CHAPTER 5

Cost-Volume-Profit

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

1. Explain variable, fixed, and

mixed costs and the relevant

range.

1, 2, 3, 4, 5,

6

1, 2

1

1, 2, 3, 4, 5,

6

1A, 6A

2. Apply the high-low method to

determine the components of

mixed costs.

7, 8

1, 3, 4, 5

2

3, 5,

1A

3. Prepare a CVP income

statement to determine

contribution margin.

9, 10, 11, 17

6, 7

3

7, 8, 9, 10, 11,

12, 13, 17

1A, 2A, 4A,

5A, 6A

4. Compute the break-even

point using three approaches.

12, 13, 14

8, 9

8, 9, 10, 11,

12, 13, 14,

16, 17

1A, 2A, 3A,

4A, 5A

5. Determine the sales required

to earn target net income and

determine margin of safety.

15, 16

10, 11, 12

5

14, 15, 16,

2A, 4A, 5A,

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Determine variable and fixed costs, compute break-even

point, prepare a CVP graph, and determine net income.

Simple

20–30

2A

Prepare a CVP income statement, compute break-even

point, contribution margin ratio, margin of safety ratio,

and sales for target net income.

Moderate

30–40

5A

Compute contribution margin, fixed costs, break-even

point, sales for target net income, and margin of safety

ratio.

Moderate

20–30

6A

Determine contribution margin ratio, break-even point, and

margin of safety.

Moderate

20–30

3A

Compute break-even point under alternative courses

of action.

Simple

20–30

changes in business environment.

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

* 1. Explain variable, fixed, and mixed

costs and the relevant range.

E5-4

Q5-1

Q5-2

Q5-3

Q5-4

Q5-5

Q5-6

BE5-1

DI5-1

E5-1

E5-2

E5-4

E5-2

E5-5

E5-6

BE5-2

E5-3

P5–1A

P5–6A

* 2. Apply the high-low method to

determine the components of mixed

costs.

E5-4

E5-5

Q5-7

BE5-1

E5-1

Q5-8

BE5-4

BE5-5

DI5-2

E5-5

E5-6

BE5-3

E5-3

P5–1A

* 3. Prepare a CVP income statement to

determine contribution margin.

E5-7

Q5-9

Q5–10

Q5–11

Q5–17

BE5-6

BE5-7

E5-9

E5–10

E5–11

E5–12

BE5-6

P5–1A

P5–2A

P5–5A

P5–4A

P5–6A

* 4. Compute the break-even point

using three approaches.

Q5–12

Q5–14

Q5–13

BE5-8

BE5-9

DI5-4

DI5-5

E5-8

E5-9

E5–10

E5–11

E5–12

E5–13

E5–14

E5–16

E5–17

E5–16

P5–1A

P5–2A

P5–5A

P5–3A

P5–4A

* 5. Determine the sales required to

earn target net income and

determine margin of safety.

Q5–15

Q5–16

BE5-10

BE5-11

BE5-12

DI5-5

E5–12

E5–14

E5–15

E5–17

E5–16

P5–2A

P5–5A

P5–4A

P5–6A

Continuing Problems

CD5

Broadening Your Perspective

BYP5-5

BYP5-3

BYP5-1

BYP5-4

BYP5-2

BYP5-6

BYP5-7

BLOOM’ S TAXONOMY TABLE

ANSWERS TO QUESTIONS

1. (a) Cost behavior analysis is the study of how specific costs respond to changes in the level of activity

within a company.

(b) Cost behavior analysis is important to management in planning business operations and in deciding

between alternative courses of action.

2. (a) The activity index identifies the activity that causes changes in the behavior of costs. Once the

index is determined, it is possible to classify the behavior of costs in response to changes in

activity levels into three categories: variable, fixed, or mixed.

(b) Variable costs may be defined in total or on a per-unit basis. Variable costs in total vary directly

and proportionately with changes in the activity level. Variable costs per unit remain the

same at every level of activity.

3. Fixed costs remain the same in total regardless of changes in the activity level. In contrast, fixed

costs per unit vary inversely with activity. As volume increases, fixed costs per unit decline and vice

versa.

4. (a) The relevant range is the range of activity over which a company expects to operate during

the year.

(b) Disagree. The behavior of both fixed and variable costs are linear only over a certain range

of activity. CVP analysis is based on the assumption that both fixed and variable costs

remain linear within the relevant range.

5. This is true. Most companies operate within the relevant range. Within this range, it is possible to

establish a linear (straight-line) relationship for both variable and fixed costs. If a relevant range

cannot be established, segregation of costs into fixed and variable becomes extremely difficult.

6. Apartment rent is fixed because the cost per month remains the same regardless of how much Adam

uses the apartment. Rent on a Hertz rental truck is a mixed cost because the cost usually includes a

per day charge (a fixed cost) plus an activity charge based on miles driven (a variable cost).

7. For CVP analysis, mixed costs must be classified into their fixed and variable elements. One approach

to the classification of mixed costs is the high-low method.

8. Variable cost per unit is $1.30, or [($165,000 – $100,000) ÷ (90,000 – 40,000)]. At any level of activity,

fixed costs are $48,000 per month [$165,000 – (90,000 X $1.30)].

9. No. Only two of the basic components of cost-volume-profit (CVP) analysis, unit selling prices and

variable cost per unit, relate to unit data. The other components, volume, total fixed costs, and

sales mix, are not based on per-unit amounts.

10. There is no truth in Faye’s statement. Contribution margin is sales less variable costs. It is the

revenue that remains to cover fixed costs and to produce income (profit) for the company.

11. Contribution margin is $14 ($40 – $26). The contribution margin ratio is 35% ($14 ÷ $40).

Questions Chapter 5 (Continued)

12. Disagree. Knowledge of the break–even point is useful to management in deciding whether to introduce

new product lines, change sales prices on established products, and enter new market areas.

