35 Minutes, Medium

Nov. 5 13,390

Sales 13,390

5 9,105

Inventory 9,105

Dec. 5 13,390

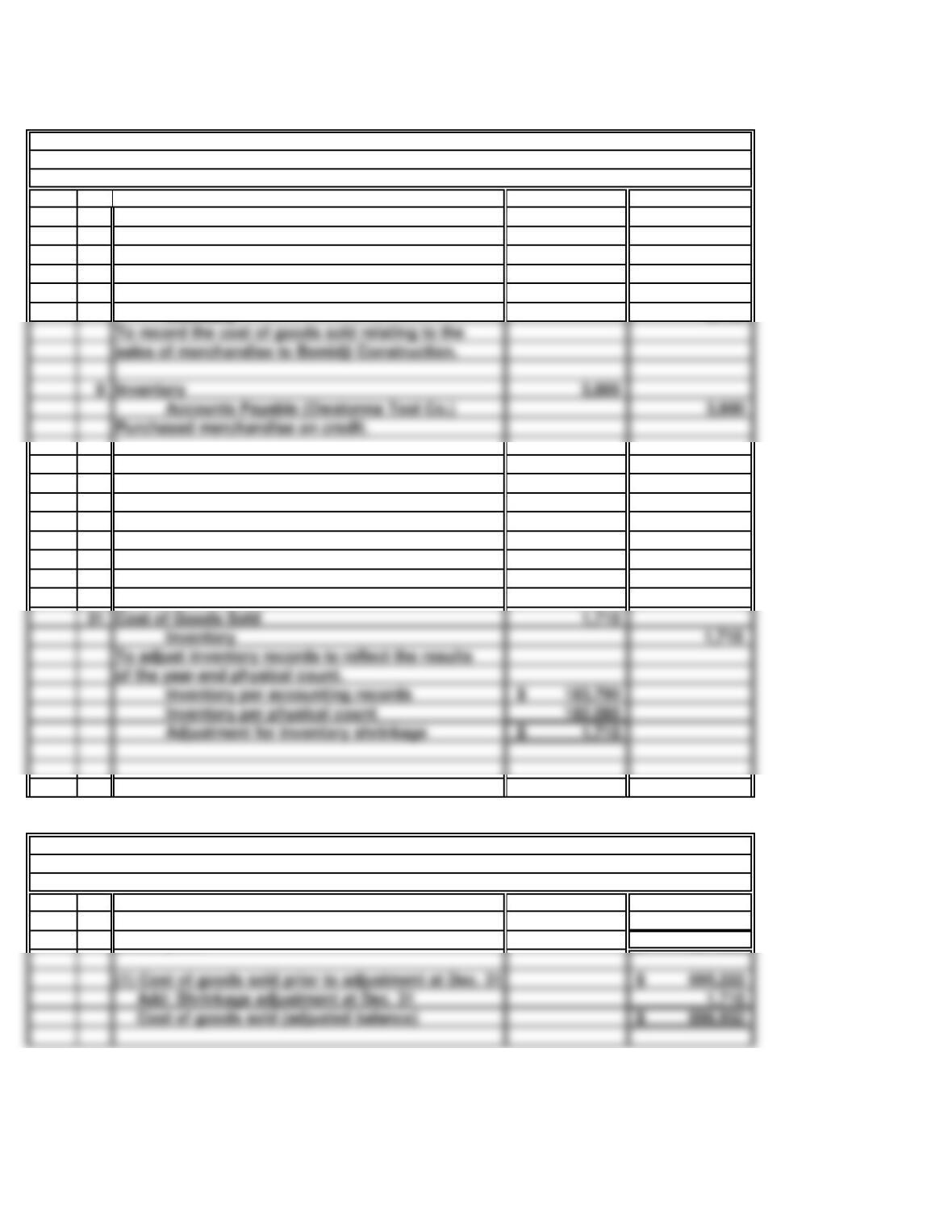

Accounts Receivable (Bemidji Construction) 13,390

9 3,800

Cash 3,800

