CHAPTER 6

Cost-Volume-Profit Analysis: Additional Issues

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

1. Apply basic CVP concepts.

1, 2, 3, 4, 5,

6

1, 2, 3, 4, 5,

6

1

1, 2, 3, 4, 5

1A, 2A, 6A

2. Explain the term sales mix and

its effects on break-even sales.

7, 8, 9

7, 8, 9, 10

2

6, 7, 8, 9, 10

3A

3. Determine sales mix when a

company has limited resources.

10, 11

11, 12

3

11, 12, 13

4A

4. Indicate how operating leverage

affects profitability.

12, 13, 14,

15, 16

13, 14, 15

4

14, 15, 16

5A, 6A

*5. Explain the difference between

absorption costing and variable

costing.

17, 18, 19,

20, 21, 22

16, 17, 18,

19

17, 18, 19

7A, 8A

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Compute break-even point under alternative courses of

action.

Moderate

20–30

2A

Compute break-even point and margin of safety ratio, and

prepare a CVP income statement before and after changes

in business environment.

Moderate

20–30

3A

Determine break-even sales under alternative sales

strategies and evaluate results.

Moderate

20–30

4A

Determine sales mix with limited resources.

Simple

10–15

*7A

Prepare income statements under absorption costing and

variable costing for a company with beginning inventory,

and reconcile differences.

Moderate

20–30

*8A

Prepare absorption and variable costing income statements

and reconcile differences between absorption and variable

costing income statements when sales level and production

level change. Discuss relative usefulness of absorption

costing versus variable costing.

Moderate

20–30

impact of operating leverage on financial results.

6A

Determine contribution margin, break-even point, target

sales, and degree of operating leverage.

Moderate

20–30

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

*1. Apply basic CVP concepts.

Q6-1

Q6-3

Q6-2

Q6-4

Q6-5

Q6-6

BE6-2

BE6-3

BE6-4

BE6-5

BE6-6

DI6-1

E6-1

E6-2

E6-3

E6-4

E6-5

P6–3A

P6–6A

BE6-1

P6–1A

P6–2A

P6–6A

*2. Explain the term sales mix and

its effects on break-even sales.

Q6-7

Q6-8

Q6-8

Q6-9

BE6-7

BE6-8

BE6-9

BE6-10

DI6-2

E6-6

E6-7

E6-8

E6-9

E6–10

P6–3A

E6-6

E6-7

E6-8

P6–3A

*3. Determine sales mix when a

company has limited resources.

Q6–11

Q6–10

BE6-11

BE6-12

DI6-3

E6–11

E6–12

E6–13

P6–4A

E6–11

E6–12

E6–13

P6–4A

*4. Understand how operating

leverage affects profitability.

Q6–12

Q6–13

Q6–15

Q6–14

Q6–16

BE6-13

BE6-14

BE6-15

E6–14

E6–15

E6–16

P6-5A

P6-6A

DI6-4

E6–14

E6–15

E6–16

P6-5A

P6–6A

**5. Explain the difference between

absorption costing and

variable costing.

Q6-17

Q6–18

Q6–19

Q6–20

Q6–21

Q6–22

Q6–19

BE6-16

BE6-17

BE6-18

BE6-19

E6–17

E6–18

E6–19

P6–7A

P6–8A

E6–18

E6–19

P6–7A

P6–8A

Broadening Your Perspective

BYP6-6

BYP6-3

BYP6-4

CD6

BYP6-1

BYP6-5

BYP6-8

BYP6-2

BYP6-7

BYP6-9

ANSWERS TO QUESTIONS

1. CVP or cost-volume-profit analysis is the study of the effects of changes in costs and volume on

a company’s profit.

2. Managers use CVP analysis to make decisions involving break-even point, sales required to

reach a target net income, margin of safety, the most profitable sales mix, allocation of limited

resources, and operating leverage.

3. Both types of income statements report the same amount of net income. But the format used to

reach net income differs.

A traditional income statement’s format consists of:

Sales revenue – cost of goods sold = gross profit; Gross profit – selling and administrative expenses =

net income.

A CVP income statement’s format consists of:

Sales revenue – variable expenses = contribution margin; Contribution margin – fixed expenses =

net income.

4. The CVP income statement isolates variable costs from fixed costs while the traditional income

statement does not. The CVP format indicates contribution margin in total and frequently on a per

unit basis as well. This format facilitates calculation of break-even point and target net income.

It also highlights how changes in sales volume or cost structure affect net income.

5. WHEAT COMPANY

CVP Income Statement

Sales ………………………………………………………………………………………….. $900,000

Variable costs ($500,000 X .75) + ($200,000 X .75) …………………………... 525,000

Contribution margin ………………………………………………………………………. $375,000

6. If the selling price is reduced but variable and fixed costs remain unchanged, the break-even point

will increase.

7. Sales mix is the relative percentage of each product sold when a company sells more than one

product. Sales mix changes the calculation of the break-even point because the fixed costs must

be divided by the weighted-average unit contribution margin.

8. The 150,000-mile tire has a higher unit contribution margin, that is, each tire sold covers a larger

amount of fixed costs. Therefore, if the sales mix shifts away from the 150,000-mile tire to the

50,000-mile tire, the company will have to sell more total tires in order to break-even.

9. If a company has many products, the break-even point is calculated using sales information for

divisions or product lines, rather than individual products. The weighted-average contribution

margin ratio is computed by multiplying the sales mix percentage of each product line by the

contribution margin ratio of each product line, and then summing the results. Total break-even

sales in dollars is then calculated by dividing the company’s total fixed costs by the weighted–

average contribution margin ratio. Finally, to determine the amount of sales generated by each

product line at the break-even point, multiply the total break-even sales by the sales mix percentage

of each product line.

Questions Chapter 6 (Continued)

10. Contribution margin per unit of limited resource is determined by dividing the unit contribution

margin of the product by the number of units of the limited resource required to produce the

product.

