Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

6-1

Chapter 6

Inventories and Cost of Sales

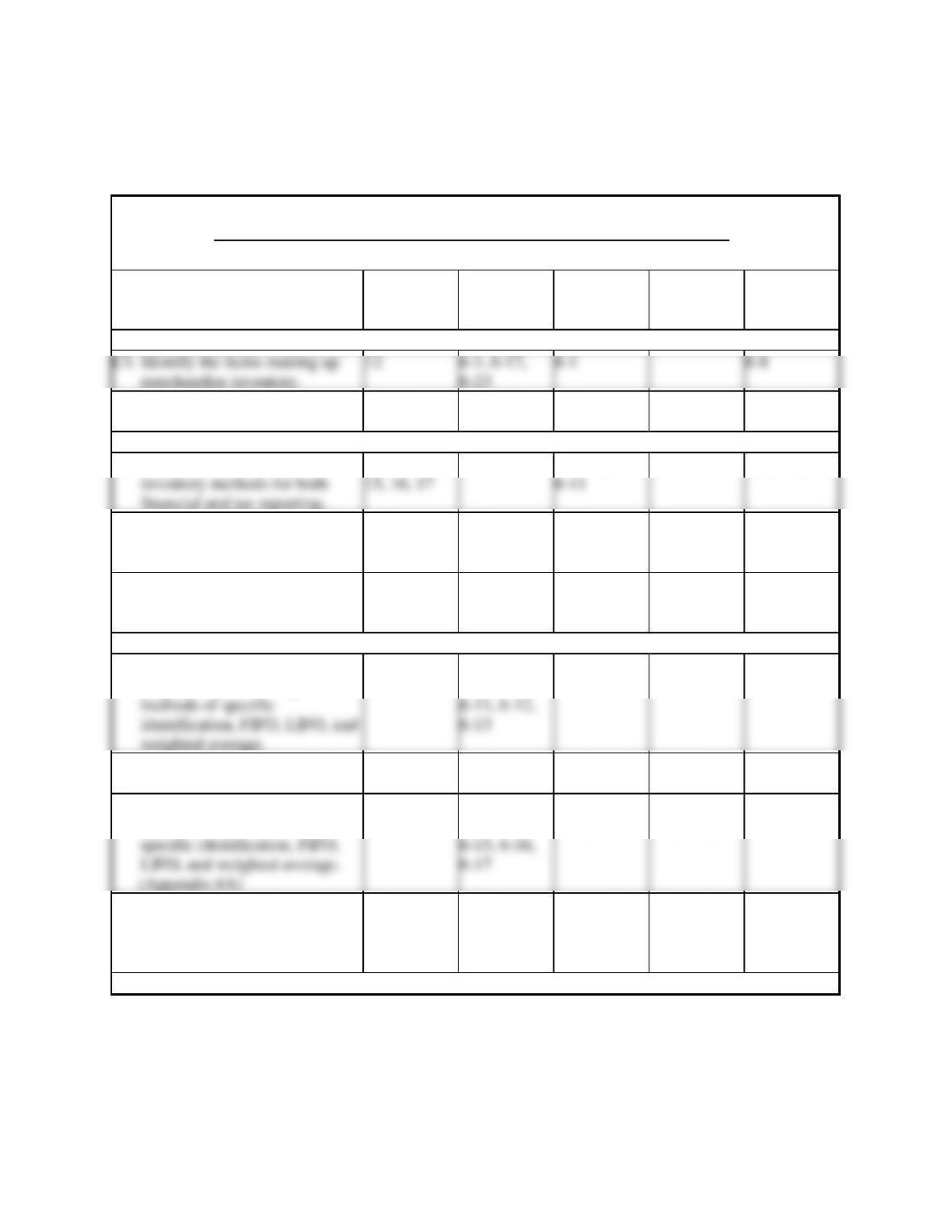

Student Learning Objectives and Related Assignment Materials*

Student Learning Objectives

Discussion

Questions

Quick

Studies

Exercises

Problems

(A &B set)**

Beyond the

Numbers

Conceptual objectives:

C2. Identify the costs of

merchandise inventory.

