BYP 6-2 COMPARATIVE ANALYSIS PROBLEM

(a) (1) Inventory turnover:

PepsiCo:

$31,243 ÷

$3,581 + 3,409

= 8.94 times

2

$3,264 + 3,277

(2) Days in inventory:

(b) PepsiCo’s turnover of 8.94 times is approximately 59% higher than Coca–

BYP 6-3 COMPARATIVE ANALYSIS PROBLEM

(a) (1) Inventory turnover:

Amazon:

$54,181 ÷

$6,031 + $7,411

= 8.06 times

2

(2) Days in inventory:

BYP 6-4 REAL-WORLD FOCUS

The following responses are based on the 2013 annual report:

(a) $1,476,000,000, as of July 27, 2013.

BYP 6-5 DECISION MAKING ACROSS THE ORGANIZATION

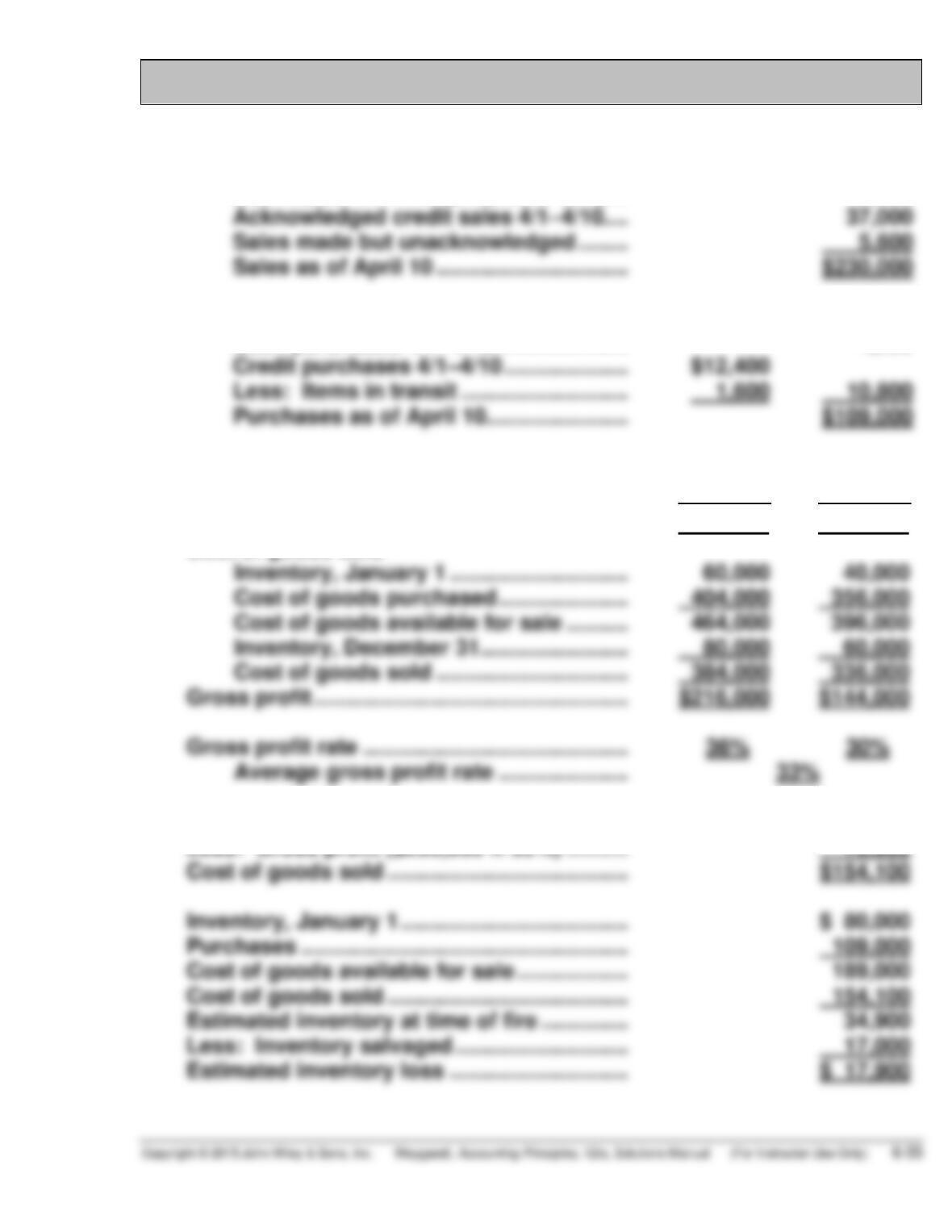

(a) (1) Sales January 1–March 31 ……………….. $180,000

Cash sales 4/1–4/10 ($18,500 X 40%) … 7,400

(2) Purchases January 1–March 31 ……….. $ 94,000

Cash purchases 4/1–4/10 …………………. 4,200

*(b)

2016

2015

Net sales ……………………………………………….. $600,000 $480,000

Cost of goods sold

Inventory, January 1 ……………………….. 60,000 40,000

Cost of goods purchased ………………… 404,000 356,000

Cost of goods available for sale ………. 464,000 396,000

*(c) Sales …………………………………………………….. $230,000

Less: Gross profit ($230,000 X 33%) ………. 75,900

Cost of goods sold ………………………………… $154,100

BYP 6-6 COMMUNICATION ACTIVITY

MEMO

To: Pamela Barnes, President

From: Student

Re: 2016 ending inventory error

As you know, 2016 ending inventory was overstated by $1 million. Of course,

this error will cause 2016 net income to be incorrect because the ending

inventory is used to compute 2016 cost of goods sold. Since the ending inven–

BYP 6-7 ETHICS CASE

(a) The higher cost of the items ordered, received, and on hand at year–

end will be charged to cost of goods sold, thereby lowering current

year’s income and income taxes. If the purchase at year-end had been

made in the next year, the next year’s cost of goods sold would have

absorbed the higher cost. Next year’s income will be increased if unit

income taxes will increase.

(b) No. The president would not have given the same directive because the

purchase under FIFO would have had no effect on net income of the

current year.

BYP 6-8 ALL ABOUT YOU

Students responses to this question will vary depending on the inventory

fraud they choose to investigate. Here are responses for the two examples

given in the activity.

The fraud at Leslie Fay involved a number of illegal actions, all of which

increased net income. The company intentionally overstated ending inventory,

which has the effect of understating cost of goods sold. It also understated

BYP 6-9 FASB CODIFICATION ACTIVITY

(a) The primary basis of accounting for inventories is cost, which has

been defined generally as the price paid or consideration given to

acquire an asset. As applied to inventories, cost means in principle

the sum of the applicable expenditures and charges directly or

(b) The basis of stating inventories shall be consistently applied and

shall be disclosed in the financial statements; whenever a significant

change is made therein, there shall be disclosure of the nature of the

IFRS EXERCISES

IFRS6-1

Key Similarities are (1) the definitions for inventory are essentially the same,

(2) the guidelines on who owns the goods—goods in transit, consigned

goods, and the costs to include in inventory are essentially accounted for

the same under IFRS and U.S. GAAP; (3) use of specific identification cost

flow assumption, where appropriate.

IFRS6-2

Under IFRS, LaTour’s inventory turnover is computed as follows:

Cost of Goods Sold/Average Inventory

€578/ €154 = 3.75 or approximately 97 days (365 ÷ 3.75).

Difficulties in comparison to a company using U.S. GAAP could arise if the

U.S. company uses the LIFO cost flow assumption, which is prohibited under

IFRS6-3

(a) Louis Vuitton’s Note 1.15 states that inventories are valued using the

weighted average of FIFO methods.