CCC6 CONTINUING COOKIE CHRONICLE

(a)

Feb. 2

Purchases …………………………………………

1,150

Accounts Payable ………………………

1,150

16

Cash …………………………………………………

1,100

Sales Revenue …………………………...

1,100

25

Accounts Payable ……………………………..

1,150

Cash ………………………………………….

1,150

Mar. 2

Purchases …………………………………………

Accounts Payable ………………………

30

Cash …………………………………………………

2,200

Sales Revenue …………………………...

2,200

31

Accounts Payable ……………………………..

Cash ………………………………………….

Apr. 1

Purchases …………………………………………

1,172

Accounts Payable ………………………

1,172

13

Cash …………………………………………………

3,300

Sales Revenue …………………………...

3,300

Accounts Payable ……………………………..

1,172

Cash ………………………………………….

1,172

May 4

Purchases …………………………………………

1,800

Accounts Payable ………………………

1,800

27

Cash …………………………………………………

1,100

Sales Revenue …………………………...

1,100

CONTINUING COOKIE CHRONICLE (Continued)

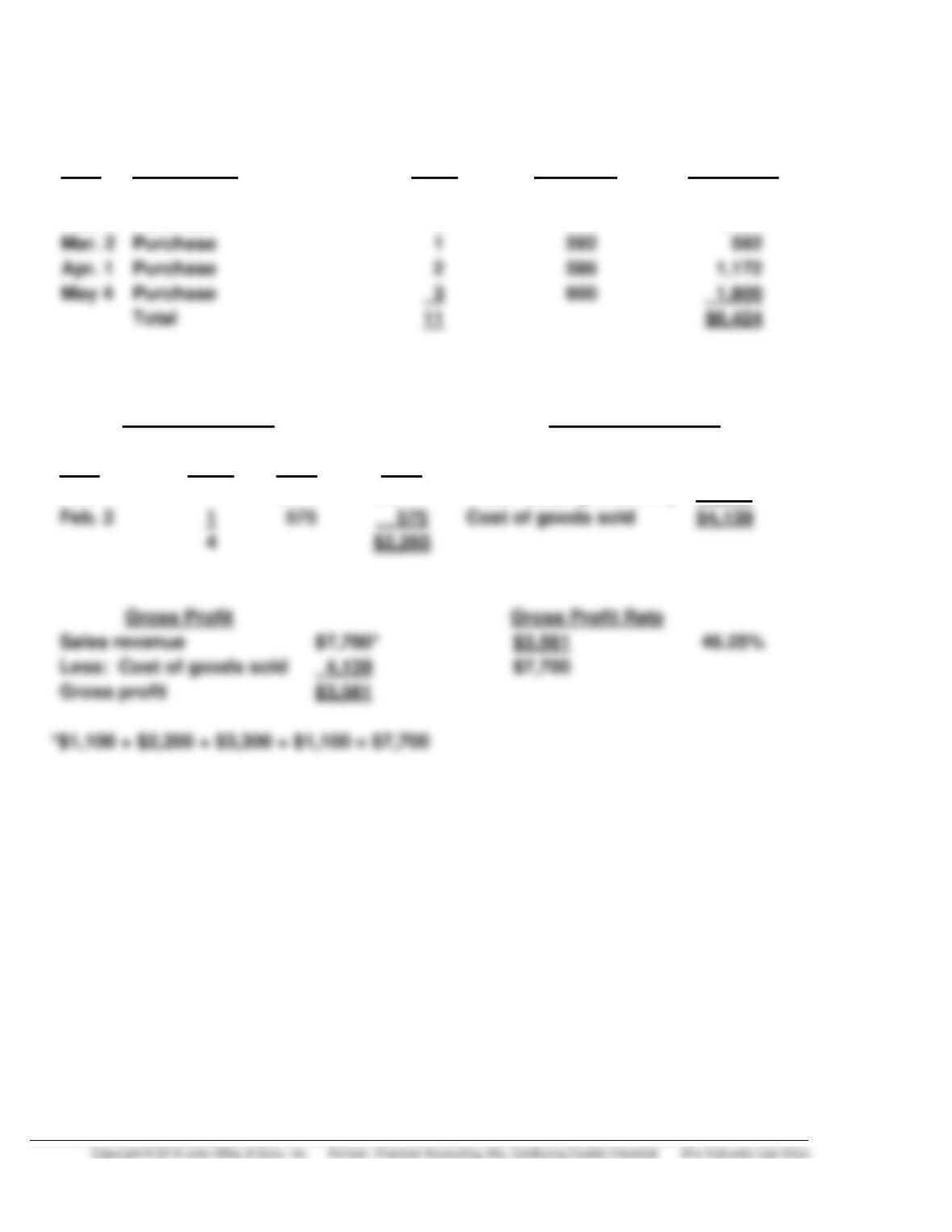

(b) COST OF GOODS AVAILABLE FOR SALE

Date

Explanation

Units

Unit Cost

Total Cost

Feb. 1

Beginning Inventory

3

$570

$1,710

Feb. 2

Purchase

2

575

1,150

Mar. 2

Purchase

1

592

592

Apr. 1

Purchase

2

586

1,172

May 4

Purchase

3

600

1,800

Total

$6,424

(c)

