1. The individual accounts receivable ledger accounts provide business managers with information on

the status of individual customer accounts, which is necessary for managing collections. Managers

need to know which customers owe money, how much they owe, and how long the amount owed has

b

een outstanding.

5. a. Sometime following the end of the current month, one of two things may happen: (1) an

overdue notice will be received from Kelly Co., and/or (2) a letter will be received from

Kelley Co., informing the buyer of the overpayment. (It is also possible that the error will be

discovered at the time of making payment if the original invoice is inspected at the time the

check is being written.)

b. The schedule of accounts payable would not agree with the balance of the accounts payable

account. The error might also be discovered at the time the invoice is paid.

c. The creditor will call the attention of the debtor to the unpaid balance of $800.

d. The error will become evident during the verification process at the end of the month. The

total debits in the purchases journal will be less than the total credits by $3,600.

8. Transactions are posted when they are entered into the computerized system. Thus, balances are

updated continuously as transactions occur.

9. For automated systems that use electronic forms, the special journals are not used to record original

transactions. Rather, electronic forms capture the original transaction detail from an invoice, for

example, and automatically post the transaction details to the appropriate ledger accounts.

CHAPTER 5

ACCOUNTING SYSTEMS

DISCUSSION QUESTIONS

CHAPTER 5 Accounting Systems

PE 5-1A

PE 5-1B

Apr. 6 78 BlueBird Co. 1,710

11 79 Hitchcock Inc. 3,320

19 80 Fletcher Inc. 550

PE 5-2A

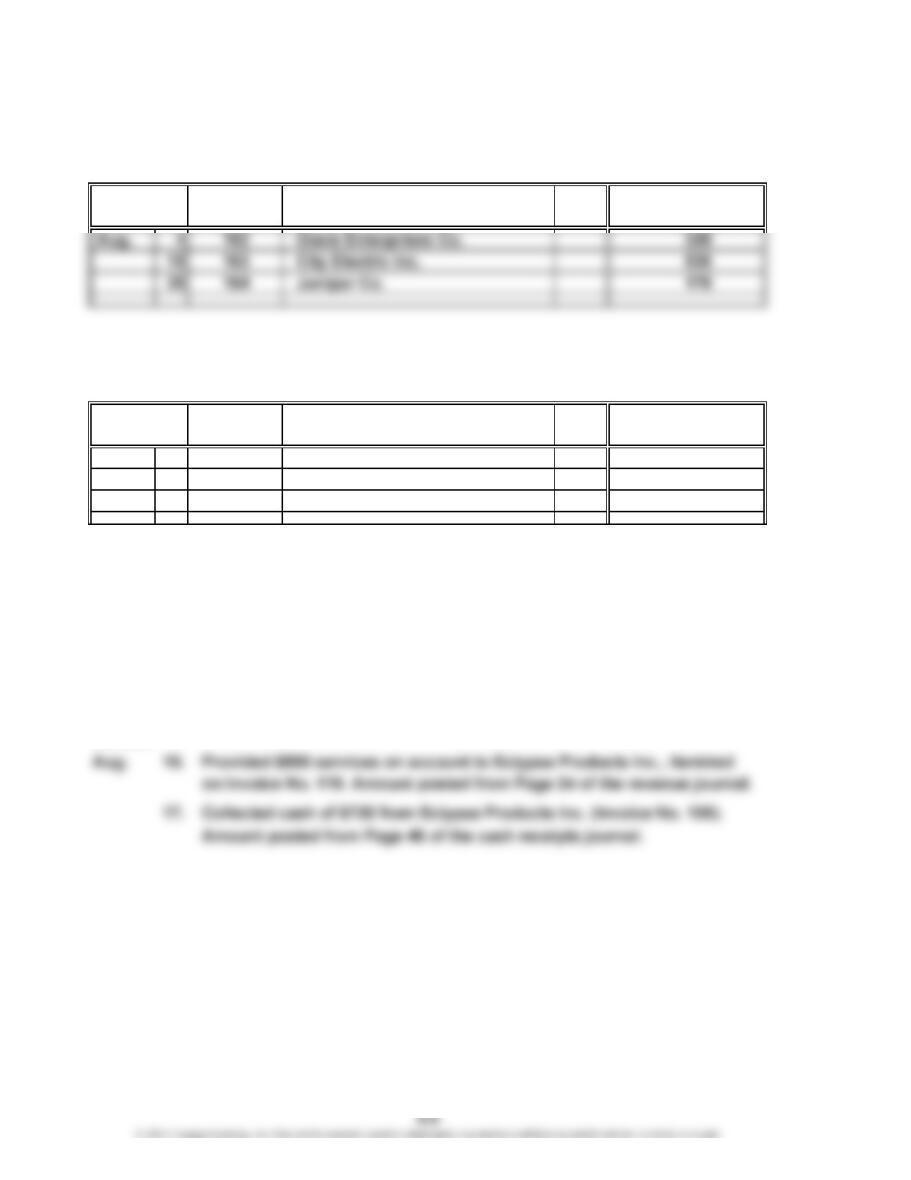

Feb. 22. Collected cash of $200 from Central Entertainment (Invoice No. 422).

Amount posted from Page 106 of the cash receipts journal.

27. Provided $280 of services on account to Central Entertainment,

itemized on Invoice No. 445. Amount posted from Page 92 of the revenue

journal.

PE 5-2B

Accounts Rec. Dr.

Fees Earned Cr.

Date

Invoice

No.

Post.

Ref.Account Debited

PRACTICE EXERCISES

REVENUE JOURNAL

REVENUE JOURNAL

Date

Invoice

No. Account Debited

Post.

Ref.

Accounts Rec. Dr.

Fees Earned Cr.

CHAPTER 5 Accounting Systems

PE 5-3A

PE 5-3B

Mar. 11 Gift Pack Supplies Inc. 820 820

Accounts

Payable

Cr.