11. The theory of constraints is a specific approach used to identify and manage constraints to achieve

the company’s goals. According to this theory, a company must continually identify its constraints

and find ways to reduce or eliminate them, where appropriate. Examples of constraints would be

production bottlenecks or poorly trained workers.

12. Cost structure refers to the relative proportion of fixed costs versus variable costs that a company

incurs. Companies that rely heavily on fixed costs will have higher break-even points.

13. Operating leverage refers to the extent to which a company’s net income reacts to a given change

in sales. A company can increase its operating leverage by increasing its reliance on fixed costs.

14. Typically manual labor is considered a variable cost. Depreciation on factory equipment is a fixed

cost. Therefore, if a company replaces manual labor with automated factory equipment it will

increase its operating leverage, and increase its break-even point.

15. The degree of operating leverage is a measure of a company’s relative operating leverage. It is

calculated by dividing the contribution margin by net income at a particular level of sales.

16. Pine’s degree of operating leverage of 8 versus Fir’s measure of 4 tells us that Pine will

experience twice (8 ÷ 4) the increase (or decrease) in net income for a given increase

(decrease) in sales as Fir.

*17. Under absorption costing, both variable and fixed manufacturing costs are considered to be

product costs. Under variable costing, only variable manufacturing costs are product costs and

fixed manufacturing costs are expensed when incurred.

*18. (a) The rationale for variable costing centers on the purpose of fixed manufacturing costs, which

is to have productive facilities available for use. Since these costs are incurred whether a

company operates at zero or 100% capacity, it is argued that they should be expensed

when they are incurred. Variable costing is useful in product costing internally by management

and it is useful in controlling manufacturing costs.

(b) Variable costing cannot be used for financial reporting purposes because it does not follow

generally accepted accounting principles.

*19. One way to compute the difference is as follows:

Ending inventory X Fixed manufacturing overhead cost per unit

8,500 X $5 = $42,500

Absorption costing will report a $42,500 higher net income than variable costing because a

portion of the fixed manufacturing overhead costs are deferred in inventory.

Questions Chapter 6 (Continued)

*20. If production equals sales in any given period, the net incomes under both methods will be equal.

In this case, there is no increase in the ending inventory. So fixed manufacturing overhead costs

in the current period are not deferred to future periods through the ending inventory.

*21. If production is greater than sales, absorption costing net income will be greater than variable

costing net income. Absorption costing net income is higher because some of the fixed

manufacturing overhead costs will be deferred in the inventory account until the products are

sold.

*22. In the long run, neither method will produce a higher net income amount. Over a long period of

time, sales can never exceed production, nor production exceed sales by significant amounts.

For this reason, over the lifetime of a corporation, variable costing and absorption costing will

tend to yield the same net income amounts.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 6-1

1. (a) $70 = ($250 – $180)

2. (c) $300 = ($500 – $200)

BRIEF EXERCISE 6-2

HAMBY INC.

Income Statement

For the Quarter Ended March 31, 2017

Sales ……………………………………………………………… $2,000,000

Variable expenses

Cost of goods sold ………………………………….. $760,000

Selling expenses……………………………………… 95,000

Administrative expenses ………………………….. 79,000

BRIEF EXERCISE 6-3

Contribution margin ratio = [($250,000 – $150,000) ÷ $250,000] = 40%

BRIEF EXERCISE 6-4

(a) $400Q = $250Q + $210,000 + $0

(b) Unit contribution margin $150, or ($400 – $250)

X = $210,000 ÷ $150

BRIEF EXERCISE 6-5

BRIEF EXERCISE 6-6

Margin of safety = $1,200,000 – $960,000 = $240,000

BRIEF EXERCISE 6-7

Model

Sales Mix

Percentage

Unit Contribution

Margin

Weighted-Average Unit

Contribution Margin

A12

60%

$15 ($50 – $35)

$ 9.00

BRIEF EXERCISE 6-8

Total break-even = ($269,500 ÷ $38.50*) = 7,000 units

Sales Units

Units of A12 = .60 X 7,000 = 4,200

BRIEF EXERCISE 6-9

(a) Weighted-average

(b) Total break-even

point = ($450,000 ÷ .30) = $1,500,000

in dollars

BRIEF EXERCISE 6-10

(a) Sales Mix

Bedroom Division $500,000 ÷ $1,250,000 = .40

(b)

Weight-average contribution

$575,000

OR

Contribution Margin Ratio

Bedroom Division ($275,000 ÷ $500,000) = .55

BRIEF EXERCISE 6-11

Product A

Product B

Unit contribution margin (a)

$10.0

$12

BRIEF EXERCISE 6-12

Product 1

Product 2

[(a) ÷ (b)]

Unit contribution margin (a)

$ 42

$ 32

Product 2 has a higher contribution margin per limited resource, even though

BRIEF EXERCISE 6-13

Degree of operating

leverage (old) = $200,000 ÷ $40,000 = 5

[(a) ÷ (b)]

BRIEF EXERCISE 6-14

Break-even point in dollars:

Diggs Co. Doggs Co.

$75,000 ÷ ($120,000 ÷ $200,000) $105,000 ÷ ($150,000 ÷ $200,000)

= $125,000 = $140,000

Doggs Company’s cost structure relies much more heavily on fixed costs

BRIEF EXERCISE 6-15

Degree of operating leverage = Contribution margin ÷ Net income

*BRIEF EXERCISE 6-16

Variable Costing

Direct materials

$14,400

Direct labor

25,600

Variable manufacturing overhead

Total product costs

*BRIEF EXERCISE 6-17

Absorption Costing

Direct materials

$14,400

Direct labor

25,600

Variable manufacturing overhead

Fixed manufacturing overhead

12,000

Total product costs

$81,400

*BRIEF EXERCISE 6-18

(a) Absorption Costing

……. Direct materials ………………………………………………………. $20

Direct labor …………………………………………………………….. 14

(b) Variable Costing

Direct materials ……………………………………….. $20

*BRIEF EXERCISE 6-19

MEMO

To: Chief financial officer

From: Student

Re: Absorption and variable costing

Under absorption costing, fixed manufacturing overhead is a product cost,

while under variable costing, fixed manufacturing overhead is a period cost

(expensed as incurred).