1, 2, 3

6-2, 6-23

6-2

6-1, 6-8

Analytical objectives:

inventory methods for both

financial and tax reporting.

A1. Analyze the effects of

4, 5, 6, 7, 14,

6-18

6-4, 6-6,

6-8

6-3, 6-4, 6-6

A2. Analyze the effects of

inventory errors on current and

future financial statements.

8, 9

6-20

6-12

6-6

A3. Assess inventory management

using both inventory turnover

and days’ sales in inventory.

6-21

6-11, 6-13

SP

6-1, 6-2, 6-5,

6-7, 6-9

Procedural objectives:

methods of specific

identification, FIFO, LIFO, and

weighted average.

6-11, 6-12,

6-13

P1. Compute inventory in a

perpetual system using the

1

6-3, 6-4, 6-5,

6-6, 6-10,

6-3, 6-7, 6-8

6-1, 6-3

6-6

P2. Compute the lower of cost or

market amount of inventory.

10, 11

6-19, 6-23

6-10, 6-18

6-5, SP

LIFO, and weighted average.

6-17

P3. Compute inventory in a periodic

system using the methods of

1, 13

6-7, 6-8,

6-9, 6-14,

6-5, 6-9,

6-14, 6-15

6-2, 6-4,

6-7, 6-8, ES

P4. Apply both the retail inventory

and gross profit methods to

estimate inventory.

(Appendix 6B)

13

6-22

6-16, 6-17

6-9, 6-10

Notes appear on next page.

*See additional information on next page that pertains to these quick studies, exercises and problems.

SP refers to the Serial Problem

GL refers to the General Ledger problems

ES refers to Excel Simulations

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

6-2

Additional Information on Related Assignment Material

Connect

Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all Exercises

and Problems Set A. Connect also provides algorithmic versions for Quick Study, Exercises and

Problems. It allows instructors to monitor, promote, and assess student learning. It can be used in

practice, homework, or exam mode.

Connect Insight

The first and only analytics tool of its kind, Connect Insight is a series of visual data displays that are each framed

The Serial Problem (SP) for Success Systems continues in this chapter.

General Ledger

Assignable within Connect, General Ledger (GL) problems offer students the ability to see how transactions post

Excel Simulations

Assignable within Connect, Excel Simulations allow students to practice their Excel skills—such as basic formulas

Synopsis of Chapter Revisions

NEW opener—Homegrown Sustainable Sandwich and entrepreneurial assignment.

Simplified “specific identification” calculations in Exhibit 6.4.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

6-3

Chapter Outline

Notes

I. Inventory Basics

A. Determining Inventory Items

Merchandise inventory includes all goods that a company owns and

holds for sale. The following inventory items require special

attention:

1. Goods in Transit – if ownership has passed to the purchaser, the

goods are included in the purchaser’s inventory. Ownership is

2. Goods on Consignment—goods shipped by the owner, called the

consignor, to another party, the consignee.

3. Goods Damaged or Obsolete

a. Damaged and obsolete (and deteriorated) goods are not

reported in inventory if they cannot be sold.

B. Determining Inventory Costs

1. The cost of an inventory item includes its invoice cost minus any

2. The expense recognition or matching principle states that

C. Internal Controls and Taking a Physical Count

2. Nearly all companies take a physical count of inventory at least

3. Internal controls when taking a physical count of inventory:

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

accounted for.

b. Those responsible for the inventory do not count the

inventory.

II. Inventory Costing under a Perpetual System

The major goal is to properly assign costs with sales. The expense

recognition (or matching principle) is used to compute how much of

the cost of goods available for sale is expensed (on the income

statement) and how much is carried forward as inventory (on the

balance sheet). One of the most important issues in accounting for

inventory is determining the per unit cost assigned to inventory items.