13. $26,000 ÷ 25% = $104,000

14. (a) The break-even point involves the plotting of three lines over the full range of activity: the total

revenue line, the total fixed cost line, and the total cost line. The break-even point is deter-

mined at the intersection of the total revenue and total cost lines.

(b) The break-even point in units is obtained by drawing a vertical line from the break-even point to

the horizontal axis. The break-even point in sales dollars is obtained by drawing a horizontal line

from the break-even point to the vertical axis.

15. Margin of safety is the difference between actual or expected sales and sales at the break-even

point. 1,250 X $12 = $15,000; $15,000 – $13,200 = $1,800; $1,800 ÷ $15,000 = 12%.

16. At break-even sales, the contribution margin is equal to the fixed costs. The contribution margin

ratio is:

$180,000

$500,000

= 36%

The sales volume to achieve net income of $90,000 is as follows:

$180,000 + $90,000

.36

= $750,000

17. PACE COMPANY

CVP Income Statement

Sales ……………………………………………………………………………………. $900,000

Variable expenses

Cost of goods sold ($600,000 X .70) …………………………………… $420,000

Operating expenses ($200,000 X .70) …………………………………. 140,000

Total variable expenses …………………………………………….. 560,000

Contribution margin ………………………………………………………………… $340,000

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 5-1

Indirect labor is a variable cost because it increases in total directly and

proportionately with the change in the activity level.

BRIEF EXERCISE 5-2

VARIABLE COST

Relevant Range

FIXED COST

Relevant Range

$10,000

$10,000

8,000

8,000

6,000

6,000

4,000

4,000

2,000

2,000

BRIEF EXERCISE 5-3

$60,000

Total Cost Line

45,000

BRIEF EXERCISE 5-4

High

Low

Difference

$15,000

$13,500

=

$1,500

$1,500 ÷ 1,000 = $1.50—Variable cost per mile.

High

Low

Total cost

Less: Variable costs

$15,000

$13,500

30,000

15,000

BRIEF EXERCISE 5-5

High

Low

Difference

$74,500

–

$36,000

=

$38,500

Activity Level

High

Low

Total fixed costs

Total cost

$74,500

$36,000

BRIEF EXERCISE 5-6

1. (a) $288 = ($640 – $352)

(b) 45% ($288 ÷ $640)

BRIEF EXERCISE 5-7

RUSSELL INC.

CVP Income Statement

For the Quarter Ended March 31, 2017

Sales ………………………………………………………………………. $2,200,000

Variable costs ($920,000 + $70,000 + $86,000) …………… 1,076,000

BRIEF EXERCISE 5-8

18,000

(a) $520Q – $286Q – $163,800 = $0

$234Q = $163,800

BRIEF EXERCISE 5-9

BRIEF EXERCISE 5-10

If variable costs are 70% of sales, the contribution margin ratio is ($1 – $0.70) ÷

BRIEF EXERCISE 5-11

Margin of safety = $1,000,000 – $800,000 = $200,000

Margin of safety ratio = $200,000 ÷ $1,000,000 = 20%

BRIEF EXERCISE 5-12

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 5-1

Variable costs: Indirect labor, direct labor, and direct materials.

DO IT! 5-2

(a) Variable cost: ($18,580 – $16,200) ÷ (10,500 – 8,800) = $1.40 per unit

(b) Total cost to produce 9,200 units: $3,880 + ($1.40 X 9,200) = $16,760

DO IT! 5-3

Cedar Grove Industries

CVP Income Statement

For the Month Ended May 31, 2017

Total Per Unit

Sales $360,000 $45

DO IT! 5-4

(a) The formula is $250Q – $170Q – $160,000 = 0. Therefore, 80Q =

$160,000, and the breakeven point in units is 2,000 ($160,000 ÷ $80).

DO IT! 5-5

(a) CM per unit = Unit selling price – Unit variable costs

$12 = $30 – $18

(b)

Margin of safety

=

Actual sales – Break-even sales

Actual sales

(c) Sales – Variable costs – Fixed costs = Net income

$30Q – $18Q = $220,000 + $140,000

SOLUTIONS TO EXERCISES

EXERCISE 5-1

(a) The determination as to whether a cost is variable, fixed, or mixed can

be made by comparing the cost in total or on a per-unit basis at two

different levels of production.

(b) Using these criteria as a guideline, the classification is as follows:

Direct materials

Variable

Rent

Fixed

EXERCISE 5-2

(a)

Fixed Costs

Remain constant in total but vary on a per-unit basis.

EXERCISE 5-2 (Continued)

(b) The relevant range is 3,000 – 8,000 units of output since a straight-line

relationship exists for both direct materials and rent within this range.

(c)

Variable cost per unit

Within the relevant range

=

Cost

Units

(3,000 – 8,000 units)

(d) Fixed cost within the

EXERCISE 5-3

(a) Maintenance Costs:

700

Machine Hours

300

Machine Hours

300 X $7

Total fixed costs

Total costs

$5,500

$2,700

=

$15,000*

5,000*

=

EXERCISE 5-3 (Continued)

(b)

$6,000

COSTS

$4,000

$3,000

Variable Cost Element

$2,000

EXERCISE 5-4

1.

Wood used in the production of furniture.

Variable.

2.

Fuel used in delivery trucks.

Variable.

3.

Straight-line depreciation on factory building.

Fixed.

4.

Screws used in the production of furniture.

Variable.

5.

Sales staff salaries.

Fixed.

6.

Sales commissions.

Variable.

7.

Property taxes.

Fixed.

8.

Insurance on buildings.

Fixed.

9.

Hourly wages of furniture craftsmen.

Variable.

Salaries of factory supervisors.

Fixed.

Utilities expense.

Mixed.

Telephone bill.

Mixed.

