PROBLEM 6-2C

(a)

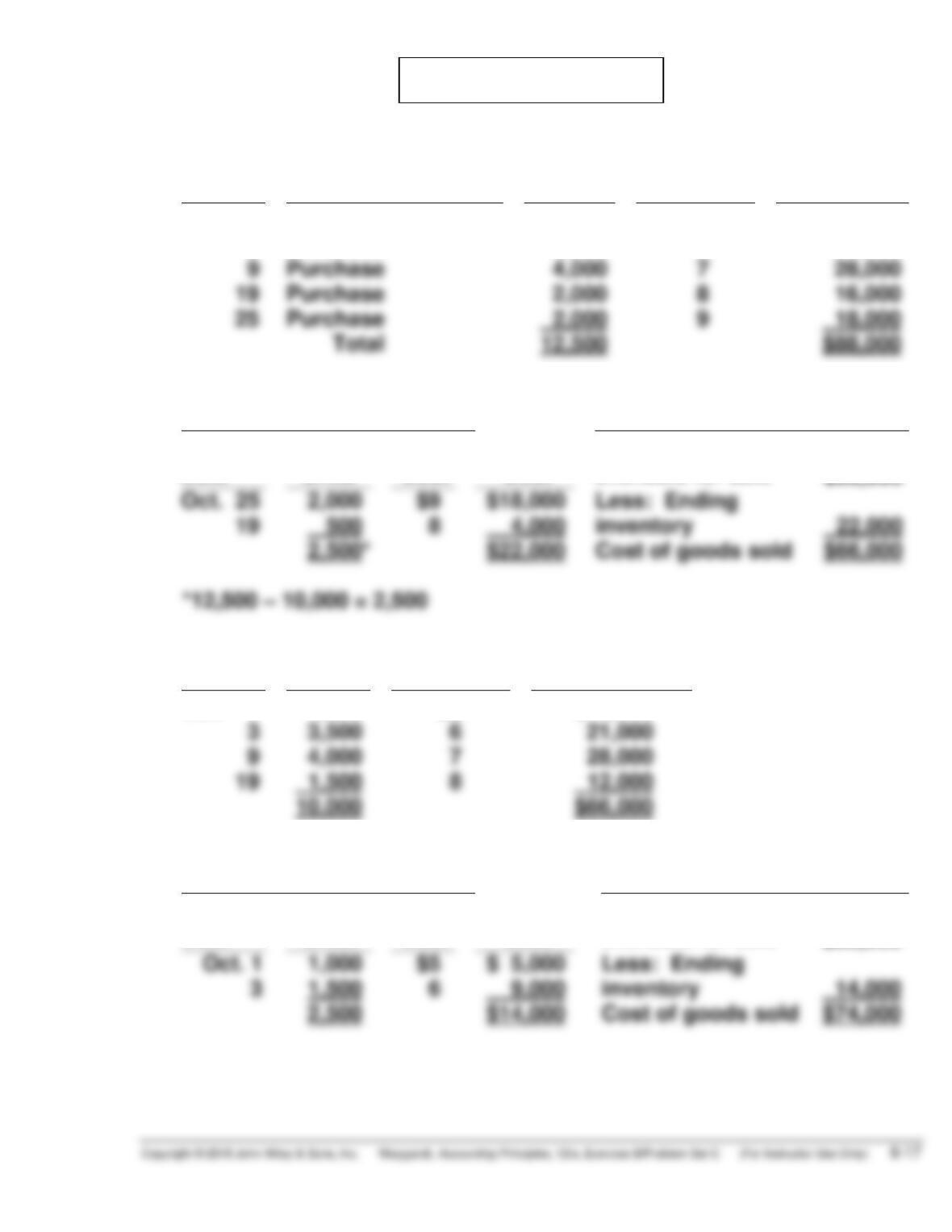

COST OF GOODS AVAILABLE FOR SALE

Date

Explanation

Units

Unit Cost

Total Cost

Oct. 1

Beginning Inventory

1,000

$5

$ 5,000

3

Purchase

3,500

6

21,000

9

Purchase

4,000

7

28,000

Purchase

2,000

Purchase

9

(b)

FIFO

(1)

Ending Inventory

(2)

Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

Cost of goods

available for sale

$88,000

2,000

500

8

4,000

2,500*

$22,000

Cost of goods sold

$66,000

Proof of Cost of Goods Sold

Date

Units

Unit Cost

Total Cost

Oct. 1

1,000

$5

$ 5,000

3

3,500

6

21,000

9

4,000

7

8

10,000

$66,000

LIFO

(1)

