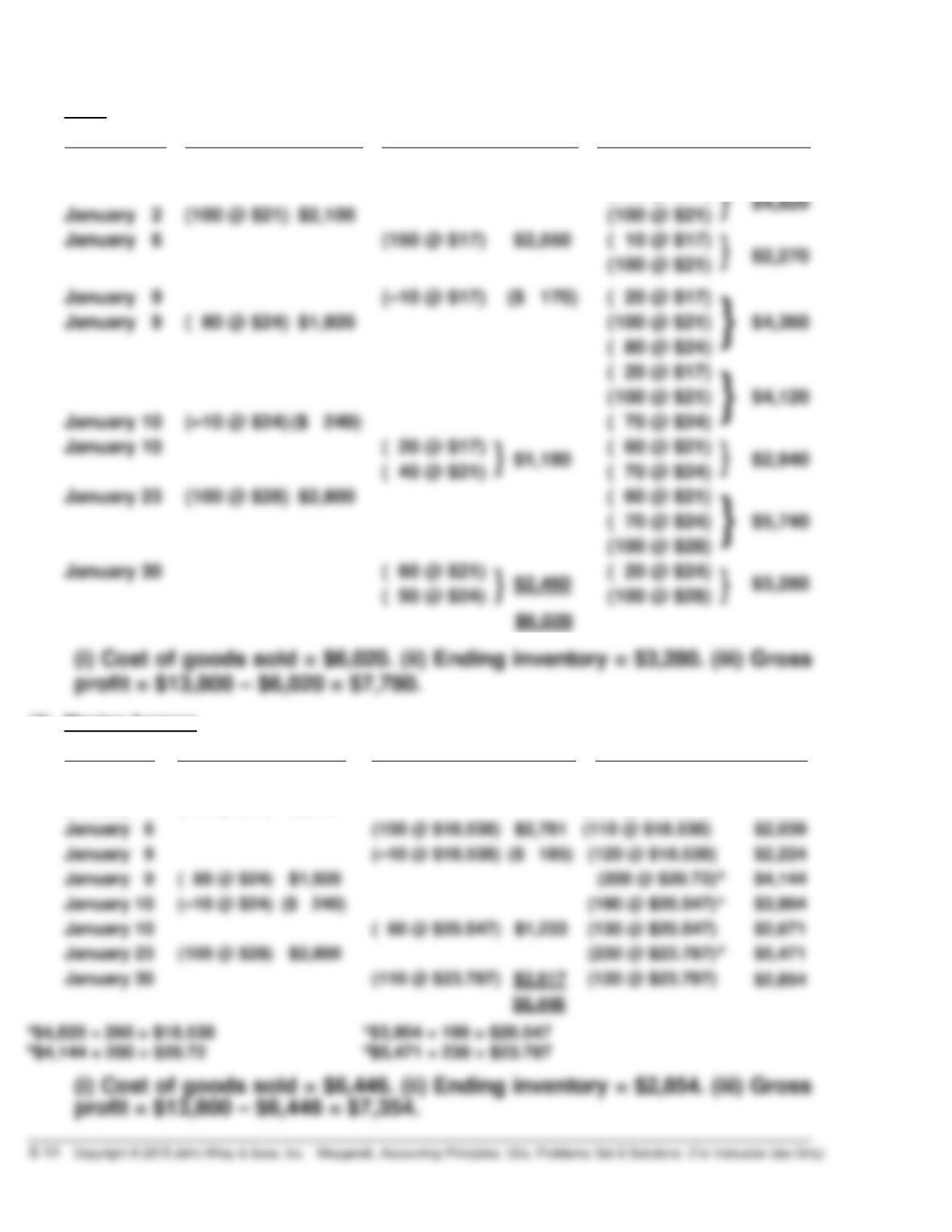

*PROBLEM 6-8B

(a)

Sales:

Date

January 6

150 units @ $40

$ 6,000

January 9 (return)

(10 units @ $40)

(400)

January 30

110 units @ $50

5,500

(1)

LIFO

Date

Purchases

Cost of Goods Sold

Balance

January 1

(160 @ $17)

$2,720

(160 @ $17)

January 2

(100 @ $21) $2,100

(100 @ $21)

January 6

(100 @ $21)

(110 @ $17)

$1,870

( 50 @ $17)

January 9

( 80 @ $24) $1,920

(120 @ $17)