SOLUTIONS TO DO IT! REVIEW EXERCISES

DO IT! 6-1

(a) Break-even point in units is 7,500 units ($150,000 ÷ $20).

Break-even point in sales dollars is $375,000 ($150,000 ÷ .40*).

(b) Break-even point in units is 8,333 units (rounded) ($150,000 ÷ $18*).

Break-even point in sales dollars is $400,000 ($150,000 ÷ .375**).

The margin of safety in dollars is $118,400 ($518,400*** – $400,000).

*$50 – (.04 X $50) – 30 = $18.

DO IT! 6-2

(a) The sales mix percentages as a function of units sold is:

Basic

Basic Plus

Premium

750 ÷ 1,500 = 50%

450 ÷ 1,500 = 30%

300 ÷ 1,500 = 20%

DO IT! 6-2 (Continued)

(d) The break-even units to produce for each product are:

Basic: 1,300 units X 50% = 650 units

DO IT! 6-3

(a) The Best binoculars have the highest unit contribution margin. Thus,

(b) The contribution margin per unit of limited resource is calculated as:

Good

Better

Best

(c) The Better binoculars have the highest contribution margin per unit of

DO IT! 6-4

(a)

Contribution

Margin

Net Income

=

Degree of operating

Leverage

Old

$1,400,000

$400,000

=

3.5

New

$2,300,000

$400,000

=

5.8

SOLUTIONS TO EXERCISES

EXERCISE 6-1

(a) 1. Contribution margin per room = $60 – ($8 + $34)

Contribution margin per room = $18

Contribution margin ratio = $18 ÷ $60 = 30%

(b) 1. Margin of safety in dollars:

Planned activity = 50 rooms per day X 30 days

= 1,500 rooms per month

$39,000

= 43%

EXERCISE 6-2

(a) Contribution margin in dollars: Sales = 4,000 X $30 = $120,000

Variable costs = $120,000 X .75 = 90,000

Contribution margin $ 30,000

EXERCISE 6-2 (Continued)

(b) Break-even sales in dollars:

$16,800

25%

= $67,200.

EXERCISE 6-3

Current selling price = $325,000 ÷ 5,000 units

Current selling price = $65

2. Reduce variable costs to 58% of sales.

Net income = $325,000 – $188,500** – $75,000 = $61,500.

EXERCISE 6-4

(a)

1. Contribution margin ratio is:

$30,000

= 62.5%

$48,000

Break-even point in dollars =

$20,250

= $32,400

62.5%

(b) At the break-even point fixed costs and contribution margin are equal.

Therefore, the contribution margin at the break-even point would be

$20,250.

(c)

Fare revenue ($108* X 500**)

$54,000

Variable costs ($18,000 X 1.25)

Contribution margin

Fixed costs

Net income

EXERCISE 6-5

(a) CAREY COMPANY

CVP Income Statement

For the Year Ended December 31, 2017

Total

Per Unit

Sales (60,000 X $26) ………………………………..

$1,560,000

$26

$48,000

(b) CAREY COMPANY

CVP Income Statement

For the Year Ended December 31, 2017

Total

Per Unit

Sales [(60,000 X 105%) X $24.50*] …………….

$1,543,500

$24.50

EXERCISE 6-6

Sales Mix

Percentage

Unit contribution

Margin

Weighted-Average

Contribution Margin

Lawnmowers

20%

$30

$ 6

Sales Mix

Percentage

Total

Break-even Sales

in Units

Sales Units

Needed

Per Product

Weed-trimmers

Total units

X

=

Lawnmowers

20%

X

150,000

=

30,000 units

Net income ……………………………………………..

$ 187,500

EXERCISE 6-7

(a)

Sales Mix

Percentage

Contribution

Margin Ratio

Weighted-Average

Contribution

Margin Ratio

Oil changes

70%

20%

.14

Sales Mix

Percentage

Total

Break-even Sales

in Dollars

Sales Dollars

Needed

Per Product

Oil changes

Total sales

70%

X

=

(b)

Sales to achieve target net income = ($78,000 + $52,000) ÷ .26 = $500,000

Sales Mix

Percentage

Total

Sales Needed

Sales Dollars

Needed Per Product

Per Store

Total sales

Oil changes

70%

X

$500,000

=

$350,000

EXERCISE 6-8

(a)

Sales Mix

Percentage

Contribution

Margin Ratio

Weighted-Average

Contribution

Margin Ratio

Mail pouches

and small boxes

80%

20%

.16

EXERCISE 6-8 (Continued)

Sales Mix

Percentage

Total Break-

even Sales

in Dollars

Sales Dollars

Needed

Per Product

Mail pouches

and small boxes

80%

X

$40,000,000

=

$32,000,000

(b)

Sales Mix

Percentage

Contribution

Margin Ratio

Weighted-Average

Contribution

Margin Ratio

Mail pouches

and small boxes

40%

20%

.08

Sales Mix

Percentage

Total Break-

even Sales

in Dollars

Sales Dollars

Per Product

Total sales

Mail pouches

and small boxes

40%

X

$24,000,000

=

$ 9,600,000

EXERCISE 6-9

(a) Weighted-average unit

contribution margin = ($40 X .35) + ($20 X .55) + ($60 X .10) = $31

Total sales

EXERCISE 6-9 (Continued)

(c) Shoes: 7,000 X $40 = $280,000

Gloves: 11,000 X $20 = 220,000

EXERCISE 6-10

(a) Sales mix percentage

iPad division: $600,000 ÷ ($600,000 + $400,000) = .60

iPod division: $400,000 ÷ ($600,000 + $400,000) = .40

(b)

Weighted-average contribution

=

$320,000

= .32 OR

margin ratio

$1,000,000

(c) Break-even point in dollars = $120,000 ÷ .32 = $375,000

EXERCISE 6-11

(a)

Product

A

B

C

Contribution margin per unit of limited resource (a) ÷ (b)

Unit contribution margin (a)

$ 6

$ 2

$ 3

(b) Product A should be manufactured because it results in the highest

contribution margin per machine hour.

