CHAPTER 6

SOLUTIONS TO EXERCISES—SET B

EXERCISE 6-1B

(a) (1) Contribution margin per room = $50 – ($5 + $25)

Contribution margin per room = $20

Contribution margin ratio = $20 ÷ $50 = 40%

(2) Break-even point in dollars = 1,000 rooms X $50 per room

= $50,000 per month

(b) (1) Margin of safety in dollars:

Planned activity = 40 rooms per day X 30 days

= 1,200 rooms per month

EXERCISE 6-2B

(a) Contribution margin (in dollars): Sales = (3,100 X $32) = $99,200

Variable costs = $99,200 X .60 = 59,520

EXERCISE 6-2B (Continued)

(b) Breakeven sales (in dollars):

$28,000

40%

= $70,000

(c) Margin of safety (in dollars): $99,200 – $70,000 = $29,200.

EXERCISE 6-3B

1. Unit sales price = $320,000 ÷ 4,000 units = $80

2. Reduce variable costs to 65% of sales.

Alternative 1, increasing selling price, will produce the highest net income.

EXERCISE 6-4B

(a)

(1) Contribution margin ratio is:

$37,500

= 62.5%

$60,000

EXERCISE 6-4B (Continued)

(b) At the break-even point fixed costs and contribution margin are equal.

Therefore, the contribution margin at the break-even point would be

$22,500.

(c)

Fare revenue ($135* X 480**) ………………

$64,800

Variable costs ($22,500 X 1.20) …………..

27,000

EXERCISE 6-5B

DARRON COMPANY

CVP Income Statement (Current)

For the Year Ended December 31, 2017

Total

Per Unit

Sales (50,000 X $25) …………………………………

$1,250,000

$25

Contribution margin ………………………….

Fixed costs ……………………………………….

Net income ……………………………………….

EXERCISE 6-5B (Continued)

DARRON COMPANY

CVP Income Statement (with Changes)

For the Year Ended December 31, 2017

Total

Per Unit

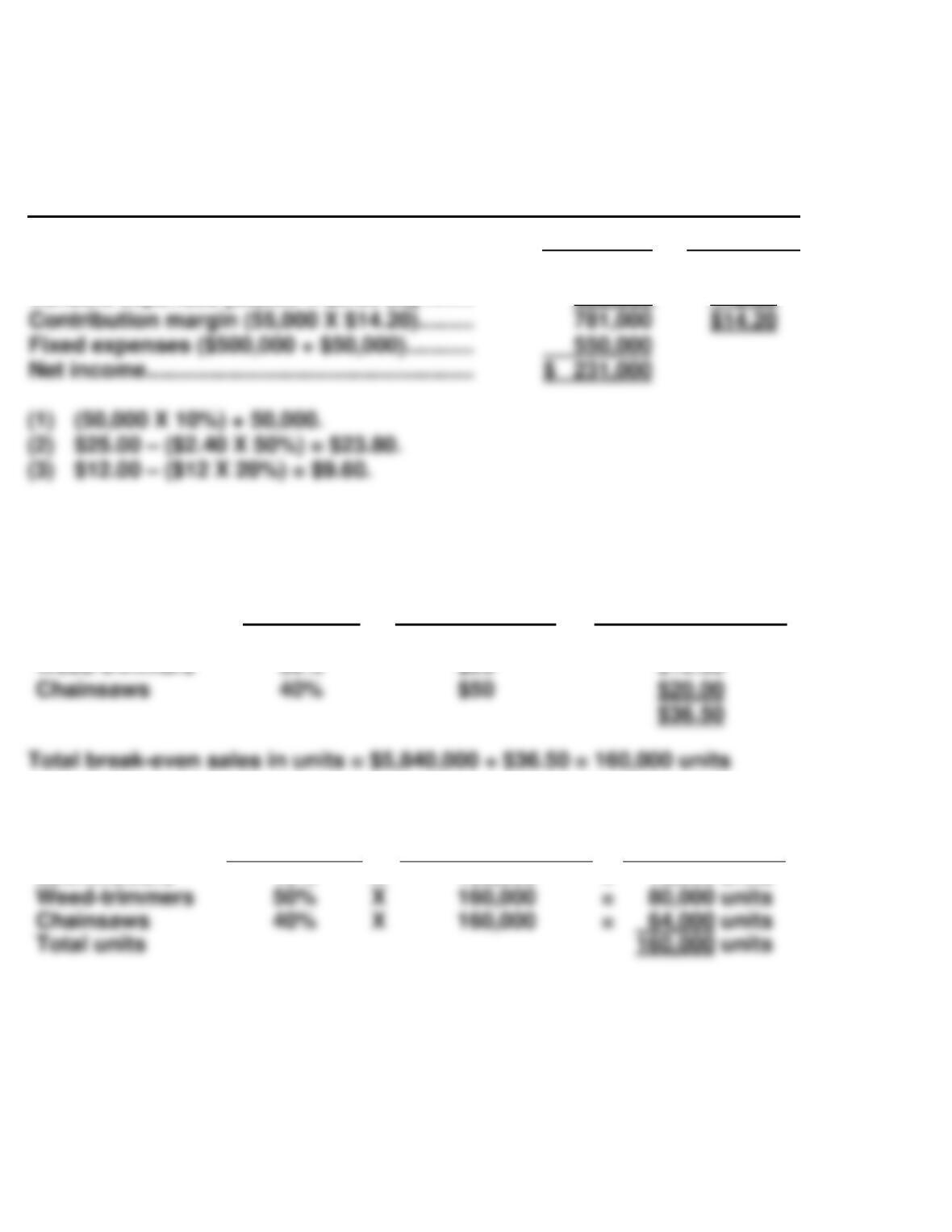

Sales [55,000 units (1) X $23.80 (2)] ………….

Variable expenses [55,000 X $9.60 (3)] ……..

