Financial Accounting

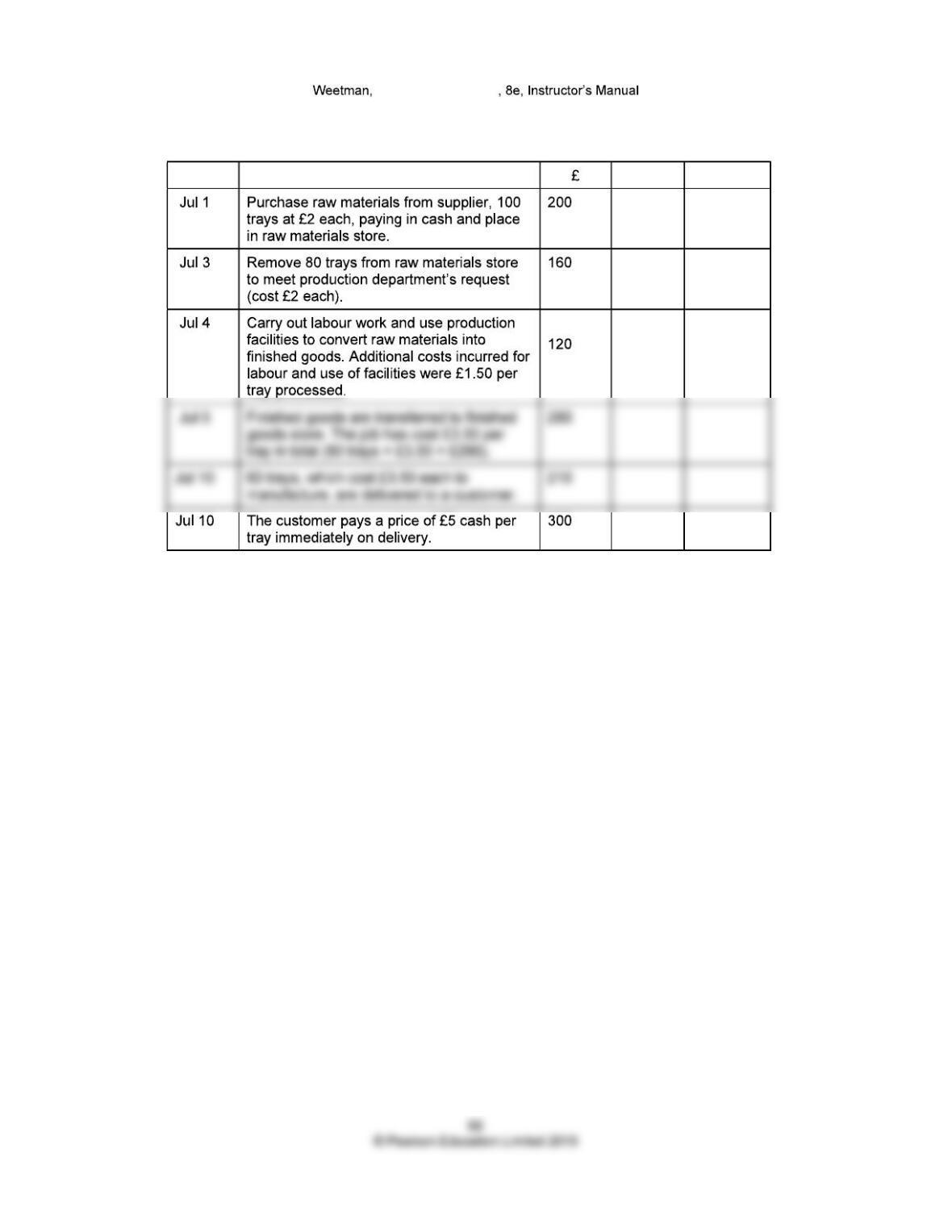

Transactions of a manufacturing company: debit and credit entries

Debit Credit

Financial Accounting