EXERCISE 5-5

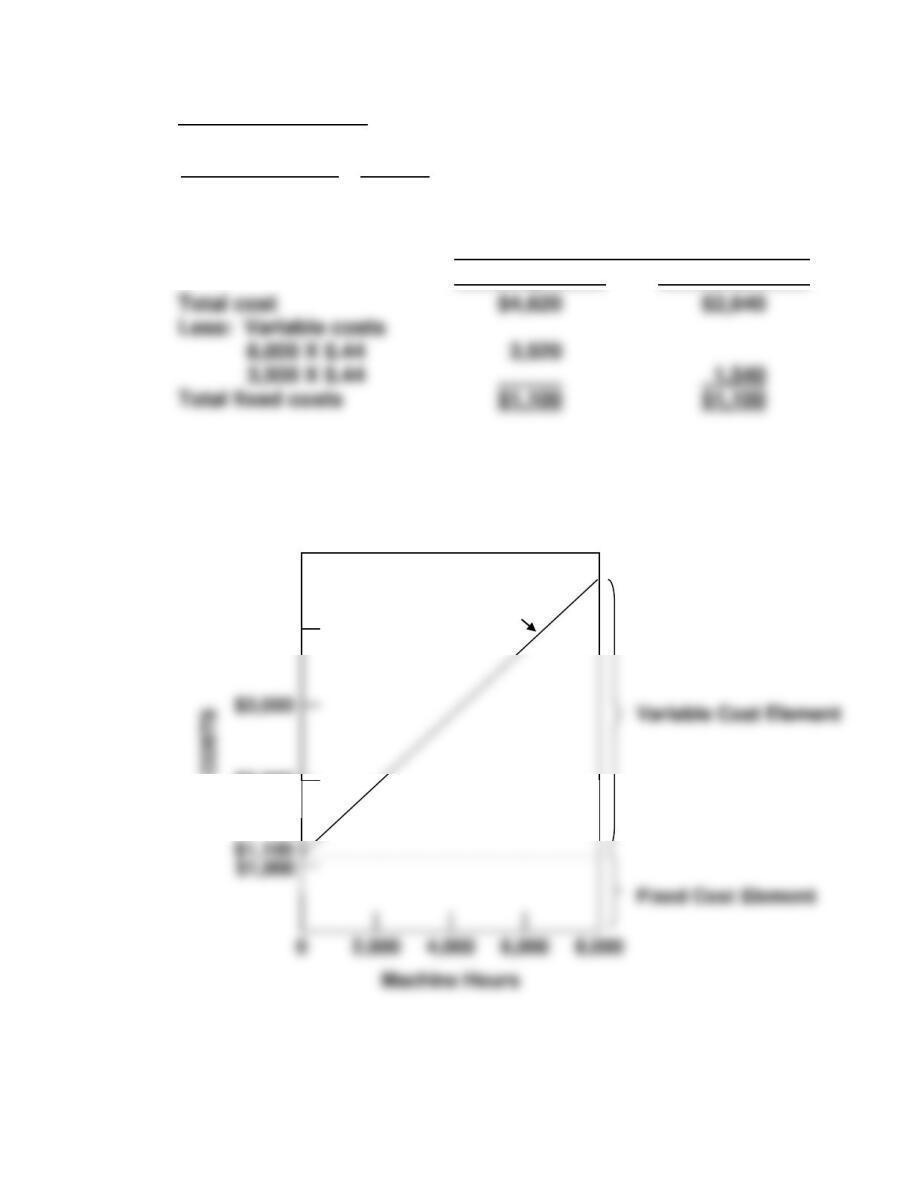

(a) Maintenance Costs:

$4,620 – $2,640 $1,980

=

8,000 – 3,500 4,500

= $.44 variable cost per machine hour

Activity Level

High

Low

Thus, maintenance costs are $1,100 per month plus $.44 per machine

hour.

(b)

$5,000

COSTS

$4,620

$4,000

Total Cost Line

$3,000

$2,000

Total fixed costs

EXERCISE 5-6

(a)

Cost

Fixed

Variable

Mixed

Direct materials

X

Direct labor

X

(b) Fixed costs = $1,000 + $1,900 + $2,400 +

$300 + $200

= $5,800

Variable costs to produce 3,000 units = $7,500 + $18,000 + $4,500

= $30,000

Utilities

Property taxes

X

Indirect labor

X

Supervisory salaries

X

Maintenance

Depreciation

X

EXERCISE 5-7

MEMO

To: Marty Moser

From: Student

Re: Assumptions underlying CVP analysis

CVP analysis is a useful tool in analyzing the effects of changes in costs

and volume on a company’s profits. However, there are some assumptions

which underlie CVP analysis. When these assumptions are not valid,

the results of CVP analysis may be inaccurate.

EXERCISE 5-8

(a)

Contribution margin per lawn

Contribution margin per lawn

=

=

$60 – ($12 + $10 + $2)

$36

(b) Break-even point in dollars = 100 lawns X $60 per lawn

= $6,000 per month

EXERCISE 5-9

1.

Contribution margin per room

=

$60 – ($14 + $28)

2. Break-even point in dollars = 450 rooms X $60 per room

= $27,000 per month

EXERCISE 5-10

(a) Contribution margin in dollars: Sales = 560 X $120 = $67,200

Variable costs = $67,200 X .60 = 40,320

Contribution margin $26,880

EXERCISE 5-11

(a)

1. Contribution margin ratio is:

$27,000

= 75%

$36,000

2. Round-trip fare =

$36,000

= $24

1,500 fares

(b) At the break-even point fixed costs and contribution margin are equal.

