SOLUTION

Chapter 6 Waterways Continuing Problem

WCP6

Part 1

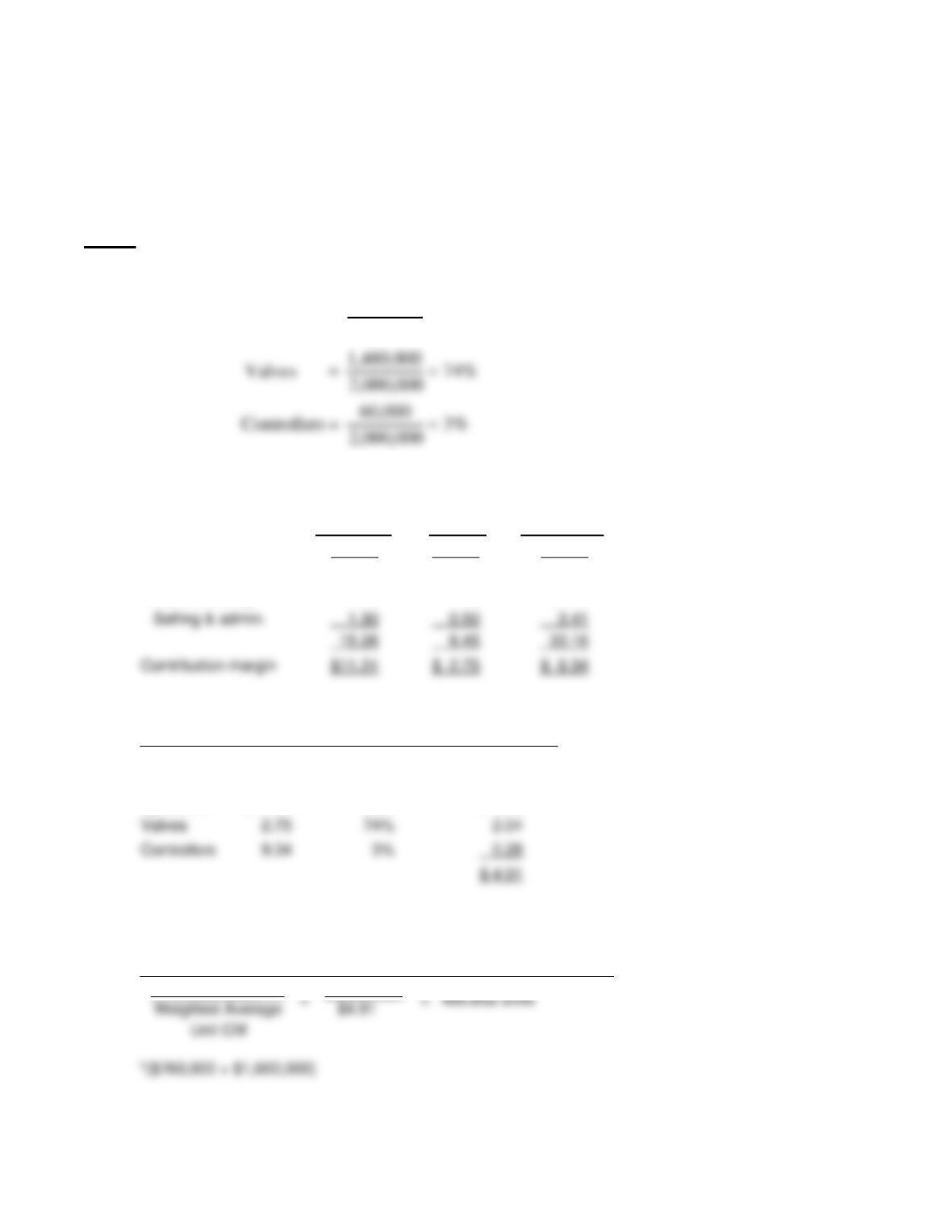

(a) Total units = 460,000 + 1,480,000 + 60,000 = 2,000,000

Sales mix

(b)