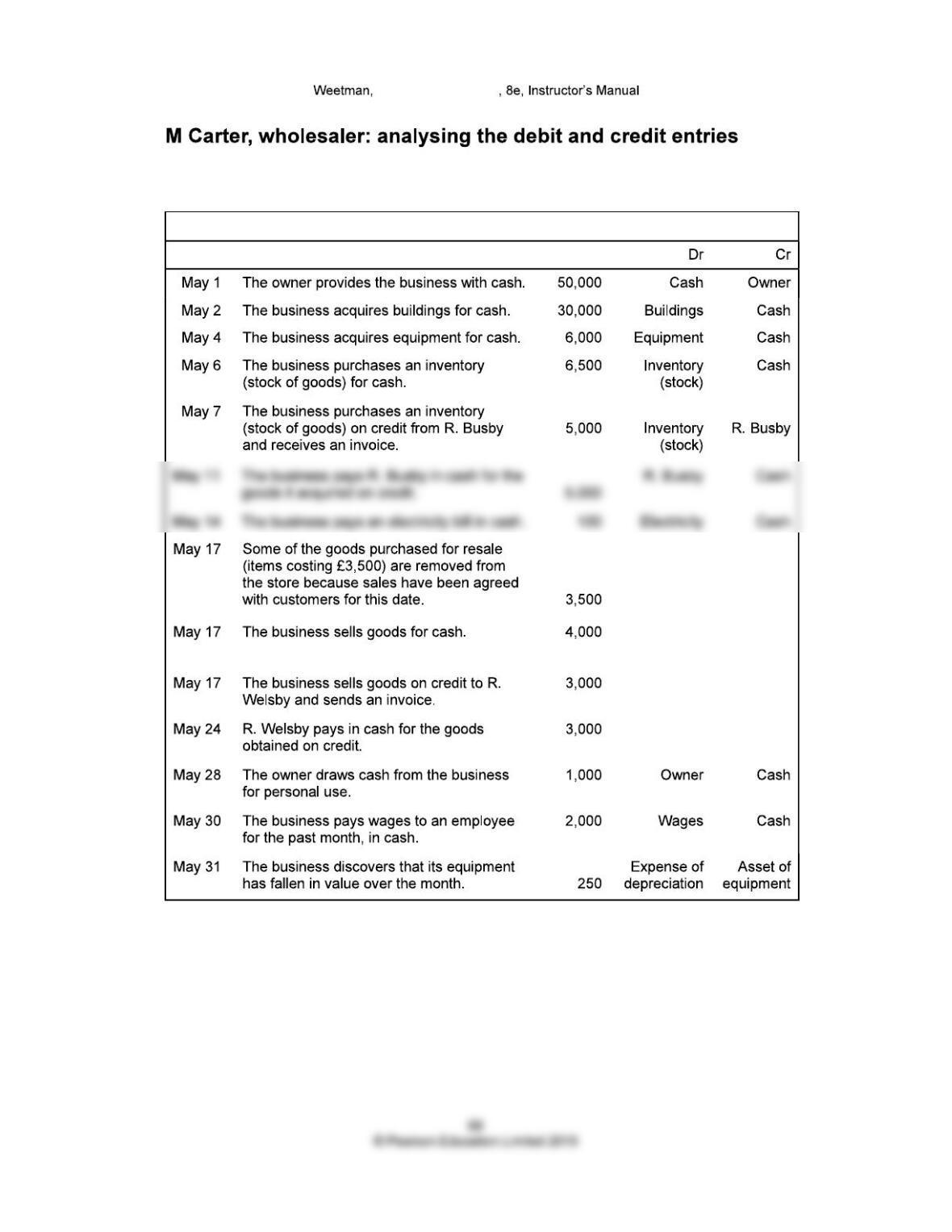

Analysis of transactions for M. Carter, wholesaler

Date Business transactions Amount Aspects