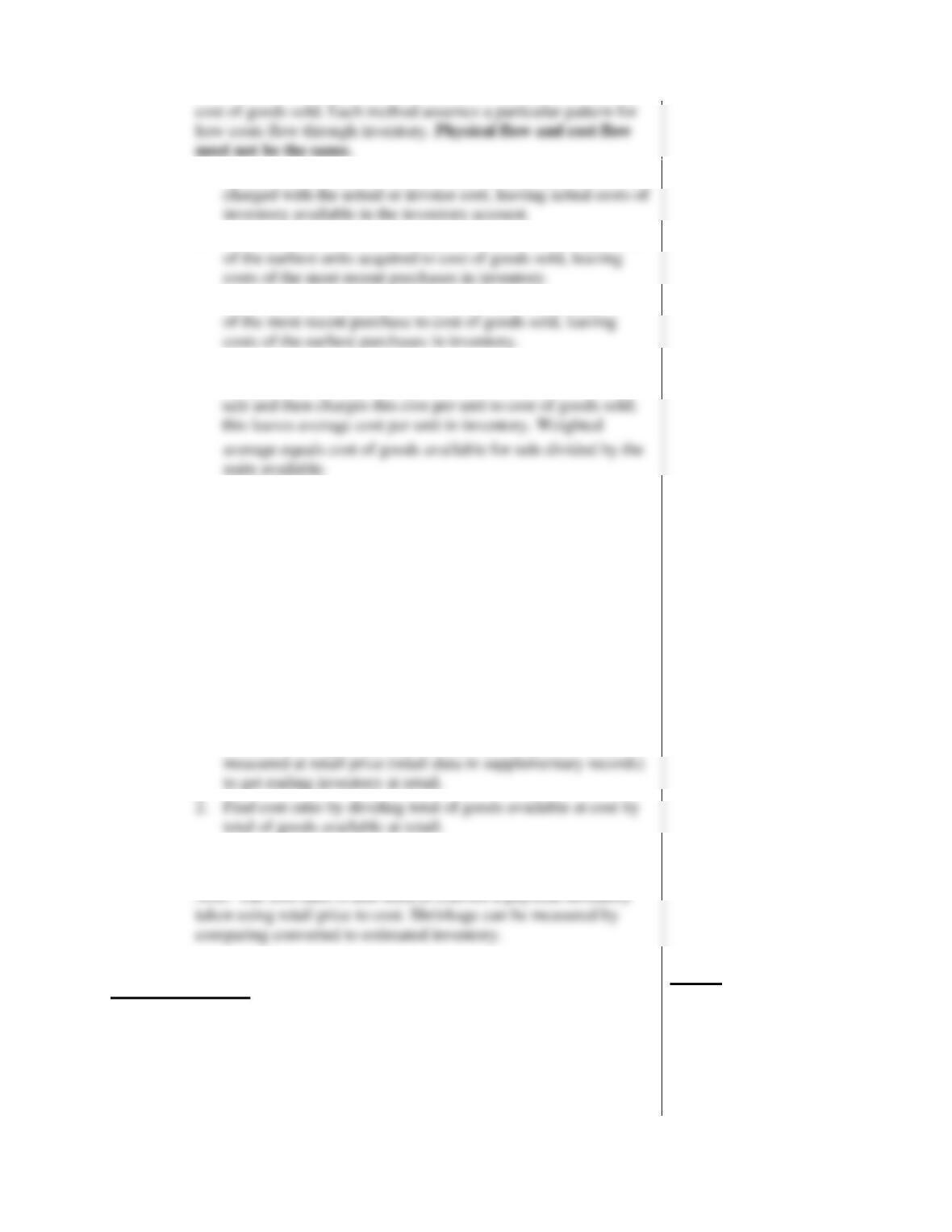

A. Inventory Cost Flow Assumptions

Four methods are used to assign costs to inventory and cost of

goods sold. Each method assumes a particular pattern for how

costs flow through inventory. Physical flow and cost flow need

not be the same.