$1,309,000

528,000

$23.80

9.60

EXERCISE 6-6B

Sales Mix

Percentage

Contribution

Margin Per Unit

Weighted-Average

Contribution Margin

Lawnmowers

10%

$40

$4.00

Sales Mix

Percentage

Total

Break-even Sales

in Units

Sales Units

Needed

Per Product

Lawnmowers

10%

X

160,000

=

16,000 units

EXERCISE 6-7B

(a)

Sales Mix

Percentage

Contribution

Margin Ratio

Weighted-Average

Contribution

Margin Ratio

Oil changes

70%

20%

.14

Sales Mix

Percentage

Total

Break-even Sales

in Dollars

Sales Dollars

Needed

Per Product

Total sales

Oil changes

70%

X

$37,500,000

=

$26,250,000

(b)

Sales to achieve target net income = ($40,000 + $75,200) ÷ .32 = $360,000

Sales Mix

Percentage

Total

Sales Needed

Sales Dollars

Needed Per Product

Per Store

Total sales

Oil changes

70%

X

$360,000

=

$252,000

EXERCISE 6-8B

(a)

Sales Mix

Percentage

Contribution

Margin Ratio

Weighted-Average

Contribution

Margin Ratio

Mail pouches

and small boxes

80%

10%

.08

EXERCISE 6-8B (Continued)

Sales Mix

Percentage

Total Break-

even Sales

in Dollars

Sales Dollars

Needed

Per Product

Mail pouches

and small boxes

80%

X

$60,000,000

=

$48,000,000

(b)

Sales Mix

Percentage

Contribution

Margin Ratio

Weighted-Average

Contribution

Margin Ratio

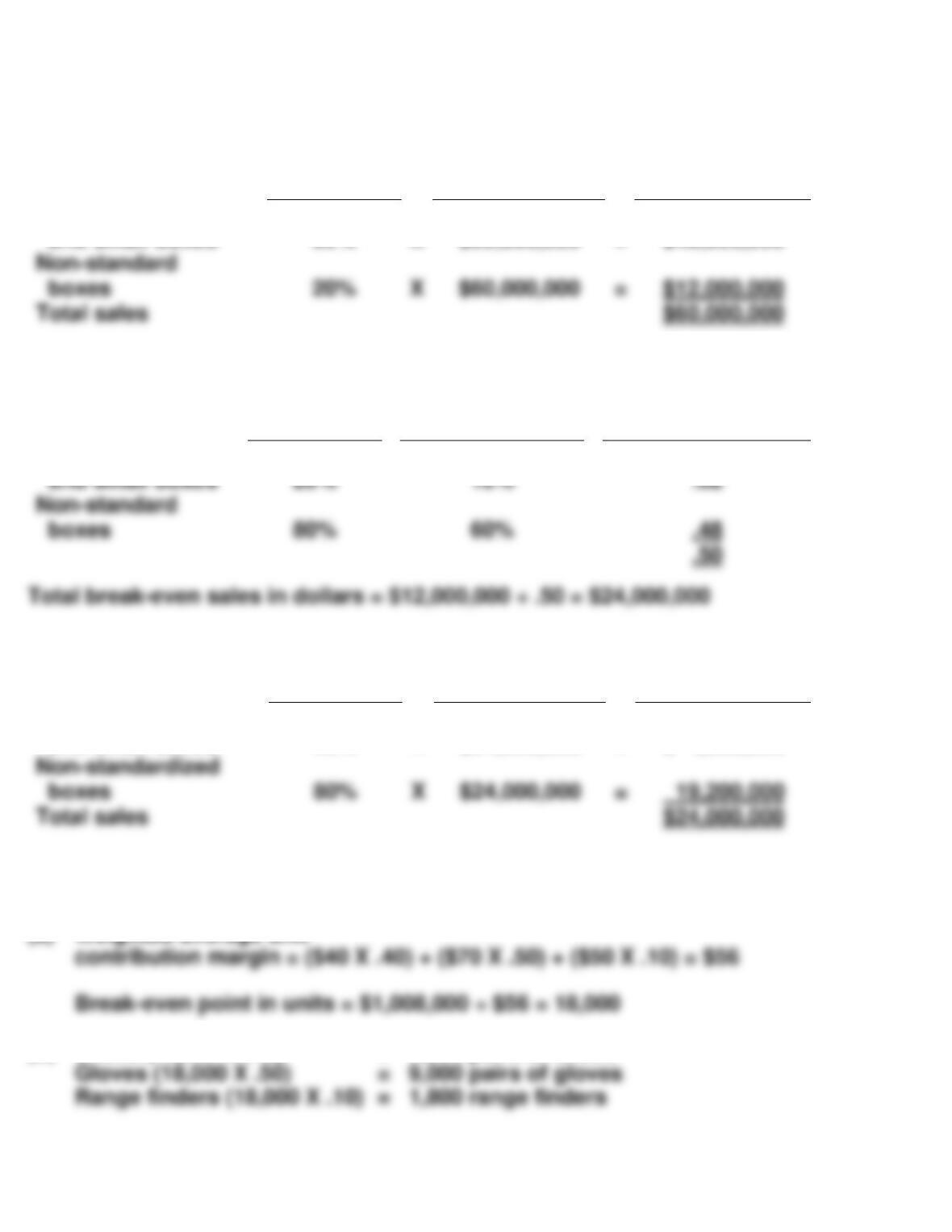

Non-standard

Mail pouches

Sales Mix

Percentage

Total Break-

even Sales

in Dollars

Sales Dollars

Per Product

Total sales

Mail pouches

and small boxes

20%

X

$24,000,000

=

$ 4,800,000

EXERCISE 6-9B

(a) Weighted-average unit

(b) Shoes (18,000 X .40) = 7,200 pairs of shoes

Non-standard

Total sales

$60,000,000

EXERCISE 6-9B (Continued)