EXERCISE 5-12

(a) Unit contribution margin =

Fixed costs

Break-even sales in units

Variable cost per unit = Unit selling price – Unit contribution margin

= $5.00 – $1.60

= $3.40

Break-even point in dollars =

EXERCISE 5-12 (Continued)

(b) Fixed costs ÷ Contribution margin ratio = Break-even sales in dollars

Since fixed costs were $112,000 in 2016, the increase in 2017 is $22,400

($134,400 – $112,000).

EXERCISE 5-13

(a) and (b) BILLINGS COMPANY

CVP Income Statement

For the Month Ended September 30, 2017

Total

Per Unit

Sales (600 video game consoles) ……………… $240,000 $400

Variable costs …………………………………………. 168,000 280

(c) Sales = Variable costs + Fixed costs

$400X = $280X + $54,000

(d) BILLINGS COMPANY

CVP Income Statement

For the Month Ended September 30, 2017

Total

Per Unit

Sales (450 video game consoles)………………. $180,000 $400

Variable costs ………………………………………….. 126,000 280

EXERCISE 5-14

(a) Units sold in 2016 =

$570,000 + $210,000

$150 – $90

= 13,000 units

(c)

$570,000 + $262,000

X – $90

= 13,000 units, where X = new selling price

$832,000 = 13,000X – $1,170,000

EXERCISE 5-15

1. Unit sales price = $400,000 ÷ 5,000 units = $80

Increase selling price to $88, or ($80 X 110%).

EXERCISE 5-16

(a)

$3,200

Sales Line

DOLLARS (000)

2,800

2,000

1,600

1,200

Fixed Cost Line

(b) 1. Break-even sales in units:

$4X = $2.50X + $600,000

2. Break-even sales in dollars:

X = .625X + $600,000

(c) 1. Margin of safety in dollars: $2,000,000 – $1,600,000 = $400,000

2,400

EXERCISE 5-17

(a) Contribution ratio = Contribution margin ÷ Sales

($40 – $24) ÷ $40 = 40%

SOLUTIONS TO PROBLEMS

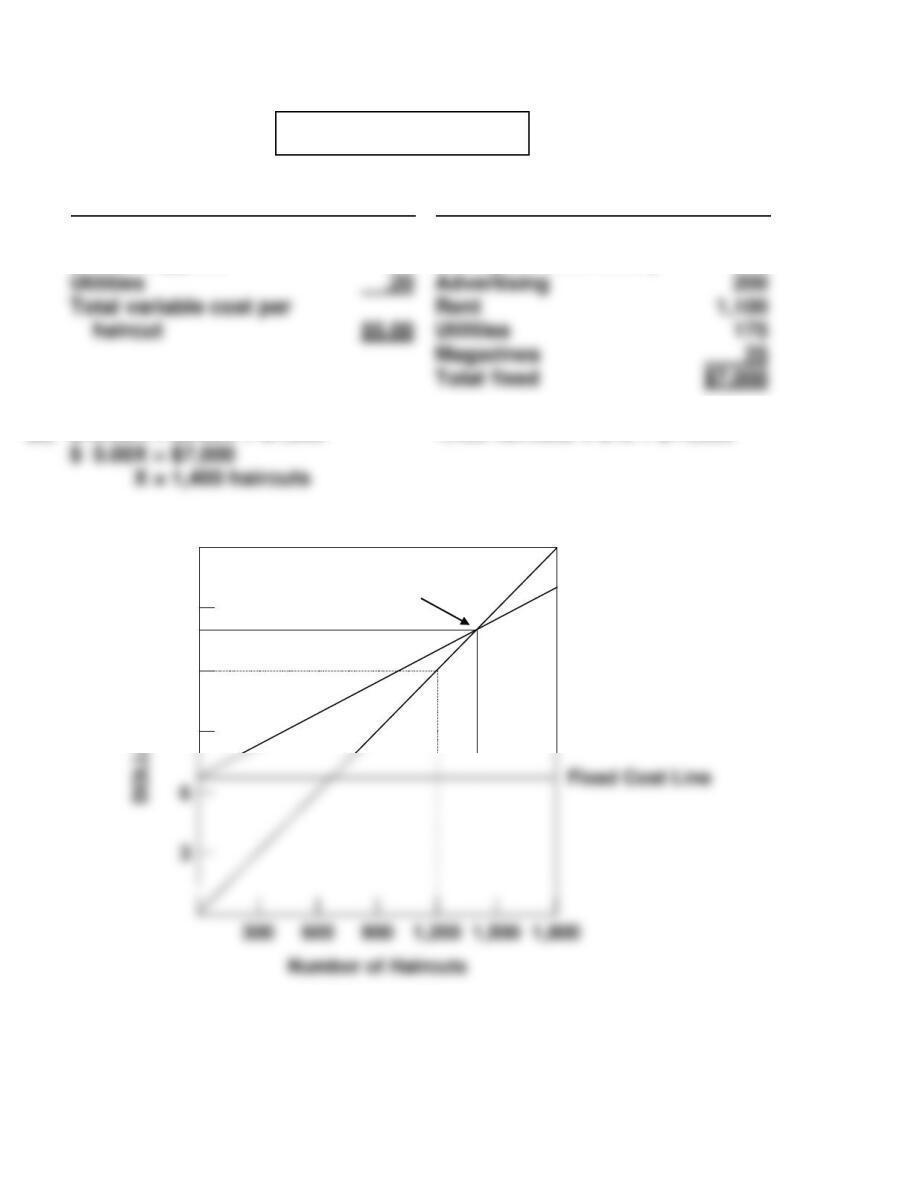

PROBLEM 5-1A

(a)

Variable costs (per haircut)

Fixed costs (per month)

Barbers’ commission $4.50

Barber supplies .30

Barbers’ salaries $5,000

Manager’s extra salary 500

(b)

$10.00X = $5.00X + $7,000

1,400 haircuts X $10 = $14,000

(c)

18

Sales Line

6

15

Break-even Point

Total Cost Line

12

9

(d) Net income = $16,000 – [($5.00 X 1,600) + $7,000]