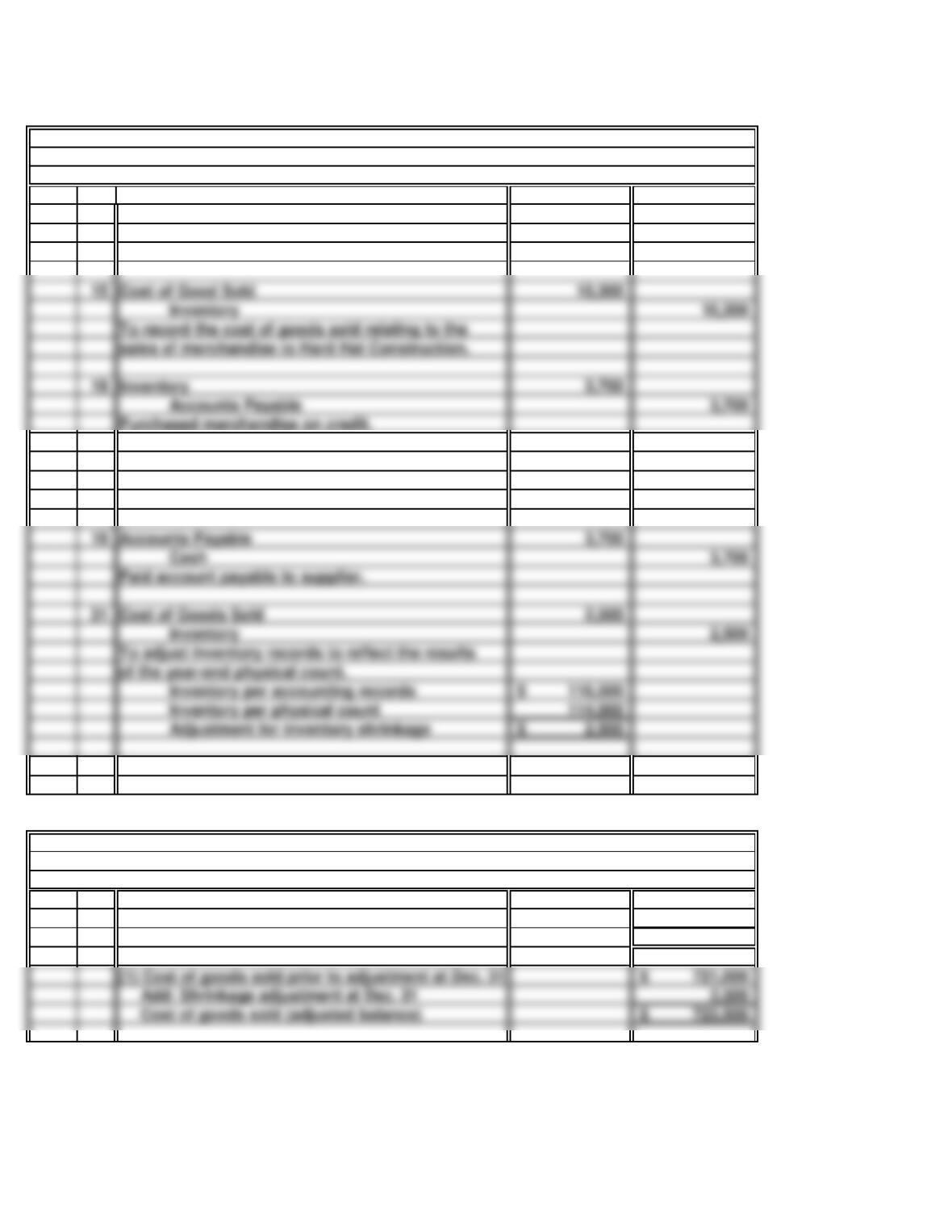

Inventory per accounting records 183,790$

Inventory per physical count 182,080

Adjustment for inventory shrinkage 1,710$

Cost of Goods Sold

of the year-end physical count.