(c) Shoes: 7,200 X $40 = $288,000

Gloves: 9,000 X $70 = 630,000

EXERCISE 6-10B

(a) Sales mix percentage

TV division: $800,000 ÷ ($800,000 + $200,000) = .80

(b) Weighted-average contribution

(c) Break-even point in dollars = $140,000 ÷ .28 = $500,000

(d) Sales dollars needed at break-even point for each division

EXERCISE 6-11B

(a)

Product

A

B

C

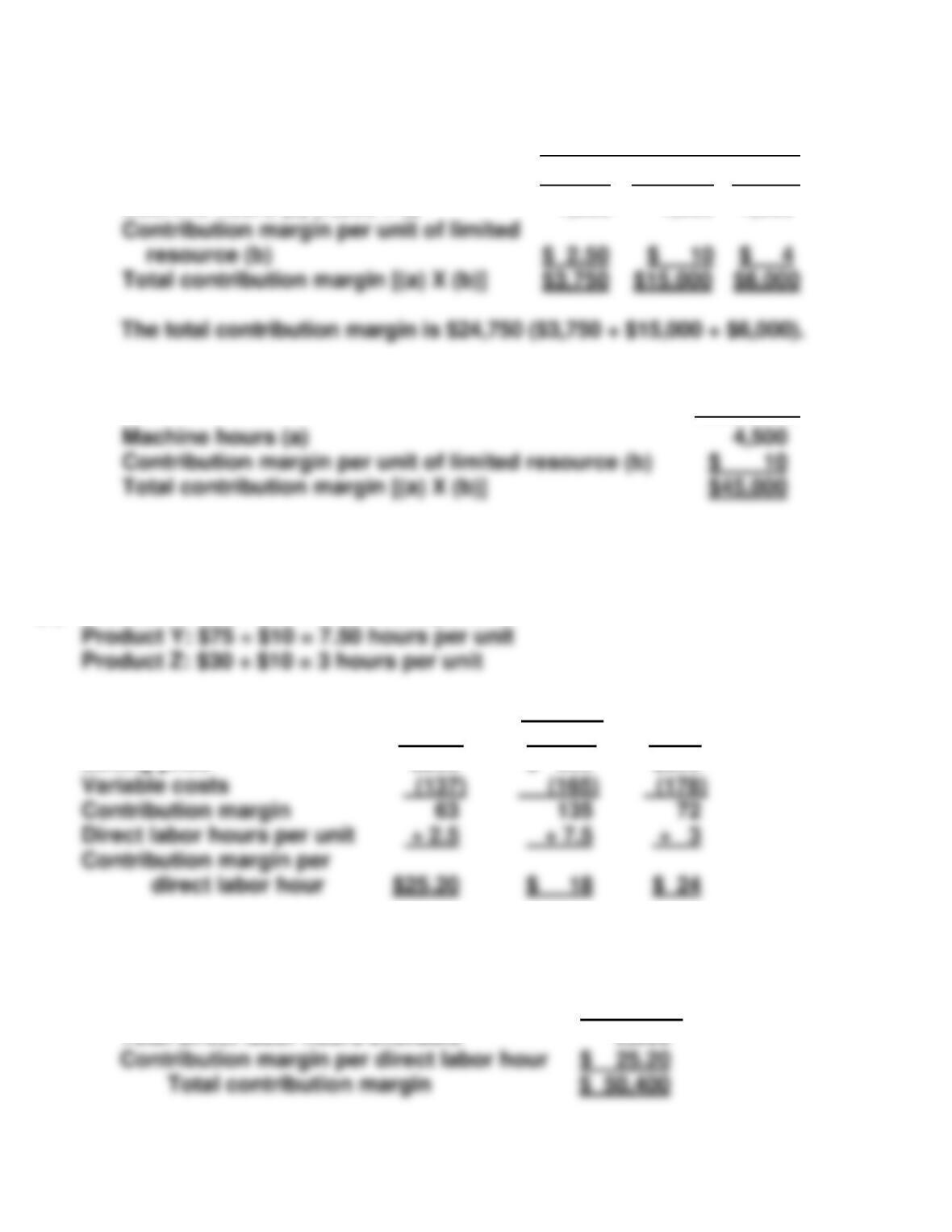

Contribution margin per unit of limited resource (a) ÷ (b)

$2.50

Contribution margin per unit (a)

$5

$10

$8

(b) Product B should be manufactured because it results in the highest

contribution margin per machine hour.

EXERCISE 6-11B (Continued)

(c)

(1)

Product

A

B

C

Machine hours (a) (4,500 ÷ 3)

1,500

1,500

1,500

(2)

Product

B

Total contribution margin [(a) X (b)]

EXERCISE 6-12B

(a)

Product X: $25 ÷ $10 = 2.50 hours per unit

Product Y: $75 ÷ $10 = 7.50 hours per unit

Product Z: $30 ÷ $10 = 3 hours per unit

(b)

Product

X

Y

Z

Selling price

$200

$ 300

$250

Variable costs

Contribution margin

Direct labor hours per unit

÷ 7.5

Contribution margin per

direct labor hour

(c) Product X should be produced because it generates the highest contri–

bution margin per direct labor hour.

Product X

Total direct labor hours available

2,000

Contribution margin per direct labor hour

Total contribution margin

Total contribution margin [(a) X (b)]

$3,750

$15,000

$6,000

EXERCISE 6-13B

(a)

Product

Basic

Deluxe

Selling price per unit

$40

$52

(b) The Basic product should be manufactured because it results in the

higher contribution margin per machine hour.