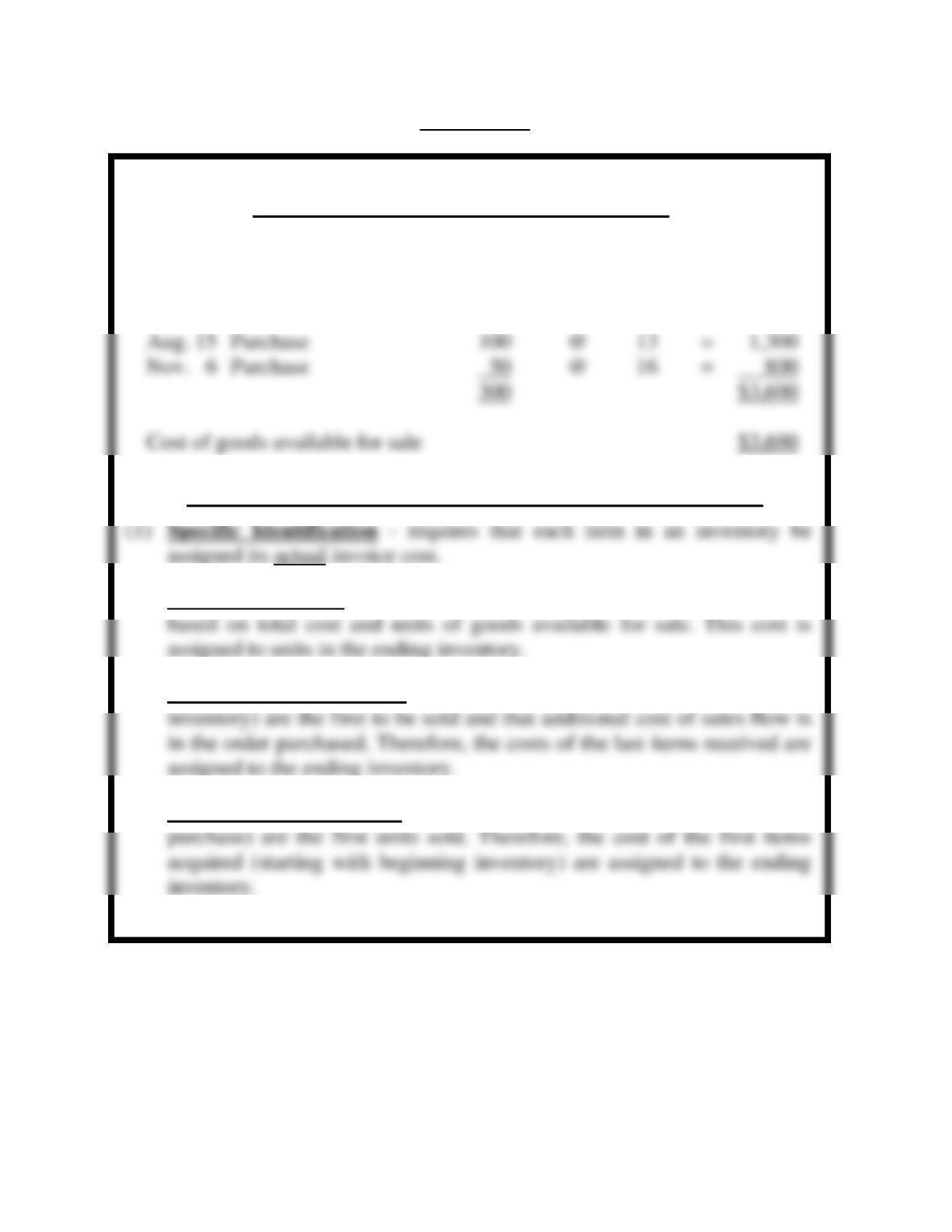

1. First-in, first-out (FIFO)—assumes costs flow in the order

2. Last-in, first-out (LIFO)—assumes costs flow in the reverse

order incurred. (Results differ from perpetual in the appendix

3. Weighted average—assumes costs flow in an average of the

costs available. (Results differ from perpetual in the appendix

4. Specific identification—each item can be identified with a

specific purchase and invoice. Specific identification is

usually only practical for companies with expensive, custom-

Chapter Outline

Notes

B. Inventory Costing Illustration

1. First-in, first-out (FIFO)—assumes costs flow in the order

incurred.