To adjust inventory records to reflect the results

b.

1,024,900$

696,932

327,968$

696,932$

Add: Shrinkage adjustment at Dec. 31

(1) Cost of goods sold prior to adjustment at Dec. 31

Cost of goods sold (adjusted balance)

SOLUTIONS TO PROBLEMS SET A

Gross profit

Partial Income Statement

For the Year Ended December 31, Current Year

Net sales

Collected accounts receivable.

Accounts Payable (Owatonna Tool. Co.)

PROBLEM 6.1A

a.

CLAYPOOL HARDWARE

(1)

General Journal

CLAYPOOL HARDWARE

Cost of goods sold (1)

Paid account payable to supplier.

Accounts receivable (Bemidji Construction)

Sold merchandise on account.

Cost of Good Sold

Cash

9 3,800

Accounts Payable (Owatonna Tool Co.) 3,800

Purchased merchandise on credit.

To record the cost of goods sold relating to the

sales of merchandise to Bemidji Construction.

c.

Claypool Industry

Hardware Average Difference

$1,024,900 $1,000,000 $24,900

To have a higher-than-average cost of goods sold and still earn a much larger-than-

average amount of gross profit, Claypool must be able to charge substantially higher

Annual sales ……………………………..

PROBLEM 6.1A

CLAYPOOL HARDWARE (concluded)

Claypool seems quite able to pass its extra transportation costs on to its customers and, in

fact, enjoys a significant financial benefit from its remote location. The following data

support these conclusions:

Gross profit ………………………………

Gross profit rate …………………………

a.

271,200$

3,000

268,200

120,690

147,510

300$

c.

d.

e.

PROBLEM 6.2A

HENDRY’S BOUTIQUE

Sales

HENDRY’S BOUTIQUE

For the Year Ended December 31, Current Year

Income Statement

15 Minutes, Easy

The use of the Purchase Discounts Lost account indicates that the store records

would have appeared in the adjusted trial balance instead.

The $3,840 of sales taxes payable appearing in the adjusted trial balance represents sales

Net sales

Cost of goods sold

Gross profit

Other expenses:

b.

Gross profit Net sales = gross profit margin

Less: Sales returns and allowances

Purchase discounts lost

9,828

Rent expense

Insurance expense

Salaries expense

Utilities expense

Office supply expense

Net income

Income tax expense

Depreciation expense: office equipment

Income before income taxes expense

Year 2-Year 3 Year 1-Year 2

1. 6% (1) 8% (2)

b.

PROBLEM 6.3A

KNAUSS SUPERMARKETS

20 Minutes, Medium

While Knauss has increased its overall revenue from sales, several of the statistics indicate

a.

Change in net sales …………………….

2. (1.1%) (3) (2.7%) (4)

3. (1.8%) (5) (3.5%) (6)

Change in net sales per square foot ….