Financial Accounting

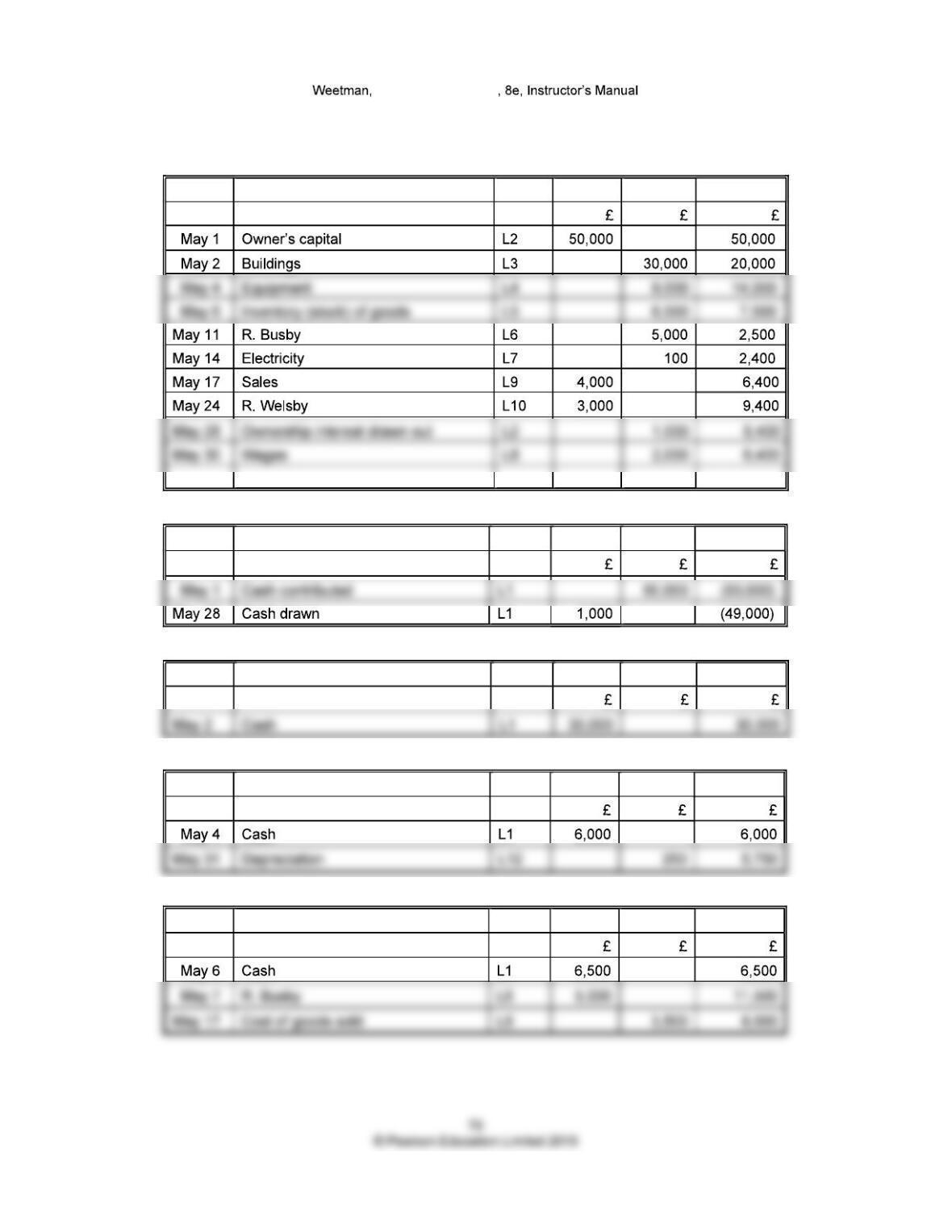

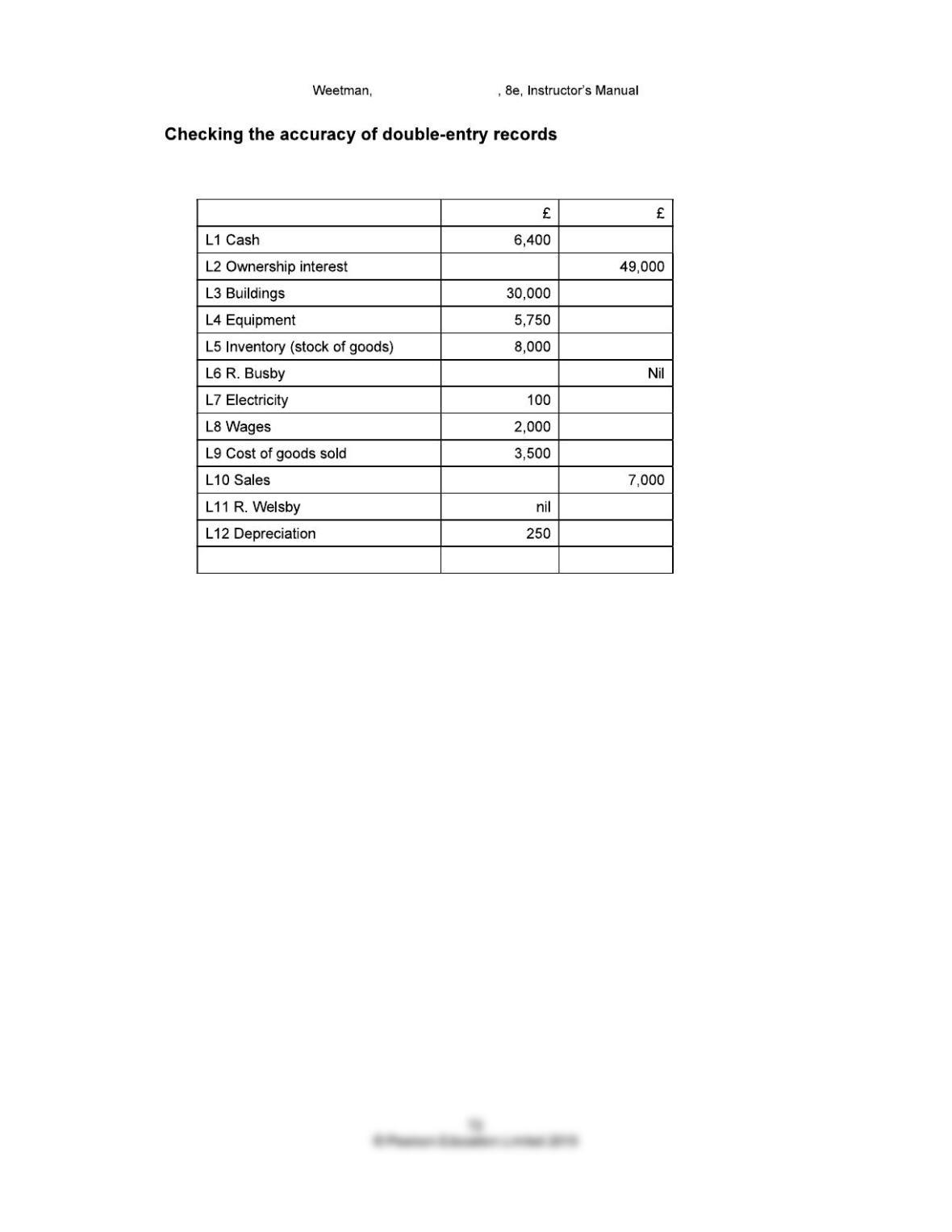

LEDGER ACCOUNTS (Read Supplement for detailed discussion)