}

$3,960

( 80 @ $24)

January 10

(120 @ $17)

}

$3,720

( 70 @ $24)

January 10

( 60 @ $24) $1,440

(120 @ $17)

}

$2,280

( 10 @ $24)

January 23

(100 @ $28) $2,800

(120 @ $17)

( 10 @ $24)

$5,080

(100 @ $28)

January 30

(100 @ $28)

(120 @ $17)

$2,040

( 10 @ $24)

*PROBLEM 6-8B (Continued)

(2)

FIFO

Date

Purchases

Cost of Goods Sold

Balance

January 1

(160 @ $17)

$2,720

(160 @ $17)

}

$4,820

January 2

(100 @ $21) $2,100

(100 @ $21)

January 6

(150 @ $17)

January 9

(–10 @ $17)

($ 170)

( 20 @ $17)

}

$4,360

January 9

( 80 @ $24) $1,920

(100 @ $21)

( 80 @ $24)

( 20 @ $17)

}

$4,120

(100 @ $21)

January 10

(–10 @ $24) ($ 240)

( 70 @ $24)

January 10

( 20 @ $17)

( 60 @ $21)

$2,940

( 40 @ $21)

( 70 @ $24)

January 23

(100 @ $28) $2,800

( 60 @ $21)

}

$5,740

( 70 @ $24)

(100 @ $28)

January 30

( 60 @ $21)

( 20 @ $24)

$3,280

( 50 @ $24)

(100 @ $28)

(3)

Moving-Average

Date

Purchases

Cost of goods sold

Balance

January 1

(160 @ $17)

$2,720

January 2

(100 @ $21) $2,100

(260 @ $18.538)a

$4,820

January 6

(150 @ $18.538)

$2,781

(110 @ $18.538)

$2,039

January 9

(120 @ $18.538)

$2,224

January 9

( 80 @ $24) $1,920

$4,144

January 10

(190 @ $20.547)

c

$3,904

January 10

( 60 @ $20.547)

$1,233

(130 @ $20.547)

$2,671

January 23

(100 @ $28) $2,800

(230 @ $23.787)

$5,471

January 30

(110 @ $23.787)

$2,617

(120 @ $23.787)

$2,854

$6,446

*PROBLEM 6-8B (Continued)

(b)

Gross profit:

LIFO

FIFO

Moving-Average

Sales

$13,800

$13,800

$13,800

Cost of goods sold

Gross profit

Ending inventory

In a period of rising costs, the LIFO cost flow assumption results in the

highest cost of goods sold and lowest gross profit. FIFO gives the

lowest cost of goods sold and highest gross profit. The moving

average cost flow assumption results in amounts between the other two.

