Chapter 5 – Receivables and Sales

Problem 5-2A (LO 5-1, 5-2)

Requirement 1

May 2

Debit

Credit

No entry

May 7

Accounts Receivable

1,200

(Provide guided tour on account)

May 9

No entry

May 15

Sales Allowances

Accounts Receivable

(Sales allowance for services on account)

May 20

Cash

789.60

Sales Discounts

50.40

Accounts Receivable

840

(Receive cash on account)

(Sales discount = $840 x 6%)

Requirement 2

Outdoor Expo

Partial Income Statement

5-42 Financial Accounting, 5e

Problem 5-3A (LO 5-3, 5-4, 5-5)

Requirement 1

June 12, 2021

Debit

Credit

Accounts Receivable

41,000

Service Revenue

41,000

(Provide services on account)

September 17, 2021

Cash

25,000

Accounts Receivable

25,000

December 31, 2021

Allowance for Uncollectible Accounts

($16,000 x 45% = $7,200)

March 4, 2022

Accounts Receivable

56,000

Service Revenue

56,000

(Provide services on account)

May 20, 2022

Cash

10,000

Accounts Receivable

10,000

(Receive cash on account)

July 2, 2022

Allowance for Uncollectible Accounts

Accounts Receivable

(Write off actual bad debts)

Cash

45,000

Accounts Receivable

45,000

(Receive cash on account)

December 31, 2022

Bad Debt Expense

Allowance for Uncollectible Accounts

Chapter 5 – Receivables and Sales

Problem 5-3A (concluded)