6-5

2. Last-in, first-out (LIFO)—assumes costs flow in the reverse

order incurred.

3. Weighted average—assumes costs flow using an average of

4. Specific identification—each item can be identified with a

5. The units of inventory are identical under all methods.

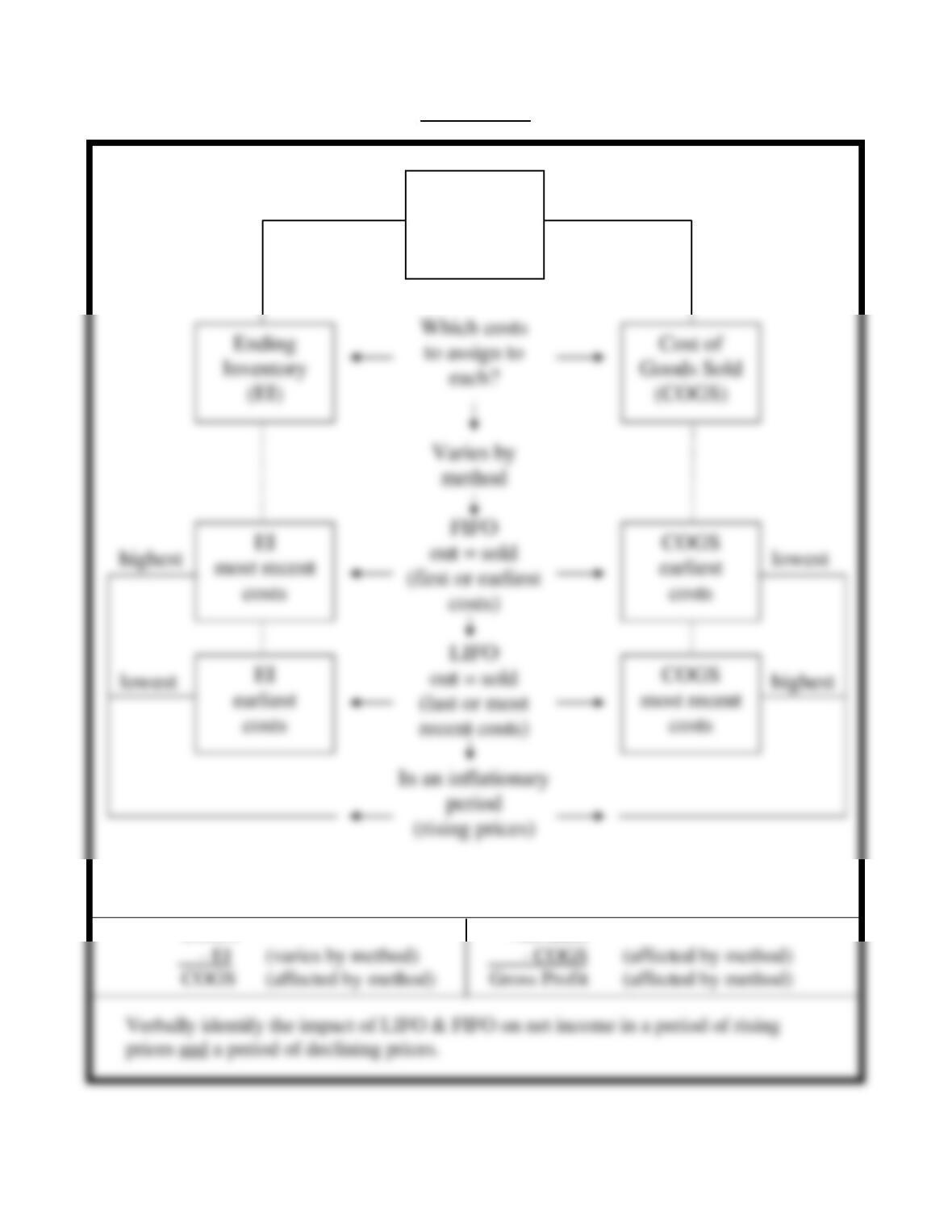

C. Financial Statement Effects of Costing Methods

1. When purchase prices do not change, each inventory costing

method assigns the same amounts to inventory and to cost of

goods sold. When purchase prices are different, the methods

assign different cost amounts. When purchase costs regularly

rise:

a. FIFO assigns the lowest amount to cost of goods sold

resulting in the highest gross profit and the highest net

D. Tax Effects of Costing Methods

Since inventory costs affect net income, they have potential tax

effects.

1. Financial reporting often differs from the method used for tax

reporting.

Chapter Outline

Notes

E. Consistency in Using Costing Methods

6-6

2. Method change is acceptable if it will improve financial

3. Different methods may be consistently applied to different

categories of inventory.

III. Valuating Inventory at LCM and the Effects of Inventory Errors

A. Lower of Cost or Market

Accounting principles require that inventory be reported on the

balance sheet at the lower of cost or market (LCM).

is lower, no adjustment is made.

1. Computing the Lower of Cost or Market:

2. When the recorded cost of inventory is higher than the

3. Lower of cost or market pricing is applied in one of three

ways to:

4. Recording the Lower of Cost or Market: accounting rules

require that inventory be adjusted to market when market is

less than cost, but inventory normally cannot be written up to

B. Financial Statement Effects of Inventory Errors.

An inventory error causes misstatements in cost of goods sold,

Chapter Outline

Notes

1. Income Statement Effects:

a. If ending inventory is understated, cost of goods sold is

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

6-7

2. Balance Sheet Effects:

a. If ending inventory is understated, assets and equity are

understated.

IV. Decision Analysis—Inventory Turnover and Days’ Sales in

Inventory

A. Inventory Turnover

1. Inventory turnover, also called simply turns, is used to

2. It is calculated by dividing cost of goods sold by average

inventory.

3. It measures the number of times a company’s average

inventory was sold during an accounting period.

B. Days’ Sales in Inventory

2. It is calculated by dividing ending inventory by cost of goods

sold, and then multiplying the result by 365.

3. It estimates how many days it will take to convert inventory at

the end of a period into accounts receivable or cash.

merchandisers; they must both plan and control inventory

C. Analysis of Inventory Management

V. Inventory Costing under a Periodic System (Appendix 6A)

The major goal is to properly assign costs with sales. The expense

statement) and how much is carried forward as inventory (on the

Chapter Outline

balance sheet). One of the most important issues in accounting for

inventory is determining the per unit cost assigned to inventory items.

Notes

A. Inventory Cost Flow Assumptions

Four methods are commonly used to assign costs to inventory and

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

6-8

1. Specific identification—At period-end, cost of goods sold is

2. First-in, first-out (FIFO)— At period-end, FIFO charges costs

3. Last-in, first-out (LIFO)— At period-end, LIFO charges costs

4. Weighted average—At period-end, weighted average

computes the average cost per unit of inventory available for

5. The units of inventory are identical under all methods.

VI. Inventory Estimation Methods (Appendix 6B)

Inventory sometimes requires estimation for two reasons. First,

companies often require interim financial statements, but only take an

annual physical count of inventory. Second, companies may require an

inventory estimate if some casualty makes taking a physical count

impossible. Estimates are usually only required for companies that use

the periodic system.

A. Retail Inventory Method

The retail inventory method estimates the cost of ending

inventory for interim statements in a periodic inventory when a

physical count is taken only annually. Steps include:

1. Subtract sales (general ledger amount) from goods available

3. Apply cost ratio to ending inventory at retail to convert to

ending inventory at cost.

taken using retail price to cost. Shrinkage can be measured by

comparing converted to estimated inventory.