L1 Cash

Date Particulars Page Debit Credit Balance

L2 Ownership interest

Date Particulars Page Debit Credit Balance

L3 Buildings

Date Particulars Page Debit Credit Balance

L4 Equipment

Date Particulars Page Debit Credit Balance

L5 Inventory (stock of goods)

Date Particulars Page Debit Credit Balance

Financial Accounting

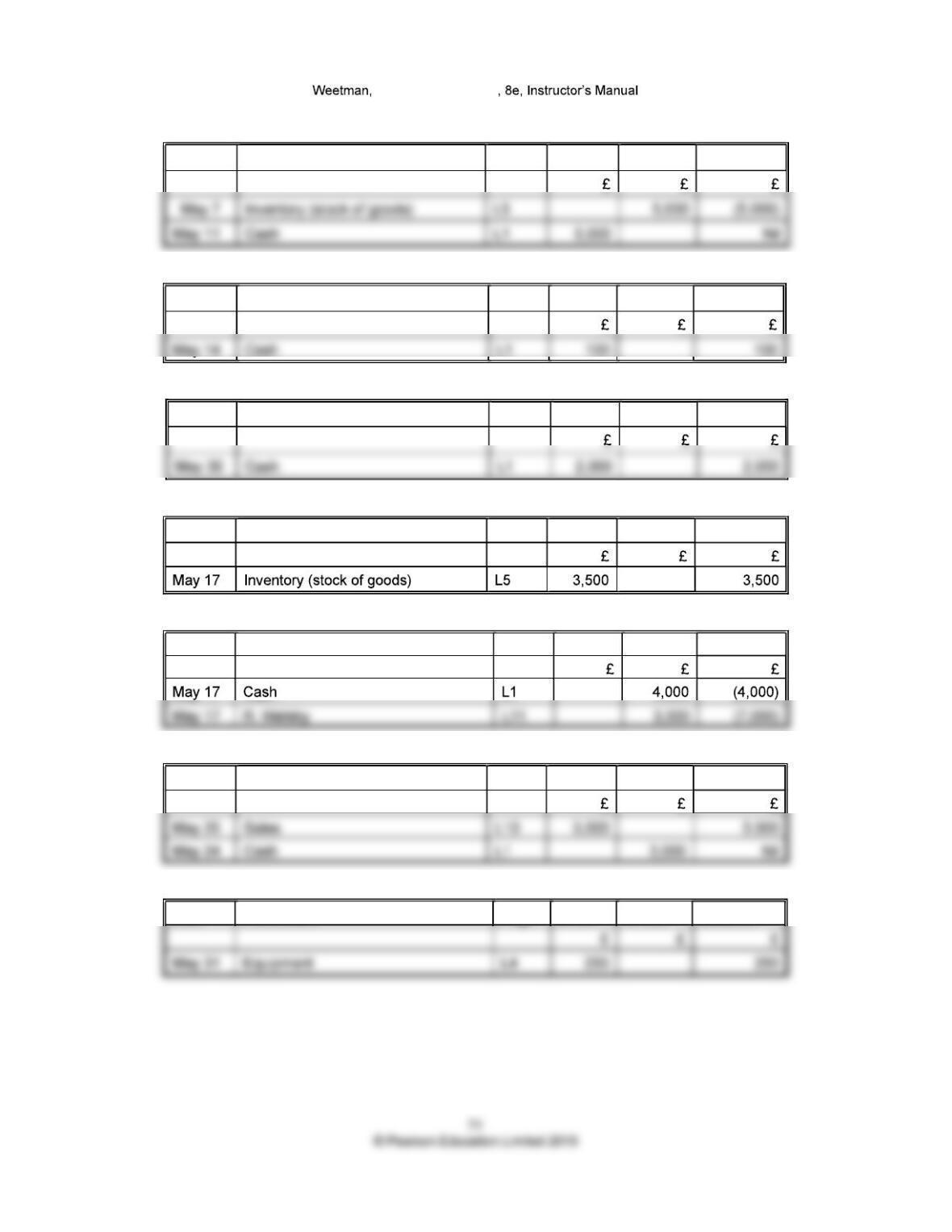

L6 R. Busby

Date Particulars Page Debit Credit Balance

L7 Electricity

Date Particulars Page Debit Credit Balance

L8 Wages

Date Particulars Page Debit Credit Balance

L9 Cost of goods sold

Date Particulars Page Debit Credit Balance

L10 Sales

Date Particulars Page Debit Credit Balance

L11 R. Welsby

Date Particulars Page Debit Credit Balance

L12 Depreciation

Date Particulars Page Debit Credit Balance

Financial Accounting

Trial balance at 31 May for M Carter, wholesaler

Leger account title

Totals 56,000 56,000

Compare this with the financial statements and check that all figures correspond.