(c)

(1)

Basic

Deluxe

Total

Machine hours allocated

500

500

1,000

X Contribution margin

(2)

Basic

Deluxe

Total

Machine hours allocated

1,000

–0–

1,000

per machine hour

X Contribution margin

EXERCISE 6-14B

(a)

Contribution

Margin

÷

Net

Income

=

Degree of Operating

Leverage

Vericelli

Boone

÷

÷

=

=

Contribution margin per unit (a)

Machine hours required (b)

Contribution margin per

machine hour (a) ÷ (b)

EXERCISE 6-14B (Continued)

(b)

Vericelli Company

Boone Company

Sales

$660,000**

$660,000***

*$600,000 X 1.1

(c) Each company experienced a $60,000 increase in sales. However, be–

cause of Boone’s higher operating leverage, it experienced a $48,000

EXERCISE 6-15B

(a)

Contribution

Margin

÷

Net Income

=

Degree of

Operating Leverage

Computerized

÷

=

(b) The computerized system would produce profits that are 1.5 times

EXERCISE 6-15B (Continued)

Manual

System

Computerized

System

Sales

Variable costs

$1,800,000

1,350,000*

$1,800,000

1,125,000**

(c)

(Actual Sales

–

Break-even Sales)

÷

Actual Sales

=

Margin of Safety Ratio

–

÷

=

Manual system

($1,600,000

–

$1,200,000*)

÷

$1,600,000

=

.25

EXERCISE 6-16B

(a)

Contribution

Margin

÷

Net

Income

=

Degree of Operating

Leverage

Jonathan

÷

=

Delicious

$100,000

÷

$ 80,000

=

1.25

EXERCISE 6-16B (Continued)

(b)

% Change

in Sales

X

Degree of

Operating

Leverage

=

% Change in

Net Income

10% decrease:

Delicious

(10%)

X

1.25

=

(12.5%)

(c) There are several possible answers that could be given. For example, if

the candied apple business is fairly stable, Jonathan might be the

choice, because it will generate the higher contribution margin and net

*EXERCISE 6-17B

(a)

Unit Cost

Direct materials

$ 7.50

Direct labor

2.25

6.00

Manufacturing cost per unit

$15.75

Jonathan

X

=

*EXERCISE 6-17B (Continued)

(b)

KARE COMPANY

Income Statement

For the Year Ended December 31, 2017

Variable Costing

Sales (80,000 lures X $28) …………………….

$2,240,000

Variable cost of goods sold

(80,000 lures X $15.75) ……………………….

$1,260,000

(c)

Unit Cost

Direct materials ……………………………………………..

$ 7.50

Direct labor …………………………..………………………

2.25

Variable manufacturing overhead …………………..

Fixed manufacturing overhead ($290,000 ÷ 100,000)

2.90

Manufacturing cost per unit ……………………………….

(d)

KARE COMPANY

Income Statement

For the Year Ended December 31, 2017

Absorption Costing

Sales (80,000 lures X $28) ………………………….

$2,240,000

Cost of goods sold (80,000 lures X $18.65) …

1,492,000

Gross profit ………………………………………………

Fixed selling and administrative expenses …

557,300

Net Income ……………………………………………….

Variable selling and administrative

expenses (80,000 lures X $4.00) ………….

320,000

Contribution margin …………………………….

Fixed manufacturing overhead …………….

Fixed selling and administrative

expenses …………………………..………………

Net Income (loss)…………………………………

*EXERCISE 6-18B

(a) Direct materials used $ 85,000

Direct labor incurred 30,000

(b) Absorption costing would show a higher net income because a portion

of the fixed costs are deferred to future periods. The following

computation indicates that finished goods inventory will be $6,000

higher under absorption costing which will cause its net income to be

$6,000 higher.

Direct materials used $ 85,000

Direct labor incurred 30,000

*EXERCISE 6-19B

(a)

Utility Expense

Months in

a year

X

Kilowatt

hours

X

Hourly

Charge

=

Variable

Utilities

*EXERCISE 6-19B (Continued)

Variable Costing

Labor:

Crate builders

$37,000

Material:

(b)

Absorption Costing

Labor:

Crate builders

$ 37,000

Material:

Variable overhead:

Utilities

Fixed overhead:

Utilities

Total manufacturing costs

(c) The entire difference in costs between the two methods is due to the

Wood

Variable Overhead:

Nails

Total manufacturing costs

$94,350

SOLUTIONS TO PROBLEMS—SET C

PROBLEM 6-1C

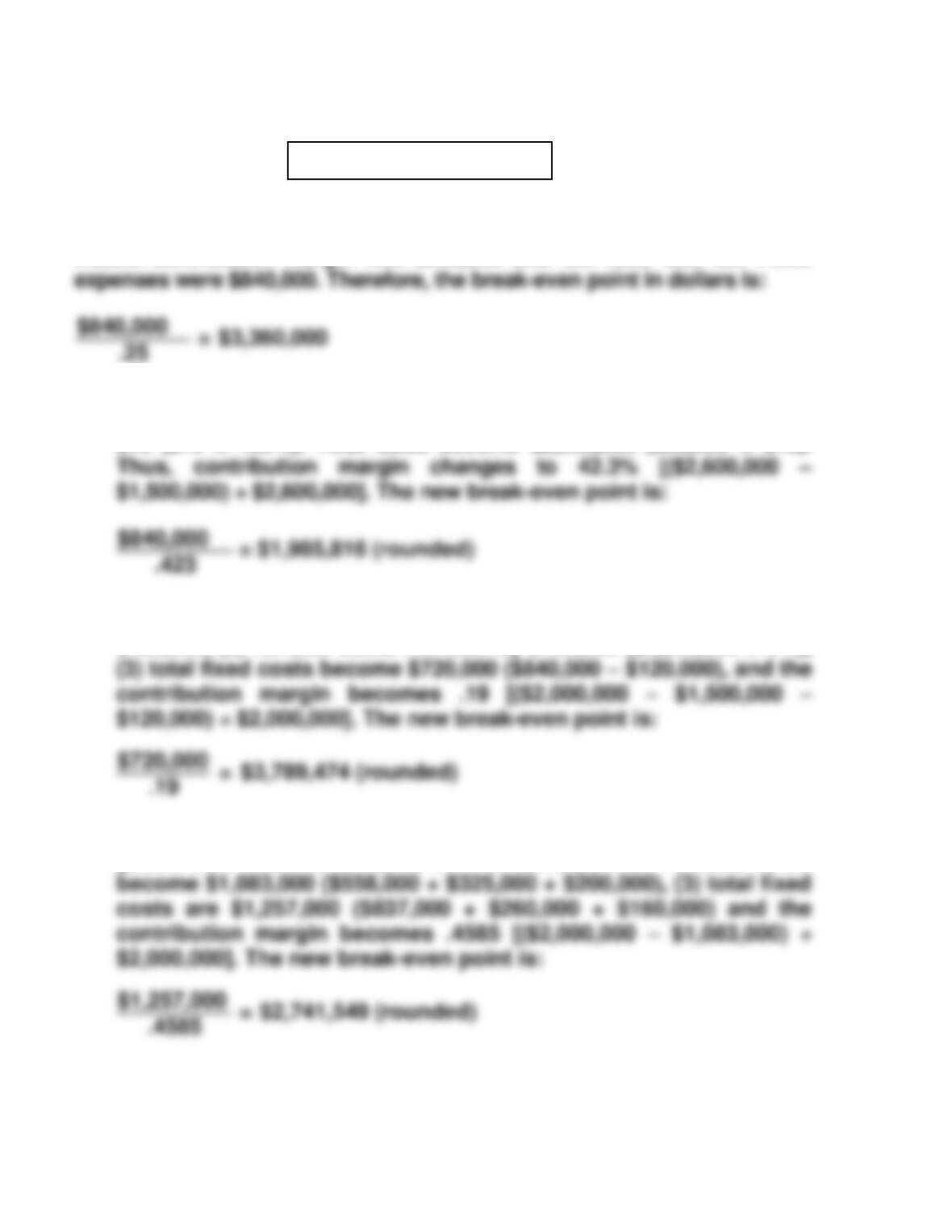

(a) Sales were $2,000,000 and variable expenses were $1,500,000, which

means contribution margin was $500,000 and CM ratio was .25. Fixed

(b) (1) The effect of this alternative is to increase the selling price per unit to

$13 ($10 X 130%). Total sales become $2,600,000 (200,000 X $13).

(2) The effects of this alternative are: (1) fixed costs decrease by

$120,000, (2) variable costs increase by $120,000 ($2,000,000 X 6%),

(3) The effects of this alternative are: (1) variable and fixed cost of

goods sold become $558,000 and 837,000, (2) total variable costs

Alternative 1 is the recommended course of action using break-even

analysis because it has the lowest break-even point.

PROBLEM 6-2C

(a)

(1)

Current Year

Sales

Variable costs

Direct materials

Direct labor

$1,500,000

300,000

169,500

Current Year

Projected Year

Contribution margin

Sales

Variable costs

Direct materials

$1,500,000

300,000

X 1.2

X 1.2

$1,800,000

360,000

(2)

