Reporting Cash Flows 151

P5–11 Office Decor Company

Statement of Cash Flows

For the Year Ended December 31, 2007

(in thousands)

Operating Activities

Net income $ 2,000

Increase in accounts receivable (2,400)

Office Decor reported net income of $2,000,000 for 2007. The compa-

ny’s cash flow from operating activities was a cash outflow of $3,600,000,

however. Thus, though the company appears to be profitable, it may be

P5–12 A. McDonald’s cash and cash equivalents increased $887 million during

2004.

B. The primary sources of cash were profitable operations. Other

sources of cash include sales of restaurant property, long-term and

short-term financing, and proceeds from the exercise of stock op-

tions.

152 Chapter 5

D. Depreciation and amortization are noncash expenses that reduce net

E. An increase in accounts receivable means that credit sales exceeded

F. Purchases of property and equipment are listed as investing activi-

ties because cash was used to purchase long-term (capital) assets.

H. The company is not facing a cash flow problem. The ending cash

balance has grown in each year presented. In addition, the company

produced enough cash from operations in 2004 and 2003 to provide

for its investing and financing activities.

P5–13 There are three primary factors that caused the rapid decrease in cash

provided by operating activities. First, the company’s profits have fallen

Reporting Cash Flows 153

P5–14 Items from the income statement (IS) and cash flow from operating activi-

ties (CF) can be used to answer each question (in millions):

A. Revenues (IS) $ 24,547

Increase in accounts receivable (27)