= $1,000

Total fixed $7,000

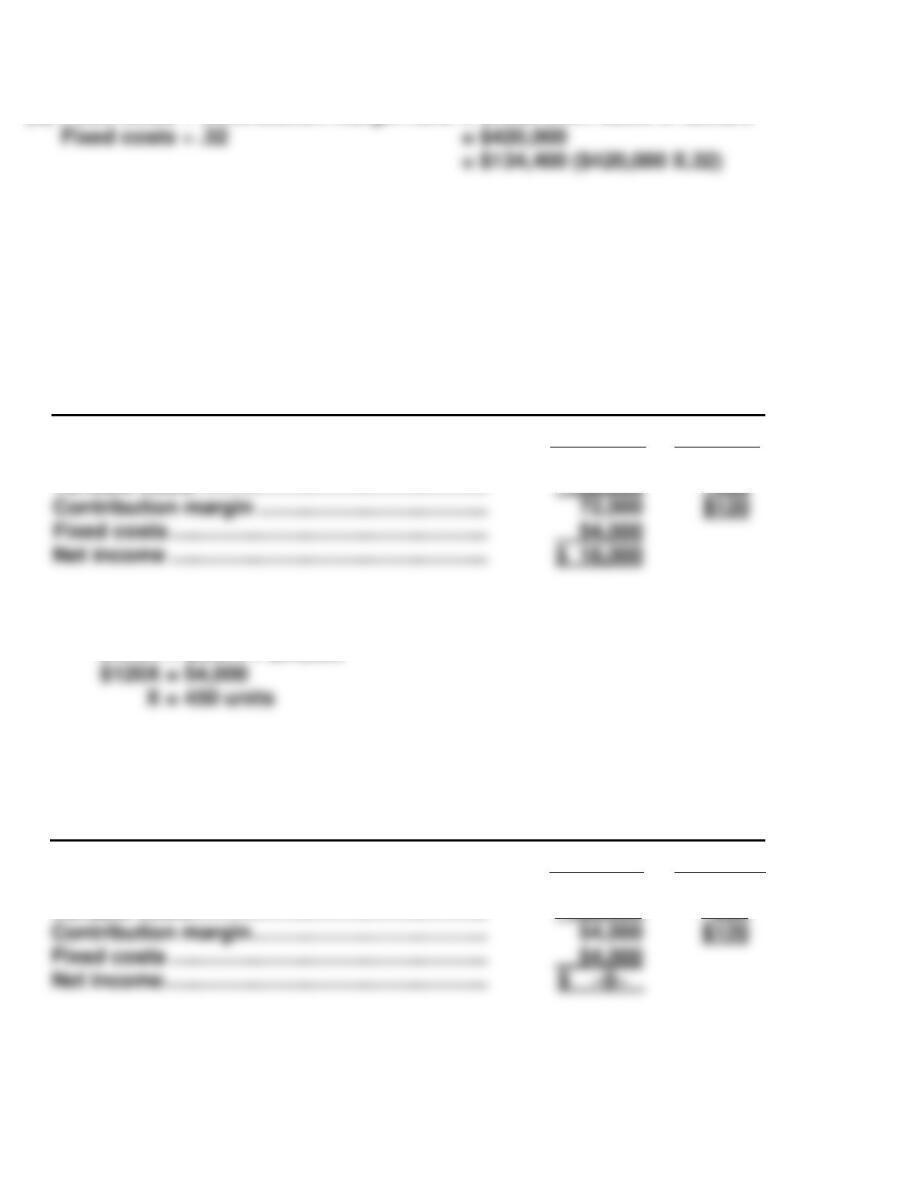

PROBLEM 5-2A

(a) JORGE COMPANY

CVP Income Statement (Estimated)

For the Year Ending December 31, 2017

Sales …………………………………………………….. $1,800,000

Variable expenses

(b) Variable costs = 70% of sales ($1,260,000 ÷ $1,800,000) or $.35 per

bottle ($.50 X 70%). Total fixed costs = $405,000.

1. $.50X = $.35X + $405,000

$.15X = $405,000

(c) Contribution margin ratio = ($.50 – $.35) ÷ $.50

= 30% (or 1 – .70)