Ending Inventory

(2)

Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

Cost of goods

available for sale

$88,000

1,000

$ 5,000

3

1,500

6

9,000

2,500

$14,000

Cost of goods sold

PROBLEM 6-2C (Continued)

Proof of Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

Oct. 25

2,000

$9

$18,000

19

2,000

8

16,000

9

4,000

7

28,000

3

6

12,000

10,000

$74,000

AVERAGE COST

(1)

Ending Inventory

(2)

Cost of Goods Sold

$88,000 ÷ 12,500 = $7.04

Cost of goods available

for sale

$88,000

Total Cost

Cost of goods sold

(c) 1. FIFO results in the highest inventory amount for the balance sheet,

$22,000.

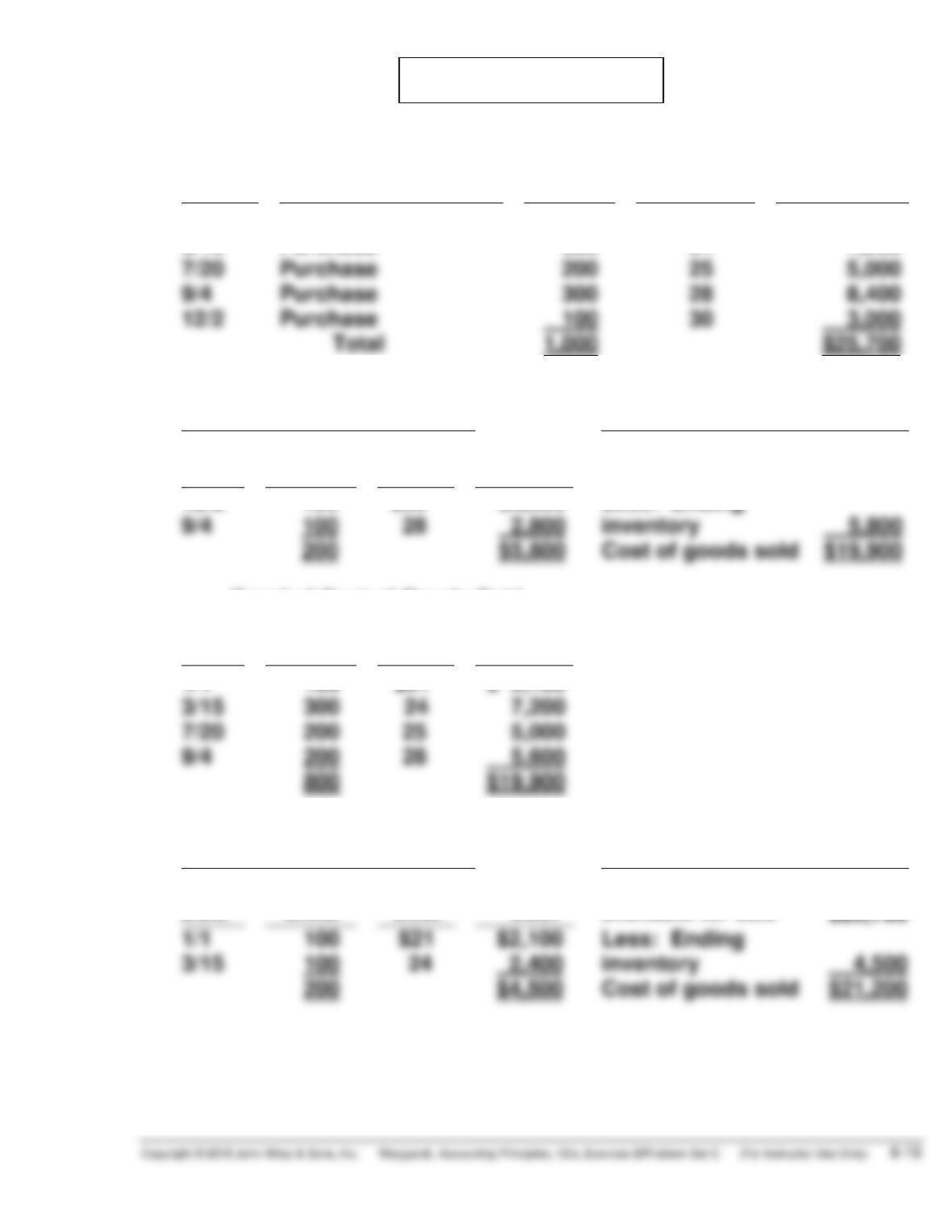

PROBLEM 6-3C

(a)