Fixed Costs

Current Year

Projected year

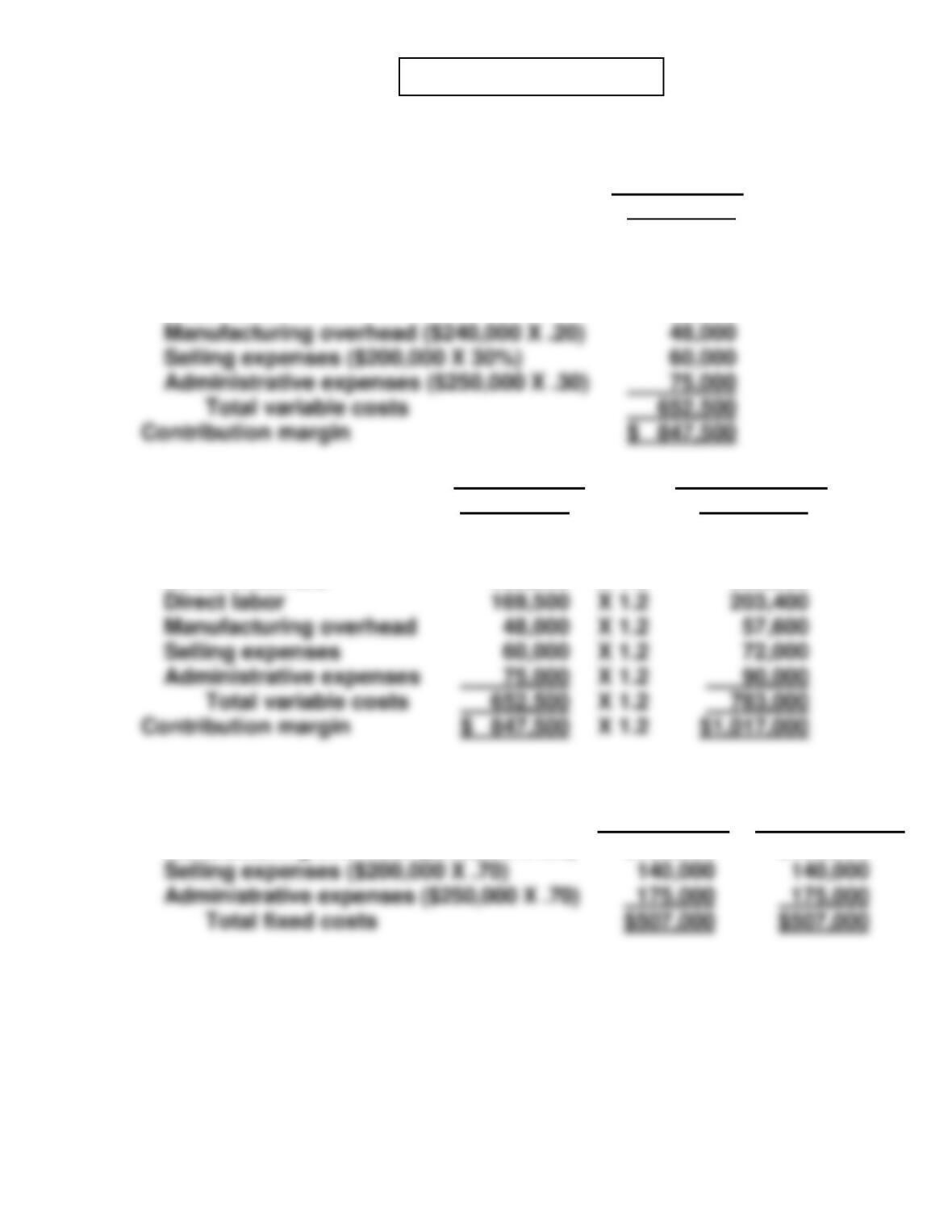

Total fixed costs

Manufacturing overhead ($240,000 X .80)

$192,000

$192,000

Selling expenses ($200,000 X 30%)

Contribution margin

PROBLEM 6-2C (Continued)

(b) Unit selling price = $1,500,000 ÷ 50,000 = $30.00

Unit variable cost = $652,500 ÷ 50,000 = $13.05

(c) Sales dollars

required for

=

(Fixed costs

+

Target net income)

÷

Contribution margin ratio

target net income

(rounded)

ratio

=

÷

(e)

(1)

Current Year

Contribution margin

Total fixed costs

Sales

Variable costs

Direct materials

Direct labor ($169,500 – $70,500)

$1,500,000

300,000

99,000

Break-even point in units

=

Fixed costs

÷

Unit contribution margin

=

÷

Break-even point in dollars

=

Fixed costs

÷

Contribution margin ratio

=

÷

PROBLEM 6-2C (Continued)

(3) Break-even point in dollars = $431,000 ÷ .561 = $768,271 (rounded)

The break-even point in dollars declined from $897,345 to $768,271. This

means that overall the company’s risk has declined because it doesn’t

have to generate so much in sales. The two changes actually had

PROBLEM 6-3C

(a)

Sales Mix

Percentage

X

Contribution

Margin Ratio

=

Weighted-Average

Contribution

Margin Ratio

Appetizers

Main entrees

30%

50%

X

X

60%

25%

=

=

.18

.125

.435

Total sales required

Sales Mix

Percentage

X

Total Sales

=

Sales from

Each Product

Main entrees

Desserts

Beverages

X

X

X

=

=

=

Appetizers

30%

X

$1,000,000

=

$300,000

(b)

Sales Mix

Percentage

X

Contribution

Margin Ratio

=

Weighted-Average

Contribution

Margin Ratio

Desserts

Beverages

X

X

=

=

Appetizers

Main entrees

35%

40%

X

X

70%

10%

=

=

.245

.04

Total sales required

to achieve target net

Desserts

Beverages

X

X

=

=

PROBLEM 6-3C (Continued)

Thus, sales would have to increase by $200,000 ($1,200,000 – $1,000,000) to

achieve the target net income. This increase in sales is driven by the

increase in fixed costs. The sales of each product line would be:

Sales Mix

Percentage

X

Total Sales

Needed

=

Sales Dollars

Per Product

Appetizers

35%

X

$1,200,000

=

$ 420,000

(c)

Sales Mix

Percentage

X

Contribution

Margin Ratio

=

Weighted-Average

Contribution

Margin Ratio

Desserts

Beverages

X

X

=

=

Appetizers

30%

X

70%

=

.21

The weighted-average contribution margin ratio computed in part (a) was

43.5%. With the contribution margin on entrees falling to 10%, that average

Sales Mix

Percentage

X

Total Sales

Needed

=

Sales from

Each Product

Beverages

X

=

Appetizers

30%

X

$1,400,000

=

$ 420,000

Relative to parts (a) and (b), the total required sales for (c) would increase. It

appears that the least risky approach would be for Bart to switch to the new

Desserts

Beverages

X

X

=

=

PROBLEM 6-4C

(a)

Product

Economy

Standard

Deluxe

Selling price

$300

$500

$700

(b)

Product

Economy

Standard

Deluxe

(c) If additional machine hours become available, the additional time should

(a) To determine the break-even point in dollars we must first calculate the

contribution margin ratio for each company.

Contribution

Margin

÷

Sales

=

Contribution

Margin Ratio

Winter Company

$400,000

÷

$2,000,000

=

.20

(b)

Contribution

Margin

÷

Net

Income

=

Degree of Operating

Leverage

Winter Company

Summer Company

$400,000

$850,000

÷

÷

$200,000

$200,000

=

=

2.00

4.25

Because Summer Company relies more heavily on fixed costs, it has a

(c)

Winter Company Summer Company

Sales $2,600,000* $2,600,000

Variable costs 2,080,000** 1,495,000***

PROBLEM 6-5C

Summer Company

÷

=

Winter Company

Summer Company

÷

÷

=

=

PROBLEM 6-5C (Continued)

(d)

Winter Company Summer Company

Sales $1,400,000* $1,400,000

Variable costs 1,120,000** 805,000***

(e) In part (b) the degree of operating leverage of Summer Company was

higher than that of Winter Company, telling us that the net income of

Summer Company was more sensitive to changes in sales than that of

Winter Company. In part (c) we see that with a 30% increase in sales

PROBLEM 6-6C

(a) Reformat the income statement to CVP format.

All amount are in $000s.