Party

Supplies

Dr.

Other

Accounts

Dr.

PURCHASES JOURNAL

Other

Accounts

Post.

Post.

Accounts

Payable

Office

Supplies

Date

Account Credited

PURCHASES JOURNAL

Post.

Ref.

Post.

Ref.

Amount

CHAPTER 5 Accounting Systems

PE 5-4A

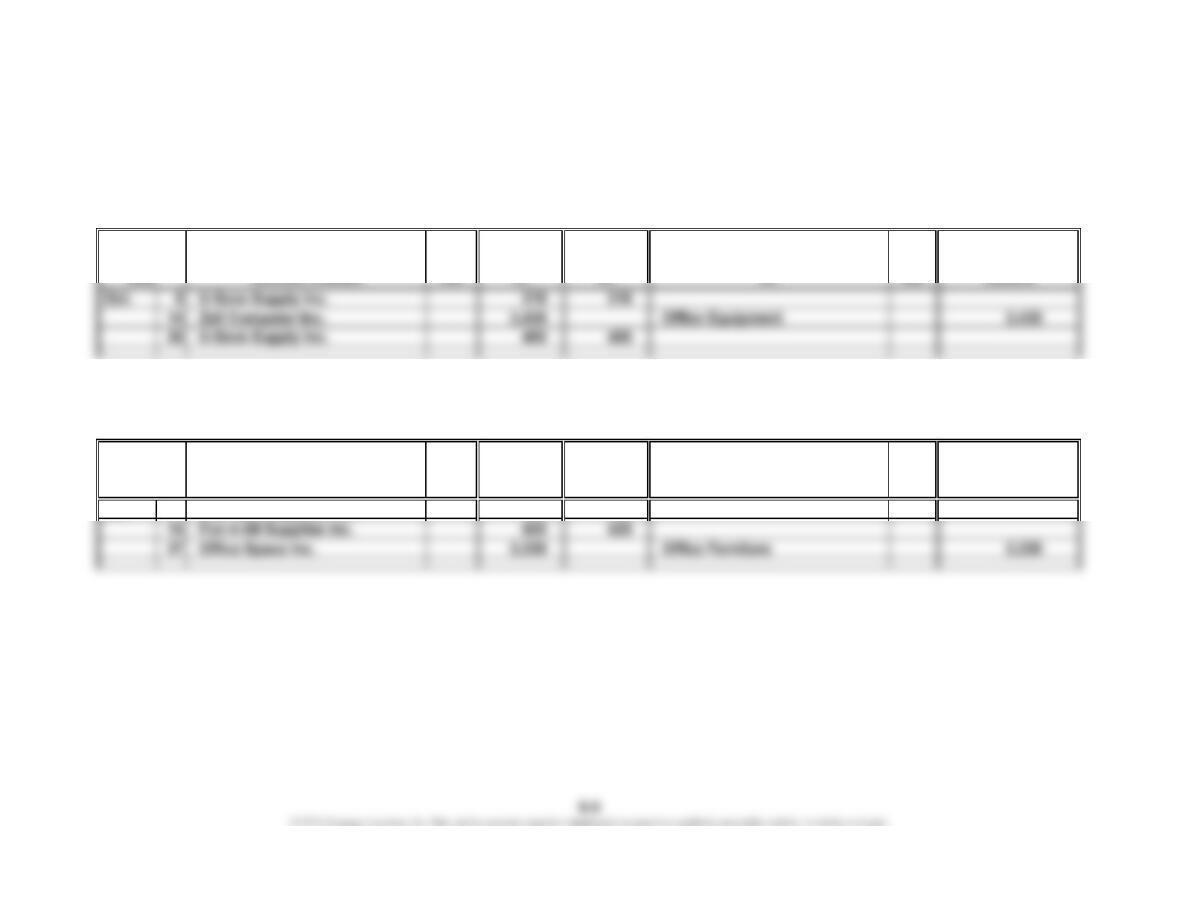

Nov. 11. Made purchases of $1,680 on account from Sunstar Technology

(Invoice No. 85). Amount posted from Page 8 of the purchases journal.

22. Paid $2,980 to Sunstar Technology on account (Invoice No. 43).

Amount posted from Page 46 of the cash payments journal.