COST OF GOODS AVAILABLE FOR SALE

Date

Explanation

Units

Unit Cost

Total Cost

1/1

Beginning Inventory

100

$21

$ 2,100

3/15

Purchase

300

24

7,200

7/20

Purchase

200

25

5,000

9/4

Purchase

300

12/2

Purchase

30

(b)

FIFO

(1)

Ending Inventory

(2)

Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

Cost of goods

available for sale

$25,700

12/2

100

$30

$3,000

9/4

100

Cost of goods sold

$19,900

Less: Ending

Proof of Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

1/1

100

$21

$ 2,100

3/15

300

24

7,200

7/20

200

9/4

200

800

(c)

LIFO

(1)

Ending Inventory

(2)

Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

Cost of goods

available for sale

1/1

100

$2,100

Less: Ending

3/15

100

200

Cost of goods sold

PROBLEM 6-3C (Continued)

Proof of Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

12/2

100

$30

$ 3,000

9/4

7/20

3/15

200

4,800

$21,200

AVERAGE COST

(1)

Ending Inventory

(2)

Cost of Goods Sold

$25,700 ÷ 1,000 = $25.70

Cost of goods available

for sale

$25,700

Cost of goods sold

$20,560

Proof of Cost of Goods Sold

800 units X $25.70 = $20,560

(c) 1. FIFO results in the highest inventory amount, $5,800, as shown in

(b) above.

PROBLEM 6-4C

(a) MATHENY INC.

Condensed Income Statements

For the Year Ended December 31, 2017

FIFO

LIFO

Sales ……………………………………………….. $865,000 $865,000

Cost of goods sold

Beginning inventory …………………… 22,800 22,800

Cost of goods purchased …………… 578,500 578,500

Cost of goods available for sale ….. 601,300 601,300

(b) 1. The FIFO method produces the most meaningful inventory amount

for the balance sheet because the units are costed at the most

recent purchase prices.