LIFO

Ending Inventory

Cost of Goods sold

Date

Units

Unit

Cost

Total

Cost

Cost of goods

available for sale

$6,424

Feb. 1

3

$570

$1,710

Less: Ending inventory

2,285

Feb. 2

1

Cost of goods sold

$4,139

4

$2,285

Gross Profit Rate

Less: Cost of goods sold

4,139

$7,700

Gross profit

$3,561

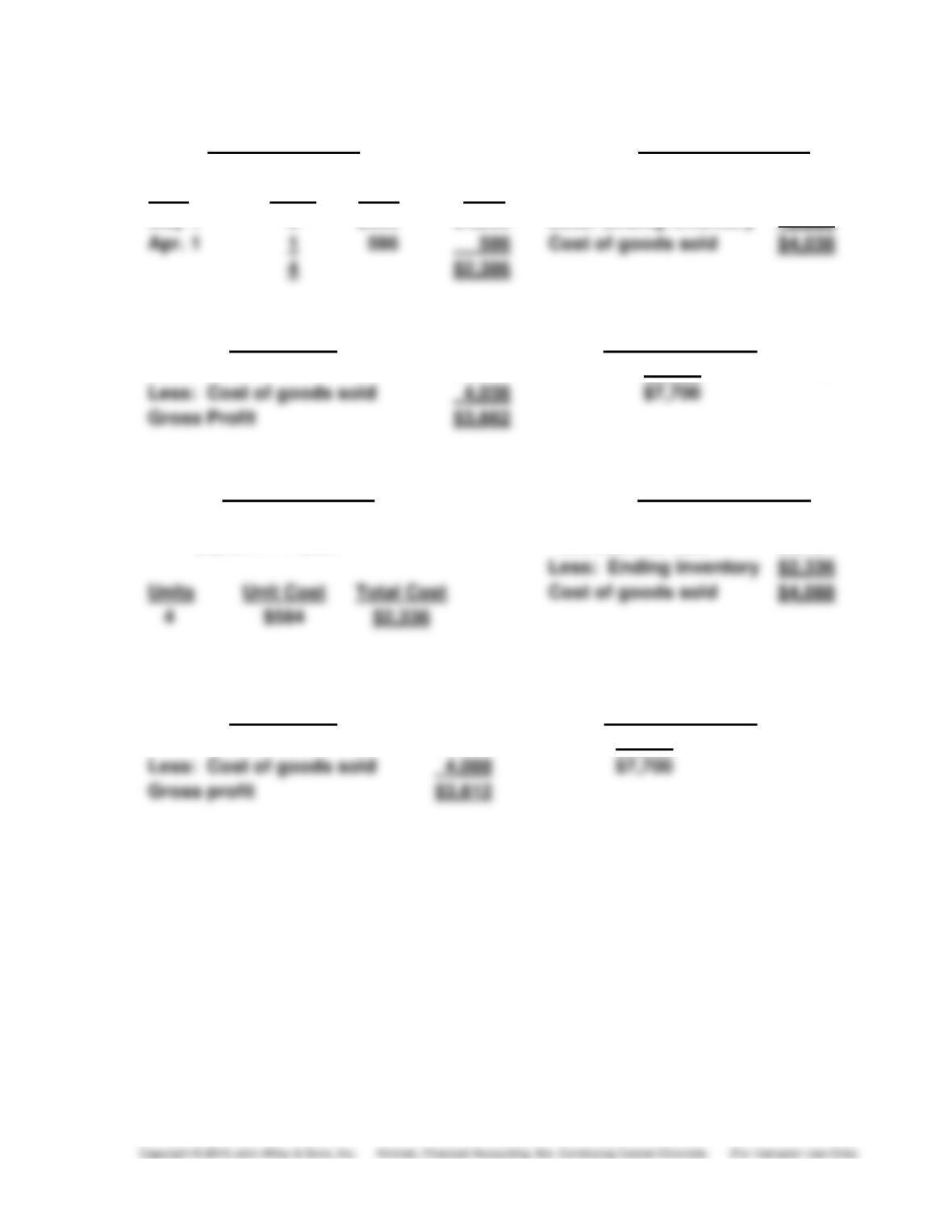

CONTINUING COOKIE CHRONICLE (Continued)

FIFO

Ending Inventory

Cost of Goods sold

Date

Units

Unit

Cost

Total

Cost

Cost of goods

available for sale

$6,424

May 4

3

$600

$1,800

Less: Ending inventory

2,386

Apr. 1

1

586

Cost of goods sold

$4,038

4

$2,386

Gross Profit

Gross Profit Rate

Sales revenue

$7,700

$3,662

47.56%

Less: Cost of goods sold

$7,700

Gross Profit

$3,662

Average Cost

Ending Inventory

Cost of Goods Sold

$6,424/11 = $584

Cost of goods

available for sale

$6,424

Less: Ending inventory

$2,336

Units

Cost of goods sold

$4,088

$2,336

Gross Profit

Gross Profit Rate

Sales revenue

$7,700

$3,612

46.91%

Less: Cost of goods sold

4,088

$7,700

Gross profit

$3,612

CONTINUING COOKIE CHRONICLE (Continued)

(d) It should not actually matter which cost flow assumption Natalie chooses

for the purpose of the bank loan. Bankers should be able to recognize