(d) Required sales

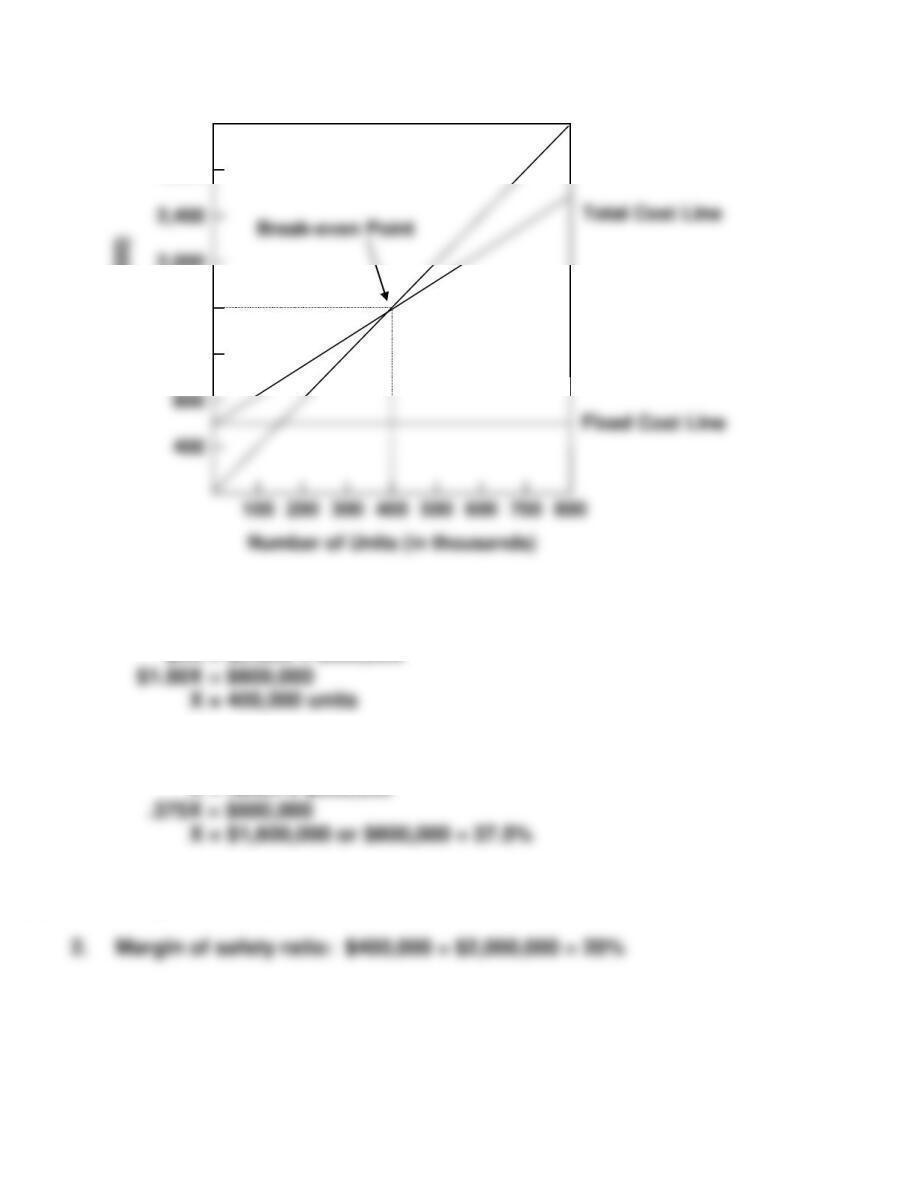

PROBLEM 5-3A

(a) Sales were $2,500,000, variable expenses were $1,750,000 (70% of sales),

and fixed expenses were $850,000. Therefore, the break-even point in

dollars is:

(b) 1. The effect of this alternative is to increase the selling price per unit

to $6 ($5 X 120%). Total sales become $3,000,000 (500,000 X $6).

2. The effects of this alternative are to change total fixed costs

to $760,000 ($850,000 – $90,000) and to change the contribution

Alternative 1 is the recommended course of action because it has a

lower break-even point.

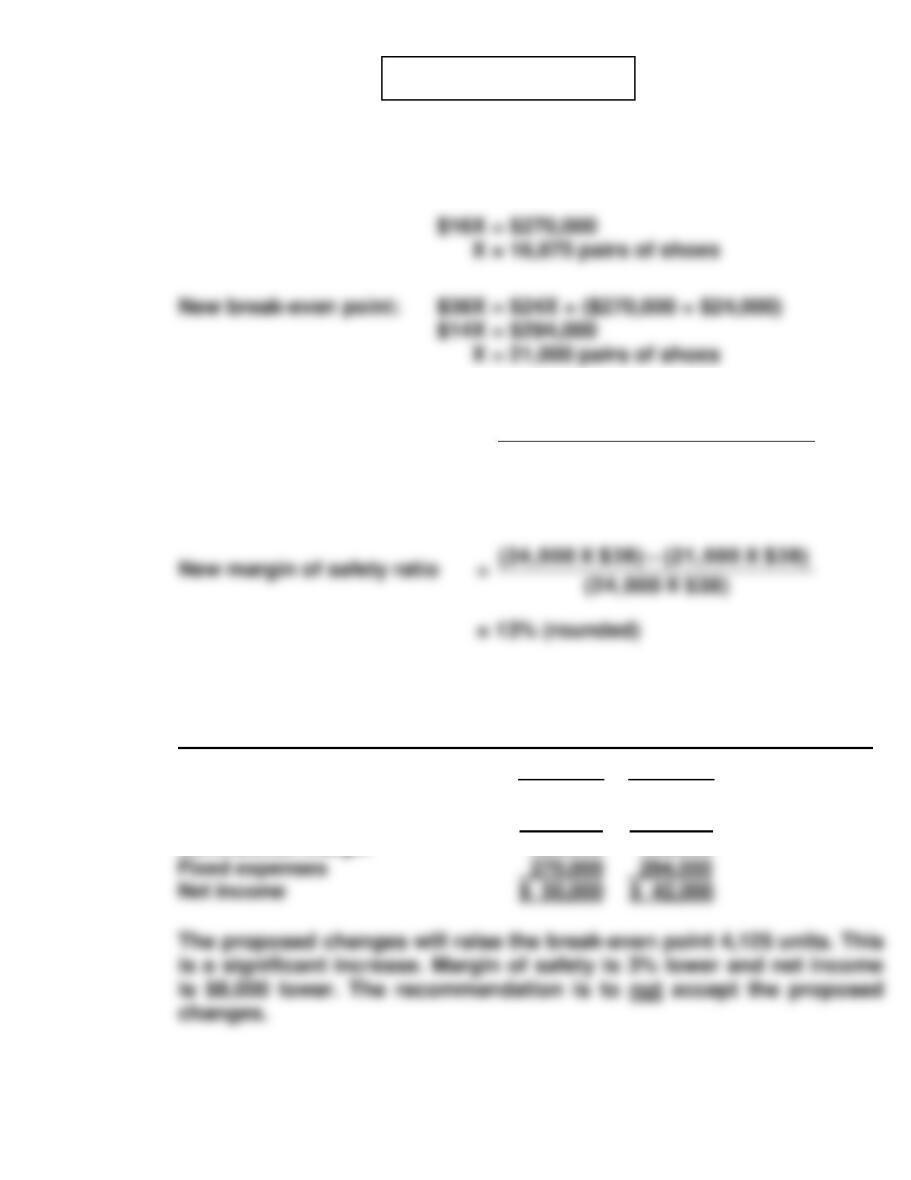

PROBLEM 5-4A

(a) Current break-even point: $40X = $24X + $270,000

(where X = pairs of shoes)