PE 5-5A

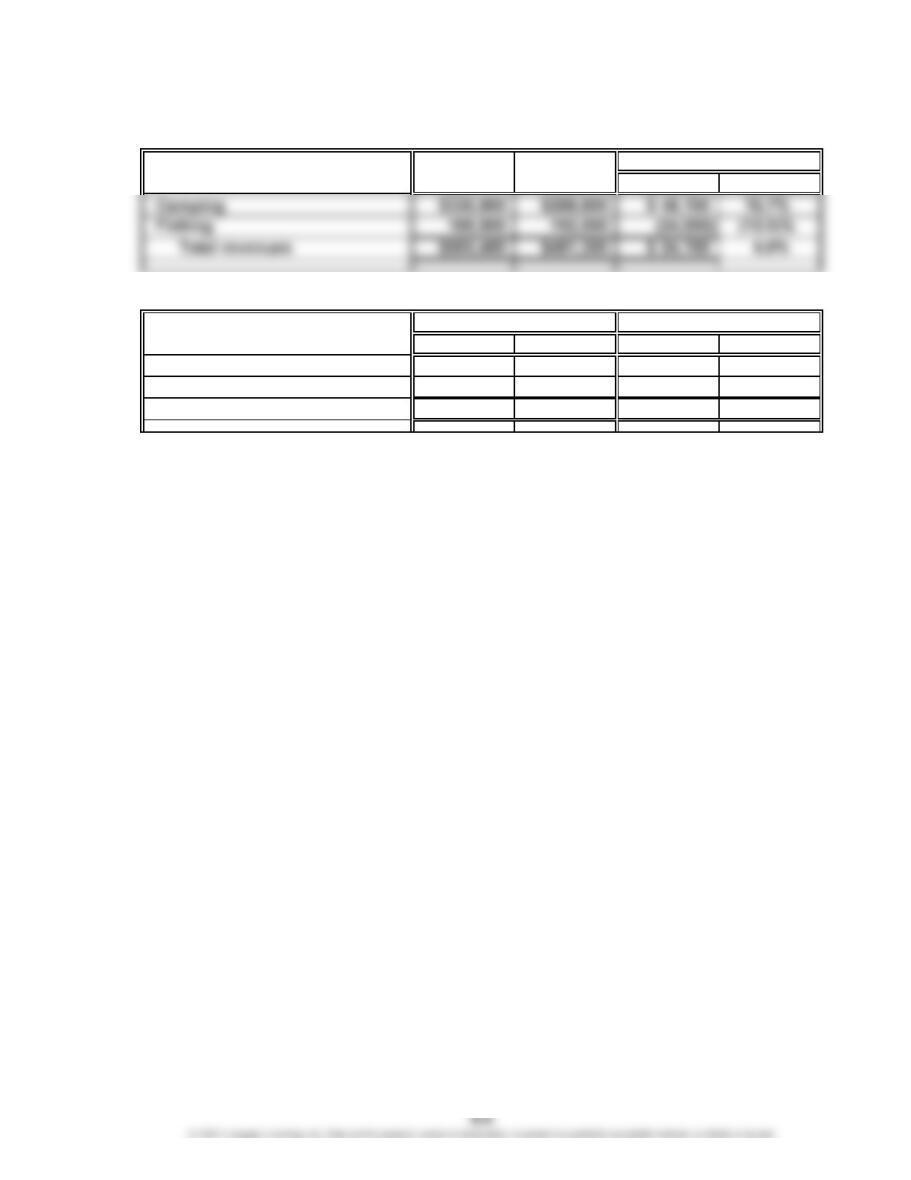

Horizontal analysis:

Vertical analysis:

Amount Percent Amount Percent

Retail $145,400 45.7% $138,500 42.3%

Wholesale 173,100 54.3% 189,300 57.7%

Total revenues $318,500 100.0% $327,800 100.0%

20Y5 20Y4

Increase/(Decrease)

CHAPTER 5 Accounting Systems

PE 5-5B

Horizontal analysis:

20Y3 20Y2 Amount Percent

Vertical analysis:

Amount Percent Amount Percent

Camping $336,900 66.7% $288,800 60.0%

Fishing 168,500 33.3% 192,500 40.0%

Total revenues $505,400 100.0% $481,300 100.0%

Increase/(Decrease)

20Y3 20Y2

CHAPTER 5 Accounting Systems

Ex. 5-1

1. General ledger accounts: (e)

2. Subsidiary ledger accounts: (a), (b), (c), (d)

Ex. 5-2

a., b., and c.

May 20 5,110 May 1 3,740

31 Bal. 5,110 31 Bal. 3,740

31 Bal. 3,340

d.

Alpha GenCorp

Hazmat Safety Co.

Ex. 5-3

a. Cash receipts journal f. Cash receipts journal

b. General journal g. Cash receipts journal

EXERCISES

Masco Co. Jordan Inc.

Accounts Receivable

Alpha GenCorp Hazmat Safety Co.

3,740

Westside Cleaners Inc.

Accounts Receivable Customer Balances

May 31, 20Y3

$ 5,110

CHAPTER 5 Accounting Systems

Ex. 5-4

a. Cash payments journal g. General journal

b. Purchases journal h. Cash payments journal

c. Purchases journal i. General journal

Ex. 5-5

Apr. 3. Provided service on account; posted from revenue journal Page 44.