Financial Accounting

FLOW OF ACCOUNTING INFORMATION

TRANSACTIONS INVOLVING CASH

For example, Paying cash to ..

Paying cash to

Paying cash for ..

Receiving cash from .

Receiving cash from .

Receiving cash from .

TRANSACTIONS NOT INVOLVING CASH

Buying goods .. from suppliers

Returning unwanted goods to suppliers

Selling goods to customers

Receiving rejected goods from customers

EVENTS AFFECTING THE BUSINESS

D of non-current (fixed) assets

B... when customers fail to pay

Financial Accounting

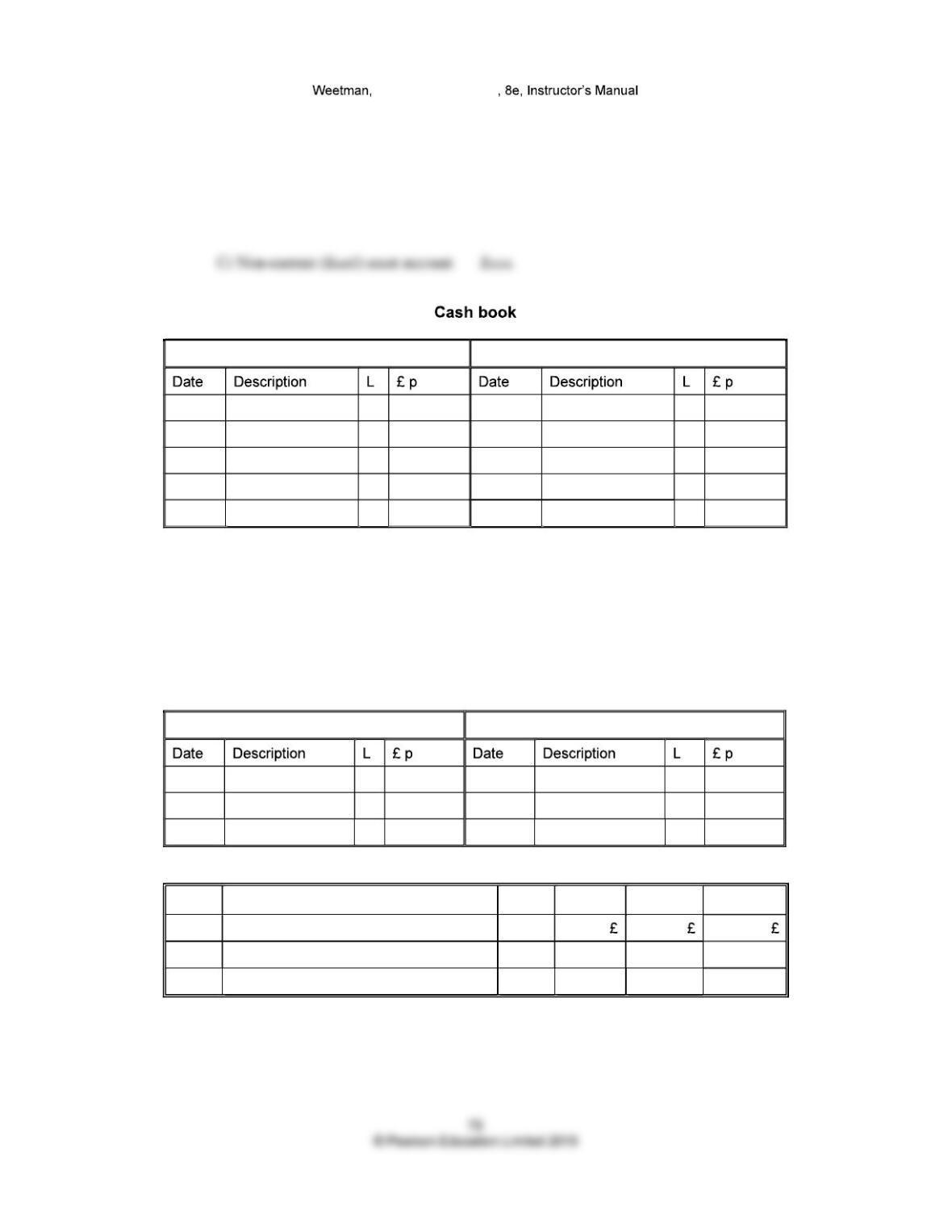

Cash book

A cash book contains details of every transaction of cash received or cash paid. At the end of

