6–1

CHAPTER 6

UNDERSTANDING THE ISSUES

1. (a) Investing activities—Purchase of Sub Company ($900,000 – $50,000) ……………. $(850,000)

(b) Investing activities—Purchase of Sub Company ($500,000 – $50,000) ……………. $(450,000)

2. Any amortizations of the $200,000 excess of cost over book value will need to be included in cash–

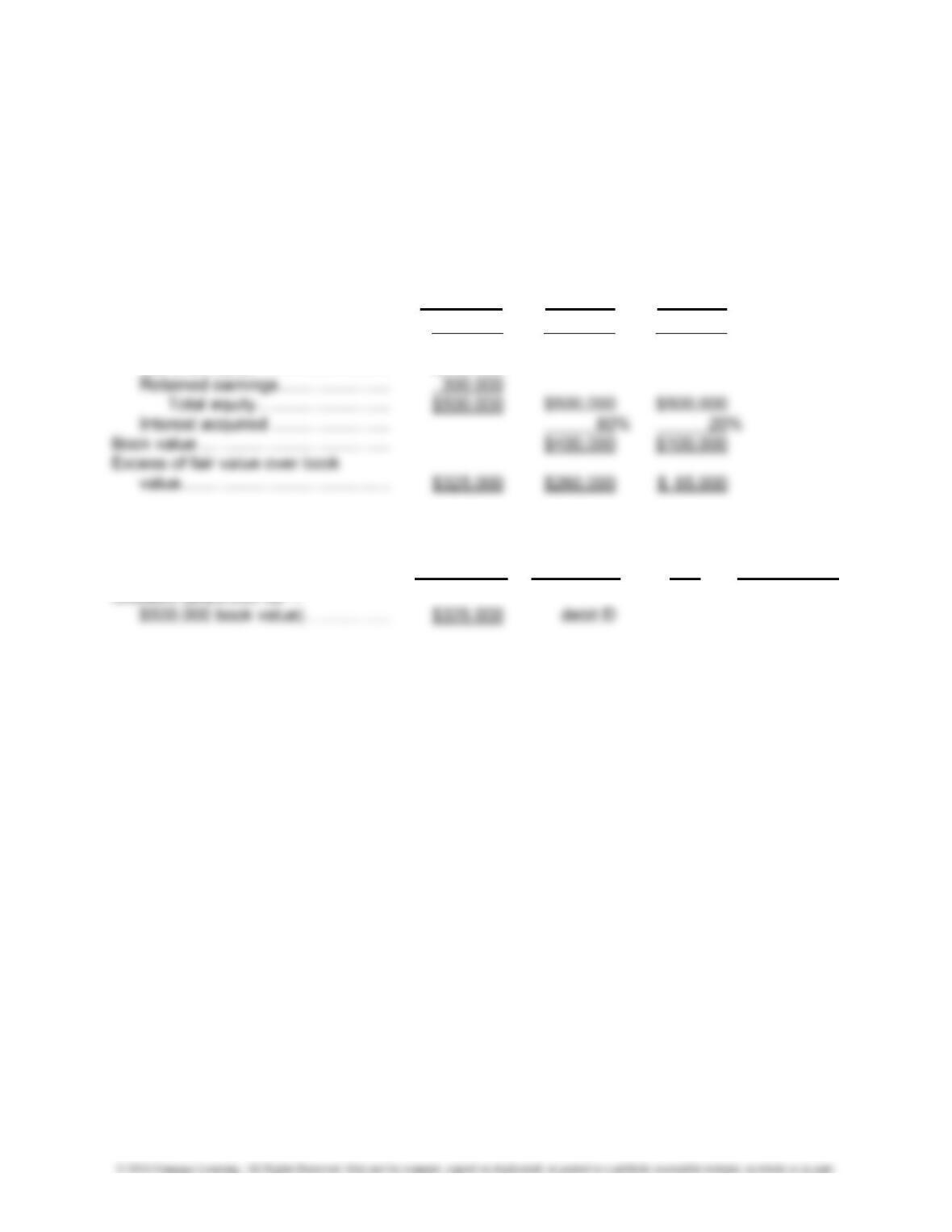

3. Determination and Distribution of Excess Schedule, Investment in Company S

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………………… $800,000 $640,000 $160,000

