131

CHAPTER 5

Reporting Cash Flows

THINKING BEYOND THE QUESTION

How is cash flow information determined and reported to external users?

A business can fail when it has insufficient cash to pay for its resource

QUESTIONS

Q5-1 The direct format statement of cash flows answers the questions “where

Q5-2 The acquisition of machinery typically involves cash. Nevertheless, the

acquisition of machinery is always an investing activity. How it was paid

Q5-3 GAAP require that the issuance of either debt or equity in exchange for

long-term assets be disclosed, but not necessarily on the statement of

132 Chapter 5

Q5-4 The usual presentation of investing activity and financing activity infor-

Q5-5 Interest is included as an operating activity because interest expense is

included on the income statement. The FASB decided that cash paid for

Q5-6 The indirect format is a reconciliation of revenues and expenses meas-

ured by accrual accounting (net income) and revenues and expenses

Q5-7 When the balance in accounts receivable increases during a fiscal period,

it means that new sales on credit have exceeded the amount of cash col-

Q5-8 The operating section of the indirect method statement of cash flows an-

swers the question “what caused net income for the period to be different

from net cash flow?” The investing and financing sections report sources

Q5-9 To grow significantly, a company usually must expand its set of operating

assets such as land, buildings, and machinery. The acquisition of these

Reporting Cash Flows 133

Q5–10 Operations consist of the primary activities that the company was set up

to perform. If the firm’s primary operations consume cash, rather than

generate it, the company cannot survive in the long run. Another way of

Q5–11 When cash flow from investing activities is positive, it means that the

company is selling off its long-term assets and reducing its productive

Q5–12 The most frequent uses of cash generated by operations are as follows:

a. payment of dividends

Q5–13 There are two possibilities. First, the company may be so profitable that it

can finance all growth out of operating cash flow and still have cash left

Q5–14 It suggests that this company is in serious difficulty. To observe this sit-

uation in any one year is bad enough; to see it consistently over a

3-year period is very worrisome. First, the inability to generate cash from

134 Chapter 5

Q5–15 For most corporations, two of the major differences between net income

and cash flow from operating activities are depreciation and amortization.

These often are large expenses on the income statement but do not re-

Q5–16 First, a company that does not have profitable opportunities in which to

EXERCISES

E5-1 a. Operating Activities:

Received from customers $ 87,500

b. Financing Activities:

Received from issuing long-term debt $ 23,000

Paid to owners (12,000)

Net cash flow from financing activities $ 11,000

Reporting Cash Flows 135

E5–2

Item

Type of Activity

Add or Subtract

a.

Purchase of plant assets

Investing

Subtract

b.

Cash paid to suppliers

Operating

Subtract

E5–3 Cash collected from customers $247,000

Cash paid to suppliers (81,400)

E5-4 a. $17,700; Cash received from customers $187,200

Cash paid to suppliers of inventory (119,850)

Cash paid to employees (31,500)

E5-5 a. Cash flows from financing activities:

Debt issued $ 13,057

Payments of debt (83,000)

c.

Cash collected from customers

Operating

Add

d.

Payment of long-term debt

Financing

Subtract

e.

Net income

Not included

Not included

Depreciation expense

Not included

Not included

g.

Payment of dividends

Financing

Subtract

h.

Issuing stock

Financing

Add

Cash paid to employees

Operating

Subtract

Cash paid for income taxes

Operating

Subtract

k.

Disposal of plant assets

Investing

Add

136 Chapter 5

E5-6 a. D

b. I

E5-7

Statement Statement Added or

Section Format Subtracted?

1. Decrease in taxes payable O I −

2. Cash paid to suppliers of inventory O D −

E5-8

Item

Type of

Activity

Add or

Subtract

a.

Purchase of plant assets

Investing

Subtract

b.

Increase in accounts payable

Operating

Add

Decrease in accounts receivable

Operating

Add

d.