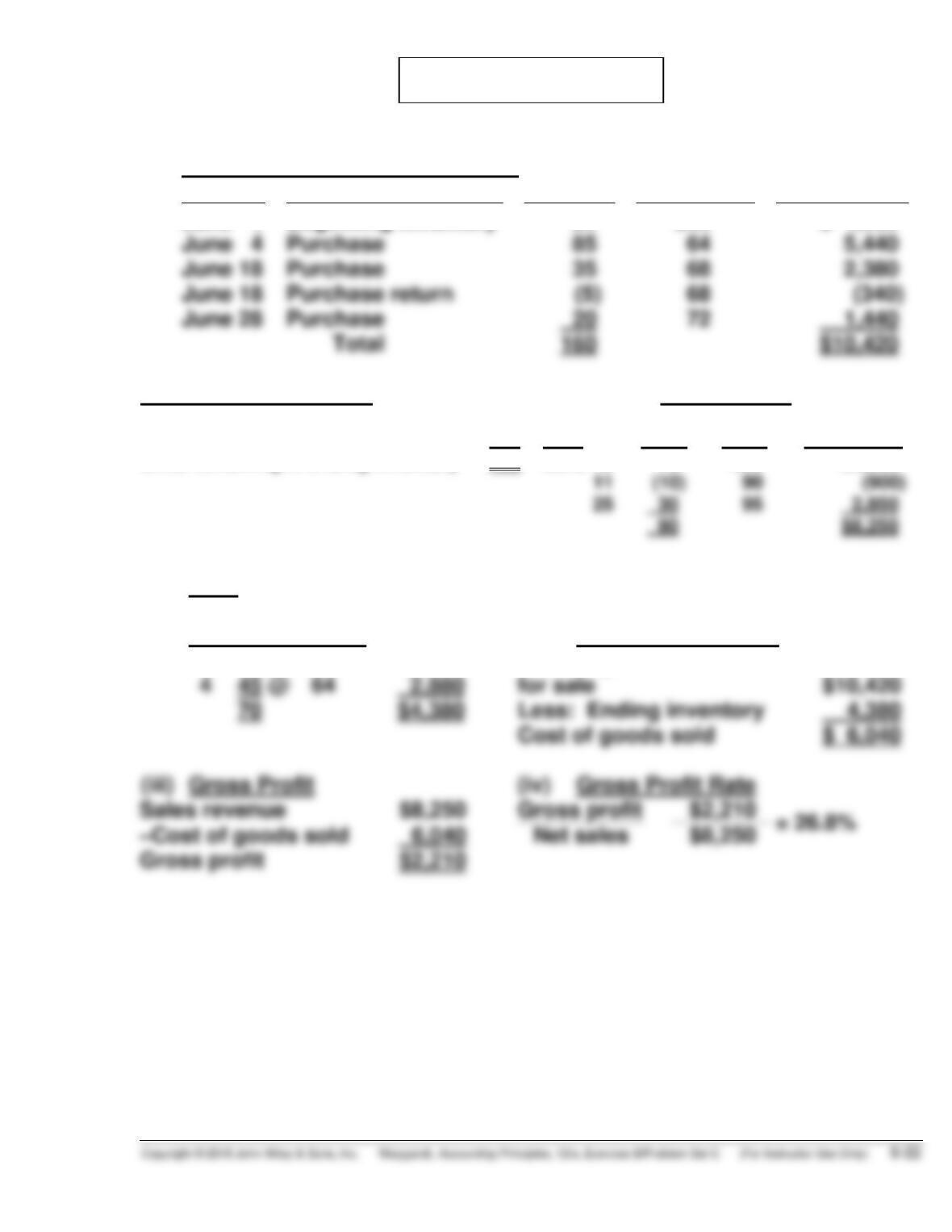

PROBLEM 6-5C

(a)

Cost of Goods Available for Sale

Date

Explanation

Units

Unit Cost

Total Cost

June 1

Beginning Inventory

25

$60

$ 1,500

June 4

Purchase

85

64

5,440

June 18

Purchase

35

68

June 18

Purchase return

(340)

June 28

Purchase

72

1,440

Ending Inventory in Units:

Sales Revenue

Units available for sale

160

Unit

—Sales (70 – 10 + 30)

90

Date

Units

Price

Total Sales

Units remaining in ending inventory

70

June 10

70

$90

$6,300

(10)

2,850

(1)

LIFO

(i)

Ending Inventory

(ii)

Cost of Goods Sold

Less: Ending inventory

Cost of goods sold

(iii)

Gross Profit

(iv)

Gross Profit Rate

Sales revenue

Gross profit

$8,250

Gross profit

June 1

25 @ $60

$1,500

Cost of goods available

PROBLEM 6-5C (Continued)

(2)

FIFO

(i)

Ending Inventory

(ii)

Cost of Goods Sold

June 28

18

20 @ $72

30 @ $68

$1,440

2,040

Cost of goods available

for sale

$10,420

Less: Ending inventory

Cost of goods sold

(iii)

Gross Profit

(iv)

Gross Profit Rate

Sales revenue

$8,250

Gross profit

$2,590

$8,250

Gross profit

$2,590

(3)

Average-Cost

Weighted-average cost per unit:

Cost of goods available for sale

Units available for sale

(i)

Ending Inventory

(ii)

Cost of Goods Sold

70 units @$65.125

4,558.75

Cost of goods available

for sale

$10,420.00

Less: Ending inventory

4,558.75

Cost of goods sold

$ 5,861.25

(iii)

Gross Profit

(iv)

Gross Profit Rate

Sales revenue

$8,250.00

Gross profit

$2,388.75

Net sales

$8,250.00

Gross profit

(b) In this period of rising prices, LIFO gives the highest cost of goods

PROBLEM 6-6C

(a) WAINWRIGHT INC.

Income Statement (partial)

For the Year Ended March 31, 2017

Specific Identification

FIFO

LIFO

Sales revenuea

$4,230

$4,230

$4,230

Beginning inventory

600

600

600

Cost of goods sold

Gross profit

(a) (1,800 @ $.60) + (4,500 @ $.70)

Beginning inventory (1,500 litres – 900 – 400)

200 @ $.40

$ 80

March 3 purchase (2,000 litres – 900 – 500)

600 @ $.45

270

March 10 purchase (3,500 litres – 2,600)

900 @ $.49

March 20 purchase (2,000 litres – 1,000)

1,000 @ $.55

550

FIFO ending inventory consists of:

March 20 purchase

$1,100

March 10 purchase

343

LIFO ending inventory consists of:

Beginning inventory

1,500 @ $.40

$ 600

March 3 purchase

1,200 @ $.45

540

(b) Companies can choose a cost flow method that produces the highest

PROBLEM 6-7C

(a) MALONE CO.