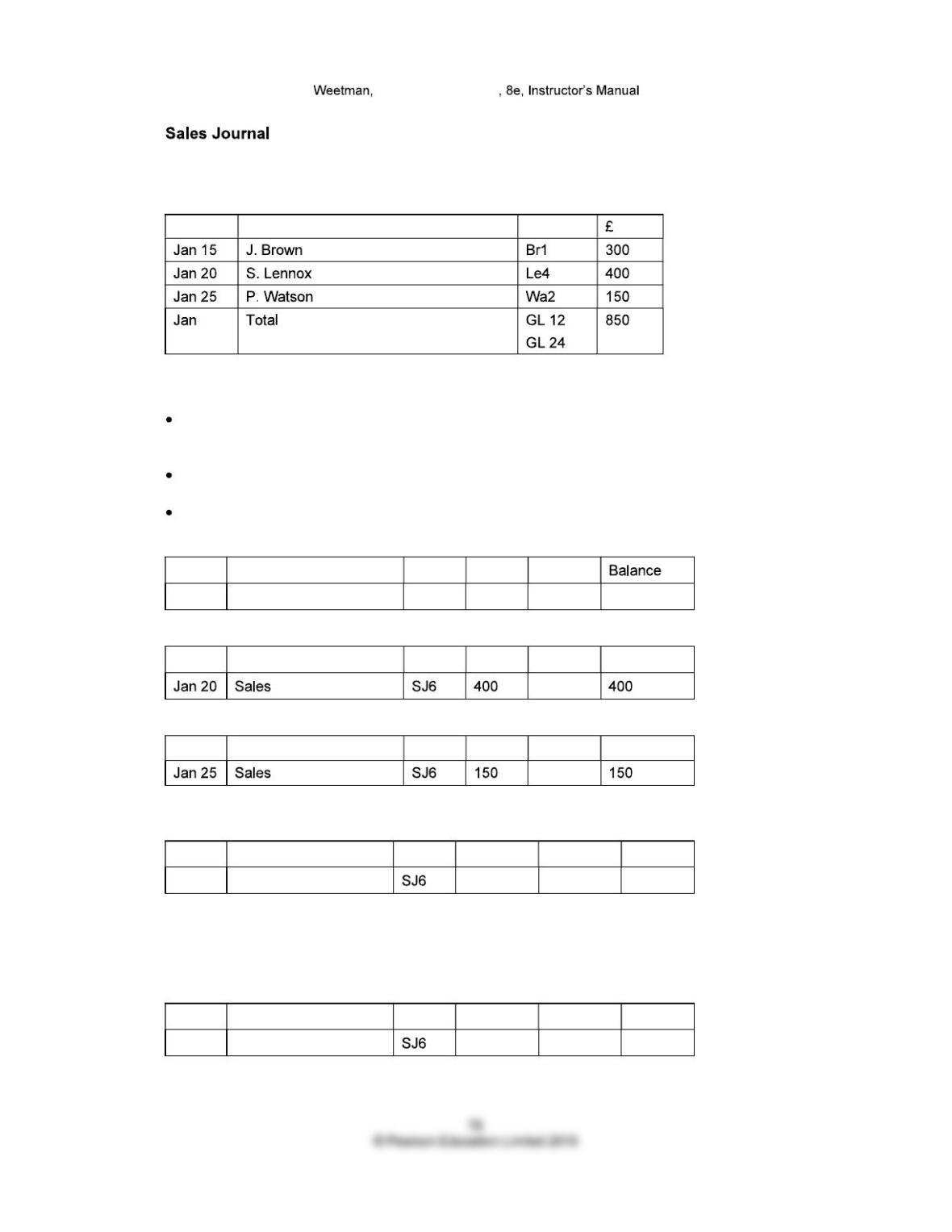

Sales day book (sales journal)

When goods or services are supplied on credit, the company sends an INVOICE.

The sales journal contains details of every transaction of sale of goods and services on credit

terms. It shows the date, name of customer and invoiced amount.