6. Granted an invoice adjustment or corrected an error related to sale of

24. Received cash for balance due; posted from cash receipts journal Page 81.

Ex. 5-6

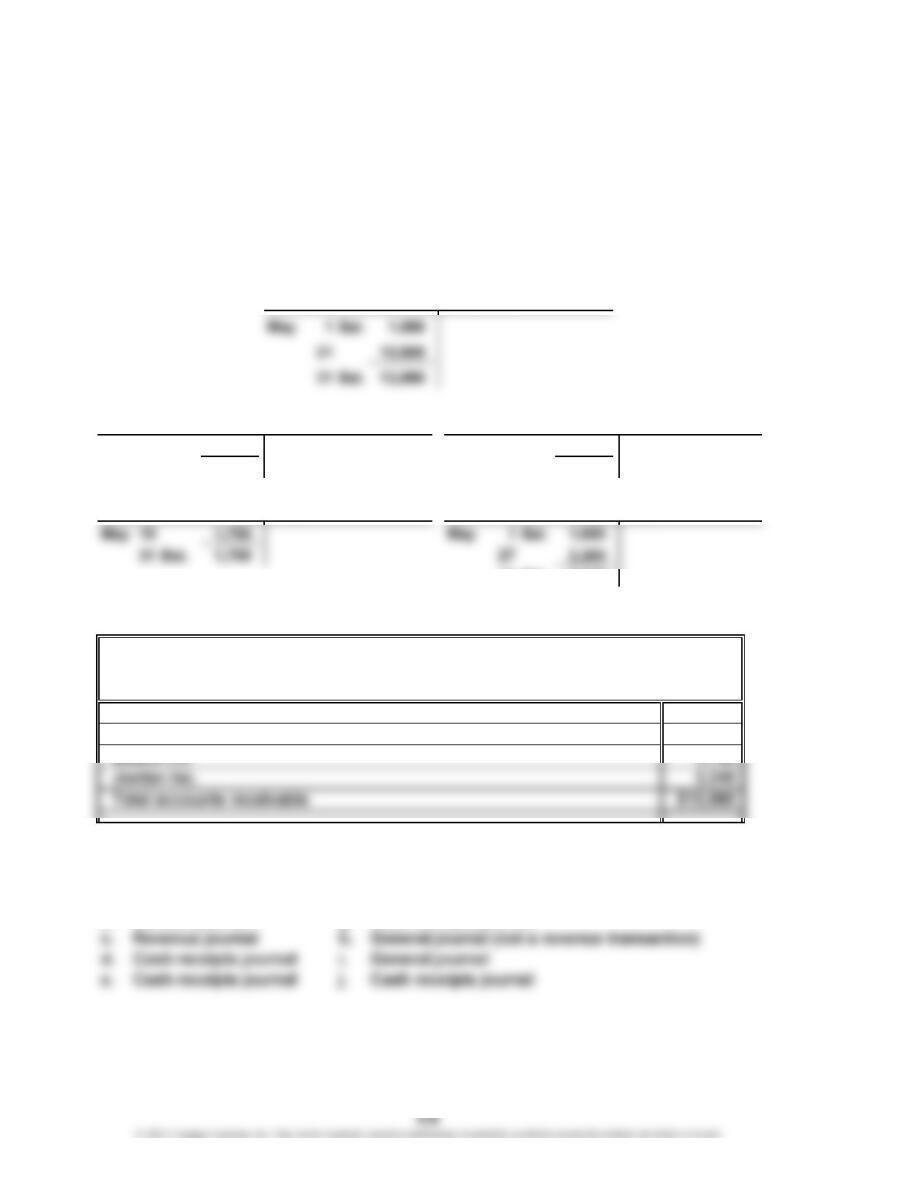

a.

Oct. 2 Pryor Corp. 1,625

c. $565 ($0 + $1,625 + $565 – $1,625)

REVENUE JOURNAL

Account Debited

Accounts Rec. Dr.

Fees Earned Cr.

Post.

Ref.

Date

Invoice

No.

321

CHAPTER 5 Accounting Systems

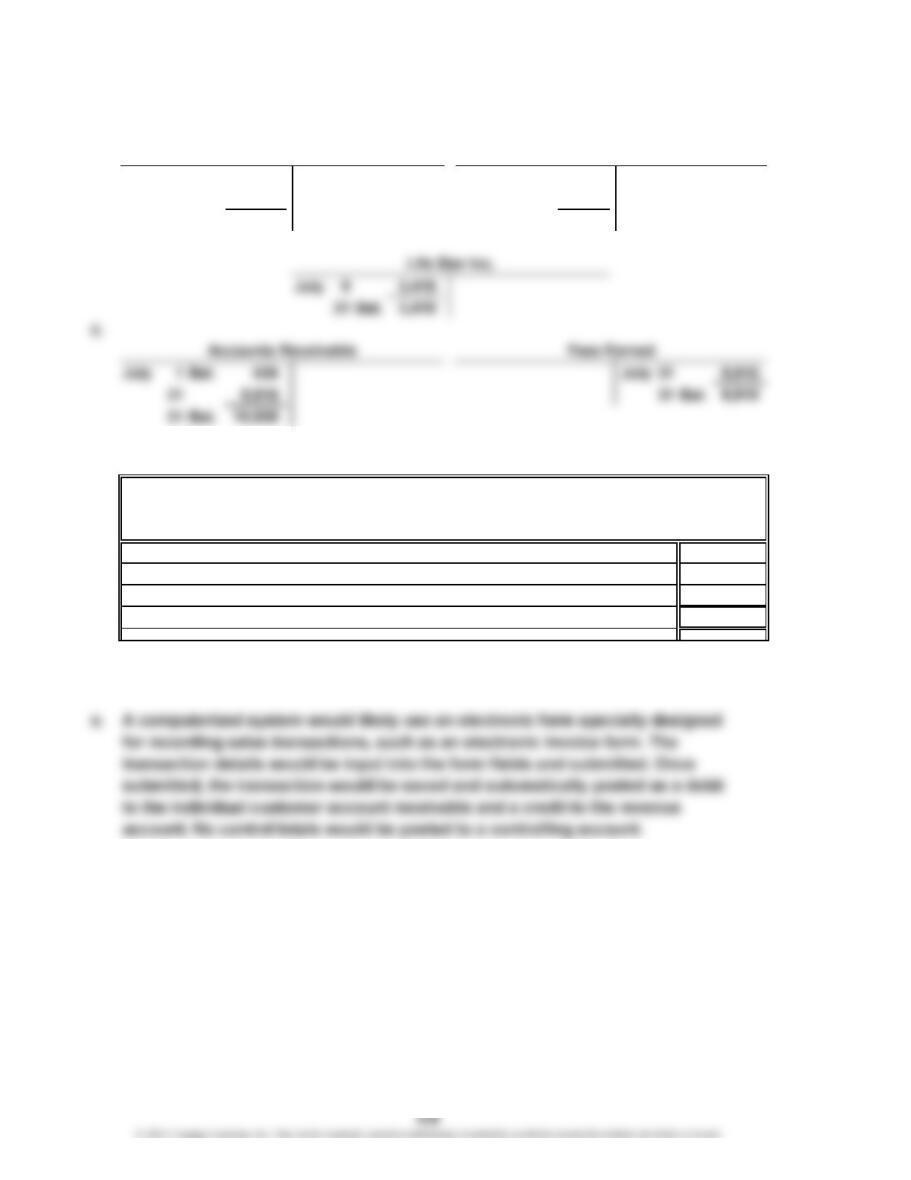

Ex. 5-7

a. and b.

July 1 Bal. 625 July 4 1,890

18 950 22 3,660

31 Bal. 1,575 31 Bal. 5,550

d.