EXERCISE 6-11 (Continued)

(c)

1.

Product

A

B

C

Machine hours (a) (3,000 ÷ 3)

1,000

1,000

1,000

2.

Product A

Total contribution margin [(a) X (b)]

Machine hours (a)

3,000

EXERCISE 6-12

(a)

Product D: $30 ÷ $10 = 3.0 hours per unit

Product E: $80 ÷ $10 = 8.0 hours per unit

Product F: $35 ÷ $10 = 3.5 hours per unit

(b)

Product

D

E

F

Selling price

$200

$ 300

$250

Variable costs

160

Contribution margin

Direct labor hours per unit

÷ 8.0

Contribution margin per

direct labor hour

$17.50

(c) Product D should be produced because it generates the highest contri-

bution margin per direct labor hour.

Product D

Total direct labor hours available

Contribution margin per direct labor hour

Total contribution margin

Contribution margin per unit of limited

Total contribution margin [(a) X (b)]

$2,000

$1,500

EXERCISE 6-13

(a)

Product

Basic

Deluxe

Selling price per unit

$40

$ 52

(b) The Basic product should be manufactured because it results in the

higher contribution margin per machine hour.

(c)

1.

Basic

Deluxe

Total

Machine hours allocated

500

500

1,000

$36

Machine hours allocated

1,000

X Contribution margin

per machine hour

–0–

X Contribution margin

EXERCISE 6-14

(a)

Contribution

Margin

÷

Net

Income

=

Degree of Operating

Leverage

Contador

÷

=

Armstrong

$260,000

÷

$100,000

=

2.60

Variable costs per unit

Unit contribution margin (a)

Machine hours required (b)

Contribution margin per

machine hour (a) ÷ (b)

EXERCISE 6-14 (Continued)

(b)

Armstrong Company

Contador Company

Sales

Variable costs

$550,000**

264,000**

$550,000***

55,000***

(c) Each company experienced a $50,000 increase in sales. However, be–

cause of Contador’s higher operating leverage, it experienced a $45,000

EXERCISE 6-15

(a)

Contribution

Margin

÷

Net Income

=

Degree of

Operating Leverage

÷

=

Manual system

$300,000

÷

$200,000

=

1.50

(b) The computerized system would produce profits that are 3.0 times

(4.50 ÷ 1.50) as much as the manual system. With a $150,000 increase in

Net income

EXERCISE 6-15 (Continued)

Manual

System

Computerized

System

Sales

$1,650,000

$1,650,000

(c)

(Actual Sales

–

Break-even Sales)

÷

Actual Sales

=

Margin of Safety Ratio

–

÷

=

Manual system

Computerized

($1,500,000

–

$500,000*)

÷

$1,500,000

=

.67

EXERCISE 6-16

(a)

Contribution

Margin

÷

Net

Income

=

Degree of Operating

Leverage

Traditional Yams

Auto-Yams

$ 80,000

$240,000

÷

÷

$50,000

$50,000

=

=

1.60

4.80

Auto-Yams, which relies more heavily on fixed costs, has the higher

EXERCISE 6-16 (Continued)

(b)

% Change

in Sales

X

Degree of

Operating

Leverage

=

% Change in

Net Income

15% decrease:

Traditional Yams

(15%)

X

1.60

=

(24.0%)

(c) There are several possible answers that could be given. For example,

if the candied Yams business is fairly stable, Auto-Yams might be the

choice, because they will generate the higher contribution margin and

EXERCISE 6-17

(a)

Unit Cost

Direct materials

$ 7.50

Direct labor

3.45

Variable manufacturing overhead

5.80

Manufacturing cost per unit

$16.75

Auto-Yams

X

=

Traditional Yams

Auto-Yams

X

X

1.60

=

=

EXERCISE 6-17 (Continued)

(b)

SIREN COMPANY

Income Statement

For the Year Ended December 31, 2017

Variable Costing

Sales (80,000 lures X $25)

$2,000,000

Variable cost of goods sold

(80,000 lures X $16.75)

$1,340,000

(c)

Unit Cost

Direct materials

$ 7.50

Direct labor

3.45

Variable manufacturing overhead

Fixed manufacturing overhead ($225,000 ÷ 90,000)

2.50

Manufacturing cost per unit

(d)

SIREN COMPANY

Income Statement

For the Year Ended December 31, 2017

Absorption Costing

Sales (80,000 lures X $25)

$2,000,000

Cost of goods sold (80,000 lures X $19.25)

1,540,000

Gross profit

Fixed selling and administrative expenses

522,100

Net Income

$ (62,100)

Variable selling and administrative

expenses (80,000 lures X $3.90)

312,000

Contribution margin

Fixed manufacturing overhead

Fixed selling and administrative

expenses

435,100

Net Income (loss)

*EXERCISE 6-18

(a) Direct materials used $ 79,000

Direct labor incurred 30,000

(b) Absorption costing would show a higher net income because a portion

of the fixed costs are deferred to future periods. The following computa–

tion indicates that finished goods inventory will be $4,000 higher under

absorption costing which will cause its net income to be $4,000 higher.