Less book value of interest acquired:

Total equity …………………………… 600,000 $600,000 $600,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Goodwill …………………………………….. $200,000 debit D3

(a) Investing activities—Purchase of S Company ($640,000 – $50,000) ……………….. $(590,000)

Noncash financing activities—Noncontrolling interest ……………………………………. 160,000

(b) Investing activities—Purchase of S Company ($400,000 – $50,000) ……………….. $(350,000)

Noncash financing activities—Issuance of notes payable ………………………………. 240,000

6–2

6. (a) Consolidated net income = ($100,000 + $40,000) × 70% = $98,000

Distribution to NCI = ($40,000 × 20%) × 70% = $5,600

7. (a) Taxes would not be paid on this intercompany profit. Taxes are based on consolidated income

after the elimination of the profit.

(b) Taxes will have been paid on this intercompany profit. The taxes paid become a deferred tax

6–3 Ch. 6—Exercises

EXERCISES

EXERCISE 6-1

Determination and Distribution of Excess Schedule, Investment in Roland Company

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………………… $825,000 $660,000 $165,000

Less book value of interest acquired:

Common stock ………………………. $200,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Goodwill ($825,000 fair –

Exercise 6-1, Concluded

Born Company and Subsidiary Roland Company

Consolidated Statement of Cash Flows

For Year Ended December 31, 2017

Cash flows from operating activities:

Consolidated net income ($150,000 + $10,000 NCI share) ……. $ 160,000

Adjustments to reconcile net income to net cash:

Cash flows from investing activities:

Payment for purchase of Roland Company,

net of cash acquired ……………………………………………………. (640,000)

Cash flows from financing activities:

Sale of stock (5,000 shares × $70) …………………………………….. $350,000

Dividend payments to controlling interests …………………………… (10,000)

Dividend payments to NCI ($5,000 × 20%) ………………………….. (1,000)

Schedule of noncash investing activity:

Born Company purchased 80% of the capital stock of Roland Company for $660,000. In con-

junction with the acquisition, liabilities were assumed and a noncontrolling interest created as

follows:

Adjusted value of assets acquired ($710,000 book

value + $325,000 excess) …………………………………………………. $1,035,000

Cash paid …………………………………………………………………………….. 660,000

Balance ……………………………………………………………………………….. $ 375,000

6–5 Ch. 6—Exercises

EXERCISE 6-2

Determination and Distribution of Excess Schedule, Investment in Panda Corporation

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………………… $306,250 $245,000* $ 61,250

Less book value of interest acquired:

Common stock ($10 par) …………. $150,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Equipment ………………………………….. $ 20,000 debit D1 4 $5,000

Exercise 6-2, Concluded

Duckworth Corporation and Subsidiary Panda Corporation

Consolidated Statement of Cash Flows

For Year Ended December 31, 2017

Cash flows from operating activities:

Consolidated net income …………………………………………………… $ 103,200

Adjustments to reconcile net income to net cash:

Depreciation ($92,000 + $28,000 + $5,000 of

Cash flows from investing activities:

Cash payment for purchase of Panda Corporation,

net of cash acquired ($155,000 – $30,000) ……………………. $(125,000)

Purchase of production equipment ………………………………………….. (76,000)

Net cash used in investing activities ………………………………………… $(201,000)

Cash flows from financing activities:

Decrease in long-term debt ……………………………………………….. $ (10,000)

terest was created as follows:

Adjusted value of assets acquired ($270,000

book value + $106,250 excess) …………………………………………. $376,250

Cash payment ………………………………………………………………………. 155,000

Balance ……………………………………………………………………………….. $221,250

EXERCISE 6-3

(1) None, goodwill is not amortized.