Change in comparable store sales ……

30 Minutes, Medium

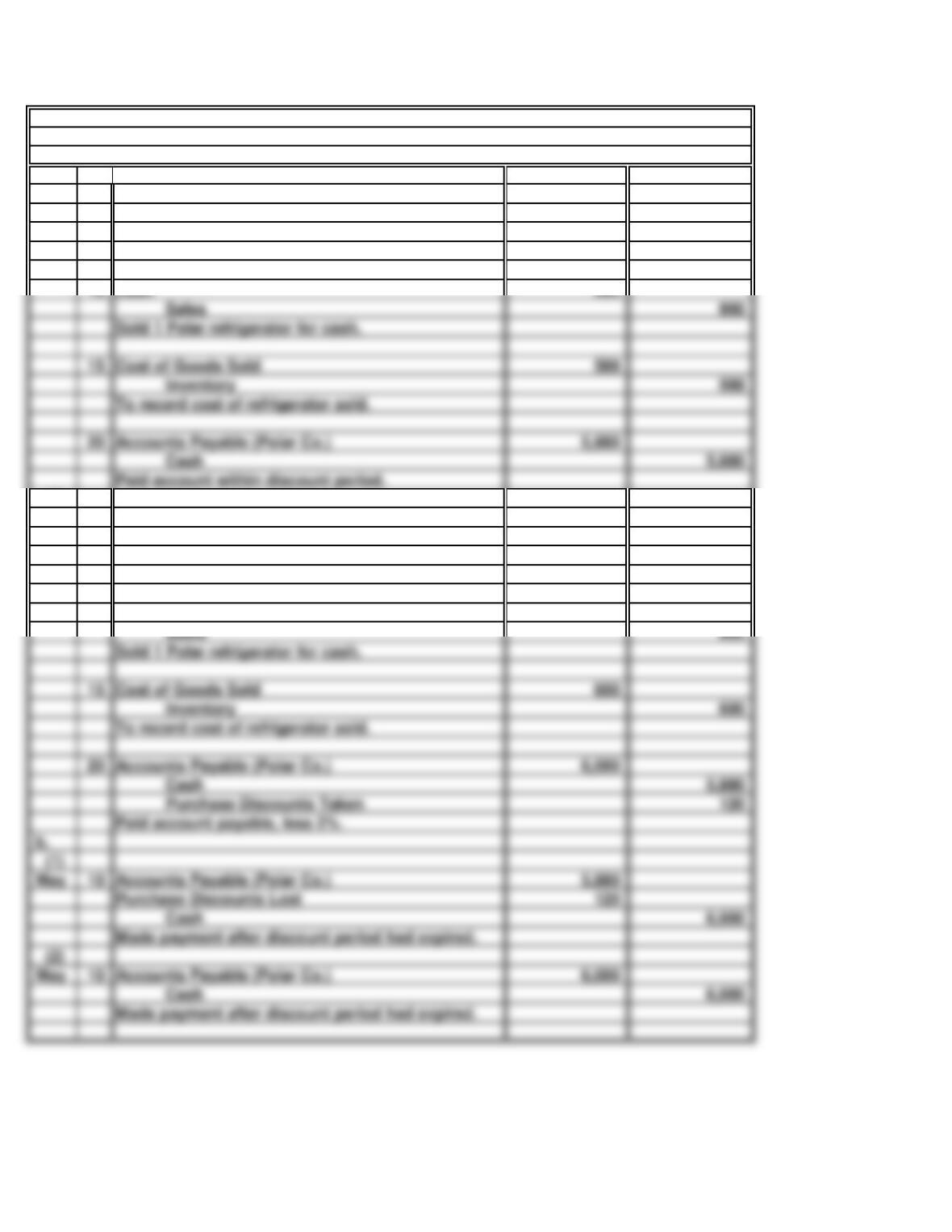

Date

(1)

April 10 5,880

Accounts Payable (Polar Co.) 5,880

(2)

April 10 6,000

Accounts Payable (Polar Co.) 6,000

15 900

15 600

b.

(1)

May 10 5,880

(2)

May 10 6,000

Cost of Goods Sold

Accounts Payable (Polar Co.)

Made payment after discount period had expired.

Accounts Payable (Polar Co.)

Purchase Discounts Lost

Made payment after discount period had expired.

Paid account payable, less 2%.

Sold 1 Polar refrigerator for cash.

Accounts Payable (Polar Co.)

To record cost of refrigerator sold.

To record purchase of 10 refrigerators at gross

invoice price ($600 per unit).

Cash

Inventory

PROBLEM 6.4A

a.

General Journal

KITCHEN ELECTRICS

$588 per unit ($600, less 2%).