Payment of long-term debt

Financing

Subtract

e.

Net income

Operating

Add

Depreciation expense

Operating

Add

Payment of dividends

Financing

Subtract

h.

Issuing stock

Financing

Add

Increase in inventory

Operating

Subtract

Decrease in taxes payable

Operating

Subtract

Disposal of plant assets

Investing

Add

Reporting Cash Flows 137

E5-9 Net income ($17,000 − $8,000)* $ 9,000

Depreciation expense 1,100

Patent amortization expense 250

E5–10 a. Cash paid to suppliers $37,500

Decrease in accounts payable (3,000)

b. Interest paid $ 4,000

Interest payable decreased (1,200)

Interest expense $ 2,800

d. Cash collected from customers $ 27,000

E5–11 a. Net cash flow from operations $ 30,000

Noncash revenues 11,000

138 Chapter 5

b. Wages expense $ 69,000

increased during a period.

c. Sales revenue $ 241,000

Cash collected from customers (224,500)

d. Net income $ 45,000

E5–12

Account Balance

Adjustment and Reason

a.

Accounts receivable

increased $10,000

Subtract $10,000 from net income because

cash collected from customers was $10,000

Reporting Cash Flows 139

f.

Prepaid insurance

decreased $22,000

Add $22,000 to net income because insur-

ance was consumed (increase in expense

and decrease in net income) that was not

paid for during the period.

E5–13 Cash flow from operating activities (in millions):

Net earnings $3,458

Depreciation and amortization 1,412

E5–14 (date)

Martha Rosenbloom

945 Oak Lane

Anytown, USA

Dear Ms. Rosenbloom:

Our mutual friend, Mr. Arthur Doyle, has asked if I can provide you assis-

tance in understanding the statement of cash flows in corporate annual

140 Chapter 5

Differences also exist between the amount of revenue or expense rec-

ognized during a period and the amount of cash flow for items such as

The cash flow statement provides an indirect calculation of cash from

operating activities by adjusting net income for amounts on the income

statement that do not affect cash. These noncash items include deprecia-

E5–15 a. The additions and subtractions are caused by events in which the

amount of revenue or expense generated was different from the

b. 1. Depreciation expense is added because it decreased net income

but did not affect cash.

2. If accounts receivable increased by $2,500, this means that sales

3. If inventory increased, this means that more inventory was pur-

4. A decrease in accounts payable means the company paid more

cash to suppliers than the amount of expense reflected in cost of

Reporting Cash Flows 141

E5–16 a. Co. B had the largest cash flow from operating activities at $15,200.

Co. C had the smallest at $2,304.

b. Cash flow associated with investing activities should be negative

E5–17 Landsdowne Company has shown a steady increase in net income over

the six-year period, with the exception of year 6. Its cash flow from oper-

ating activities has steadily declined since year 2, however. The differ-

ence between net income and cash flow can be explained by the increas-

E5–18 Sommer Company has incurred losses in its last two years of operations.

Without the large amount of depreciation recorded each year, the compa-

ny would have had net income in each year. The company has maintained

a steady growth in cash flows from operating activities. These cash flows

142 Chapter 5

E5–19

Account and balance

Anticipated future event and cash flow

a.

Accounts receivable,

$12,000

$12,000 cash should be received from cus-

tomers during the next fiscal year. Operat-

ing activities section.

e.

Accounts payable, $6,500

Currently, $6,500 is owed to short-term

creditors that will be repaid during the

next fiscal year. Operating activities sec-

tion.

g.

Notes payable, long-term,

$88,000

The company borrowed $88,000 in the past

and is expected to repay it sometime after

the next fiscal year. A financing activity.

(Any interest paid on the borrowing ap-

pears in the operating activities section.)

Taxes payable, $7,800

Currently the company owes $7,800 to the

government, which it expects to pay dur-

ing the next fiscal period. An operating ac-

Retained earnings,

$56,000

$56,000. If any portion of this is distributed

in the future it will be a financing activity.