Aladdin Co.

Clearmark Co.

Life Star Inc.

Total accounts receivable

The total in the schedule above agrees with the T account balance for the

accounts receivable controlling account in part (c).

Accounts Receivable Customer Balances

Aladdin Co. Clearmark Co.

Sapling Consulting Inc.

$10,535

July 31, 20Y2

$ 1,575

5,550

3,410

CHAPTER 5 Accounting Systems

Ex. 5-8

Amber Communications Inc. $ 4,550

Note: The balances are determined by adding the debits and subtracting the credits

for each subsidiary receivable account.

Balance, January 1, 20Y4 $ 4,720

Ex. 5-9

Invoice Post.

No. Ref.

20Y8

Mar. 2 512 Santorini Co.

31

20Y8

Mar. 4 CMI Inc.

19 Yarnell Inc.

2,135

Accounts Rec. Dr.

Account Debited Fees Earned Cr.

Birmingham Productions Inc.

Accounts Receivable Customer Balances

January 31, 20Y4

Accounts Receivable

(Controlling)

REVENUE JOURNAL

5,095

Cash

Dr.

Post.

Ref.Account Credited

Fees Earned

Cr.

Accts.

Rec. Cr.

CASH RECEIPTS JOURNAL

Date

Date

475

1,305

475

1,305

CHAPTER 5 Accounting Systems

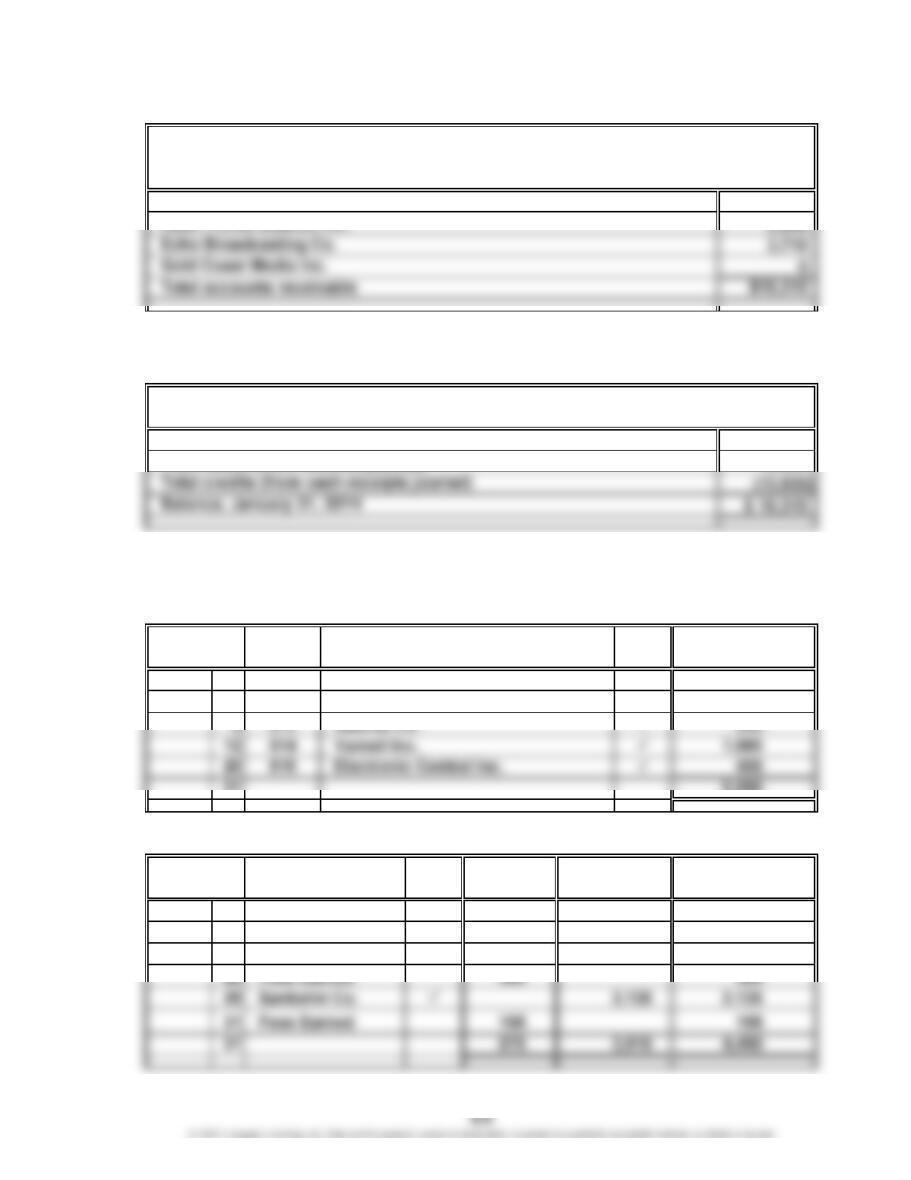

Ex. 5-10

a.

20Y5

Oct. 3 622 Palace Corp.

20Y5

Oct. 5 Champion Co. 1,060

12 Wayfarer Co. 1,450

b.

Amex Services Inc. $2,970

Sunny Style Inc. 1,940

The total of the customer accounts on October 31, 20Y5, $5,810, equals the

balance of the accounts receivable controlling account, shown as follows:

REVENUE JOURNAL

Account Debited

Post.

Ref.

Date

2,890

Accounts Rec. Dr.

Fees Earned Cr.

Invoice

No.

CASH RECEIPTS JOURNAL

Date

Cash

Dr.

Accts.

Rec.

Cr.

Fees

Earned

Cr.

1,060

1,450

Accounts Receivable

Lasting Summer Inc.

Accounts Receivable Customer Balances

October 31, 20Y5

Post.

Ref.