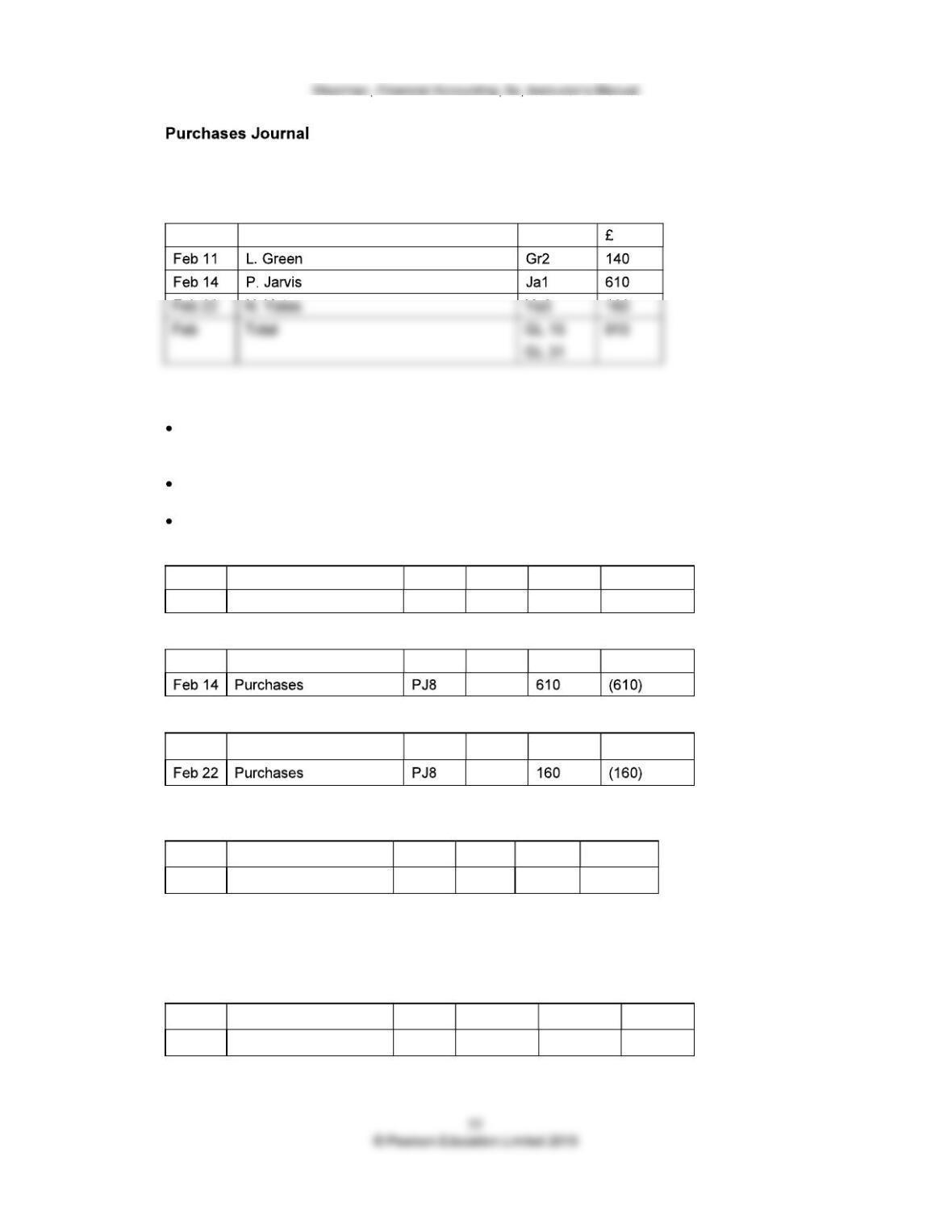

Purchases day book (purchases journal)

When goods or services are taken on credit, the supplier sends an INVOICE.

Sales returns book (sales returns journal)

When the customer returns the goods or rejects the service, a CREDIT NOTE is given. This

Purchases returns book (purchases returns journal)

Financial Accounting

Journal

Any transaction or event that cannot be recorded in one of the above is recorded in the journal.

It shows the debit and credit entry; for example:

Dr Expense of depreciation £xxx

Cash received Cash paid

The cash book is itself a ledger account and so has debit and credit sides. The bookkeeping

entry is completed by a matching credit or debit in another ledger account. The column headed

L gives the reference of the matching ledger account.

For example, on 12 January, the business pays wages of £100. The transaction is recorded as:

DEBIT Expense of wages £100

CREDIT Asset of cash £100

Cash received Cash paid

W1 WAGES

Date Particulars Page Debit Credit Balance

Financial Accounting

Sales on credit are as follows:

Sales Journal page SJ6

Ref

Transfers to ledger accounts:

Make one debit entry in the ledger account of each customer (not part of double entry but

useful for controlling records of payment by each customer).

Make debit entry for total receivables (debtors) in General Ledger (Nominal Ledger).

Make credit entry for total sales in General Ledger (Nominal ledger).

J. BROWN (Br1)

Debit Credit

S. LENNOX (Le4)

Debit Credit Balance

P. WATSON (Wa2)

Debit Credit Balance

GENERAL LEDGER (ALSO CALLED NOMINAL LEDGER)

RECEIVABLES (DEBTORS) ACCOUNT (Ref GL 12)

Debit Credit Balance

A single page in the general ledger (nominal ledger) is the total of the separate pages in the

Receivables (debtors) ledger (sometimes, confusingly, called the Sales ledger).

GENERAL LEDGER (ALSO CALLED NOMINAL LEDGER)

SALES ACCOUNT (Ref GL 24)

Debit Credit Balance

Purchases on credit are as follows:

Purchases Journal page PJ8

Ref

Transfers to ledger accounts:

Make one credit entry in the ledger account of each supplier (not part of double entry but

useful for tracking records of payment to each supplier).

Make credit entry for total payables (creditors) in General Ledger (Nominal Ledger).

Make debit entry for total purchases in General Ledger (Nominal ledger).

L. GREEN (Gr2)

Debit Credit Balance

P. JARVIS (Ja1)

Debit Credit Balance

N. YATES (Ya3)

Debit Credit Balance

GENERAL LEDGER (ALSO CALLED NOMINAL LEDGER)

TOTAL PAYABLES (CREDITORS) ACCOUNT (Ref GL 15)

Debit Credit Balance

A single page in the general ledger (nominal ledger) is the total of the separate pages in the

Payables (creditors) ledger (sometimes, confusingly, called the Purchases ledger).