Inventory

To record purchase of 10 refrigerators at net cost of

15 900

15 588

Cash

Sold 1 Polar refrigerator for cash.

Cost of Goods Sold

To record cost of refrigerator sold.

Accounts Payable (Polar Co.)

Paid account within discount period.

c.

PROBLEM 6.4A

KITCHEN ELECTRICS (concluded)

The net cost method provides more useful information for evaluating the company’s

efficiency in paying its bills. This method clearly indicates the lowest price that the

30 Minutes, Strong

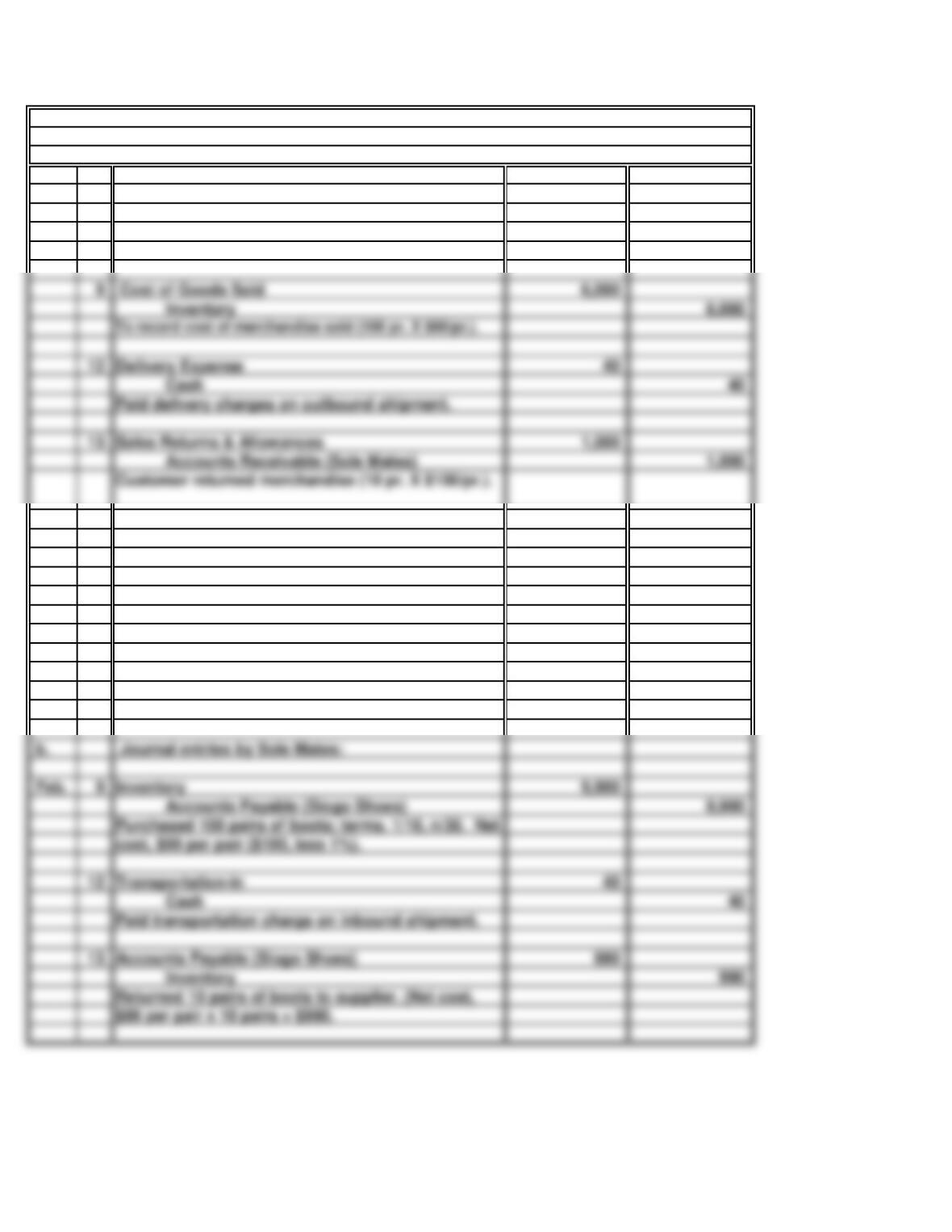

a. Journal entries by Siogo Shoes:

Feb . 9 10,000

Sales 10,000

13 600

Cost of Goods sold 600

19 8,910

90

Accounts Receivable (Sole Mates) 9,000

b.