P5–15 The cash flow patterns of Dell and Apple Computer are remarkably simi-

lar. For example, both companies earned a positive net income during the

year. In addition, both companies increased the account balance of ac-

P5–16 A. False. Depreciation expense is added to net income because depre-

ciation reduces net income but not cash flow. Therefore, to deter-

154 Chapter 5

C. False. An increase in accounts payable indicates that some of the

E. True. Gamma’s operating activities are generating a negative cash

flow. (Note: The $80 is a net outflow—“Net cash for operating activi-

Reporting Cash Flows 155

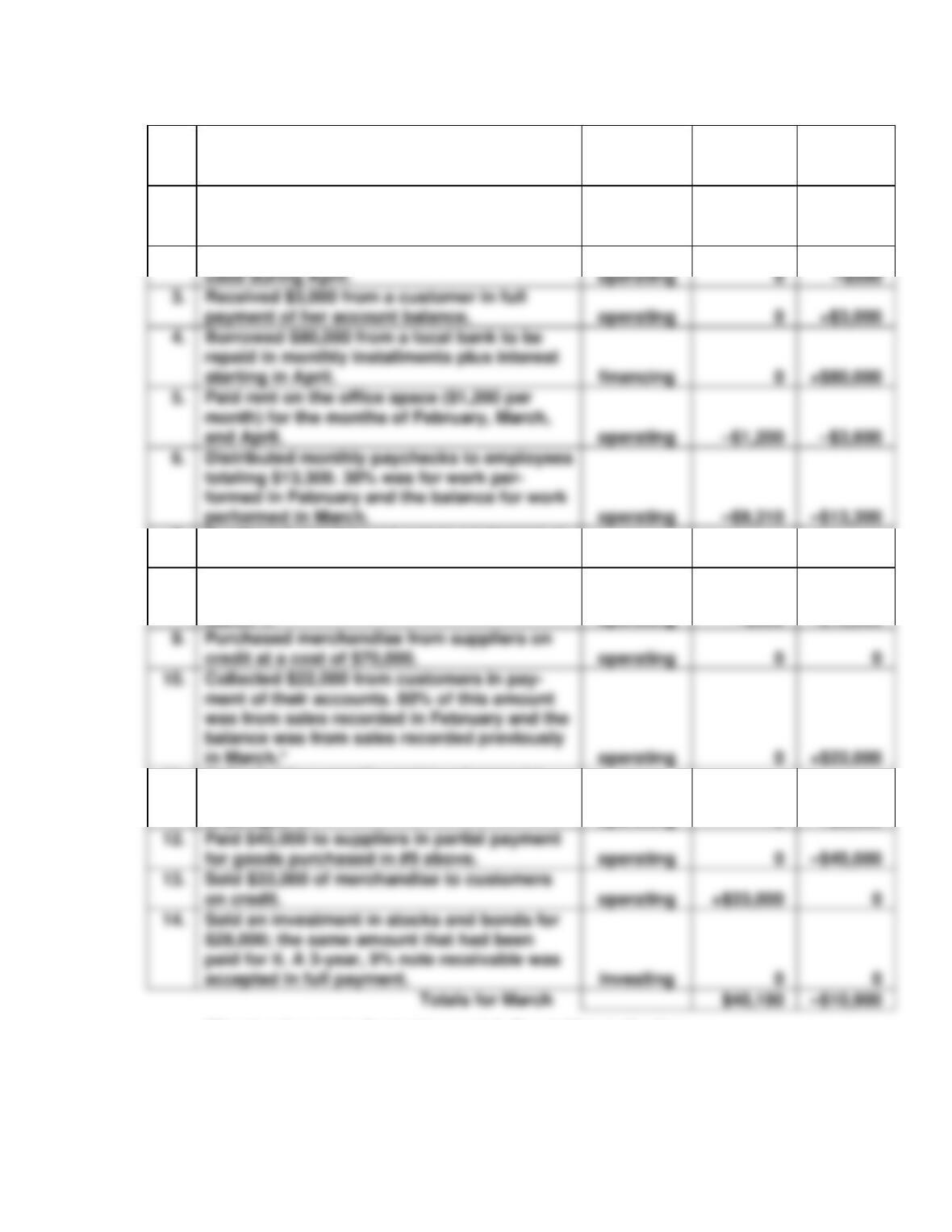

P5–17 A. and B.

Event

Type

of Activity

Effect on

March’s

Net Income

Effect on

March’s

Cash Flow

1.

Sold $18,000 of goods on credit to custom-

ers. Received a 25% down payment with the

balance on account.

operating

+$18,000

+$4,500

2.

Paid $500 cash for office supplies that will be

7.

Purchased new Internet server equipment at

a cost of $50,000.

investing

0

–$50,000

8.

Purchased a 3-year fire insurance policy at a

total cost of $10,800. Its coverage began on

March 1.

operating

–$300

–$10,800

9.

Purchased merchandise from suppliers on

credit at a cost of $70,000.

operating

operating

11.

Collected four months rent in advance (at

$700 per month) from a tenant who will move

in on April 1.

operating

0

+$2,800

Paid $45,000 to suppliers in partial payment

operating

–$45,000

on credit.

operating

paid for it. A 3-year, 9% note receivable was

accepted in full payment.

investing

0

–$10,900

*March sales are indicated in event 1. Event 10 is indicating

collection of some of the receivables from those sales. (continued)

C. Student responses will vary. One possible response is as follows. It

is foolish to try to manage an organization with accrual-basis ac-

operating

0

3.

Received $3,000 from a customer in full

operating

0

+$3,000

starting in April.

5.

Paid rent on the office space ($1,200 per

operating

totaling $13,300. 30% was for work per-

performed in March.

operating

–$13,300

156 Chapter 5

counting information only. As illustrated by this problem, a company

P5–18 Sheik Company: Sheik’s cash flow information is characterized by

steady and reliable cash flow from operations over the

Speer Company: Speer’s cash flow information is not encouraging.

First, cash flow from operations has swung from quite

favorable 5 years ago to quite unfavorable today. If this

Love Company: Love’s cash flow from operations is growing rapidly.

While smaller than the other two firms, it is growing

the most rapidly. Further, the company appears to plan

on even more expansion as the investment in new

Reporting Cash Flows 157

P5–19 A. The primary source of cash inflow was $1,014 provided by an in-

crease in long-term debt. Operating activities provided $278 and the

sale of investments provided $206.