Chapter Outline

B. Gross Profit Method

The gross profit method estimates the cost of ending inventory

by applying the gross profit ratio to net sales (at retail). This type

of estimate is often used for insurance claims when inventory is

Notes

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

6-9

destroyed, lost or stolen. Steps include:

1. Determine the normal gross profit percentage from recent

years.

3. Multiply actual sales by the cost of goods sold percentage to

get estimated cost of goods sold.

4. Subtract estimated cost of goods sold from the actual amount

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

6-10

VISUAL #6-1

Computation of Cost of Goods Available

Units Cost Total

Jan. 1 Beginning Inventory 60 @ $10 = $ 600

Mar. 27 Purchase 90 @ 11 = 990

Methods of Assigning Cost to Units in Ending Inventory

(2) Weighted Average – a weighted average cost per unit is determined

(3) First-in, First-out (FIFO) – assumes the first units acquired (beginning

(4) Last-in, First-out (LIFO) – assumes the last units acquired (most recent

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

6-11

VISUAL #6-2

O

OBSERVATIONS

COGA Net Sales

Goods

Available

(COGA)

has 2 parts

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

Chapter 6 Alternate Demonstration Problem #1 (Periodic)

The ABC Company had the following inventory record for the month of

January:

# of

Unit

Date

Description

Items

Price

Item

1/1

Beginning

inventory

5

$20

Z1, Z2, Z3, Z4, Z5

1/5

Sale

2

Z2, Z5

1/11

Purchase

9

12

Z6, Z7, Z8, Z9, Z10, Z11,

Z12, Z13, Z14

1/28

Sale

7

Z1, Z3, Z6, Z7, Z8, Z9, Z14

Required:

Assuming a periodic system is in use, determine the following:

1. Cost of goods available for sale.

2. Cost of goods sold and the ending inventory using each of the

following methods:

a. FIFO

b. LIFO

c. Weighted Average

d. Specific Identification

6-13

Solution: Chapter 6 Alternate Demonstration Problem #1

1. Cost of goods available for sale:

Date

Units

Unit Cost

Cost

inventory

1/11

Purchase

9

Total goods available for sale

$208

2. a. FIFO Periodic (FIFO under periodic and perpetual yields identical results).

Total goods available for sale

$208

Ending inventory

1/28

Purchase

5

Cost of goods sold

$148

b. LIFO Periodic:

Total goods available for sale

$208

Ending inventory

inventory

Cost of goods sold

$108

Units

Unit cost

Total cost

5

$100

9

$208

Total cost of 14units available for sale

$208

Less ending inventory priced on a weighted average cost basis:

5 units at $14.86

Cost of goods sold

$134

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

6-14

Specific Identification Periodic

Date

Purchases

Sales at Cost

Inventory

Balance

1/1

Beginning

Inventory

5 @ $ 20 = $100

Z1–Z5

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

Chapter 6 Alternate Demonstration Problem #2 (Perpetual)

The ABC Company had the following inventory record for the month of

January:

# of

Unit

Date

Description

Items

Price

Item

1/1

Beginning

inventory

5

$20

Z1, Z2, Z3, Z4, Z5

1/5

Sale

2

Z2, Z5

1/11

Purchase

9

12

Z6, Z7, Z8, Z9, Z10, Z11,

Z12, Z13, Z14

1/28

Sale

7

Z1, Z3, Z6, Z7, Z8, Z9, Z14

Required:

Assuming a perpetual system is in use, determine the cost of goods sold

and the ending inventory using each of the following methods:

1. FIFO

2. LIFO

3. Weighted average

4. Specific identification

6-16

Solution: Chapter 6 Alternate Demonstration Problem #2

1.

FIFO Perpetual

Date

Purchases

Sales at Cost

Inventory

Balance

Total COGS

2.

LIFO Perpetual

Date

Purchases

Sales at Cost

Inventory

Balance

Total COGS

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

Solution: Chapter 6 Alternate Demonstration Problem #2, continued

3.