Account

Credited

CHAPTER 5 Accounting Systems

Ex. 5-10 (Concluded)

c. The accounts receivable subsidiary ledger is needed to track customer services

provided on account and customer collections. Without the subsidiary ledger,

Lasting Summer Inc. would not know who owes how much for services rendered.

Ex. 5-11

1. General ledger account: (g), (h), (i), (j), (k), (l)

2. Subsidiary ledger account: (a), (b), (c), (d), (e), (f)

3. No posting required: (m)

Ex. 5-13

June 6. Purchased services, supplies, equipment, or other commodities on

account; posted from purchases journal Page 49.

CHAPTER 5 Accounting Systems

Ex. 5-14

a.

Apr. 4 825 825

9 4,890 Office Equipment 4,890

Accts.

Payable

Cr.

Office

Supplies

Dr.

Other

Accounts

Dr.

Post.

Ref. Amount

PURCHASES JOURNAL

Post.

Ref.

Date

Account Credited

Officemate Inc.

Tek Village Inc.

CHAPTER 5 Accounting Systems

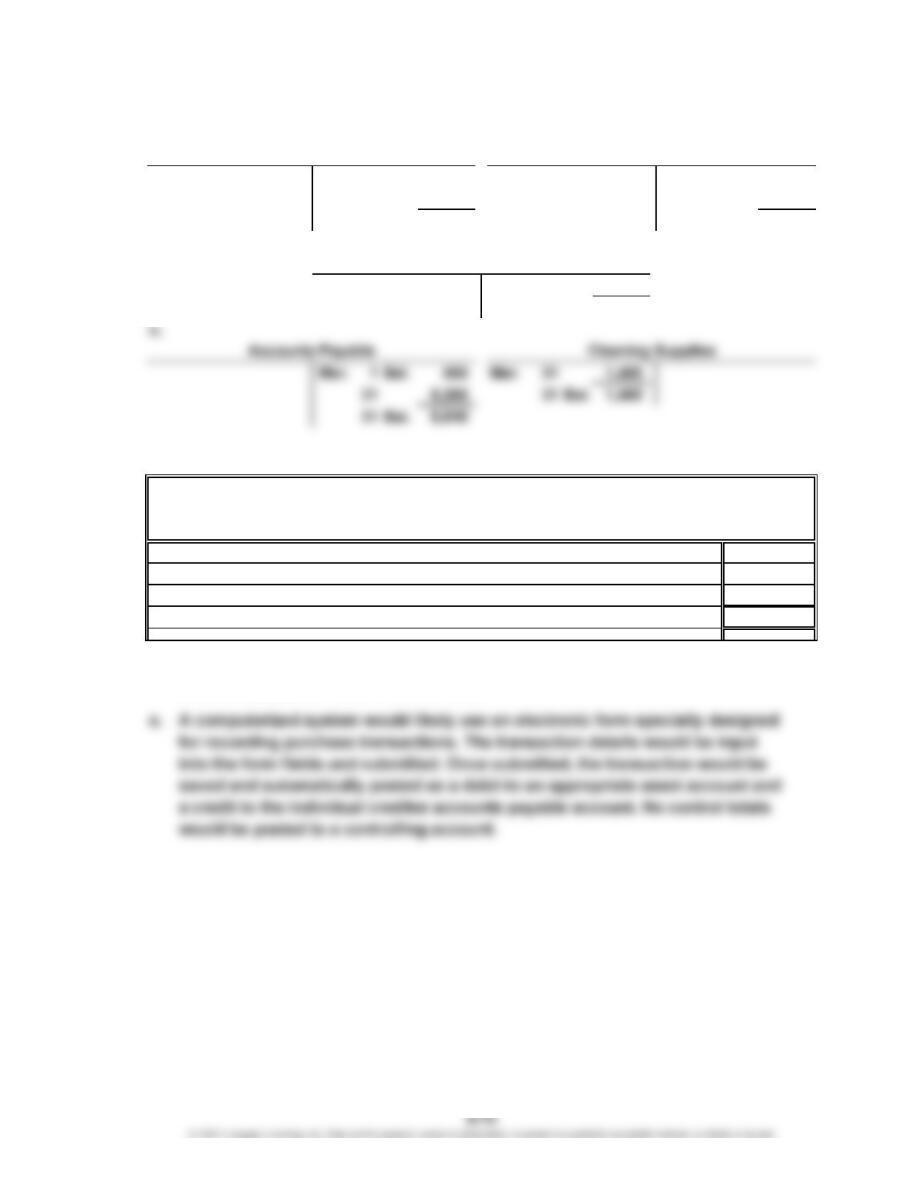

Ex. 5-15

a. and b.

Mar. 4 690 Mar. 1 Bal. 580

26 385 15 325

31 Bal. 1,075 31 Bal. 905

Mar. 20 3,860

31 Bal. 3,860

d.

Enviro-Wash Supplies Inc.

Nicely Co.

Office Mate Inc.

Total accounts payable

The total in the schedule above agrees with the T account balance for the

accounts payable control account in (c).

March 31, 20Y2

$1,075

905

3,860

$5,840

Accounts Payable Creditor Balances

Enviro-Wash Supplies Inc. Nicely Co.

Office Mate Inc.

Newmark Exterior Cleaners Inc.

CHAPTER 5 Accounting Systems

Ex. 5-16

Augusta Sod Co. $10,380

Concrete Equipment Co. 10,790

Note: The account balances are determined by subtracting the debits from the credits

for each account.

Balance, June 1, 20Y1 $ 3,590

Accounts Payable

(Controlling)

Magnolia Landscaping

Accounts Payable Creditor Balances

June 30, 20Y1

CHAPTER 5 Accounting Systems

Ex. 5-17

20Y5

May 3

20Y5

May 1 57 Bio Safe Supplies Inc. 345

8 58 Equipment 18 2,860

2,860

345

Other

Accounts

Dr.