D. Receivables decreased; the cash inflow from customers was greater

P5–20 A. 1. Net income: The purpose of the operating activities

section under the indirect format is to

show why cash flow differed from net in-

2. Depreciation expense: Depreciation expense consumes zero

cash. Therefore, the entire amount of de-

B. 1. Accounts receivable: The increase in accounts receivable bal-

ance is deducted from net income be-

158 Chapter 5

2. Inventory: The decrease in inventory is added to net

income because some of the inventory

3. Prepaid advertising: The increase in prepaid advertising is

4. Rent payable: The decrease in rent payable is deducted

from net income because cash payments

5. Wages payable: The increase in wages payable is added

to net income because not all wages

D. 1. Buildings and equipment: The increase in account balance dur-

ing the year indicates that additional

2. Land: The increase in the account balance

3. Investments, long-term: The decrease in the account balance

indicates that a portion of investments

Reporting Cash Flows 159

F. 1. Notes payable, long-term: The increase in the account balance

2. Common stock: The increase in the account balance

3. Retained earnings: Although retained earnings itself does

not appear on the cash flow state-

P5–21 A. Beltway Distributors, Inc.

Statement of Cash Flows

For the Year Ended January 30, 2007

(In thousands)

Operating Activities

Net income $ 5,300

Add/Deduct:

Depreciation expense 2,900

B. It appears that the company is slowly decreasing the size of its oper-

ations. No new investment in long-term assets is occurring. Cash

P5–22 The Book Wermz

Statement of Cash Flows

For the Month Ended November 30, 2007

Direct Method Indirect Method

Operating Cash Flow: Operating Cash Flow:

From customers $ 45,003.48 Net income $ 2,447.45

Financing Cash Flow: Financing Cash Flow:

Payment of debt (1,122.77) Payment of debt (1,122.77)

P5–23

1

2

3

4

5

6

7

8

9

10

Reporting Cash Flows 161

CASES

C5-1 A. The three categories of cash flows are from operating activities, in-

C. In years 2004 and 2003, cash flows from operating activities were

sufficient to meet cash flow needs for investing activities. The ex-

cess cash flow generated by operating activities was used to reduce

C5-2 A. General Mills’ operating activities during 2004 included sales of

goods for $11,070 million that cost the company $6,594 million. Sell-

ing and administrative activities resulted in expenses of $2,443 mil-

B. 2004 2003

Return on total assets 5.7% 5.0%

($1,055 ÷ $18,448) ($917 ÷ $18,227)

Return on assets improved from 2003 to 2004.

162 Chapter 5

E. In 2004, the company used cash to reduce notes payable. Manage-

bly in connection with the acquisition of Pillsbury).

F. The company’s most important reported assets were goodwill and

C5-3 A. General Mills’ statement of cash flows reveals that its net earnings

B.

Increased

Decreased

Cash

Inventories

Accounts receivable

Deferred income taxes

Prepaid expenses

Accounts payable

Current portion of long-term debt

Notes payable

Other current liabilities

Beginning accounts receivable $ 980

(plus) Sales 11,070

Reporting Cash Flows 163

C. The overall trend in operating cash flow is positive; however, cash flow

from operating activities declined in 2004. Also, cash flow from operat-

C5-4 A. The statements are similar in that both report the results of operat-

ing, investing, and financing activities. The differences between the

which cash is paid during a period.

B. The reconciliation of net income to cash flow provided by operating ac-

tivities looks like the indirect format of the operating activities section.