Condensed Income Statement

For the Year Ended December 31, 2017

FIFO

LIFO

Sales ……………………………………………….. $630,000 $630,000

Cost of goods sold

Beginning inventory ………………….. 37,000 37,000

Cost of goods purchased …………… 479,000 479,000

(b) Answers to questions:

1. The FIFO method produces the most meaningful inventory amount

for the balance sheet because the units are costed at the most

recent purchase prices.

2. The LIFO method produces the most meaningful net income

because the costs of the most recent purchases are matched

against sales.

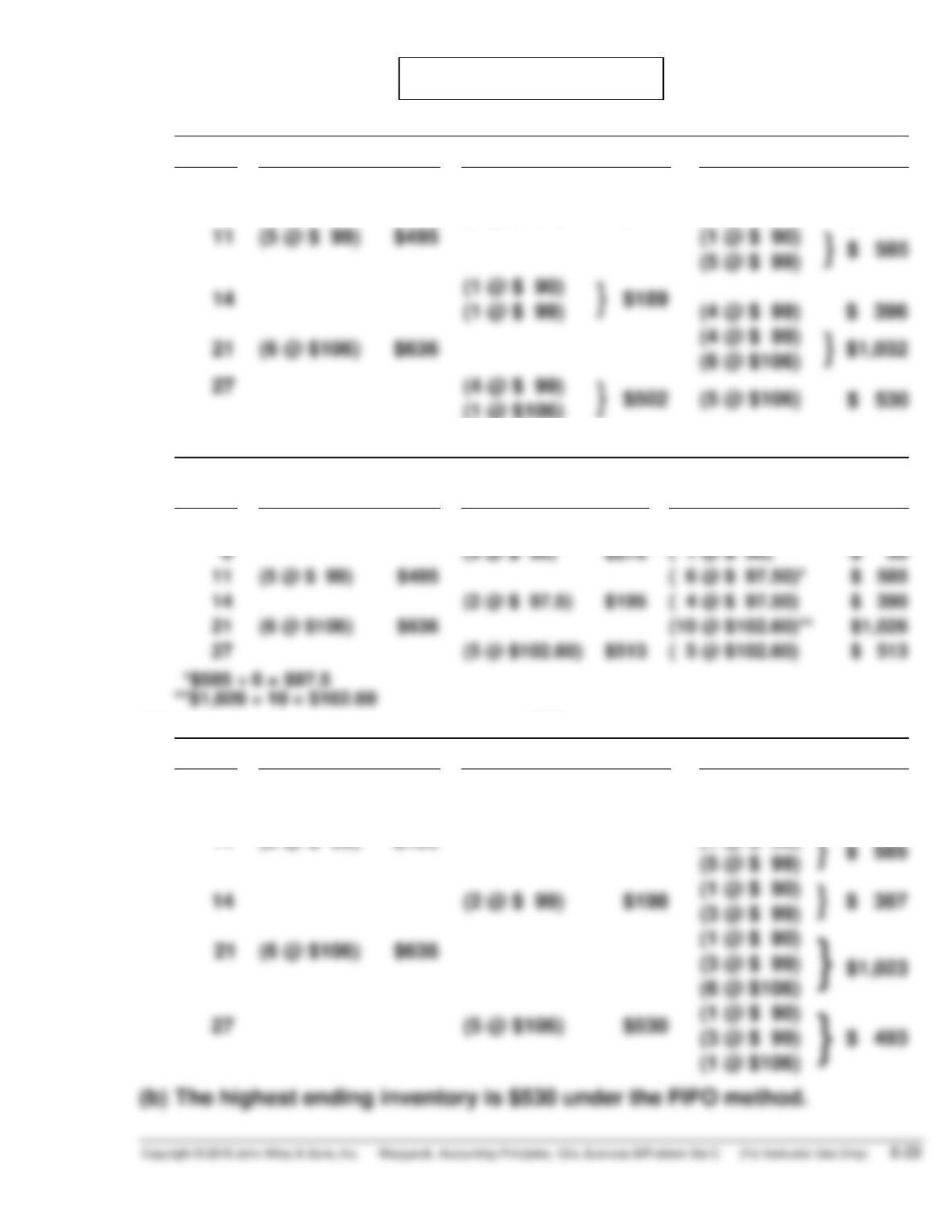

*PROBLEM 6-8C

(a) Cost of goods available for sale:

Inventory

50 units @ $12

$ 600

Purchases:

January 5

100 units @ $14

1,400

January 15

30 units @ $18

January 16 (return)