Feb. 9 9,900

Accounts Payable (Siogo Shoes) 9,900

12 40

Cash 40

Inventory 990

Paid transportation charge on inbound shipment.

Inventory

cost, $99 per pair ($100, less 1%).

Journal entries by Sole Mates:

Returned 10 pairs of boots to supplier. (Net cost,

Purchased 100 pairs of boots; terms. 1/10, n/30. Net

Transportation-in

Accounts Payable (Siogo Shoes)

$99 per pair x 10 pairs = $990.

PROBLEM 6.5A

returned (10 pr. X $60/pr.).

Cash

Collected amount due, less $1,000 return and less

Reduce cost of goods sold for cost of merchandise

SIOGO SHOES AND SOLE MATES

Accounts Receivable (Sole Mates)

Sold merchandise on account; terms, 1/10, n/30.

1% cash discount on remaining $9,000 balance.

General Journal

Inventory

Sales Discount

13 1,000

Accounts Receivable (Sole Mates) 1,000

Cost of Goods Sold

Paid delivery charges on outbound shipment.

Sales Returns & Allowances

Delivery Expense

Feb .

19

8,910

Cash 8,910

c.

PROBLEM 6.5A

General Journal

SIOGO SHOES AND SOLE MATES (concluded)

Yes. Sole Mates should take advantage of 1/10, n/30 purchase discounts, even if it must

Accounts Payable (Siogo Shoes)

Siogo Shoes ($9,900 – $990 = $8,910).

Paid within discount period balance owed to

60 Minutes, Strong

a.

Jan. 10 9,800

Cash……………………………………. 9,800

Purchase of $20,000 of books net of the purchase

Entries that Should Have Been Recorded by the Accounting Clerk

Jan. 10 Accounts Payable……………………………….. 9,800

Cash……………………………………. 9,800

a.1.

PROBLEM 6.6A

KING ENTERPRISES

The easiest way for a student to solve this problem is to record the journal entries that the

accounting clerk made and to compare them with the journal entries that should have

been made.

Entries Recorded by the Accounting Clerk

Based on a comparison of the above entries, accounts receivable is understated by

$30,000.

Payment for books received on December 15th of

prior year.

Inventory…………………………………………

Payment for books received on December 15th of

30,000

d.

Accounts receivable………………………………… 30,000

e.

PROBLEM 6.6A

KING ENTERPRISES (concluded)

The journal entry to correct the accounting clerk’s errors is (assuming that King’s books

have yet to be closed for the year).

The journal entry to correct the accounting clerk’s errors assuming that the ending

Accounts receivable………………………………..

c.

The journal entry to correct the accounting clerk’s errors is (assuming that King’s books

have been closed for the year).

24,500

Cost of goods sold………………………………….

30 Minutes, Strong

a.

$ 630,000

c.

d.

Inventory…………………………………………………………..

180,000

Revaluation of Inventory to Market Value.. 180,000

PROBLEM 6.7A

THOMPSON PLUMBING

The difference between the $210,000 of gross profit under accrual accounting and the

negative $240,000 gross profit under a cash-basis system reflects the balances in the

Sales ($180,000 + $450,000)

(420,000)

$ 210,000

Gross profit

Cost of goods sold ($120,000 + $300,000)

a.

f.

g.