GENERAL LEDGER (ALSO CALLED NOMINAL LEDGER)

PURCHASES ACCOUNT (Ref GL 31)

Debit Credit Balance

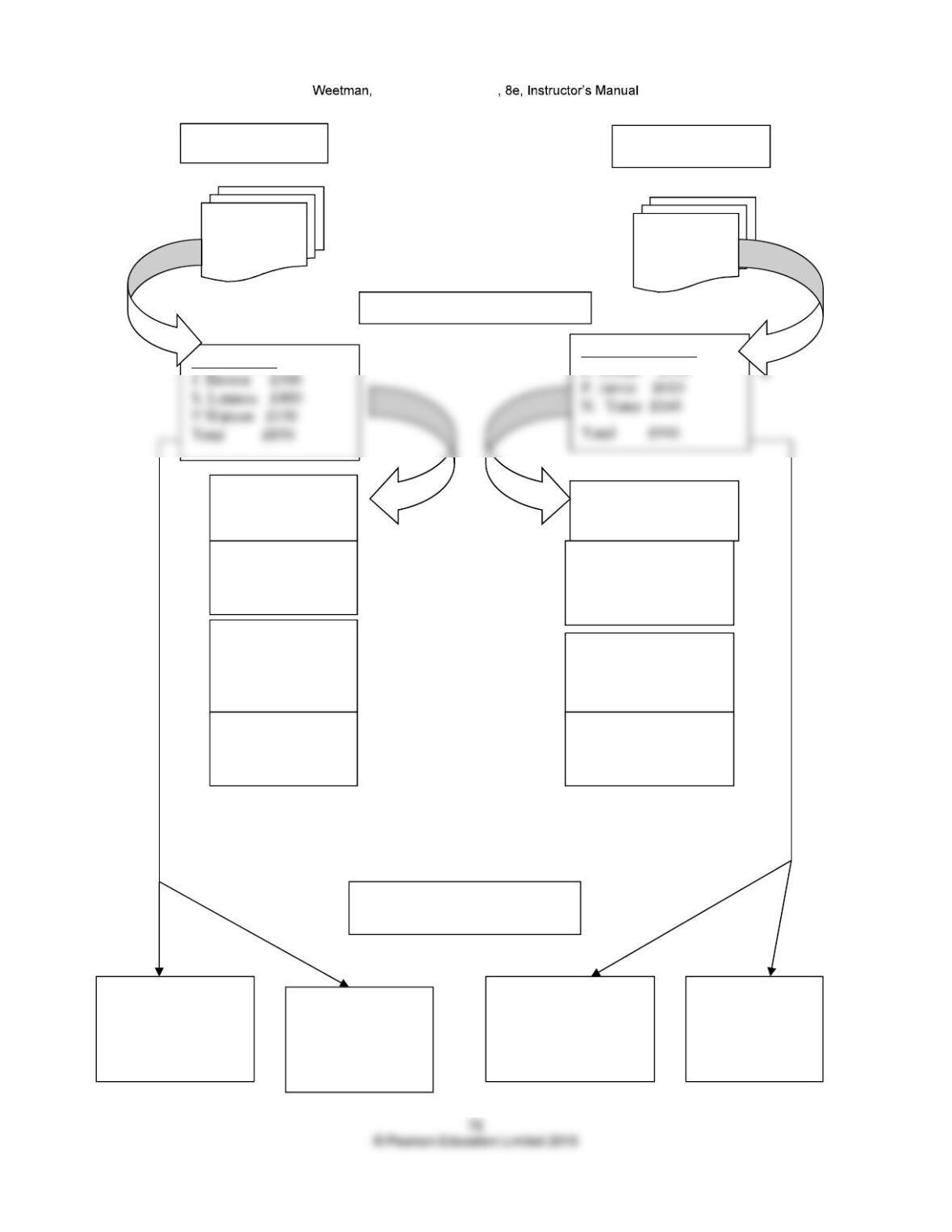

Financial Accounting

Customer

Goods

£

Supplier

Goods

£

Sales Journal

Purchases Journal

L. Green £140

Day Books

Sales invoices Purchase invoices

Receivables

(Debtors) ledger Payables

(Creditors) ledger

J. Brown

Dr Cr Bal

300

S. Lennox

Dr Cr Bal

400

P. Watson

Dr Cr Bal

.. 150

P. Jarvis

Dr Cr Bal

(610)Cr

L. Green

Dr Cr Bal

(140)Cr

N. Yates

Dr Cr Bal

.. (160)Cr

General Ledger

(Nominal Ledger)

Sales

Dr Cr Bal

.. (850)Cr

Purchases

Dr Cr Bal

.. 910

Receivables

(debtors)

Dr Cr Bal

... 850

Payables

(creditors)

Dr Cr Bal

(910)Cr