Requirement 2

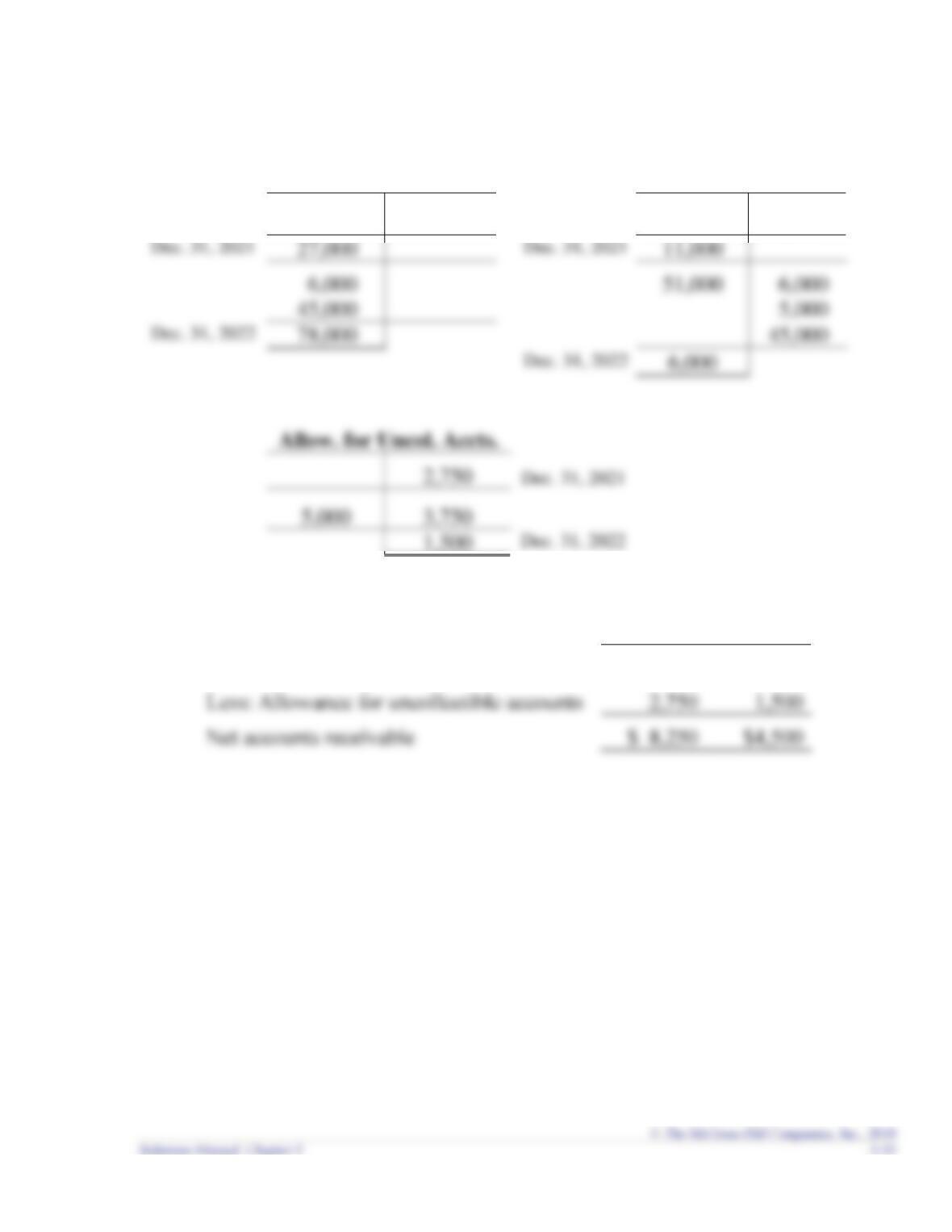

Cash

Accounts Receivable

25,000

41,000

25,000

25,000

10,000

45,000

80,000

Allow. for Uncol. Accts.

7,200

Dec. 31, 2021

Requirement 3

2021

2022

Total accounts receivable

$16,000

$11,000

Less: Allowance for uncollectible accounts

5-44 Financial Accounting, 5e

Problem 5-4A (LO 5-4, 5-5)

Requirement 1

Age group

Amount

receivable

Estimated

percent

uncollectible

Estimated

amount

uncollectible

Not yet due

$40,000

4%

$ 1,600

0-90 days past due

More than 180 days past due

Requirement 2

December 31, 2021

Debit

Credit

Bad Debt Expense

12,950

Requirement 3

July 19, 2022

Allowance for Uncollectible Accounts

8,000

Requirement 4

September 30, 2022

Accounts Receivable

8,000

Cash

8,000

Chapter 5 – Receivables and Sales

Problem 5-5A (LO 5-3, 5-6)

Requirement 1

Arnold should not use the direct write-off method. Even if no accounts are known to

Requirement 2

Allowance for uncollectible accounts = $170,000 x 70% = $119,000.

Requirement 3

Problem 5-6A (LO 5-5)

Requirement 1

Debit

Credit

Bad Debt Expense

59,000

Allowance for Uncollectible Accounts

59,000

Requirement 2

Revised operating income = $260,000 − $59,000 (bad debt expense)

Requirement 3

Debit

Credit

Bad Debt Expense

26,000

Allowance for Uncollectible Accounts

26,000

Requirement 4

Using 6% instead of 9% to estimate future bad debts causes total assets to be

Chapter 5 – Receivables and Sales

Problem 5-7A (LO 5-3, 5-4)

Requirement 1

December 31, 2021

Debit

Credit

Bad Debt Expense

455,000

Requirement 2

Because actual bad debts in 2022 were only $300,000 when the company estimated

Requirement 3

Humanity International should not prepare new financial statements for 2021. The fact

5-48 Financial Accounting, 5e

Problem 5-8A (LO 5-7)

Requirement 1

December 1, 2021

Debit

Credit

Notes Receivable

Service Revenue

(Provide services in exchange for a note)

Requirement 2

December 31, 2021

Debit

Credit

Interest Receivable (2021)

Interest Revenue

(Adjust interest receivable)

(Interest revenue = $90,000 x 10% x 1/12)

December 1, 2022

Cash

9,000

Interest Receivable (2021)

750

Interest Revenue

8,250

(Receive annual interest)

(Interest revenue = $90,000 x 10% x 11/12)

December 31, 2022

Interest Receivable (2022)

Interest Revenue

750

(Adjust interest receivable)

(Interest revenue = $90,000 x 10% x 1/12)

Chapter 5 – Receivables and Sales

Problem 5-8A (concluded)

December 1, 2023

Cash

9,000

Interest Receivable (2022)

750

December 31, 2023

Interest Receivable (2023)

750

Interest Revenue

750

Requirement 3

December 1, 2024

Debit

Credit

Cash

99,000

Notes Receivable

90,000

Interest Receivable (2021)