(2) The cash from shares sold to the NCI shareholders, $90,000 (1,000 shares × $90), would

(3) The bonds were held by parties outside the consolidated company. They are now retired by

(4) This is a transaction within the consolidated company, and it would have no impact on the

consolidated statement of cash flows.

EXERCISE 6-4

Marco Company:

Provision for Income Tax ………………………………………………….. 33,000

Tole Company:

Optional entry to record tax effect of subsidiary tax:

Subsidiary Investment Income …………………………………………… 26,400

Investment in Marco Company …………………………………….. 26,400

80% × $33,000 tax.

EXERCISE 6-5

Deko Company and Subsidiary Farwell Company

Consolidated Income Statement

For Year Ended December 31, 2019

Sales (less $50,000 intercompany sales) …………………………………………………. $ 370,000

Cost of goods sold ($290,000 – $50,000 intercompany sales – $8,000

beginning inventory profit + $2,400 ending inventory profit) …………………… $ (234,400)

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………………… $1,062,500 $850,000 $212,500

Less book value of interest acquired:

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Patent ………………………………………… $93,750 debit D1 10 $9,375

Consolidated

Deko

Farwell Dr. Cr. Income

Sales ……………………. $(300,000) $(120,000) (IS) $50,000 $(370,000)

Cost of goods sold …. 200,000 90,000 (IS) $50,000

(EI) 2,400 (BI) 8,000 234,400

Gain on machine ……. (5,000) (F1) 5,000 0

Exercise 6-5, Concluded

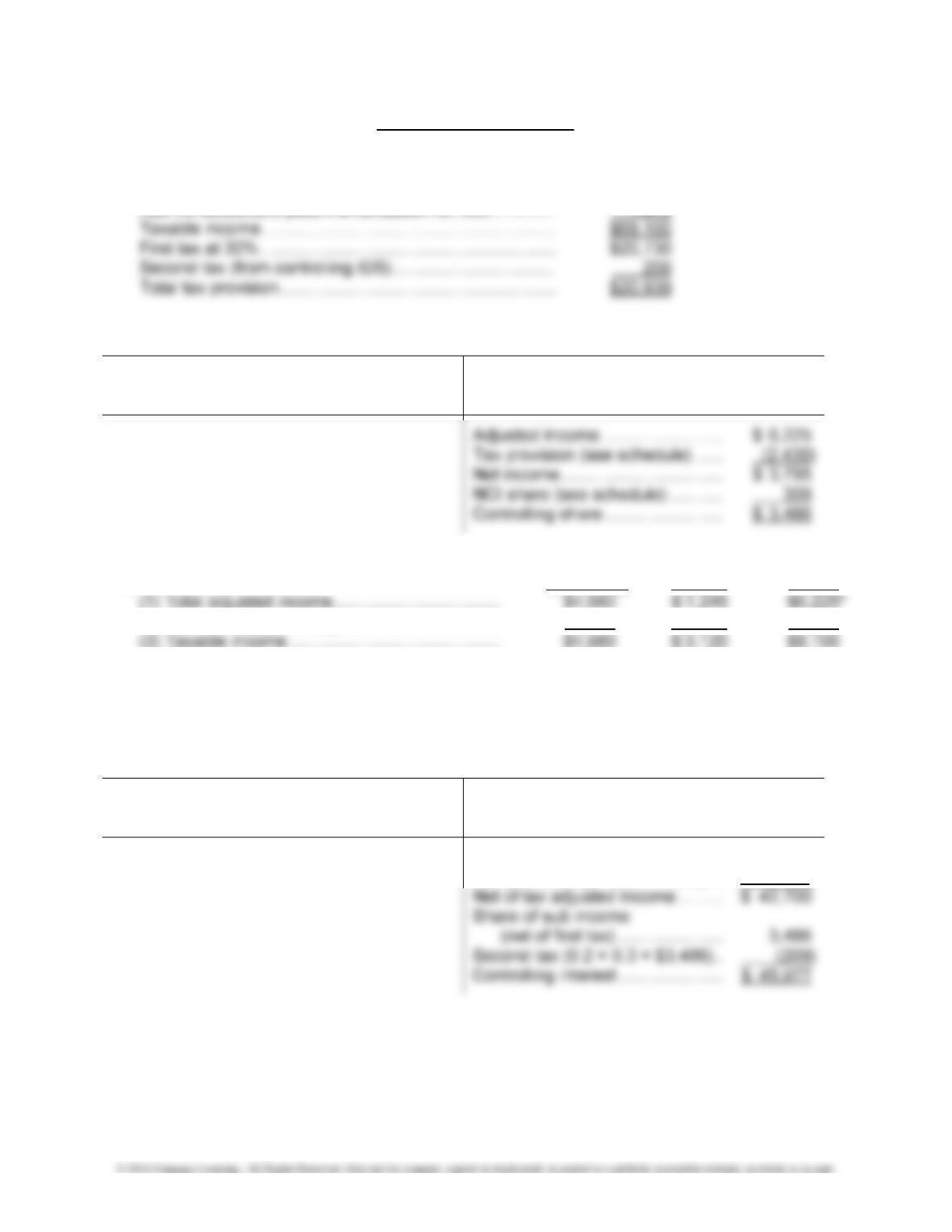

Tax provision:

Consolidated income before tax ………………………………. $67,225

Add nondeductible patent amortization on NCI

($9,375 × 20%) ………………………………………………… 1,875

Subsidiary Farwell Company Income Distribution

Ending inventory ……………………. $2,400 Internally generated income …… $10,000

Patent amortization ………………… 9,375 Beginning inventory ………………. 8,000

Subsidiary tax schedule: Controlling NCI Total