Accounts

Payable

Dr.

Cash

Cr.

CASH PAYMENTS JOURNAL

Ck.

No.

Account Debited

PURCHASES JOURNAL

Date

Post.

Ref.

Accounts

Payable

Cr.

200

Date

Account Credited

Brite N’ Shine Products Inc.

Post.

Ref.

Post.

Ref.

Amount

Cleaning

Supplies

Dr.

Other

Accounts

Dr.

200

CHAPTER 5 Accounting Systems

Ex. 5-18

a.

20Y4

Sept. 4

20Y4

Sept. 6 345 Labradore Inc. 320

18 346 Meow Mart Inc. 300

Post.

Ref.

Amount

Pet

Supplies

Dr.

Other

Accounts

Dr.

Post.

Ref.

Date

Account Credited

Best Friend Supplies Inc.

Ck.

No.

Account Debited

PURCHASES JOURNAL

Date

Post.

Ref.

Accounts

Payable

Cr.

295

CASH PAYMENTS JOURNAL

295

Other

Accounts

Dr.

Accounts

Payable

Dr.

Cash

Cr.

320

300

CHAPTER 5 Accounting Systems

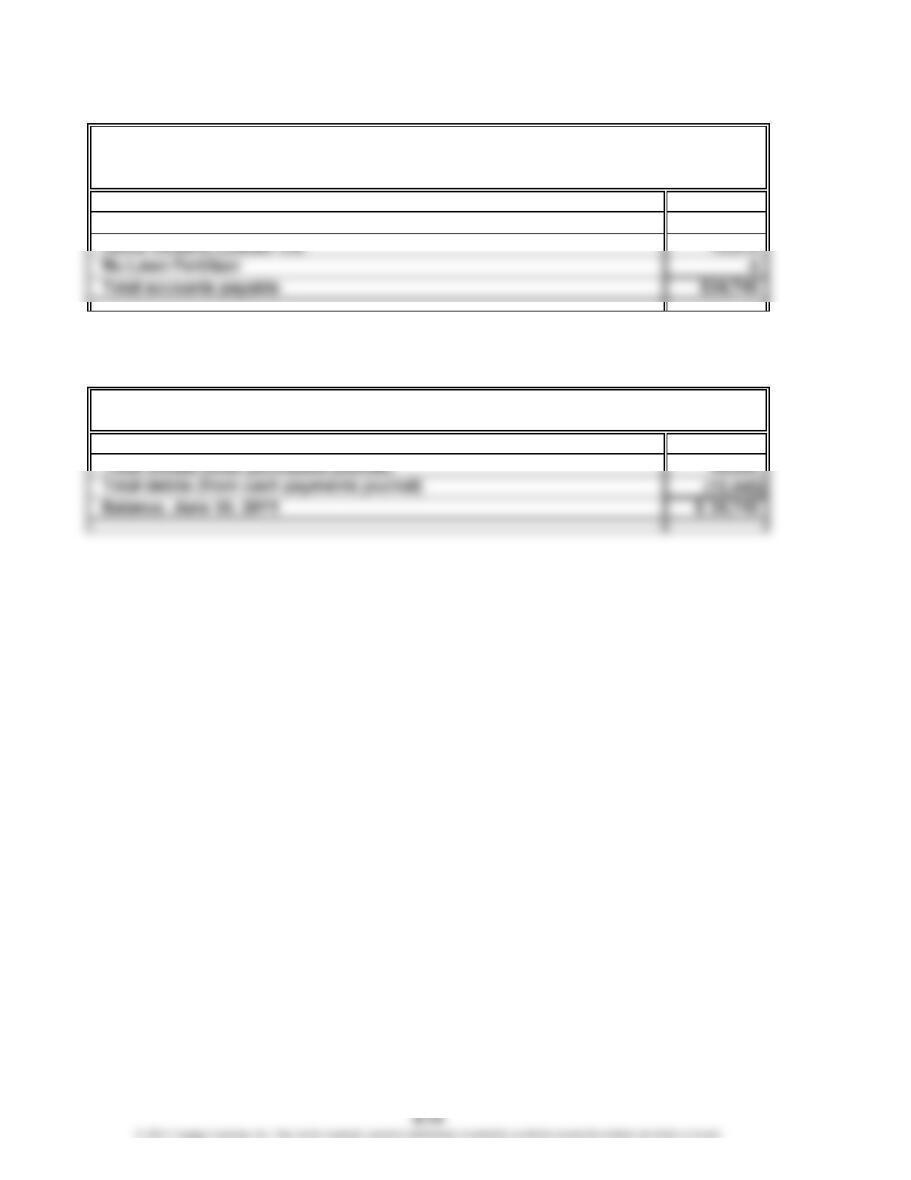

Ex. 5-18 (Concluded)

b.

Meow Mart Inc. $ 450

The total of the creditor accounts on September 30, 20Y4, $3,750, equals the

balance of the accounts payable controlling account, shown as follows:

Sept. 30 915 Sept. 1 Bal.

30

30 Bal.

Ex. 5-19

a. Two errors were made in balancing the accounts in the subsidiary ledger:

(1) The Carbon Supplies Inc. transaction of March 9 should have resulted in a

balance of $15,300 instead of $14,000, and the account balance at March 12

should have been $15,000 instead of $13,700. The account balance at March 20

should have been $9,200 instead of $7,900.

4,045

3,750

Accounts Payable

Happy Tails Inc.

Accounts Payable Creditor Balances

September 30, 20Y4

620

CHAPTER 5 Accounting Systems

Ex. 5-19 (Concluded)

b.