Direct materials used $ 79,000

Direct labor incurred 30,000

*EXERCISE 6-19

(a)

Utility Expense

Months in

a year

X

Kilowatt

hours

X

Hourly

Charge

=

Variable

Utilities

12

X

500

X

$0.50

=

$3,000

*EXERCISE 6-19 (Continued)

Variable Costing

Labor:

Crate builders

$43,000

Material:

(b)

Absorption Costing

Labor:

Crate builders

$ 43,000

Material:

Wood

54,000

Variable overhead:

Utilities

Nails

Fixed overhead:

Rent

Total manufacturing costs

(c) The entire difference in costs between the two methods is due to the

fact that fixed overhead is included as part of manufacturing costs

Wood

Variable Overhead:

Nails

Total manufacturing costs

SOLUTIONS TO PROBLEMS

PROBLEM 6-1A

(a) Sales were $2,000,000 and variable expenses were $1,200,000, which

means contribution margin was $800,000 and CM ratio was .40. Fixed ex-

(b) 1. The effect of this alternative is to increase the selling price per unit

to $31.25 ($25 X 125%). Total sales become $2,500,000 (80,000 X

$31.25). Thus, contribution margin ratio changes to 52%

2. The effects of this alternative are: (1) fixed costs decrease by

$160,000, (2) variable costs increase by $100,000 ($2,000,000 X 5%),

(3) total fixed costs become $875,000 ($1,035,000 – $160,000), and

3. The effects of this alternative are: (1) variable and fixed cost of

goods sold become $784,000 each, (2) total variable costs become

PROBLEM 6-2A

(a)

(1)

Current Year

Sales

Variable costs

Direct materials

Direct labor

$1,500,000

511,000

290,000

Current Year

Projected Year

Contribution margin

Sales

Variable costs

Direct materials

$1,500,000

511,000

X 1.1

X 1.1

$1,650,000

562,100

(2)

Fixed Costs

Current Year

Projected year

Total fixed costs

Manufacturing overhead ($350,000 X .30)

$105,000

$105,000

Contribution margin

PROBLEM 6-2A (Continued)

(b) Unit selling price = $1,500,000 ÷ 100,000 = $15

Break-even point in units

=

Fixed costs

÷

Unit contribution margin

=

÷

Break-even point in dollars

=

Fixed costs

÷

Contribution margin ratio

=

÷

(c) Sales dollars

required for

=

(Fixed costs

+

Target net income)

÷

Contribution margin ratio

target net income

=

+

÷

ratio

=

÷

(e)

(1)

Current Year

Sales

Variable costs

Direct materials

Direct labor ($290,000 – $104,000)

$1,500,000

511,000

186,000

PROBLEM 6-2A (Continued)

Fixed cost

Manufacturing overhead ($350,000 X .70)

Selling expenses ($250,000 X .10)

$245,000

25,000

(3) Break-even point in dollars = $486,000 ÷ .28 = $1,735,714 (rounded)

The break-even point in dollars declined from $2,355,000 to $1,735,714.

PROBLEM 6-3A

(a)

Sales Mix

Percentage

X

Contribution

Margin Ratio

=

Weighted-Average

Contribution

Margin Ratio

Appetizers

15%

X

50%

=

.075

Sales Mix

Percentage

X

Total Sales

Needed

=

Sales from

Each Product

Main entrees

Desserts

Beverages

X

X

X

=

=

=

Appetizers

15%

X

$2,600,000

=

$ 390,000

(b)

Sales Mix

Percentage

X

Contribution

Margin Ratio

=

Weighted-Average

Contribution

Margin Ratio

Desserts

Beverages

X

X

=

=

Appetizers

Main entrees

25%

25%

X

X

50%

10%

=

=

.125

.025

Main entrees

Desserts

Beverages

50%

X

X

X

25%

=

=

=

PROBLEM 6-3A (Continued)

Thus, sales would have to increase by $775,000 ($3,375,000 – $2,600,000) to

achieve the target net income. This increase in sales is driven by the

increase in fixed costs. The sales of each product line would be:

Sales Mix

Percentage

X

Total Sales

Needed

=

Sales from

Each Product

Appetizers

25%

X

$3,375,000

=

$ 843,750

(c)

Sales Mix

Percentage

X

Contribution

Margin Ratio

=

Weighted-Average

Contribution

Margin Ratio

Desserts

Beverages

X

X

=

=

Appetizers

15%

X

50%

=

.075

The weighted-average contribution margin ratio computed in part (a) was

45%. With the contribution margin ratio on entrees falling to 10%, that

Total sales required

to achieve target net

income = ($1,638,000 + $117,000) ÷ .375 = $ 4,680,000

Sales Mix

Percentage

X

Total Sales

Needed

=

Sales from

Each Product

Beverages

X

=

Appetizers

15%

X

$4,680,000

=

$ 702,000

Relative to parts (a) and (b), the total required sales for (c) would increase.

It appears that the least risky approach would be for Paul to switch to the

new sales mix, but not to incur the additional fixed costs of expanding

Desserts

Beverages

X

X

=

=

PROBLEM 6-4A

(a)

Product

Economy

Standard

Deluxe

Selling price

$30

$50

$100

(b)

Product

Economy

Standard

Deluxe

Unit contribution margin (a)

$14

$ 30

$ 54

(c) If additional machine hours become available, the additional time should

Less: Variable costs

PROBLEM 6-5A

(a) To determine the break-even point in dollars we must first calculate

the contribution margin ratio for each company.

Contribution

Margin

÷

Sales

=

Contribution Margin

Ratio

Blanc Company

$220,000

÷

$500,000

=

.44

(Actual Sales

–

Break-even Sales)

÷

Actual Sales

=

Margin of Safety

Ratio

Noir Company

–

÷

=

(b)

Contribution

Margin

÷

Net

Income

=

Degree of Operating

Leverage

Noir Company

÷

Blanc Company

$220,000

÷

$50,000

=

4.4

(c)

Blanc Company Noir Company

Sales $600,000* $600,000

Variable costs 336,000** 216,000***

$320,000

Costs

$270,000

PROBLEM 6-5A (Continued)

(d)

Blanc Company Noir Company

Sales $400,000* $400,000

Variable costs 224,000** 144,000***

Contribution margin 176,000 256,000

(e) In part (b) the degree of operating leverage of Noir Company was

higher than that of Blanc Company, telling us that the net income of

Noir Company was more sensitive to changes in sales than that of

Blanc Company. In part (c) we see that a 20% increase in sales

increased the net income of Noir Company by $64,000 ($114,000 –

PROBLEM 6-6A

(a) Reformat the income statement to CVP format.

All amount are in $000s.

Sales ………………………………………………… $75,000

Variable costs ($31,500 + $13,500) ………. 45,000

(b) If a hired workforce replaces sales agents, commissions will be reduced

to 8% of sales, or $6,000; but fixed costs will increase by $7,500.