(1) Total adjusted income …………………………….. $4,980 $ 1,245 $6,225*

(3) Taxable income …………………………………….. $4,980 $ 3,120 $8,100

(5) Net of tax share of income (line 1 – line 4) … $3,486 $ 309 $3,795

*From subsidiary’s IDS.

Parent Deko Company Income Distribution

Machine gain …………………………. $5,000 Internally generated income …… $ 65,000

Gain realized ……………………….. 1,000

Adjusted income…………………… $ 61,000

EXERCISE 6-6

Dunker Company and Subsidiary Fennig Company

Consolidated Income Statement

For Year Ended December 31, 2019

Sales (less $50,000 intercompany sales) …………………………………………………. $ 370,000

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………………… $1,062,500 $850,000 $212,500

Less book value of interest acquired:

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Patent ………………………………………… $93,750 debit D1 10 $9,375

Consolidated

Dunker

Fennig Dr. Cr. Income

Sales ……………………. $(300,000) $(120,000) (IS) $50,000 $(370,000)

Cost of goods sold …. 200,000 90,000 (IS) $50,000

(EI) 2,400 (BI) 8,000 234,400

6–11 Ch. 6—Exercises

Exercise 6-6, Concluded

Tax provision:

Consolidated income before tax ………………………………. $67,225

Add nondeductible patent amortization on NCI ………….. 1,875

Subsidiary Fennig Company Income Distribution

Ending inventory ……………………. $2,400 Internally generated income …….. $10,000

Patent amortization ………………… 9,375 Beginning inventory ………………… 8,000

Subsidiary tax schedule: Controlling NCI Total

(2) NCI share of asset adjustments ……………….. 1,875 1,875

(4) Tax (30% of taxable income) …………………… $1,494 $ 936 $2,430

(5) Net of tax share of income (line 1 – line 4) … $3,486 $ 309 $3,795

*From subsidiary’s IDS

Parent Dunker Company Income Distribution

Machine gain …………………………. $5,000 Internally generated income …….. $ 65,000

Gain realized …………………………. 1,000

Adjusted income…………………….. $ 61,000

Tax provision ($61,000 × 30%) … (18,300)