(b) Current margin of safety ratio =

(20,000 X $40) – (16,875 X $40)

(20,000 X $40)

(24,000 X $38) – (21,000 X $38)

(24,000 X $38)

= 16% (rounded)

(c) BARGAIN SHOE STORE

CVP Income Statement

Current

New

Sales (20,000 X $40)

Variable expenses (20,000 X $24)

Contribution margin

$800,000

480,000

320,000

$912,000

576,000

336,000

(24,000 X $38)

(24,000 X $24)

PROBLEM 5-5A

(a)

(1)

Current Year

Sales

Variable costs

Direct materials

Direct labor

$1,600,000

490,000

290,000

Current Year

Projected Year

Contribution margin

Sales

Variable costs

Direct materials

Direct labor

Manufacturing overhead

$1,600,000

490,000

290,000

266,000

X 1.1

X 1.1

X 1.1

X 1.1

$1,760,000

539,000

319,000

292,600

(2)

Fixed Costs

Current Year

Projected year

Total fixed costs

Manufacturing overhead ($380,000 X .30)

Selling expenses ($250,000 X .60)

$114,000

150,000

$114,000

150,000

Contribution margin

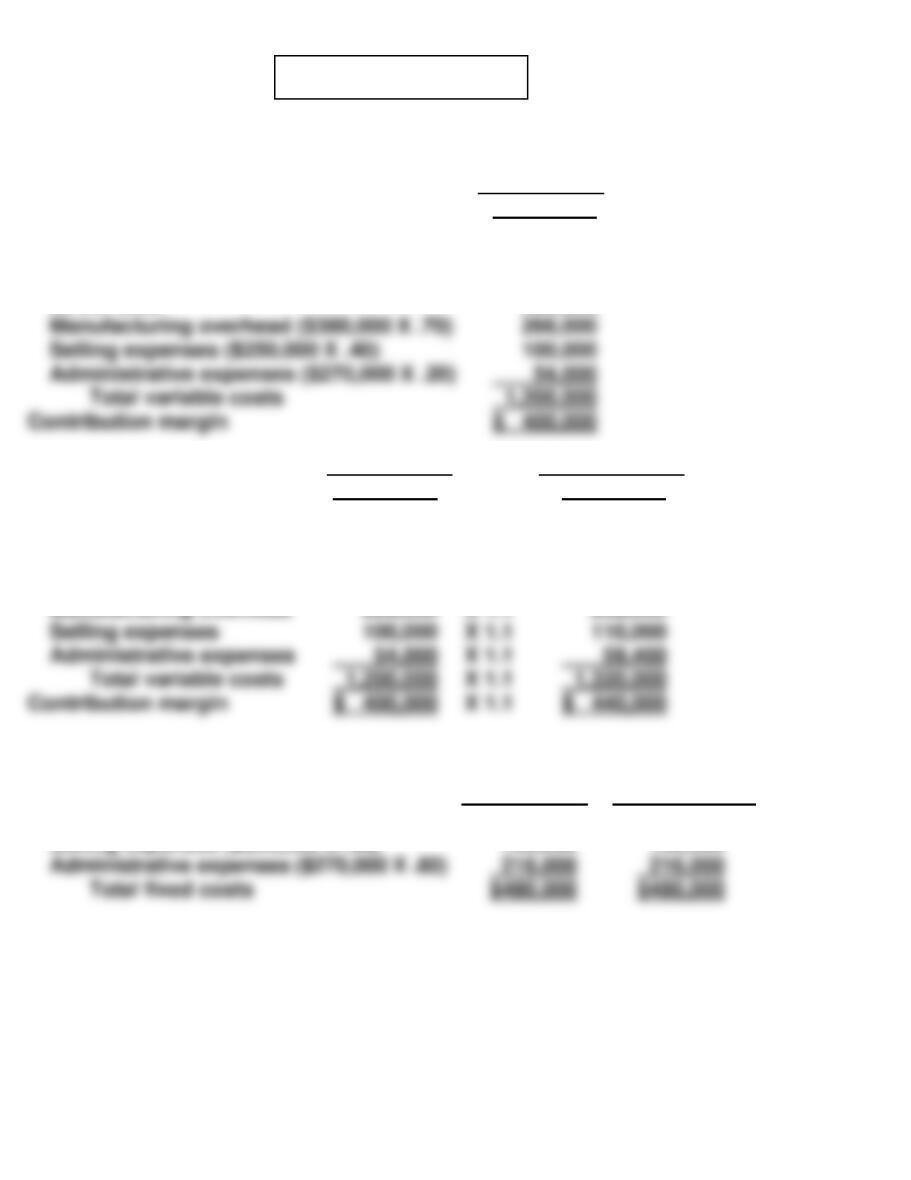

PROBLEM 5-5A (Continued)

(b) Unit selling price = $1,600,000 ÷ 100,000 = $16

Unit variable cost = $1,200,000 ÷ 100,000 = $12

Break-even point in units

=

Fixed costs

÷

Unit contribution margin

120,000 units

=

$480,000

÷

$4

Break-even point in dollars

Fixed costs

÷

Contribution margin ratio

$480,000

÷

.25

(c) Sales dollars

required for

=

(Fixed costs

+

Target net income)

÷

Contribution margin ratio

=

Break-even sales)