Sales ………………………………………………… $75,000

Variable costs ($31,500 + $6,000) ………… 37,500

(c) Operating leverage = contribution margin ÷ operating income

(1) Current situation: from part (a)

$30,000 ÷ $11,130 = 2.70

PROBLEM 6-6A (Continued)

The calculations indicate that at a sales level of $75 million, a percentage

change in sales and contribution margin will result in 2.70 times that

percentage change in operating income if Bonita continues to use sales

(d) The sales level at which operating incomes will be identical is called

the point of indifference. This would be when the cost of the network of

agents (18% of sales) is exactly equal to the cost of paying employees

8% commission along with additional fixed costs of $7.5 million. None

of the other costs is relevant, because they will not change between

alternatives.

*PROBLEM 6-7A

(a) JACKSON COMPANY

Income Statement

For the Year Ended December 31, 2016

Variable Costing

Sales (3,500 tons X $2,000) …………………….

Variable cost of goods sold

Inventory, January 1 ……………………….

Variable cost of goods manufactured

[4,000 tons X ($2,000 X .15)] …………

$ –0–

1,200,000

$7,000,000

*PROBLEM 6-7A (Continued)

JACKSON COMPANY

Income Statement

For the Year Ended December 31, 2017

Variable Costing

Sales (4,000 tons X $2,000) ………………………

Variable cost of goods sold

Inventory, January 1 …………………………

Variable cost of goods manufactured

[3,500 tons X ($2,000 X .15)] …………..

$ 150,000

1,050,000

$8,000,000

(b) JACKSON COMPANY

Income Statement

For the Year Ended December 31, 2016

Absorption Costing

Sales (3,500 tons X $2,000) ………………….

Cost of goods sold

Inventory, January 1 …………………….

Cost of goods manufactured …………

$ –0–

4,000,000

(1)

$7,000,000

Variable cost of goods available

*PROBLEM 6-7A (Continued)

JACKSON COMPANY

Income Statement

For the Year Ended December 31, 2017

Absorption Costing

Sales (4,000 tons X $2,000) ………………

Cost of goods sold

Inventory, January 1 …………………

Cost of goods manufactured………

Cost of goods available for sale …

$ 500,000

3,850,000

4,350,000

(1)

$8,000,000

(c) The variable costing and the absorption costing net income can be

reconciled as follows:

2016

2017

Absorption costing net income

Variable costing net income

Fixed manufacturing overhead

expensed with variable costing

$2,800,000

$1,950,000

$2,800,000

$2,700,000

(1)In 2016, with absorption costing $2,450,000

3,500 units sold

$2,800,000 X 4,000 units produced

of the

fixed manufacturing overhead is expensed as part of cost of goods sold, and $350,000

$2,800,000 X 4,000 units produced

*PROBLEM 6-7A (Continued)

(d) Income parallels sales under variable costing as seen in the increase

*PROBLEM 6-8A

(a)

DILITHIUM BATTERIES DIVISION

Income Statement

For the Year Ended December 31, 2017

Absorption Costing

_______________________________________________________________

60,000 90,000

Produced Produced

Sales (60,000 units X $30) $1,800,000 $1,800,000

Cost of goods sold

(60,000 units X $21) 1,260,000 (60,000 X $18) 1,080,000

Gross profit 540,000 720,000

(b)

DILITHIUM BATTERIES DIVISION

Income Statement

For the Year Ended December 31, 2017

Variable Costing

_______________________________________________________________

60,000 90,000

Produced Produced

Sales (60,000 units X $30) $1,800,000 $1,800,000

Variable cost of goods sold

(60,000 units X $12) 720,000 720,000

*PROBLEM 6-8A (Continued)

(c) If the company produces 90,000 units, but only sells 60,000 units,

then 30,000 units will remain in ending inventory. Under absorption

costing these 30,000 units will each include $6 of fixed manufacturing

overhead—a total of $180,000. However, under variable costing, fixed

(d) Variable costing has a number of advantages over absorption costing

for decision making and evaluation purposes. (1) The use of variable

costing is consistent with cost-volume-profit and incremental analysis.

(2) Net income computed under variable costing is unaffected by

changes in production levels. Note that, under variable costing the

company’s net income is $370,000 no matter what the level of production

CD 6 CURRENT DESIGNS

(a)

Weighted

Average Unit

Contribution

(b) Break-even Sales = $820,000 ÷ $436 = 1,881 units

(c) Target Net Income in Units:

Rotomolded Kayaks

+

Composite Kayaks

=

Weighted-Average

CM/Unit

($380 X .70)

($660 X .30)

$464

(d) CVP Income Statement

Rotomolded

Composite

Sales

$2,000,000

$1,000,000

Variable Costs

Contribution Margin

Fixed Costs

660,000

Net Income

Rotomolded Kayaks

(e) Degree of Operating Leverage

Rotomolded Kayaks = $800,000 ÷ $140,000 = 5.71

Composite Kayaks = $330,000 ÷ $170,000 = 1.94

BYP 6-1 DECISION-MAKING ACROSS THE ORGANIZATION

(a) Sales (10,000 seats X $500) $5,000,000

Variable costs (10,000 seats X $200) 2,000,000

(b) Contribution margin ratio = $3,000,000 ÷ $5,000,000 = .60

(c) Sales (10,000 seats X $500) $5,000,000

(d) Contribution margin ratio = $4,000,000 ÷ $5,000,000 = .80

(e) By automating its manufacturing process the company will replace some

of its variable costs with fixed costs. This shift toward more fixed costs

will increase its break-even point from $3,333,333 to $3,750,000 and

reduce its margin of safety from 33.3% to 25%. This means that under

BYP 6-2 MANAGERIAL ANALYSIS

(a) The contribution margin ratios under each approach are:

(b) The break-even points in sales dollars under each approach are:

(c) At the current level of sales, the margin of safety ratio under each

approach is:

Current approach ($2,000,000 – $1,520,000)/$2,000,000 = .24

(d) The degree of operating leverage under each approach at the current

level of sales is:

BYP 6-2 (Continued)

(e) In order to solve for the sales level where net income would be equal

under either approach, set the two CVP equations equal to each other

and solve for sales:

Sales – ((1 – .75) X Sales) – $380,000 = Sales – ((1 – .5) X Sales) – $800,000

(f) Based upon this numeric analysis it would appear that the decision to

purchase the automated system would be a good decision. The

current level of sales far exceeds the break-even point, and, unless

sales were to fall all the way to $1,680,000, the company would be

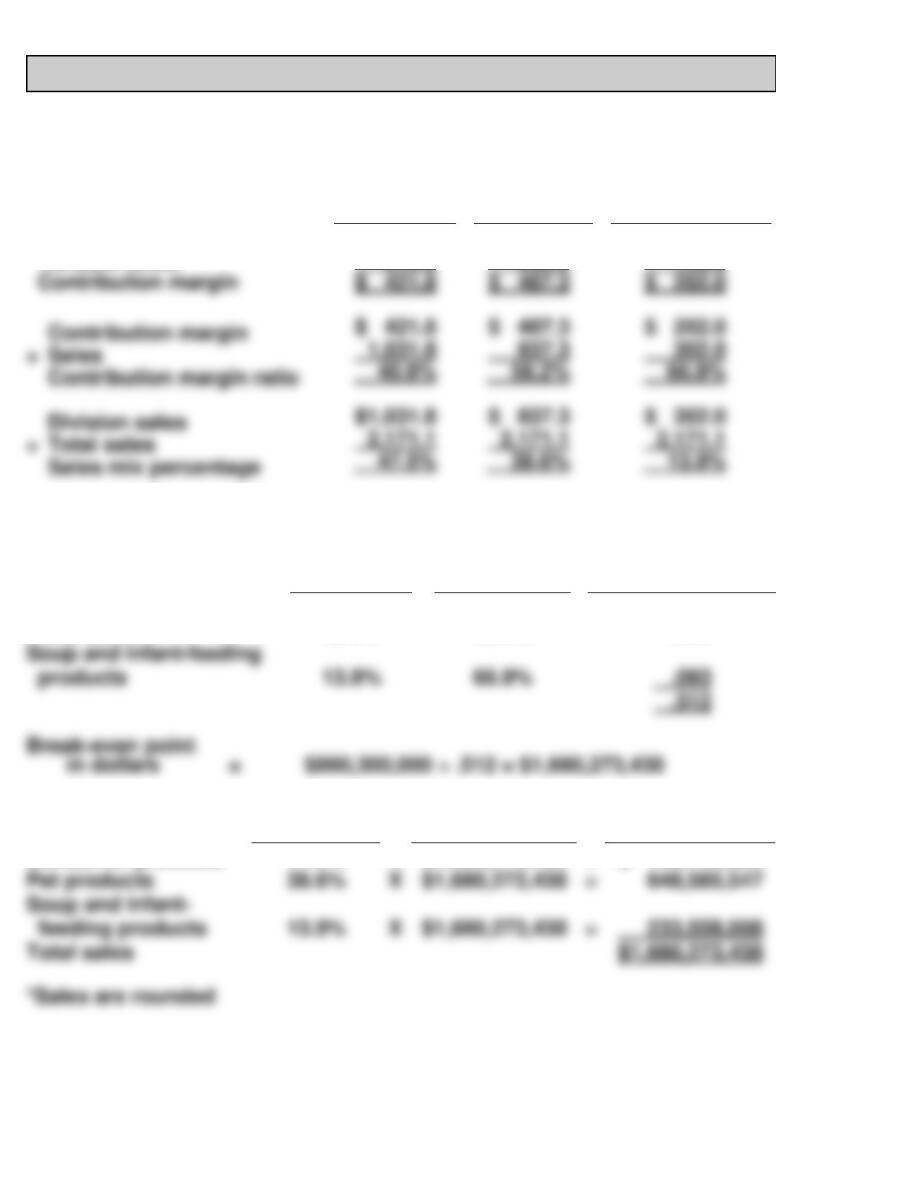

BYP 6-3 REAL-WORLD FOCUS

(a)

($ in millions)

Consumer

Products

Pet

Products

Soup and

Infant-Feeding

Products

Sales

Variable costs

$1,031.8

610.0

$ 837.3

350.0

$ 302.0

100.0

(b)

Sales Mix

Percentage

X

Contribution

Margin Ratio

=

Weighted–Average

Contribution

Margin Ratio

13.9%

Consumer products

Pet products

47.5%

38.6%

40.9%

58.2%

.194

.225

Sales Mix

Percentage

X

Total Sales

=

Sales from

Each Product*

Soup and infant-

Total sales

X

$1,680,273,438

=

Consumer products

47.5%

X

$1,680,273,438

=

$ 798,129,883

÷ Total sales

BYP 6-4 REAL-WORLD FOCUS

(a) The four primary product lines are FedEx Express (provides express

transportation); FedEx Ground (small package ground delivery); FedEx

Freight (regional, less-than-truckload freight service); and FedEx

Services (Sales, information technology, communications). The key

(b)

FEDEX GROUND

Income Statement

For the Year Ended May 31, 2013

Variable Costing

(In Millions)

____________________________________________________________

Revenues ……………………………………………… $10,578

Variable costs:

Salaries and employee benefits …………. $1,586

Purchased transportation …………………. 4,191

Fixed costs:

Fixed Costs

÷

Contribution

Margin Ratio

=

Break-even Point

in Dollars

(c)