EXERCISE 6-7

Adjustment to January 1, 2017, retained earnings:

Machine depreciation:

Retained Earnings—Coors (1½ yrs. × $5,000 × 60%) ……… 4,500

Retained Earnings—Vespa (1½ yrs. × $5,000 × 40%) …….. 3,000

Accumulated Depreciation—Equipment ………………………. 7,500

*Increase in Deferred Tax Assets:

Total

Controlling NCI

Gain on machine (net) ($4,000 × 30%) ………………………………. $1,200 $ 720 $480

Secondary tax ($4,000 × 70% × 60% × 30% × 20%)** …………. 101 101

Equipment depreciation ($4,500 parent share × 30%) ………….. 1,350 1,350

Total …………………………………………………………………………. $2,651 $2,171 $480

**100% – 80% dividend exclusion

Adjustments to income:

Sales ……………………………………………………………………………… 15,000

Cost of Goods Sold …………………………………………………….. 15,000

Tax:

Deferred Tax Asset** ……………………………………………………….. 725

Provision for Tax ………………………………………………………… 725

**Increase in Deferred Tax Assets:

Total

Controlling NCI

Machine gain realized (30% × $1,000) …………………………….. $(300) $(180) $(120)

6–13 Ch. 6—Problems

PROBLEMS

PROBLEM 6-1

Determination and Distribution of Excess Schedule, Investment in Marion Company

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………………… $850,000 $680,000 $170,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Equipment ………………………………….. $ 50,000 debit D1 5 $10,000