Prepaid insurance,

Insurance coverage costing $22,000 is ex-

Reporting Cash Flows 143

PROBLEMS

P5-1 San Garza Properties

Statement of Cash Flows (direct format)

For the Month of January 2007

Operating Activities

Receipts:

Collections from customers $ 8,100

Payments:

To suppliers of inventory $ (7,000)

P5-2 A. 1. $134,850 ($135,800 Sales − $950 increase in Accounts

Receivable)

B. Purchase of property, plant and equipment $(5,015)

Purchase of land (1,000)

144 Chapter 5

D. Planet Accessories Company

Statement of Cash Flows (Direct Format)

For the Year Ended December 31, 2007

Operating Activities:

Cash collections from customers $ 134,850 1

Cash paid to suppliers of inventory (55,800) 2

Financing Activities:

Addition to loan payable $ 4,000 8

Sale of common stock 1,000 9

1 proof given in part A

2 proof given in part A

Reporting Cash Flows 145

2. Cash flow from Cash received from customers:

operations = ($25,950) Cash sales $ 88,250

Collections on account 321,000

B. 1. Decrease in accounts Credit sales to customers $ 307,400

receivable = $13,600 Collections from customers

3. Decrease in accounts Purchases on credit $ 233,700

payable = $59,900 Cash payments on

C. Dollar Sine Enterprises

Statement of Cash Flow

(Operating Activities Only—Indirect Method)

For the Year Just Ended

Net income $ 44,750

Add (deduct):

146 Chapter 5

P5-4 Reuben Corporation

Statement of Cash Flows (Indirect Format)

For the Year Ended December 31, 2007

Operating Activities

Net income $ 7,000

Add (deduct):

Investing Activities

Financing Activities

Repayment on loan $ (8,250)

P5-5 A. 1. $6,738 (from the income statement)

B. Purchase of property, plant and equipment $(5,015)

Purchase of land (1,000)

C. Addition to loan payable $4,000

Reporting Cash Flows 147

D. Planet Accessories Company

Statement of Cash Flows (Indirect Format)

For the Year Ended December 31, 2007

Operating Activities

Net income $ 6,738

Add/deduct items to reconcile net income

to cash flow from operating activities:

Financing Activities

Addition to loan payable $ 4,000 9

1 proof given in part A

2 proof given in part A

148 Chapter 5

P5-6 A. Harley-Davidson also provides financing services to customers who

E. Harley-Davidson is a growing, profitable company. In 2004 and 2003,

the company produced sufficient cash from operations to provide for

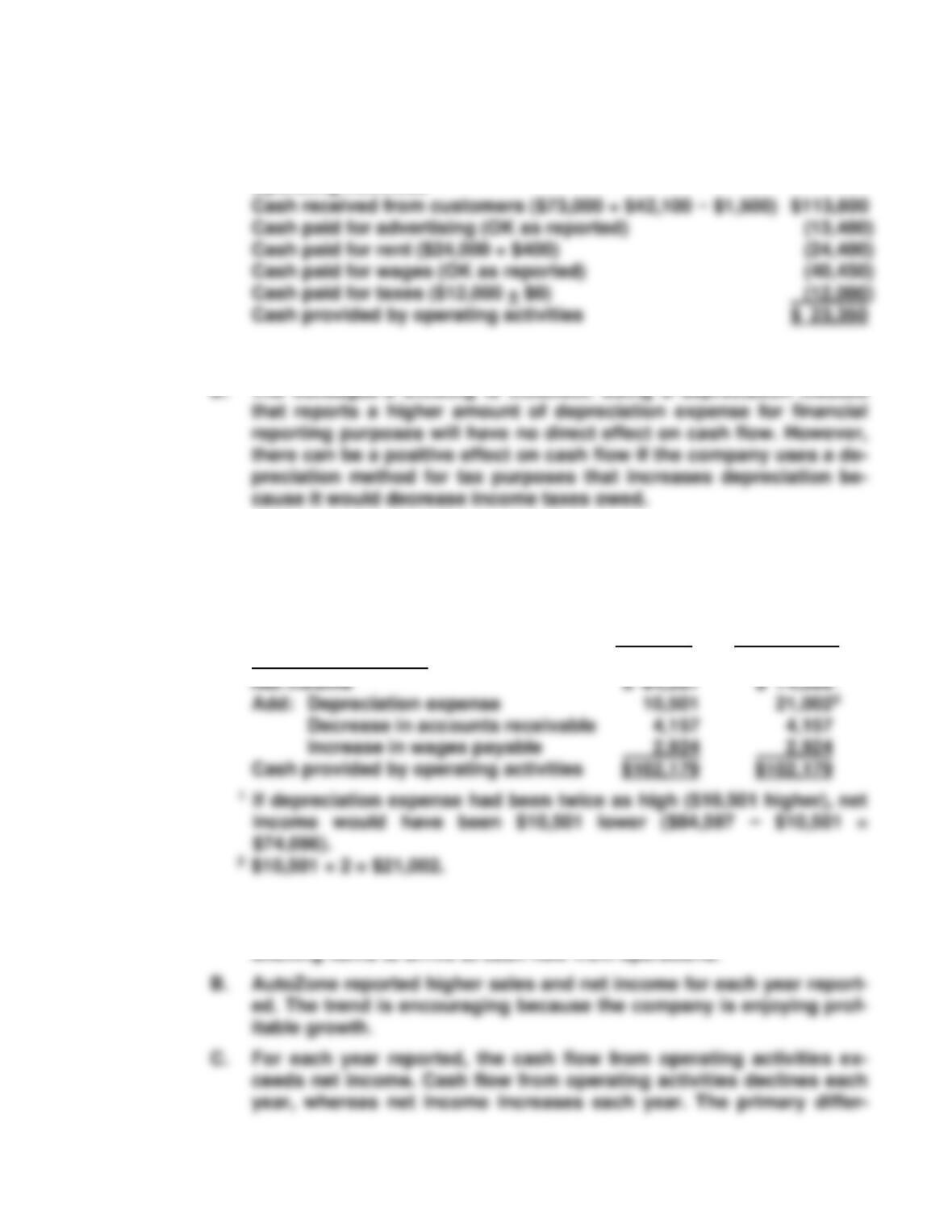

P5-7 A. 1. Cash received from customers is incorrect. It has been reported

as the accrual basis sum of revenues ($73,000 + $42,100 =

2. Cash paid for rent is incorrect. Accrual basis rent expense of

$24,000 apparently was adjusted for the $400 decrease in Rent

3. Cash paid for taxes is incorrect. The accrual basis Tax Expense

The amounts reported as cash payments for advertising and wages

are correct.

Reporting Cash Flows 149

B. Starkovich Architects, Inc.

Operating Activities (Direct Format)

For the Year Ending December 31, 2007

Operating Activities

P5-8 A. Indirect format

C. In the first column hypothetical data is shown. The second column

shows the data assuming that depreciation expense for the period

had been twice as high as reported. Cash flow from operating activi-

ties is the same under either option.

Original Adjusted

Data Data

Operating Activities

P5-9 A. AutoZone uses the indirect method for reporting cash flows. The op-

erating section begins with net income and provides a variety of rec-

150 Chapter 5

D. Cash and cash equivalents: decreased (see the bottom of the cash

flow statement)

E. The major use of cash for investing activities has been capital ex-

F. The major use of cash for financing activities has been the purchase

P5–10 A. Circuit City’s income declined each year between 2002 and 2004, alt-

hough in years 2002 and 2003 the company was profitable. The com-

pany reported a loss of $89,269,000 in 2004. Circuit City’s cash flow