Sales ………………………………………………… $80,000

Variable costs ($36,000 + $12,000) ………. 48,000

(b) If a hired workforce replaces sales agents, commissions will be reduced

to 10% of sales, or $8,000; but fixed costs will increase by $4,000.

Sales ………………………………………………… $80,000

Variable costs ($36,000 + $8,000) ………… 44,000

(c) Operating leverage = contribution margin ÷ operating income

Current situation: from part (a)

PROBLEM 6-6C (Continued)

The calculations indicate that at a sales level of $80 million, a percentage

change in sales and contribution margin will result in 3.20 times that

percentage change in operating income if Chang continues to use sales

(d) The sales level at which operating incomes will be identical is called the

point of indifference. This would be when the cost of the network of

agents (15% of sales) is exactly equal to the cost of paying employees

10% commission along with additional fixed costs of $4.0 million. None

of the other costs is relevant, because they will not change between

alternatives.

*PROBLEM 6-7C

(a) PEPPER COMPANY

Income Statement

For the Year Ended December 31, 2016

Variable Costing

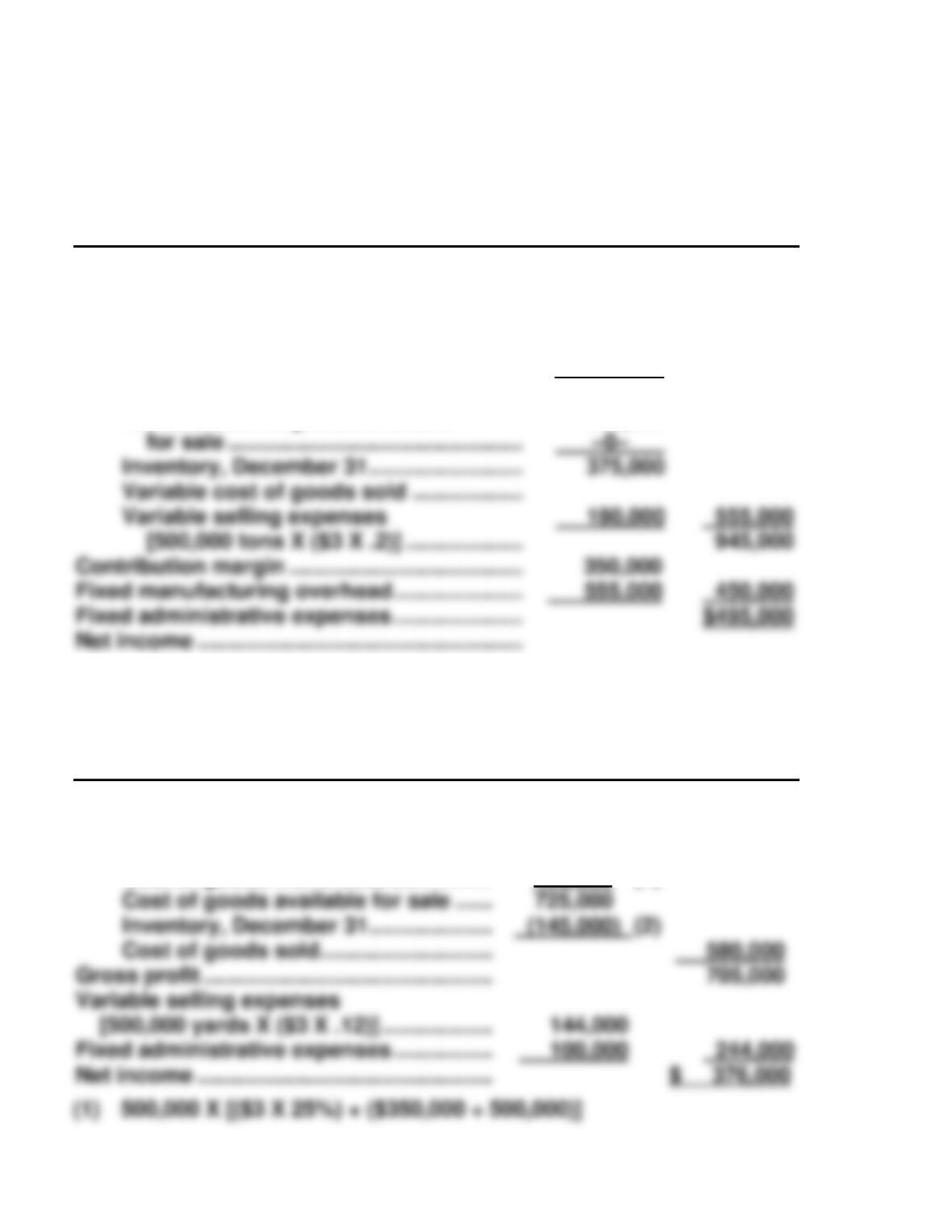

Sales (400,000 yards X $3) ………………………

Variable cost of goods sold

Inventory, January 1 ………………………..

Variable cost of goods manufactured

$ –0–

375,000

$1,200,000

*PROBLEM 6-7C (Continued)

PEPPER COMPANY

Income Statement

For the Year Ended December 31, 2017

Variable Costing

Sales (500,000 tons X $3) …………………………

Variable cost of goods sold

Inventory, January 1 …………………………

Variable cost of goods manufactured

[400,000 tons X ($3 X .25)] ……………..

Variable cost of goods available

$ 75,000

300,000

375,000

$1,500,000

(b) PEPPER COMPANY

Income Statement

For the Year Ended December 31, 2016

Absorption Costing

Sales (400,000 yards X $3) …………………..

Cost of goods sold

Inventory, January 1 …………………….