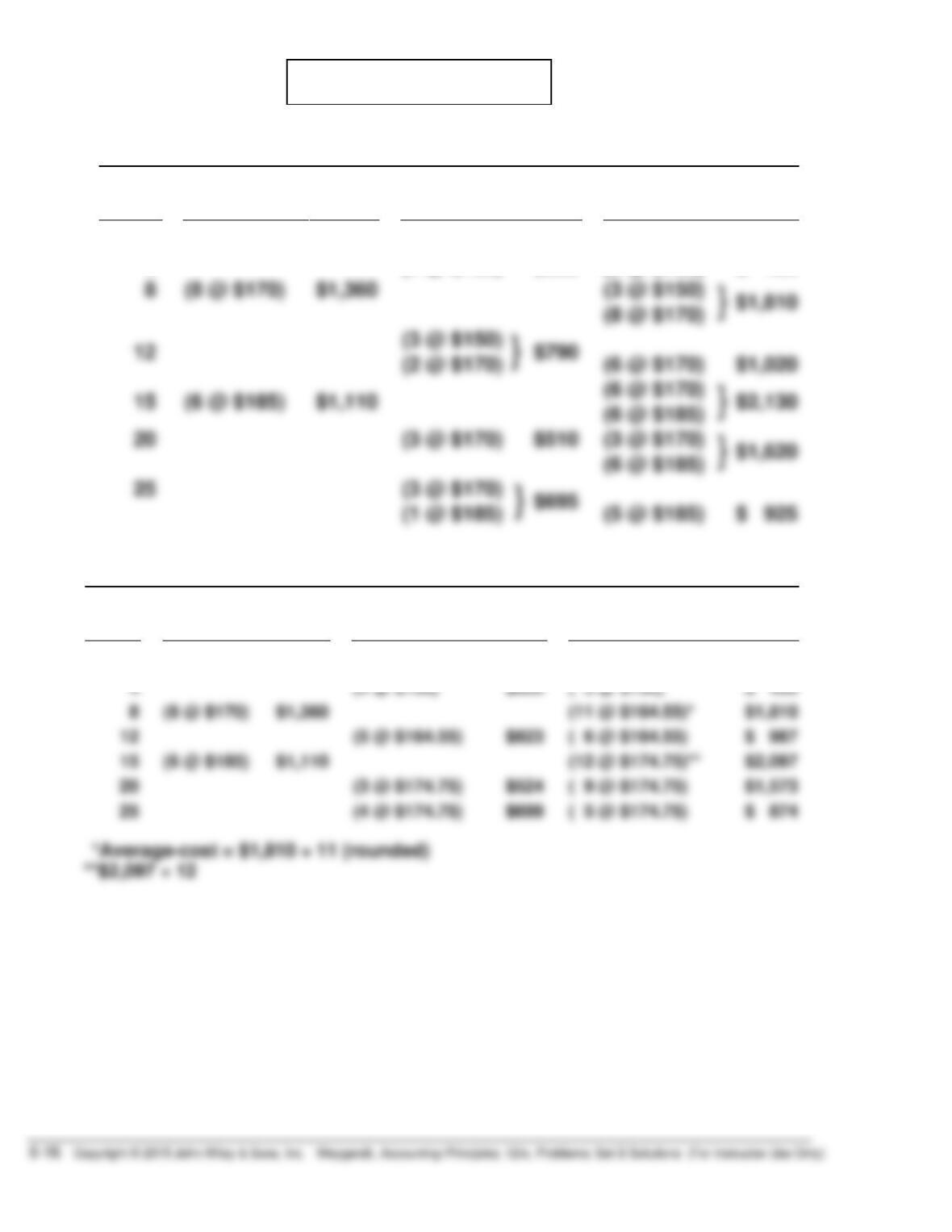

*PROBLEM 6-9B

(a)

(1)

FIFO

Date

Purchases

Cost of

Goods Sold

Balance

May 1

(7 @ $150)

$1,050

(7 @ $150)

$1,050

(4 @ $150)

(3 @ $150)

}

$1,810

(8 @ $170)

12

(3 @ $150)

15

(6 @ $185)

$1,110

(6 @ $170)

}

$2,130

(6 @ $185)

}

$1,620

(6 @ $185)

(3 @ $170)

(2)

MOVING-AVERAGE COST

Date

Purchases

Cost of

Goods Sold

Balance

May 1

(7 @ $150)

$1,050

( 7 @ $150)

$1,050

4

(4 @ $150)

$600

( 3 @ $150)

$ 450

(8 @ $170)

$1,360

(11 @ $164.55)*

$1,810

(5 @ $164.55)

( 6 @ $164.55)

$ 987

(6 @ $185)

$1,110

(12 @ $174.75)**

$2,097

(3 @ $174.75)

( 9 @ $174.75)

$1,573

(4 @ $174.75)

( 5 @ $174.75)

$ 874

*PROBLEM 6-9B (Continued)

(3)

LIFO

Date

Purchases

Cost of

Goods Sold

Balance

May 1

(7 @ $150)

$1,050

(7 @ $150)

$1,050

4

(4 @ $150)

$600

(3 @ $150)

$ 450

8

(8 @ $170)

$1,360

(3 @ $150)

(8 @ $170)

12

(5 @ $170)

(3 @ $150)

(3 @ $170)

15

(6 @ $185)

$1,110

(3 @ $150)

}

$2,070

(3 @ $170)

(6 @ $185)

20

(3 @ $185)

(3 @ $150)

(3 @ $170)

(3 @ $185)

25

(3 @ $185)

(3 @ $150)

(1 @ $170)

(2 @ $170)

(b) (1) The highest ending inventory is $925 under the FIFO method.