Sprinklers

Valves

Controllers

Sales price

$26.50

$11.20

$42.50

Variable costs

Manufacturing

13.96

7.95

29.75

8.45

Contribution margin

$11.24

$ 2.75

$ 9.34

Weighted-Average Unit Contribution Margin

Weighted-Avg

Unit CM X

Sales Mix % =

Unit CM

Sprinklers

$11.24

23%

$ 2.59

Valves

74%

Controllers

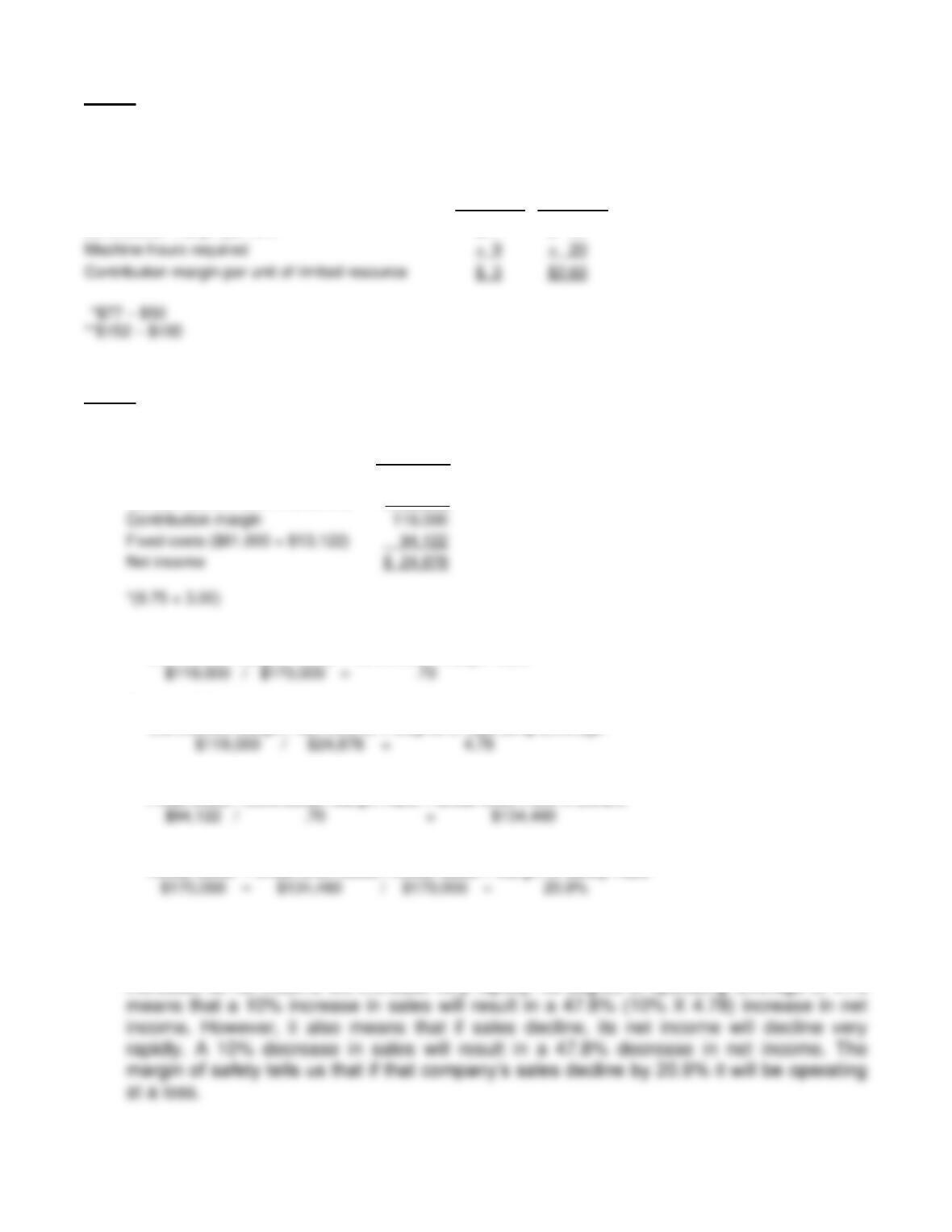

(c)

Break-even Point in Units

Fixed Costs

$2,360,000*

Sprinklers = 460,000

2,000,000 =23%

Part 2

The small set is the best use of a limited resource as it produces a higher contribution margin

per machine hour.

Small Set

Large Set

Contribution margin per unit

$27*

$ 52**

Part 3

(a)

February

Sales (4,000 X $42.50) $170,000

Variable costs (4,000 X $12.75*) 51,000*

Contribution Margin Ratio

Contribution Margin / Sales = Contribution Margin Ratio

Degree of Operating Leverage

Contribution Margin / Net Income = Degree of Operating Leverage

Break-even Point in Dollars

Fixed Costs / Contribution Margin Ratio = Break-even Point in Dollars

Margin of Safety Ratio

Actual Sales – Break-even Sales / Actual Sales = Margin of Safety Ratio

(b) Waterways has high fixed costs relative to its variable costs. This results in a high degree of

operating leverage. As a consequence, if the market is good and the company’s sales

increase, its net income will increase very rapidly. Its degree of operating leverage of 4.78

Machine hours required