January 25

10 units @ $20

200

185 units

$2,650

Sales:

January 8

80 units @ $25

$2,000

January 10 (return)

(10 units @ $25)

January 20

65 units @ $25

135 units

$3,375

(1)

LIFO

Date

Purchases

Cost of Goods Sold

Balance

January 1

( 50 @ $12)

$ 600

January 5

(100 @ $14) $1,400

( 50 @ $12)

}

$2,000

(100 @ $14)

January 8

( 80 @ $14) $1,120

( 50 @ $12)

$ 880

( 20 @ $14)

January 10

( 50 @ $12)

$1,020

( 30 @ $14)

January 15

( 30 @ $18) $ 540

( 50 @ $12)

$1,560

( 30 @ $14)

}

( 30 @ $18)

January 16

( –5 @ $18) ($ 90)

( 50 @ $12)

}

$1,470

( 30 @ $14)

( 25 @ $18)

( 25 @ $18)

January 20

( 30 @ $14)

( 40 @ $12)

$ 480

( 10 @ $12)

January 25

( 10 @ $20) $ 200

( 40 @ $12)

$ 680

( 10 @ $20)

*PROBLEM 6-8C (Continued)

(2)

FIFO

Date

Purchases

Cost of Goods Sold

Balance

January 1

( 50 @ $12)

$ 600

January 5

(100 @ $14) $1,400

( 50 @ $12)

}

$2,000

(100 @ $14)

January 8

$1,020

$ 980

( 30 @ $14)

( 80 @ $14)

$1,120

January 15

( 30 @ $18) $ 540

( 80 @ $14)

}

$1,660

( 30 @ $18)

( 80 @ $14)

( 25 @ $18)

January 20

(65 @ $14)

$ 910

( 15 @ $14)

( 25 @ $18)

}

$ 660

( 10 @ $20)

( 15 @ $14)

(3)

Moving-Average

Date

Purchases

Cost of Goods Sold

Balance

January 1

( 50 @ $12)

$ 600

January 5

(100 @ $14) $1,400

(150 @ $13.333)a

$2,000

January 8

( 80 @ $13.333)

$1,067*

( 70 @ $13.333)

$ 933

January 10

(–10 @ $13.333)

($ 133)*

( 80 @ $13.333)

$1,066

January 15

( 30 @ $18) $ 540

$1,606

January 16

( –5 @ $18) ($ 90)

$1,516

January 20

( 65 @ $14.438)

$ 938*

$ 578

January 25

( 10 @ $20) $ 200

( 50 @ $15.56)

$ 778

*rounded

a$2,000 ÷ 150 = $13.333 c$1,516 ÷ 105 = $14.438

b$1,606 ÷ 110 = $14.60 d$578 ÷ 40 = $14.438

*PROBLEM 6-8C (Continued)

(b)

Gross profit:

LIFO

FIFO

Moving-Average

Sales

$3,375

$3,375

$3,375

Gross profit

$1,405

$1,585

$1,503

In a period of rising costs, the LIFO cost flow assumption results in the

highest cost of goods sold and lowest gross profit. FIFO gives the lowest

cost of goods sold and highest gross profit. The moving-average-cost flow

assumption results in amounts between the other two.

*PROBLEM 6-9C

(1)

FIFO

Date

Purchases

Cost of Goods Sold

Balance

July 1

(4 @ $ 90)

$360

(4 @ $ 90)

$ 360

6

(3 @ $ 90)

$270

(1 @ $ 90)

$ 90

11

(5 @ $ 99)

$495

(1 @ $ 90)

}

$ 585

(5 @ $ 99)

(1 @ $ 90)

(1 @ $ 99)

(4 @ $ 99)

$ 396

(4 @ $ 99)

(6 @ $106)

27

(2)

AVERAGE-COST

Date

Purchases

Cost of

Goods Sold

Balance

July 1

(4 @ $ 90)

$360

( 4 @ $ 90)

$ 360

6

(3 @ $ 90)

$270

( 1 @ $ 90)

$ 90

(5 @ $ 99)

$495

( 6 @ $ 97.50)*

$ 585

(2 @ $ 97.5)

( 4 @ $ 97.50)

$ 390

(6 @ $106)

(10 @ $102.60)**

$1,026

(5 @ $102.60)

( 5 @ $102.60)

$ 513

(3)

LIFO

Date

Purchases

Cost of Goods Sold

Balance

July 1

(4 @ $ 90)

$360

(4 @ $ 90)