Weighted Average Perpetual

Date

Purchases

Sales at Cost

Inventory

Balance

12 @ $14 = $168

Total COGS

4.

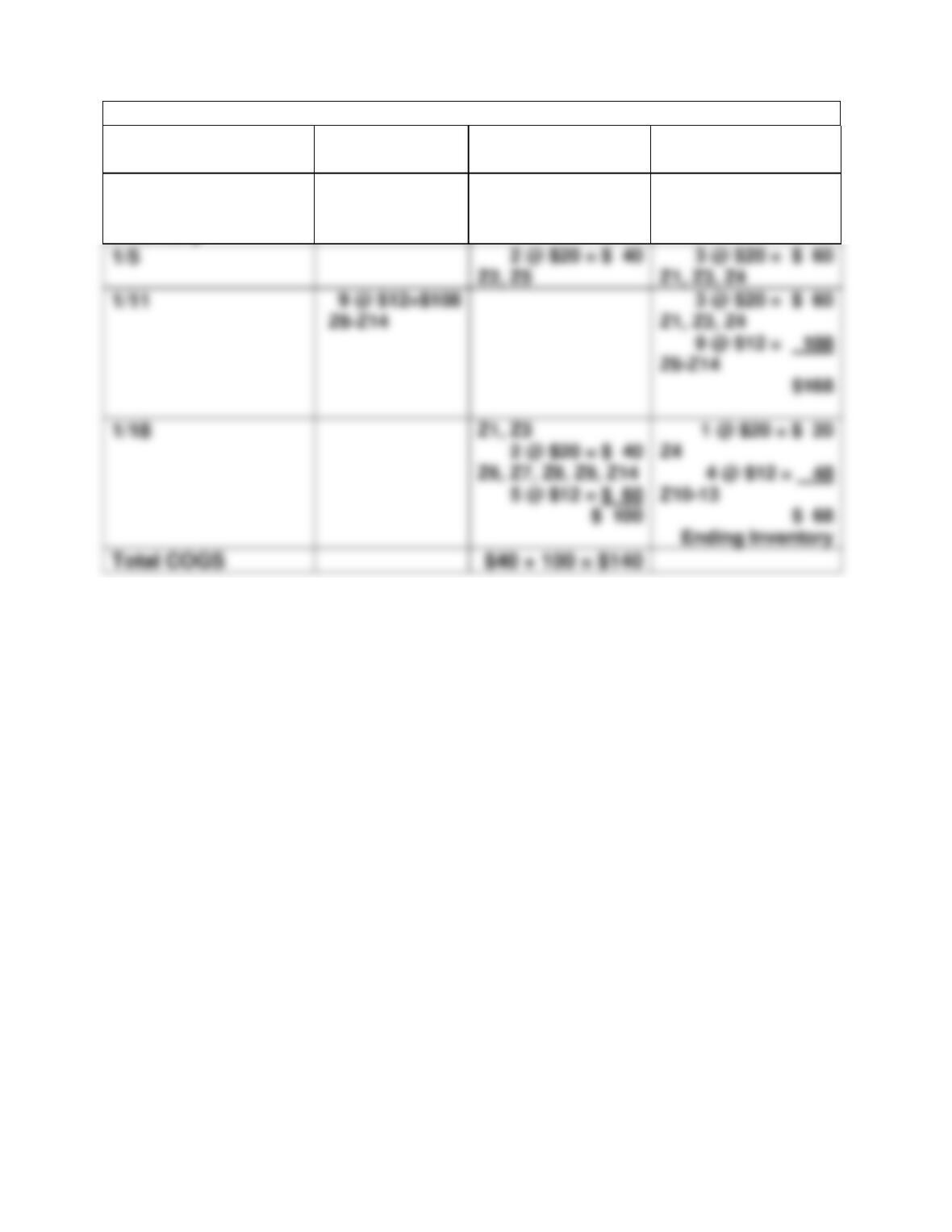

Specific Identification Perpetual

Date

Purchases

Sales at Cost

Inventory

Balance

1/1

5 @ $ 20 = $100