C. D. Greer and Son $15,750

Carbon Supplies Inc. 9,200

Cutler and Powell 7,800

Ex. 5-20

Cash receipts journal: (a)

Cash payments journal: (b)

Revenue journal: (c)

Purchases journal: (d)

General journal: (e)

Ex. 5-21

1. The Cash column is for debits (not credits).

A recommended and corrected cash receipts journal is as follows:

Page 12

Post.

Ref.

Account

Credited

Accts.

Rec.

Cr.

Other

Accounts

Cr.

Fees

Earned

Cr.

CASH RECEIPTS JOURNAL

Bunker Hill Assay Services Inc.

Accounts Payable Creditor Balances

March 31, 20Y4

Date

Cash

Dr.

CHAPTER 5 Accounting Systems

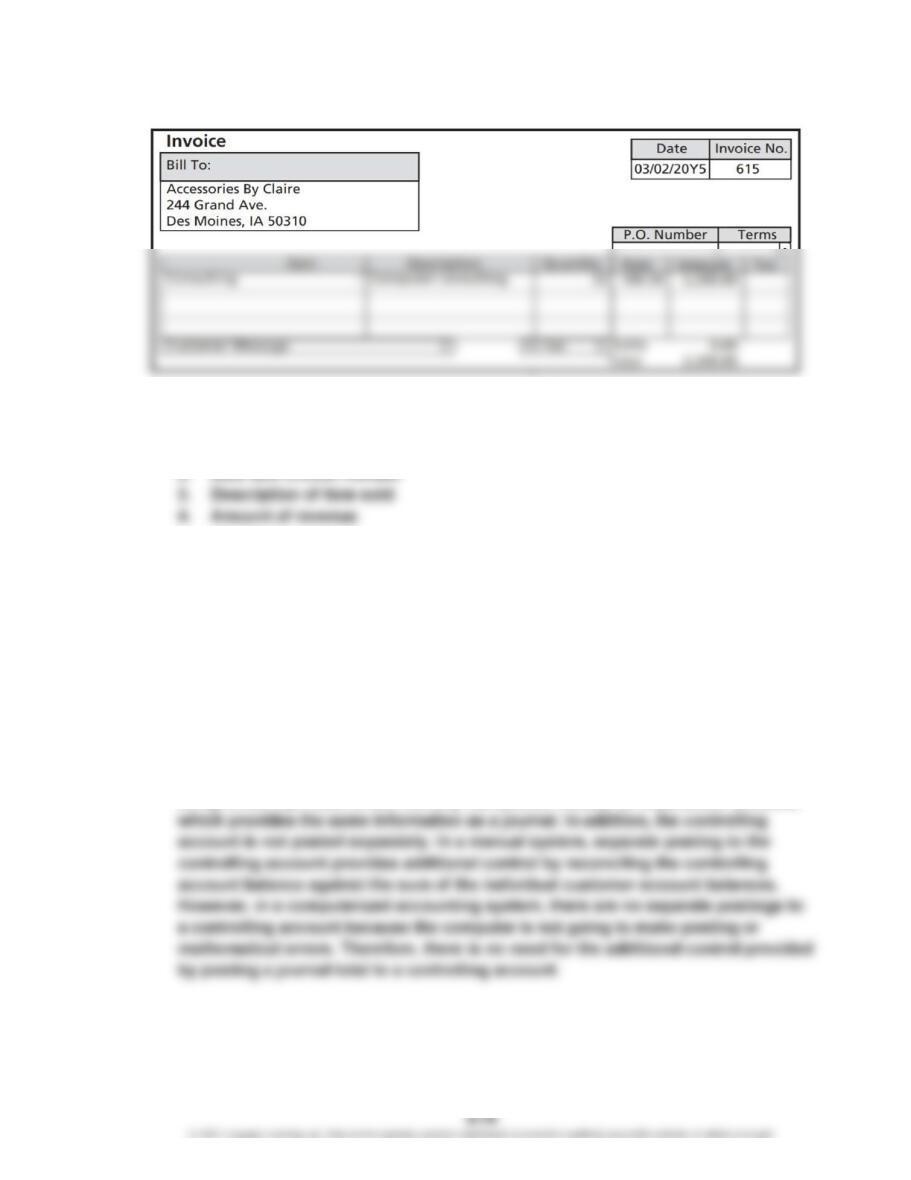

Ex. 5-22

a. In the electronic invoice form from QuickBooks

®

shown above, typical

fields for data input can be identified as follows:

1. Customer name and address

b. The customer Accounts Receivable is debited, and Fees Earned is credited.

A computerized accounting system does not require posting to a separate

accounts receivable control account. In this case, the total accounts receivable

reported on the balance sheet is merely the sum of the balances of the individual

customer account balances. That is, the accounts receivable account summarizes

the customer accounts automatically.

c. Controlling accounts are not posted at the end of the month in a computerized

accounting system. Transactions are recorded through data input into electronic

forms, into electronic special journals, or for infrequent transactions, by an

electronic general journal. Balances of affected accounts are automatically posted

and updated from the information recorded on the form. If desired, the computer

CHAPTER 5 Accounting Systems

Ex. 5-23

a. iTunes is an example of a B2C, or business-to-consumer, e-commerce application.

The B, or business, is Apple. The C, or consumers, would mostly be individuals

who purchase digital products from the iTunes Store.

d. The electronic invoice form could be used for either transactions on account, as

illustrated in the chapter, or for cash sales. The invoice form used for sales on

account is different from the one used for cash sales. The latter invoice form

makes a debit to Cash, rather than a debit to a customer account.

Ex. 5-24

a. Amazon.com B2C and B2B. Sells books, DVDs, and other products

to individual consumers. Businesses can also set up

pages on Amazon for a small fee.

b. Dell Inc. B2C and B2B. Sells computer products to both

individuals and corporations. Its site separates

individual and corporate sales.

c. DowDuPont Inc. B2B. Specialt

y

chemicals. DuPont Direc

t

® is its B2B