C. Student responses may differ. Most will argue in favor of the direct

164 Chapter 5

COMPREHENSIVE REVIEW

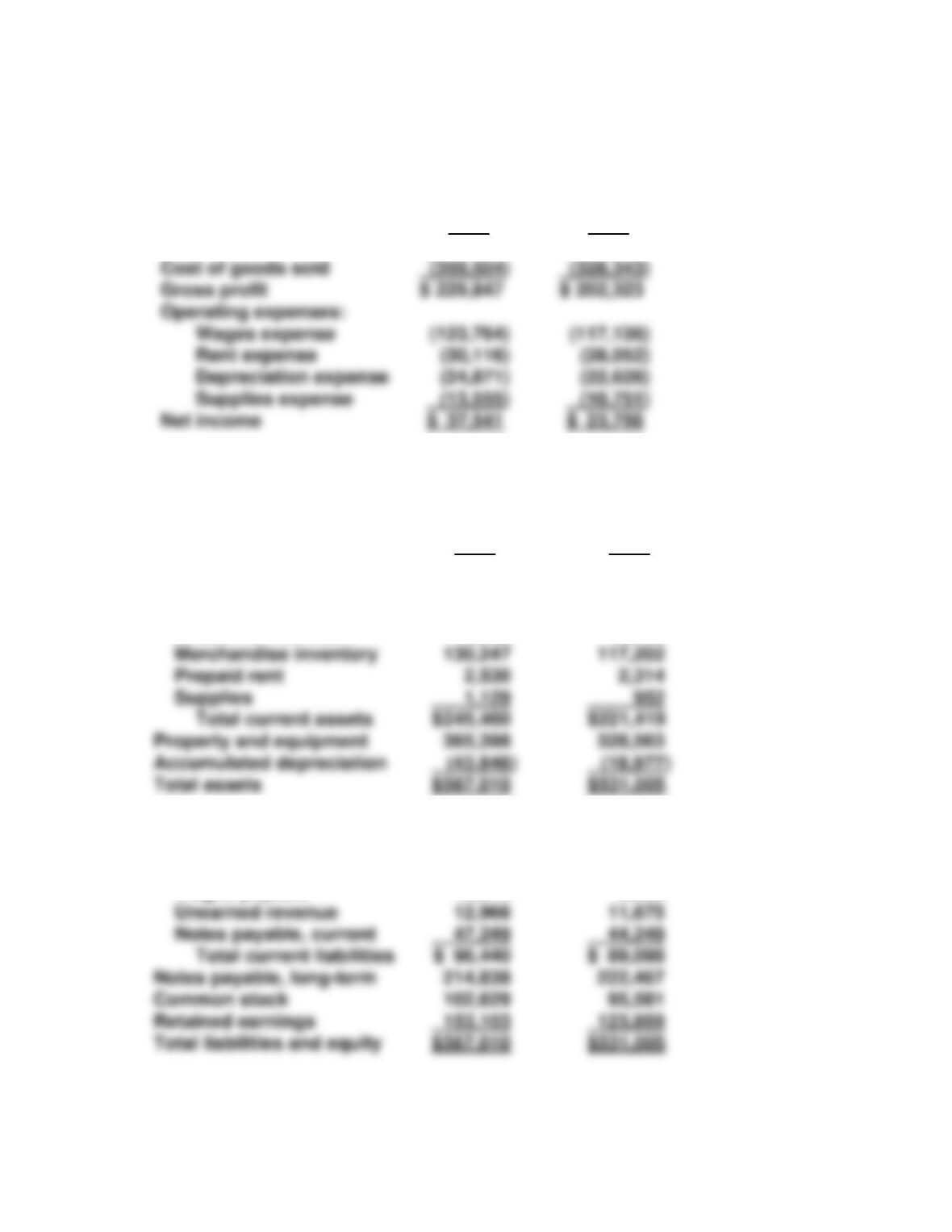

A. Alice Springs Merchandise

Income Statement

For the Year Ended January 31

2007 2006

Sales revenue $ 589,351 $ 530,666

B. Alice Springs Merchandise

Balance Sheet

At January 31

2007 2006

Assets

Current assets:

Cash $ 63,168 $ 57,845

Accounts receivable 48,386 43,106

Liabilities and Equity

Current liabilities:

Accounts payable $ 25,953 $ 23,674

Wages payable 10,272 9,500

Reporting Cash Flows 165

C. Accrual Adjustments Cash Flow

Sales revenue $589,351

Accounts receivable $ (5,280)

Unearned revenue 1,291

Cash collected from customers $ 585,362

Depreciation expense (24,871)

Adjustment for noncash expense 24,871

Cash paid for depreciation 0

Supplies expense (13,555)

(continued)

166 Chapter 5

D. Alice Springs Merchandise

Statement of Cash Flows

For the Year Ended January 31, 2007

Operating Activities:

Net cash from operating activities 48,036

Investing Activities:

Paid for property and equipment (38,802)

Dividends paid (8,297)

Net cash for financing activities (5,878)

Reporting Cash Flows 167

E. Alice Springs Merchandise

Statement of Cash Flows

For the Year Ended January 31, 2007

Operating Activities:

Net income $ 37,541

Adjustments:

Supplies (177)

Net cash from operating activities 48,036

Investing Activities:

Paid for property and equipment (38,802)