Gross profit = Sales price – Cost of goods sold

CPI probably would use a perpetual inventory system. The items in its inventory have a

Computation of profit margin on January 6 sales transaction:

40 Minutes, Strong

PROBLEM 6.8A

CPI

Parts a, f, and g follow; parts b, c, d, and e are on the next page.

The operating cycle of a merchandising company consists of purchasing merchandise,

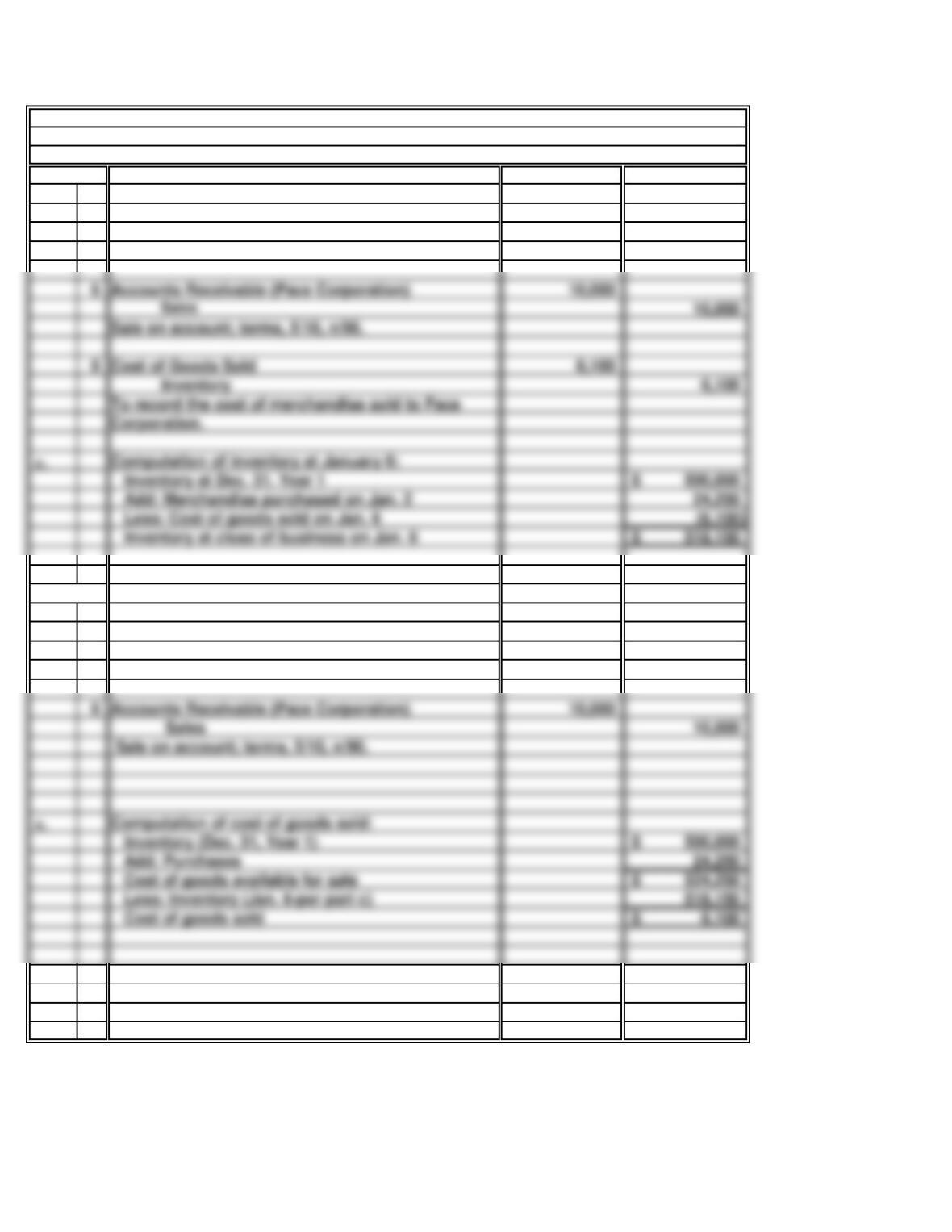

Jan 2 24,250

Accounts Payable (Sharp) 24,250

d.