$ 360

6

(3 @ $ 90)

$270

(1 @ $ 90)

$ 90

11

(5 @ $ 99)

$495

(1 @ $ 90)

}

$ 585

(5 @ $ 99)

(1 @ $ 90)

(3 @ $ 99)

(1 @ $ 90)

(3 @ $ 99)

(6 @ $106)

(1 @ $ 90)

(3 @ $ 99)

(1 @ $106)

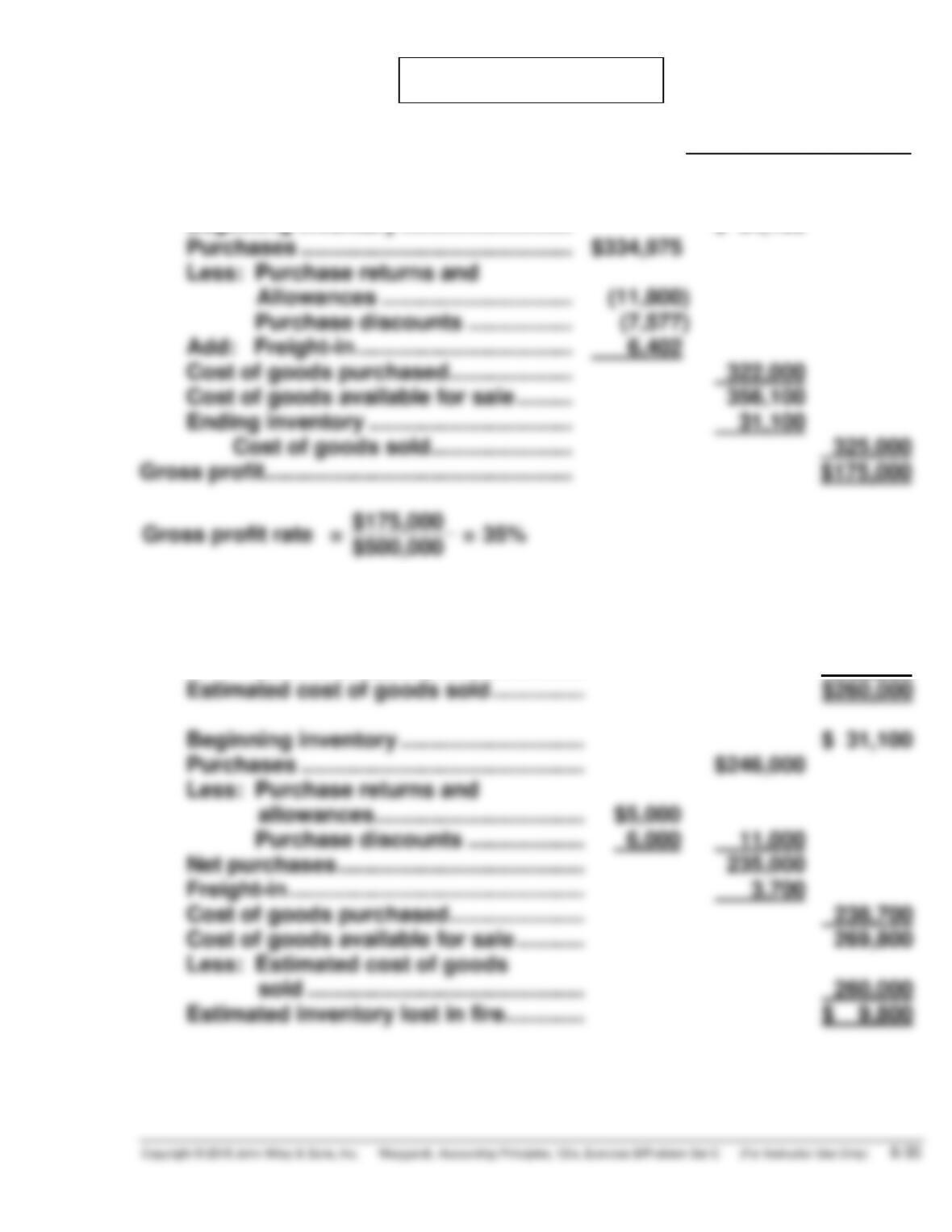

*PROBLEM 6-10C

(a)