÷

Expected sales

=

÷

target net

PROBLEM 5-6A

(a) 1. Let variable selling and administrative expenses = VSA

Sales – Variable cost of goods sold – VSA = Contribution Margin

$1,200,000 – ($400,000 + $500,000 + $50,000 + VSA) = $180,000

VSA = $70,000

2. Let fixed manufacturing overhead = FMO

(b) Incremental sales = $1,200,000 X 25% = $300,000

Incremental contribution margin = $300,000 X 15% = $45,000

The maximum increased advertising expenditure would be equal to

the incremental contribution margin earned on the increased sales,

CD5 CURRENT DESIGNS

(a) $250 + $100 + $170 + $420 + $400 = $1,340 total variable costs

(b) Contribution margin per unit = $2,000 – $1,340 = $660

(c) $359,700* ÷ $660 = 545 units

Margin of safety ratio = $910,000 ÷ $2,000,000

= 45.5%

BYP 5-1 DECISION-MAKING ACROSS THE ORGANIZATION

(a)

(1) Capital-Intensive

(2) Labor-Intensive

Fixed manufacturing costs $2,524,000

Incremental selling expenses 502,000

Total fixed costs $3,026,000

Fixed manufacturing costs $1,550,000

Incremental selling expenses 502,000

Total fixed costs $2,052,000

Contribution margin $16.00

Contribution margin $12.00

Total fixed costs (1) $3,026,000

Total fixed costs (1) $2,052,000

Selling price $32.00

Variable costs

Selling price $32.00

Variable costs

Contribution margin per unit (2) $16.00

Contribution margin per unit (2) $12.00

Break-even in units (1) ÷ (2) 189,125

Break-even in units (1) ÷ (2) 171,000

(b) Creative Ideas Company would be indifferent between the two manufac-

turing methods at the volume (X) where total costs are equal.

(c) Creative Ideas should employ the capital-intensive manufacturing

method if annual sales are expected to exceed 243,500 units and the

labor–intensive manufacturing method if annual sales are not expected

BYP 5-2 MANAGERIAL ANALYSIS

(a) The variable costs per unit are:

Cost of goods sold ($600,000 ÷ 240,000) ………………… $2.50

Selling expenses ($117,600 ÷ 240,000) …………………… .49

The break-even points are:

X = ($3.24 ÷ $5.00) X + $452,400

X = .65X + $452,400

(b) Variable unit cost of goods sold = $2.75

($600,000 ÷ 240,000 = $2.50; $2.50 + $.25)

Sales volume = 300,000 units (240,000 X 125%)

Total sales = 300,000 X $5.25 = $1,575,000

Net income computation:

Sales ………………………………………………. $1,575,000

Variable expenses

Cost of goods sold

BYP 5-2 (Continued)

Fixed expenses

Cost of goods sold …………………… $200,000

(c) Sales [384,000 (1) X ($5.00 – $.25)] …………… $1,824,000

Variable expenses

Cost of goods sold

(384,000 X $2.50) …………………………... $960,000

Selling expenses (384,000 X $.59) ……… 226,560

(1) Sales volume = 240,000 X 160% = 384,000

X = ($1,282,560 ÷ $1,824,000)X + $492,400

(d) Peri’s plan should be accepted. It produces a higher net income and

a lower break-even point than Paul’s plan.

BYP 5-3 REAL-WORLD FOCUS

(a) Sweeteners and packaging are a variable cost to Coca-Cola because

their use is directly proportional to the amount of product produced. If

the unit cost of a variable cost item increases, the contribution margin

will decline. This will lead to a decline in net income unless the company

can increase its selling price, increase the number of units it sells, or

reduce other costs.

(b) This description makes the marketing expenditures sound like they are

a variable cost, since it suggests that they vary with the amount of units

sold. However, unlike variable costs, the relationship of marketing costs

is not directly proportional to sales, since other factors also influence

BYP 5-4 REAL-WORLD FOCUS

(a) Barnes and Noble has 1,362 stores with a total of 18.8 million square

feet. That is a huge investment in fixed costs that have very little value

in an e-book environment.

(b) Barnes and Noble’s big advantage (which enabled it to put lots of

small independent book sellers out of business), was that each of its

superstores had 150,000 books in stock. However, that is no longer as

(e) Barnes and Noble was one of the first companies to have an e-reader,

called the Rocket e-book. However, it abandoned its e-reader in 2003

because sales of e-books had been very low. Four years later Amazon

introduced its Kindle e-reader, which has been hugely popular. A second

BYP 5-5 COMMUNICATION ACTIVITY

To: My Roommate

From: Your Roommate

Subject: Cost-Volume-Profit Questions

In response to your request for help, I provide you the following:

(a) The mathematical formula for break-even sales is:

Break-even Sales = Variable Costs + Fixed Costs

Break-even sales in dollars is found by expressing variable costs as a

(b) The formulas for unit contribution margin and contribution margin

ratio differ as shown below:

Unit Selling Price – Unit Variable Costs = Unit Contribution Margin

(c) When contribution margin is used to determine break-even sales, total

fixed costs are divided by either the contribution margin ratio or unit

BYP 5-5 (Continued)

The formula for determining break-even sales in dollars is:

Fixed Costs ÷ Contribution Margin Ratio = Break-even Sales in Dollars

BYP 5-6 ETHICS CASE

(a) The stakeholders in this situation are:

Scott Bestor, accountant of Westfield Company.

The dislocated personnel of Westfield.

The senior management who made the decision.

(b) Scott is hiding an error and is knowingly deceiving the company’s

management with inaccurate data.

(c) Scott’s alternatives are:

BYP 5-7 ALL ABOUT YOU

(a) The variable gasoline cost of going one mile in the hybrid car would

be $0.09 ($3.60/40). The variable gasoline cost of going one mile in the

traditional car would be $0.12 ($3.60/30).

(b) The savings per mile of driving the hybrid vehicle would be $0.03

($0.12 – $0.09).