Problem 6-1, Concluded

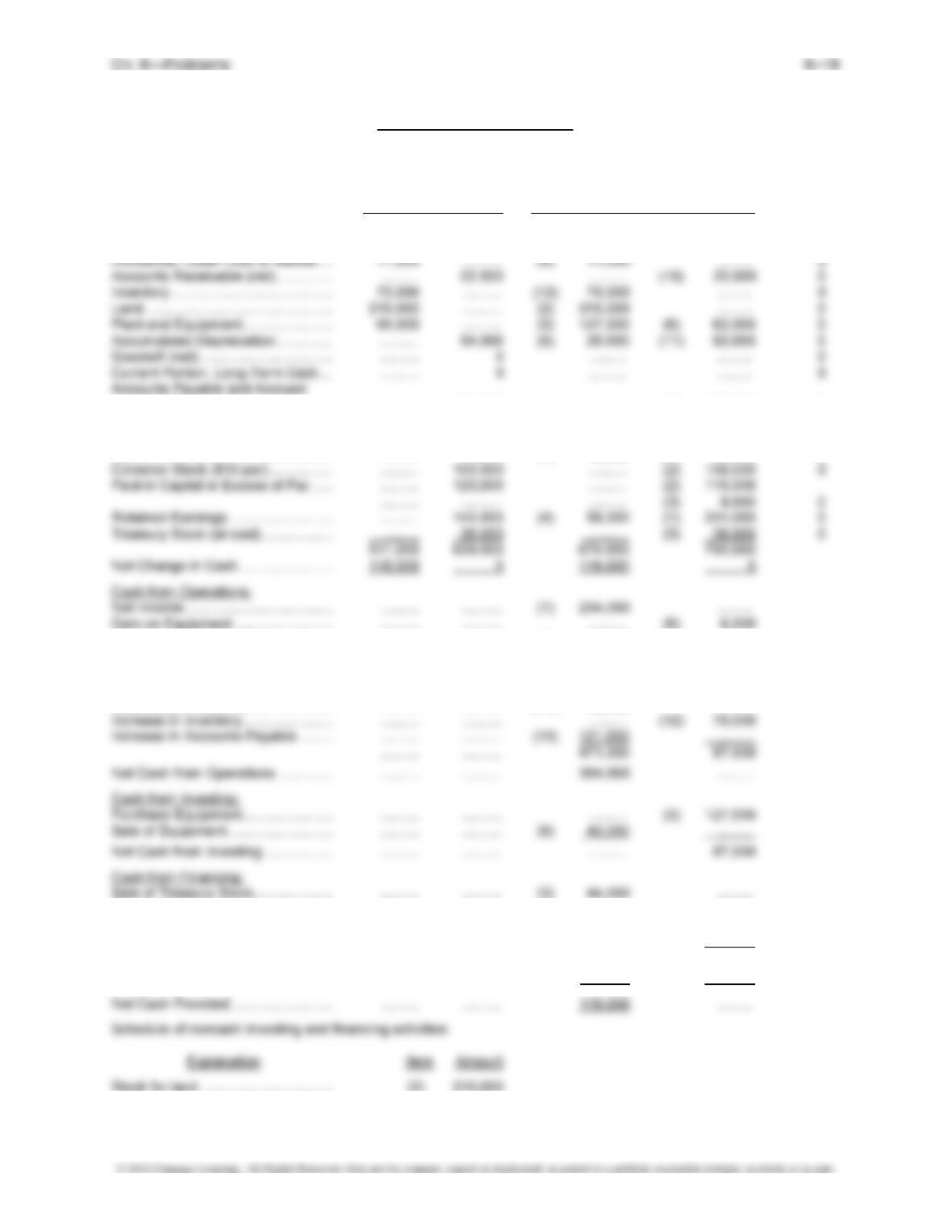

Lange Company and Subsidiary Marion Company

Consolidated Statement of Cash Flows

For Year Ended December 31, 2016

Cash flows from operating activities:

Consolidated net income ($262,000 + $15,000) …………………… $ 277,000

Adjustments to reconcile net income to net cash:

Depreciation expense ($1,292,000 – $1,086,000) …………… $ 206,000

Increase in inventory …………………………………………………… (40,000)

Net cash provided by operating activities ……………………….. $ 411,500

Cash flows from investing activities:

Purchase of building …………………………………………………………. $(350,000)

Purchase of equipment …………………………………………………….. (70,000)

Investment in Charles ………………………………………………………. (230,000)

Net cash used in investing activities ……………………………… (650,000)

mining funds provided by net income.

30% of reported Charles income (30% × $80,000) …………………… $24,000

Less amortization of excess {[$230,000 –

($700,000 × 30%)]/10 years} …………………………………………….. 2,000

Equity income ……………………………………………………………………… $22,000

6–15 Ch. 6—Problems

PROBLEM 6-2

Determination and Distribution of Excess Schedule, Investment in Rush Corporation

Company Parent NCI

Implied Price Value

Fair Value (90%) (10%)

Fair value of subsidiary ………………… $550,000 $495,000 $ 55,000

Less book value of interest acquired:

Common stock ($10 par) …………. $150,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Equipment ………………………………….. $ 20,000 debit D1 5 $4,000

Problem 6-2, Concluded

Billing Enterprises and Subsidiary Rush Corporation

Consolidated Statement of Cash Flows

For Year Ended December 31, 2015

Cash flows from operating activities:

Consolidated net income …………………………………………………… $ 92,300

Adjustments to reconcile net income to net cash:

Depreciation expense (includes amortization

of excess on equipment) ………………………………………… $ 72,400*

Cash flows from investing activities:

Payment for purchase of Rush Corporation, $95,000 cash net

of $60,000 cash acquired …………………………………………….. (35,000)

Cash flows from financing activities:

Sale of bonds ($500,000 increase – $400,000

issued to Rush) ………………………………………………………….. $ 100,000

Dividends paid to noncontrolling shareholders …………………….. (1,000)