750

5-50 Financial Accounting, 5e

Problem 5-9A (LO 5-8)

Requirement 1

Walmart

Target

Walmart has a higher receivables turnover ratio and a lower average collection period,

which means it collects cash more quickly from its customers. The receivables

turnover ratio and average collection period for Tenet Healthcare in the most recent

Requirement 2

Including cash sales in the numerator of the receivables turnover ratio is the same as

suggesting that receivables turnover instantly (in other words, the average collection

Chapter 5 – Receivables and Sales

PROBLEMS: SET B

Problem 5-1B (LO 5-1)

Revenue recognized in 2021

Scenario 1:

$900,000

Scenario 2:

Scenario 3:

Scenario 4:

Problem 5-2B (LO 5-1, 5-2)

Requirement 1

June 10

Debit

Credit

No entry

June 12

No entry

June 13

No entry

June 16

Accounts Receivable

Service Revenue

June 19

No entry

June 20

Sales Allowances

810

Accounts Receivable

810

(Sales allowance for services on account)

June 30

Cash

Accounts Receivable

Chapter 5 – Receivables and Sales

Problem 5-2B (concluded)

Requirement 2

Data Recovery Services

Partial Income Statement

Requirement 3

June 25

Cash

1,852.2

Sales Discounts

37.8

5-54 Financial Accounting, 5e

Problem 5-3B (LO 5-3, 5-4, 5-5)

Requirement 1

February 2, 2021

Debit

Credit

Accounts Receivable

38,000

Service Revenue

38,000

(Provide services on account)

July 23, 2021

Cash

27,000

Accounts Receivable

27,000

December 31, 2021

Allowance for Uncollectible Accounts

($11,000 x 25% = $2,750)

April 12, 2022

Accounts Receivable

51,000

Service Revenue

51,000

(Provide services on account)

June 28, 2022

Cash

6,000

Accounts Receivable

6,000

September 13, 2022

Allowance for Uncollectible Accounts

5,000

Accounts Receivable

5,000

(Write off actual bad debts)

Cash

45,000

Accounts Receivable

45,000

December 31, 2022

Bad Debt Expense

3,750

Allowance for Uncollectible Accounts

3,750

(Estimate future bad debts)

[($6,000 x 25%) + $2,250 = $3,750]

Chapter 5 – Receivables and Sales

Problem 5-3B (concluded)

Requirement 2

Cash

Accounts Receivable

27,000

38,000

27,000

27,000

11,000

6,000

45,000

5,000

78,000

Requirement 3

2021

2022

Total accounts receivable

$11,000

$6,000

Less: Allowance for uncollectible accounts

5-56 Financial Accounting, 5e

Problem 5-4B (LO 5-4, 5-5)

Requirement 1

Age group

Amount

receivable

Estimated

percent

uncollectible

Estimated

amount

uncollectible

Not yet due

$40,000

3%

$1,200

0-30 days past due

4%

More than 60 days past due

$60,000

Requirement 2

December 31, 2021

Debit

Credit

Bad Debt Expense

3,170

Requirement 3

April 3, 2022

Allowance for Uncollectible Accounts

500

Requirement 4

July 17, 2022

Accounts Receivable

100

July 17, 2022

Cash

100

Chapter 5 – Receivables and Sales

Problem 5-5B (LO 5-3, 5-6)

Requirement 1

Letni should not use the direct write-off method. Even if no accounts are known to be

uncollectible at the time, Paul should estimate future bad debts and record those

Problem 5-6B (LO 5-5)

Requirement 1

Debit

Credit

Bad Debt Expense

330,000

Allowance for Uncollectible Accounts

330,000

(Estimate future bad debts)

($11,000,000 x 4% − $110,000 = $330,000)

Requirement 2

Revised operating income = $2,900,000 − $330,000 (bad debt expense)

Requirement 3

Revised operating income = $2,900,000 − $700,000 (bad debt expense)

= $2,200,000

Chapter 5 – Receivables and Sales

Problem 5-7B (LO 5-3, 5-4)

Requirement 1

Debit

Credit

Bad Debt Expense

7,000

Requirement 2

Previts underestimated uncollectible accounts by $80,500. Actual bad debts in the

Requirement 3

Previts should not prepare new financial statements for the first year. The fact that