November

Net sales ……………………………………………… $500,000

Cost of goods sold

Beginning inventory ………………………. $ 34,100

Purchases …………………………………….. $334,975

Less: Purchase returns and

(b) Net sales ………………………………………… $400,000

Less: Estimated gross profit

(35% X $400,000) …………………… 140,000

Estimated cost of goods sold …………… $260,000

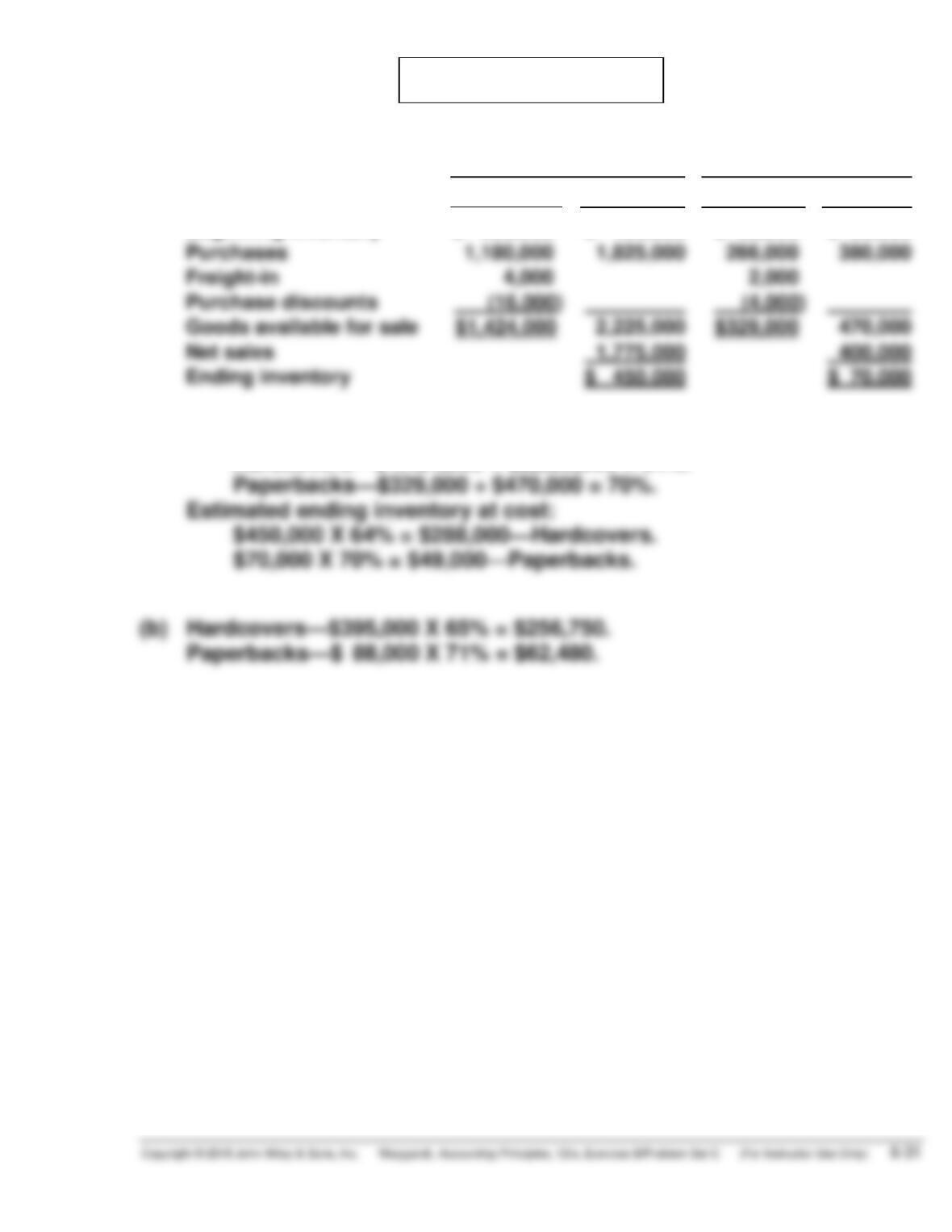

*PROBLEM 6-11C

(a)

Hardcovers

Paperbacks

Cost

Retail

Cost

Retail

Beginning inventory

$ 256,000

$ 400,000

$ 65,000

$ 90,000

Purchases

1,180,000

1,825,000

266,000

380,000

Purchase discounts

Goods available for sale

2,225,000

470,000

Net sales

$ 450,000

$ 70,000

Cost-to-retail ratio:

Hardcovers—$1,424,000 ÷ $2,225,000 = 64%.

Paperbacks—$329,000 ÷ $470,000 = 70%.