Schedule of noncash investing activity:

Billing Enterprises acquired 90% of the capital stock of Rush Corporation for $495,000. In con-

junction with the acquisition, liabilities were assumed and a noncontrolling interest created as

follows:

Adjusted value of assets acquired ($615,000

book value + $100,000 excess) …………………………………………. $715,000

Cash paid …………………………………………………………………………….. 95,000

Balance ……………………………………………………………………………….. $620,000

PROBLEM 6-3

Bush, Inc., and Subsidiary Dorr Corporation

Consolidated Statement of Cash Flows

For Year Ended December 31, 2016

Cash flows from operating activities:

Consolidated net income …………………………………………………… $ 234,000

Adjustments to reconcile net income to net cash:

Gain on sale of equipment …………………………………………… $ (6,000)

Depreciation expense …………………………………………………. 82,000

Reduction of negative allowance for marketable securities . (11,000)

Cash flows from investing activities:

Purchase of equipment …………………………………………………….. $(127,000)

Sale of equipment ……………………………………………………………. 40,000

Net cash used in investing activities ……………………………… (87,000)

Cash flows from financing activities:

Sale of treasury stock ……………………………………………………….. $ 44,000

Dividend payments to controlling interests …………………………… (58,000)

Problem 6-3, Concluded

Bush, Inc. and Subsidiary Dorr Corporation

Worksheet for Analysis of Cash Flows: Indirect Method

For Year Ended December 31, 2016

Account Change

Explanations

Debit Credit Debit Credit Balance

Marketable Equity Securities ……….. 0 ………. ………. ……… 0

Liabilities ……………………………. ………. 121,000 ………. (13) 121,000 0

Note Payable, Long-Term …………… 150,000 ………. (14) 150,000 ……… 0

Deferred Income Taxes ………………. ………. 12,000 ………. (8) 12,000 0

NCI ………………………………………….. ………. 18,000 (7) 15,000 (1) 33,000 0

Increase in Deferred Tax …………….. ………. ………. (8) 12,000 ………

Decrease in Allowance—Short-Term

Marketable Securities ……………… ………. ………. ………. (9) 11,000

Decrease in Accounts Receivable … ………. ………. (10) 22,000 ………

Depreciation Expense ………………… ………. ………. (11) 82,000 ………

Pay Dividend …………………………….. ………. ………. ………. (4) 58,000

Subsidiary Dividend …………………… ………. ………. ………. (7) 15,000

Payment on Long-Term Note Payable ………. ………. ………. (14) 150,000

………. ………. ………. 223,000

Net Cash from Financing ……………. ………. ………. ……….

179,000

6–19 Ch. 6—Problems

PROBLEM 6-4

Subsidiary calculations:

BEPS = 12,000

dividends preferred $4,000 $56,000 = $4.33

DEPS = 12.4$=

1,600 + 12,000

dividends preferred $4,000 + $52,000

a

b12,000 Sunny shares × 80% interest

DEPS = d

c

245 20,000

DEPS)Sunny $4.12 (10,560 dividends preferred $500 $55,000

+

×+

= 245 20,000

$43,507 $500 $55,000

+

+

PROBLEM 6-5

Determination and Distribution of Excess Schedule, Investment in Mercer Company

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………………… $375,000 $300,000 $ 75,000

Less book value of interest acquired:

Common stock ($2 par) …………… $ 20,000

Paid-in capital in excess of par … 50,000

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Equipment ………………………………….. $100,000 debit D1 8 $12,500

Eliminations Consolidated

and Income

Dawn

Mercer Adjustments Statement

Sales ………………………………. $(1,000,000) $(600,000) (IS) $50,000 $(1,550,000)

Less cost of goods sold …….. 800,000 375,000 (IS) (50,000)

Income before tax …………….. $ (154,495)

Less provision for tax ……….. 47,098

Consolidated net income …… $ (107,397)

Less NCI …………………………. 3,083