Cost of goods manufactured…………

–0–

725,000

(1)

$1,200,000

(2) 100,000 X [($3 X 25%) + ($350,000 ÷ 500,000)]

*PROBLEM 6-7C (Continued)

PEPPER COMPANY

Income Statement

For the Year Ended December 31, 2017

Absorption Costing

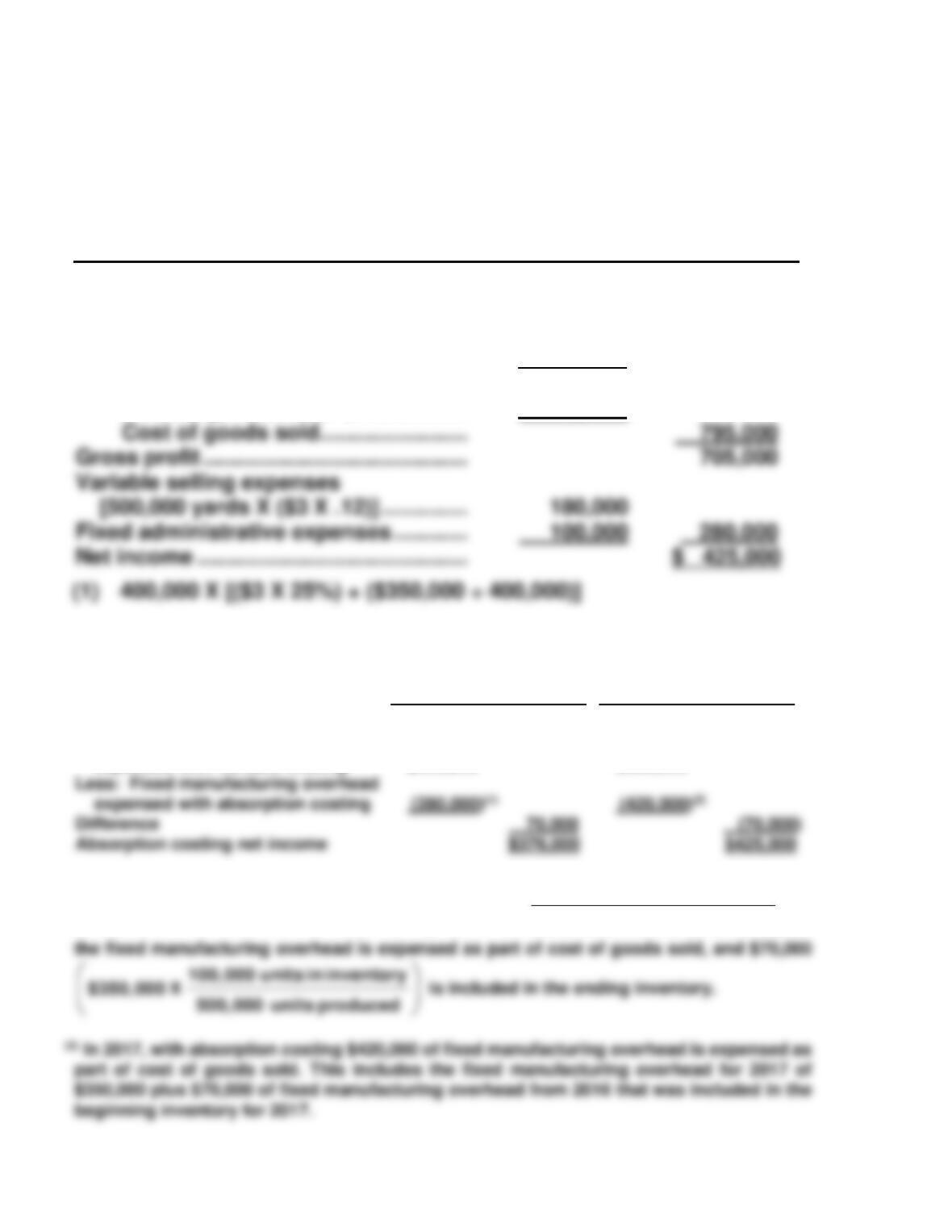

Sales (500,000 yards X $3) ……………….

Cost of goods sold

Inventory, January 1 …………………

Cost of goods manufactured………

Cost of goods available for sale …

Inventory, December 31 …………….

$ 145,000

650,000

795,000

–0–

(1)

$1,500,000

(c) The variable costing and the absorption costing income from operations

can be reconciled as follows:

2016

2017

Absorption costing net income

Variable costing net income

Fixed manufacturing overhead

expensed with variable costing

$350,000

$306,000

$350,000

$495,000

(1)In 2016, with absorption costing $280,000

400,000 units sold

$350,000 X 500,000 units manufactured

of

*PROBLEM 6-7C (Continued)

(d) Income parallels sales under variable costing as seen in the increase in

net income in 2017 when 100,000 additional units were sold. In contrast,

*PROBLEM 6-8C

(a)

SPARK DIVISION

Income Statement

For the Year Ended December 31, 2017

Absorption Costing

_______________________________________________________________

200,000 250,000

Produced Produced

Sales (200,000 units X $8) $1,600,000 $1,600,000

(b)

SPARK DIVISION

Income Statement

For the Year Ended December 31, 2017

Variable Costing

_______________________________________________________________

200,000 250,000

Produced Produced

Sales (200,000 units X $8) $1,600,000 $1,600,000

Variable cost of goods sold

(200,000 units X $3) (600,000) (600,000)

Variable selling and

administrative expenses

*PROBLEM 6-8C (Continued)

(c) If the company produces 250,000 units, but only sells 200,000 units, then

50,000 units will remain in ending inventory. Under absorption costing

these 50,000 units will each include $2.00 of fixed manufacturing cost—

a total of $100,000. However, under variable costing, fixed

(d) Variable costing has a number of advantages over absorption costing

for decision making and evaluation purposes. (1) The use of variable

costing is consistent with cost-volume-profit and incremental analysis:

(2) Net income computed under variable costing is unaffected by

changes in production levels. Note that in our example, under variable

costing the company’s net income is $388,000 no matter what the level

of production is. (3) Net income computed under variable costing is