Jan 2 24,250

Accounts Payable (Sharp) 24,250

Sales 10,000

500,000$

24,250

518,150

Add: Purchases

Less: Inventory (Jan. 6-per part c)

Cost of goods available for sale

Cost of goods sold

Inventory (Dec. 31, Year 1)

Computation of cost of goods sold:

Accounts Receivable (Pace Corporation)

Sale on account; terms, 5/10, n/90.

PROBLEM 6.8A

b.

Year 2

General Journal

CPI (concluded)

n/60. Net cost, $25,000, less 3%.

Inventory

Purchased merchandise on account; terms, 3/10,

Purchases

n/60. Net cost, $25,000, less 3%.

Purchased merchandise on account; terms, 3/10,

Journal entries assuming use of periodic system:

Year 2

500,000$

24,250

Sale on account; terms, 5/10, n/90.

Cost of Goods Sold

Accounts Receivable (Pace Corporation)

Inventory at close of business on Jan. 6

Less: Cost of goods sold on Jan. 6

To record the cost of merchandise sold to Pace

Add: Merchandise purchased on Jan. 2

Corporation.

Computation of inventory at January 6:

Inventory at Dec. 31. Year 1

35 Minutes, Medium

Apr 15 19,700

Sales 19,700

May 10 19,700

Accounts Receivable 19,700

Inventory per accounting records 116,500$

Inventory per physical count 114,000

Adjustment for inventory shrinkage 2,500$

Cost of Goods Sold

To adjust inventory records to reflect the results

of the year-end physical count.

Accounts Payable

Paid account payable to supplier.

b.

1,422,000$

723,500

698,500$

723,500$

Add: Shrinkage adjustment at Dec. 31

(1) Cost of goods sold prior to adjustment at Dec. 31

Cost of goods sold (adjusted balance)

SOLUTIONS TO PROBLEMS SET B

Accounts Receivable

Sold merchandise on account.

For the Year Ended December 31, Current Year

Cash

PROBLEM 6.1B

a.

BIG OAK LUMBER

General Journal

Net sales

Cost of goods sold (1)

Gross profit

Partial Income Statement

Collected accounts receivable.

BIG OAK LUMBER

Accounts Payable 3,700

Cost of Good Sold

To record the cost of goods sold relating to the

sales of merchandise to Hard Hat Construction.

Purchased merchandise on credit.

c.

Big Oak Industry

Lumber Average Difference

$1,422,000 $1,000,000 $422,000

PROBLEM 6.1B

BIG OAK LUMBER (concluded)

Big Oak seems quite able to pass its extra transportation costs on to its customers and, in

fact, enjoys a significant financial benefit from its remote location. The following data

support these conclusions:

Annual sales ……………………………..

Gross profit ………………………………

Gross profit rate …………………………

a.

460,800$

4,800

456,000

189,156

c.

d.

e.

The use of the Purchase Discounts Lost account indicates that the store records

would have appeared in the adjusted trial balance instead.

The $6,000 of sales taxes payable appearing in the adjusted trial balance represents sales

taxes collected by the store for the sales taxes imposed on its customers . When the store

1%).

Net sales

PROBLEM 6.2B

HARRY’S HABERDASHERY

Sales

HARRY’S HABERDASHERY

For the Year Ended December 31, Current Year

Income Statement

15 Minutes, Easy

Less: Sales returns and allowances

Cost of goods sold

Salaries expense

Rent expense

Insurance expense

Net income

Income tax expense

Depreciation expense: office equipment

Income before income taxes expense

Other expenses:

Purchase discounts lost

Utilities expense

Office supply expense

Gross profit