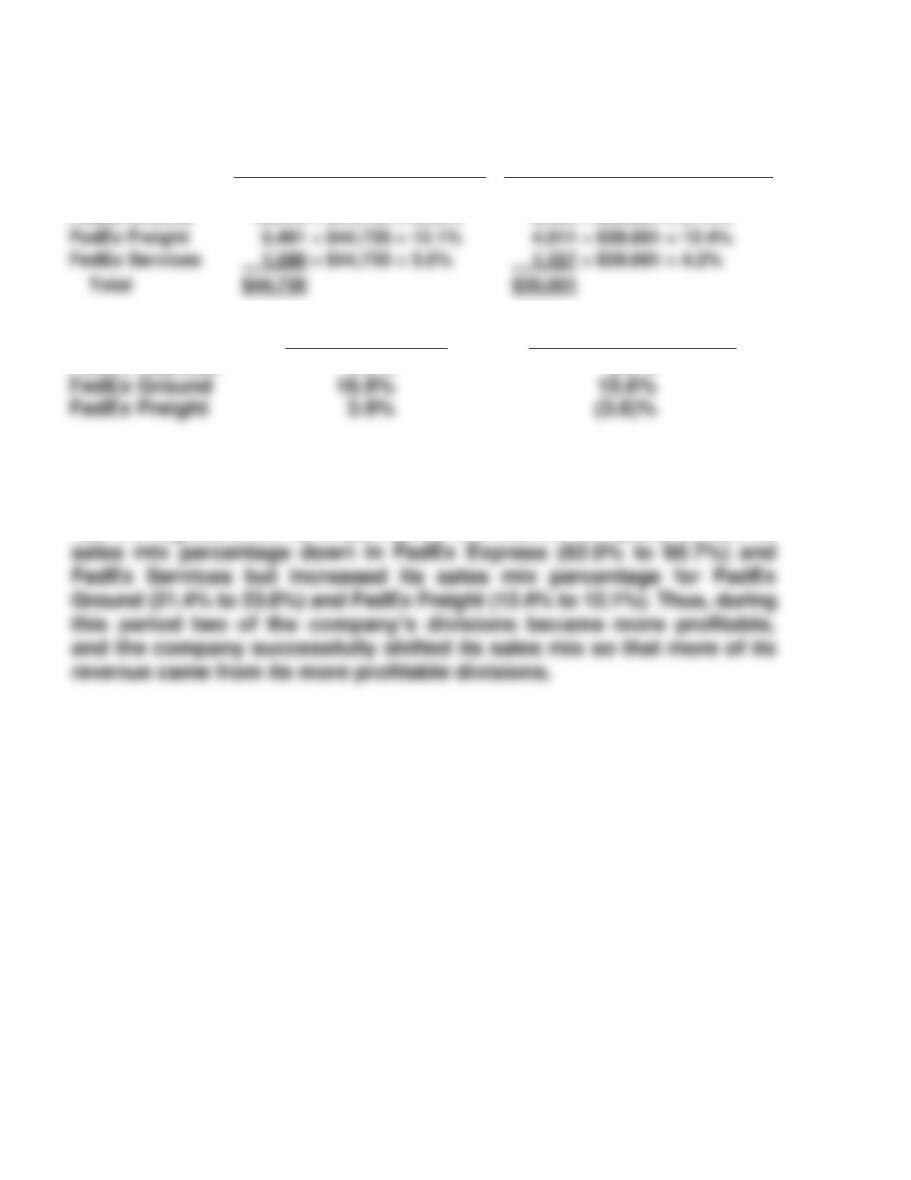

(i)

2013

2011

FedEx Express

FedEx Ground

$27,171 ÷ $44,730 = 60.7%

10,578 ÷ $44,730 = 23.6%

$24,581 ÷ $39,661 = 62.0%

8,485 ÷ $39,661 = 21.4%

(ii)

2013

2011

FedEx Express

2.0%

5.0%

(iii) In part (ii) we see that the FedEx Express’s operating margin declined,

but the other two increased. We also see in part (ii) that FedEx Express

had the lowest operating margin in 2013 (2.0%) while FedEx Ground

had the highest (16.9%). In part (i) we see that the company shifted its

Total

BYP 6-5 REAL-WORLD FOCUS

(a) Smart Balance relies very heavily on outsourcing. It keeps it employees

and investments in fixed assets to a minimum. As a consequence it

has very low fixed costs.

BYP 6-6 COMMUNICATION ACTIVITY

MEMO

To: Bjorn Borg—CEO

From: Student

Re: Best use of limited resources

I share your concern, that, since we are operating at full capacity, we need

to ensure that our product mix maximizes our profitability. The decision of

how to best utilize our limited productive resources is one of the most

important decisions we face. We currently make two different anchors, a

*BYP 6-7 ETHICS CASE

(a) The division’s net income increased by $225,000 ($525,000 – $300,000).

(b) In 2016 the number of units produced and sold were equal. When this

occurs variable costing and absorption costing provide the same

results. Thus, in 2016, net income under variable costing would have

(c) In part (b) it was determined that the division’s net income would have

been $300,000 in 2017 under variable costing. Since this is the same as

2016 net income, Brett would not receive a bonus.

(d) If Brett intentionally overproduced inventory in order to increase his

bonus, then his actions were unethical. Overproduction of inventory

increases the company’s costs related to inventory, such as storage,

BYP 6-8 ALL ABOUT YOU

Target Net Income)

(a) Using a common equation for CVP analysis,

Sales = Variable Costs + Fixed Costs + Net Income, and substituting the

information provided, and knowing that at break-even, net income = $0,

(b) To find the sales required to reach a target net income, contribution

margin must be calculated.

Contribution Margin = Sales – Variable Costs

Using the contribution margin ratio,

Required Sales in Dollars

=

(Fixed Costs +

Target Net Income)

/Contribution Margin

Ratio

(c) Answers will vary. Suggested examples include franchise fees, employee

wages, utilities, supplies, and maintenance.

(d) Answers will vary.

BYP 6-9 CONSIDERING CORPORATE SOCIAL RESPONSIBILITY

Discussion Guide: If reduction of greenhouse gas emissions is a goal, then

one step toward attainment of that goal is to assign a cost to greenhouse–

gas emissions. One approach that is currently being used is the buying and

selling of carbon-emission rights. As companies buy and sell emission rights,

the price of polluting becomes a tangible factor in the formulations that will