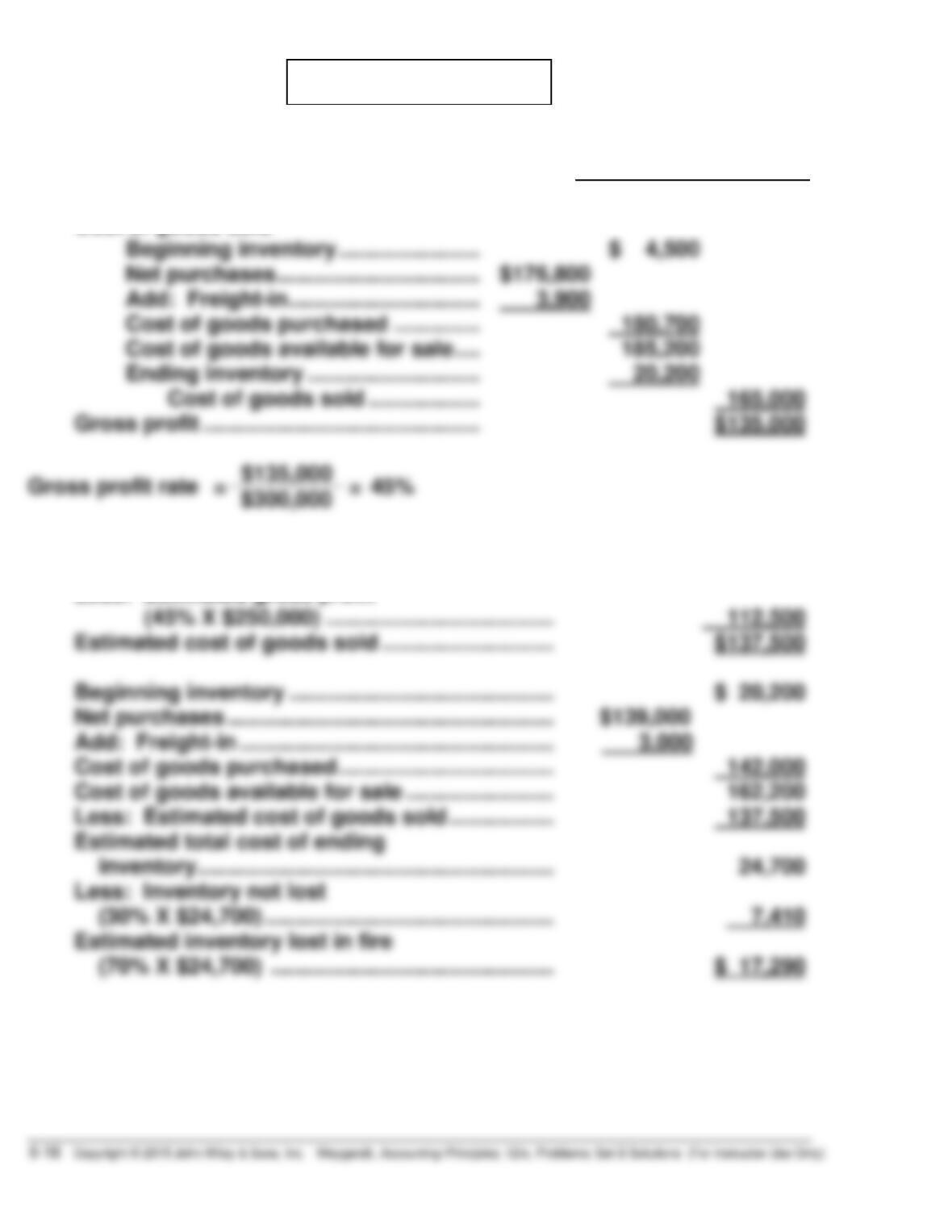

*PROBLEM 6-10B

(a)

February

Net sales ………………………………………….. $300,000

Cost of goods sold

Beginning inventory ………………….. $ 4,500

(b) Net sales …………………………………………………….. $250,000

Less: Estimated gross profit

(45% X $250,000) ………………………………. 112,500

Estimated cost of goods sold ………………………. $137,500

Beginning inventory ……………………………………. $ 20,200

Net purchases …………………………………………….. $139,000

*PROBLEM 6-11B

(a)

Sporting

Goods

Jewelry

and Cosmetics

Cost

Retail

Cost

Retail

Beginning inventory $ 47,360 $ 74,000 $ 39,440 $ 62,000

Cost-to-retail ratio:

Sporting Goods—$693,000 ÷ $1,100,000 = 63%.

Estimated ending inventory at cost: