CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN)

SUPPORT DEPARTMENT AND JOINT COST ALLOCATION

DISCUSSION QUESTIONS

1. Support department costs are only indirectly related to production, so it can be difficult to find an

appropriate cost driver for applying these costs to a product. For example, maintenance services are

necessary for safe and efficient production, but applying maintenance costs to products based on

units produced, batches run, or the number of product lines is not entirely accurate, because none

of these potential drivers cause, by themselves, the maintenance cost to occur.

3. When a single driver is used for all overhead costs, it is unlikely that the driver selected is

5. Management normally determines the order based on the following: Departments with higher costs

are allocated earlier, departmments serving a large number of support departments are allocated

earlier, and departments with more accurate cost drivers are allocated earlier.

6. Large companies are more likely to use the reciprocal services method. This is because the larger a

company is, the more likely it is that cost allocation methods will yield substantially different

results. Thus, the cost of using the more accurate reciprocal services method will be justified in

spite of the complexity of this method.

9. Revenue from by-products is most often either used to offset the cost of the joint production

process or reported as other reveue on the income statement with no related cost of goods sold.

10. Production employees are often evaluated, at least in part, on their ability to keep production

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

BASIC EXERCISES

BE 19–1 (FIN MAN); BE 5–1 (MAN)

a. Percentage of Janitorial costs to be allocated to the Assembly Department:

46,400 ÷ (33,600 + 46,400) = 58%

BE 19–2 (FIN MAN); BE 5–2 (MAN)

a. Percentage of Cafeteria costs to be allocated to the Molding Department:

27 ÷ (27 + 30 + 3) = 45%

BE 19–3 (FIN MAN); BE 5–3 (MAN)

a. Percentage of Janitorial costs to be allocated to the Security Department:

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

BE 19–4 (FIN MAN); BE 5–4 (MAN)

Joint Product

Guns per Batch

Proportion

Joint Costs

Allocation

BE 19–5 (FIN MAN); BE 5–5 (MAN)

Joint Product

Knife Blades at

Split-Off

Weight Factor

Weighted Blades

of Molding Time

Weighted

Percent of

Molding Time

Joint Costs

Allocation

Red oak handle carving knife

$6,500

$4,875

$6,500

BE 19–6 (FIN MAN); BE 5–6 (MAN)

Joint Product

Door Handles at

Split-Off

Selling Price

per Door

Handle at

Split-Off

Total Market

Value at Split-Off

Percent of Total

Market Value at

Split-Off

Joint Costs

Allocation

Standard door handle

2,000

$4

$ 8,000

80%

$29,000

$23,200

Curved door handle

29,000

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

EXERCISES

Ex. 19–1 (FIN MAN); Ex. 5–1 (MAN)

Support Department 1 cost allocation:

Production Department 1:

1,400 ÷ (1,400 + 100 + 500) = 70%

70% × $142,000 = $99,400

5% × $142,000 = $7,100

Production Department 3:

500 ÷ (1,400 + 100 + 500) = 25%

Ex. 19–2 (FIN MAN); Ex. 5–2 (MAN)

Support Department 1 cost allocation:

Support Department 2:

7 ÷ (7 + 25 + 18) = 14%

14% × $20,000 = $2,800

50% × $20,000 = $10,000

36% × $20,000 = $7,200

Ex. 19–3 (FIN MAN); Ex. 5–3 (MAN)

Total cost to be allocated from Security Department (S):

Total costs of Security Department include 10 ÷ (10 + 40 + 50) = 10% of Cafeteria

Department costs

Thus, S = $273,000 + (0.1 × C)

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

Ex. 19–3 (FIN MAN); Ex. 5–3 (MAN) (Concluded)

Security Department cost allocation:

Cafeteria Department:

2,400 ÷ (2,400 + 4,000 + 1,600) = 30%

30% × $300,000 = $90,000

Laser Department:

4,000 ÷ (2,400 + 4,000 + 1,600) = 50%

50% × $300,000 = $150,000

Forming Department:

1,600 ÷ (2,400 + 4,000 + 1,600) = 20%

20% × $300,000 = $60,000

Ex. 19–4 (FIN MAN); Ex. 5–4 (MAN)

Maintenance Department cost allocation:

Cutting Department:

9 ÷ (9 + 1) = 90%

90% × $7,800 = $7,020

Pruning Department:

1 ÷ (9 + 1) = 10%

25% × $5,000 = $1,250

Pruning Department:

10% × $7,800 = $780

Production departments’ total costs:

Cutting Department:

$7,020 + $1,250 + $54,500 = $62,770

Pruning Department:

$780 + $3,750 + $11,000 = $15,530

Ex. 19–5 (FIN MAN); Ex. 5–5 (MAN)

Security Department cost allocation:

10% × $3,000 = $300

3,200 ÷ (800 + 3,200 + 4,000) = 40%

40% × $3,000 = $1,200

4,000 ÷ (800 + 3,200 + 4,000) = 50%

50% × $3,000 = $1,500

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

Ex. 19–5 (FIN MAN); Ex. 5–5 (MAN) (Concluded)

Maintenance Department cost allocation:

Cutting Department:

3,700 ÷ (3,700 + 5,550) = 40%

40% × $2,600 = $1,040

60% × $2,600 = $1,560

Sewing Department:

$1,500 + $1,560 + $20,800 = $23,860

Ex. 19–6 (FIN MAN); Ex. 5–6 (MAN)

Total cost to be allocated from Maintenance Department (M):

Total costs of Maintenance include $2,000 ÷ ($2,000 + $2,500 + $5,500) = 20%

of Security costs

Thus, M = $36,000 + (0.2 × S)

Now plug the value for S into the M equation:

M = $36,000 + (0.2 × $20,000)

= $36,000 + $4,000

= $40,000

Maintenance Department cost allocation:

Security Department:

2,000 ÷ (2,000 + 7,200 + 10,800) = 10%

10% × $40,000 = $4,000

Cutting Department:

7,200 ÷ (2,000 + 7,200 + 10,800) = 36%

36% × $40,000 = $14,400

Sewing Department:

10,800 ÷ (2,000 + 7,200 + 10,800) = 54%

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

Ex. 19–6 (FIN MAN); Ex. 5–6 (MAN) (Concluded)

Security Department cost allocation:

Maintenance Department:

$2,000 ÷ ($2,000 + $2,500 + $5,500) = 20%

20% × $20,000 = $4,000

Cutting Department:

$2,500 ÷ ($2,000 + $2,500 + $5,500) = 25%

25% × $20,000 = $5,000

Sewing Department:

$5,500 ÷ ($2,000 + $2,500 + $5,500) = 55%

55% × $20,000 = $11,000

Production departments’ total costs:

Cutting Department:

$14,400 + $5,000 + $64,000 = $83,400

Sewing Department:

$21,600 + $11,000 + $82,000 = $114,600

Ex. 19–7 (FIN MAN); Ex. 5–7 (MAN)

Janitorial Department cost allocation:

20% × $310,000 = $62,000

Assembly Department:

4,000 ÷ (1,000 + 4,000) = 80%

80% × $310,000 = $248,000

Cafeteria Department cost allocation:

Cutting Department:

30 ÷ (30 + 10) = 75%

75% × $169,000 = $126,750

Assembly Department:

10 ÷ (30 + 10) = 25%

25% × $169,000 = $42,250

Ex. 19–8 (FIN MAN); Ex. 5–8 (MAN)

Cafeteria Department:

5,000 ÷ (5,000 + 1,000 + 4,000) = 50%

50% × $310,000 = $155,000

Cutting Department:

1,000 ÷ (5,000 + 1,000 + 4,000) = 10%

10% × $310,000 = $31,000

Assembly Department:

4,000 ÷ (5,000 + 1,000 + 4,000) = 40%

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

Ex. 19–8 (FIN MAN); Ex. 5–8 (MAN) (Concluded)

Cafeteria Department total cost to be allocated:

$169,000 + $155,000 = $324,000

Ex. 19–9 (FIN MAN); Ex. 5–9 (MAN)

Total cost to be allocated from the Janitorial Department (J):

Total costs of Janitorial include 10 ÷ (10 + 30 + 10) = 20% of Cafeteria costs

J = $310,000 + (0.2 × C)

Now plug the value for C into the J equation:

J = $310,000 + (0.2 × $360,000)

= $310,000 + $72,000

= $382,000

Janitorial Department cost allocation:

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

Ex. 19–9 (FIN MAN); Ex. 5–9 (MAN) (Concluded)

Cafeteria Department cost allocation:

Janitorial Department:

10 ÷ (10 + 30 + 10) = 20%

20% × $360,000 = $72,000

Ex. 19–10 (FIN MAN); Ex. 5–10 (MAN)

a. Under the direct method, the Assembly Department is allocated the most

support department costs, as follows:

Cutting Department:

$62,000 + $126,750 = $188,750

Assembly Department:

$248,000 + $42,250 = $290,250

Cutting Department:

$38,200 + $216,000 = $254,200

Assembly Department:

$152,800 + $72,000 = $224,800

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

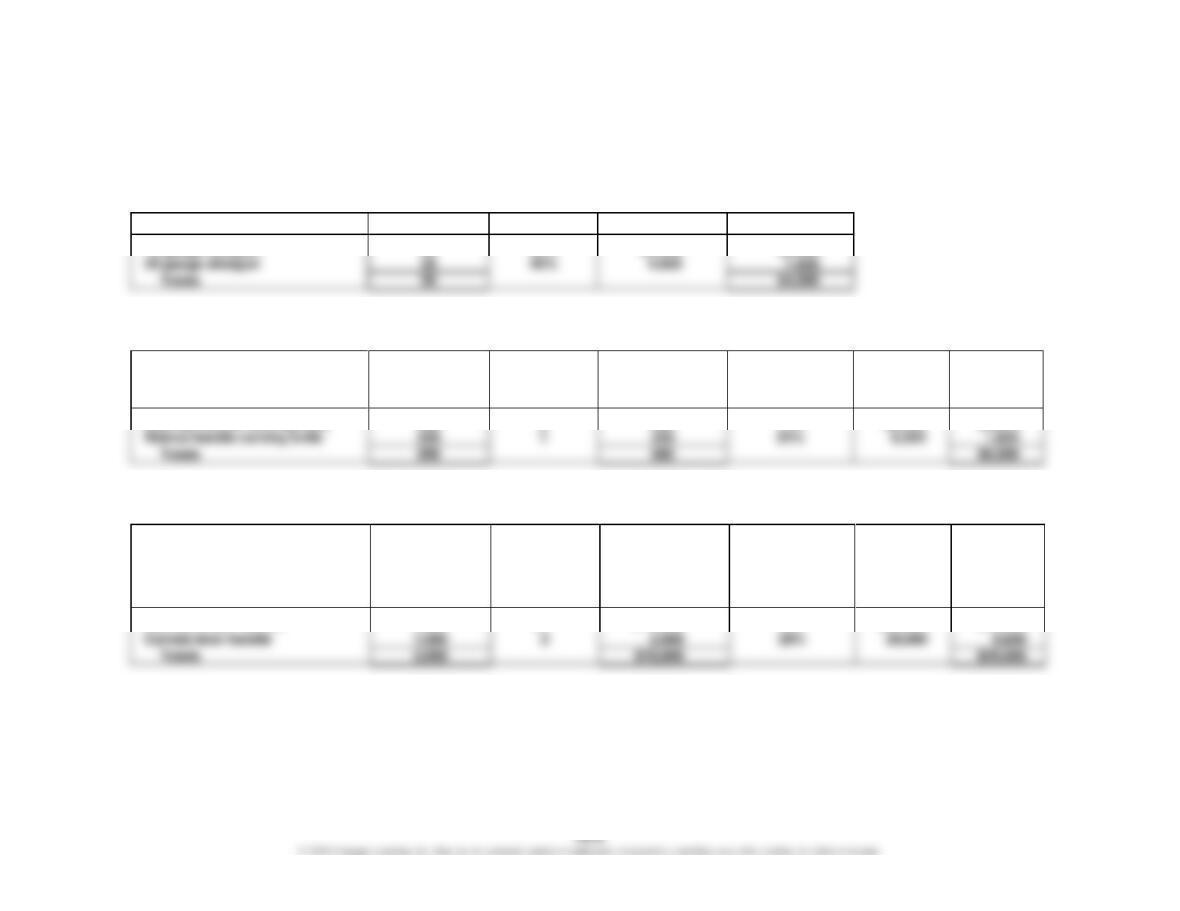

Ex. 19–11 (FIN MAN); Ex. 5–11 (MAN)

Joint Product

Boards

per Batch

Proportion

Joint Costs

Allocation

Washed

45

45%

$710

$319.50

Stained

35

35%

710

248.50

Pressure treated

20

20%

710

142.00

Totals

100

$710.00

Sawdust

Wood chips

Ex. 19–13 (FIN MAN); Ex. 5–13 (MAN)

Split-Off

Raw sugar

900

500

Pounds at

Market Value

per Pound at

Total Market

Value at

Percent of

Total Market

Value at

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

Ex. 19–14 (FIN MAN); Ex. 5–14 (MAN)

Joint Product

Cubic Yards

per Batch

Market Value

per Cubic

Yard at

Split-Off

Total Market

Value at

Split-Off

Market

Price

per Cubic

Yard

Added

Cost per

Cubic

Yard

Net Realizable

Value per

Cubic Yard

Total Net

Realizable

Value

Greater of Total

NRV and Market

Value at Split-Off

Proportion

Joint Costs

Allocation

Wood pulp

198,528

6,400

Mulch

338,400

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

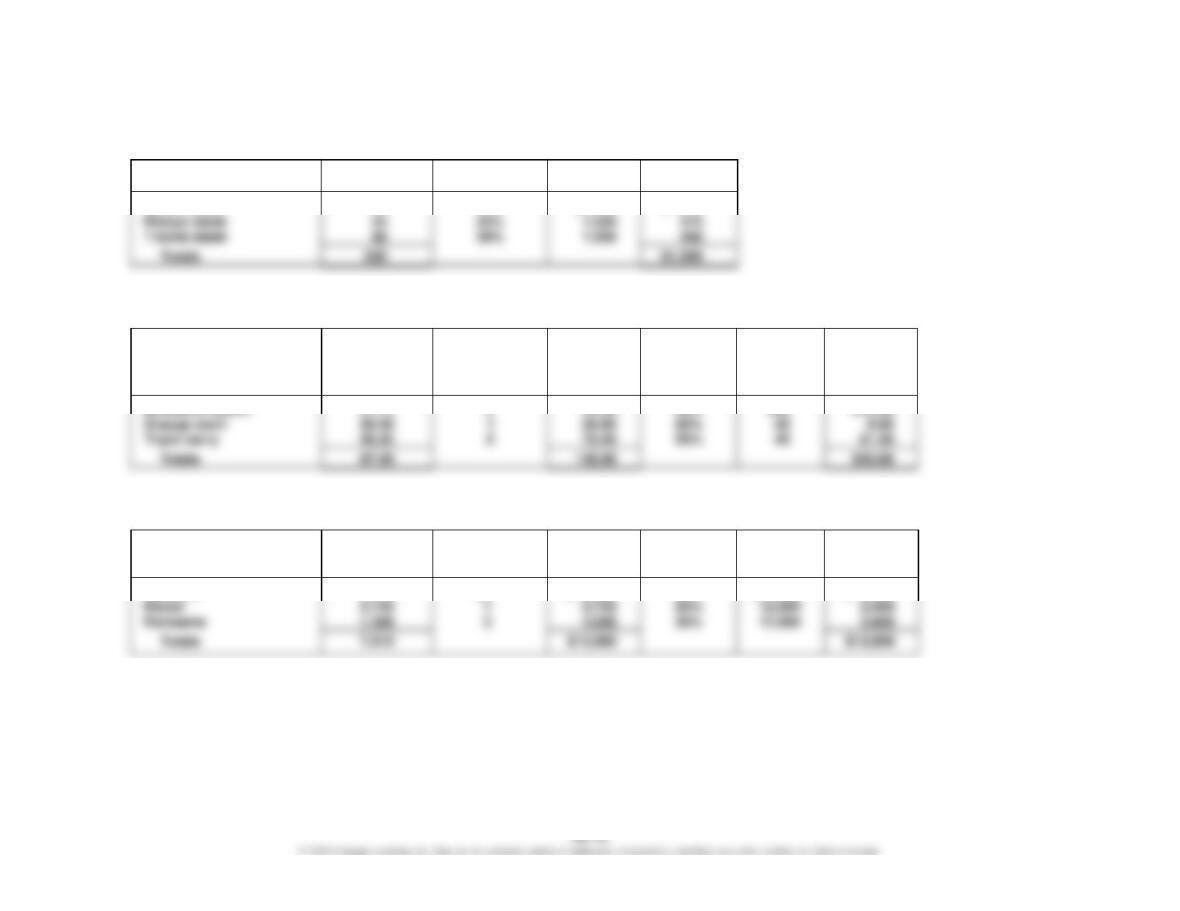

Ex. 19–15 (FIN MAN); Ex. 5–15 (MAN)

Joint Product

Pounds at

Split-Off

Proportion

Joint Costs

Allocation

Sirloin steak

99

45%

$1,500

$ 675

Ex. 19–16 (FIN MAN); Ex. 5–16 (MAN)

Joint Product

Cups per

Batch

Weight

Factor

Weighted

Cups of

Mixing Time

Weighted

Percent of

Mixing Time

Joint Costs

Allocation

Ex. 19–17 (FIN MAN); Ex. 5–17 (MAN)

Joint Product

Gallons per

Batch

Market Value

per Gallon at

Split-Off

Total Market

Value at

Split-Off

Percent of

Total MV at

Split-Off

Joint Costs

Allocation

Gasoline

3,415

$2

$ 6,830

50%

$12,000

$ 6,000

Diesel

12,000

Kerosene

1,366

30%

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

Ex. 19–18 (FIN MAN); Ex. 5–18 (MAN)

Joint Product

Cups per

Batch

Market

Value per

Cup at Split-

Off

Total

Market

Value at

Split-Off

Market Price

per Cup

Added Cost

per Batch

Total Net

Realizable

Value

Greater of

Total NRV and

Market Value at

Split-Off

Proportion

Joint Costs

Allocation

Pure lemonade

32

$0.80

$25.60

$0.80

$ —

$25.60

$25.60

40%

$30

$12

1.00

19.20

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

PROBLEMS

Prob. 19–1A (FIN MAN); Prob. 5–1A (MAN)

1. Blue Mountain Masterpieces would most likely use the direct method, because its

2. Janitorial Department cost allocation:

Printing Department:

4,230 ÷ (4,230 + 4,770) = 47%

47% × $5,200 = $2,444

53% × $5,200 = $2,756

59% × $6,600 = $3,894

Framing Department:

$8,610 ÷ ($12,390 + $8,610) = 41%

3. Using asset value, the Printing Department receives more of the Security

Department costs than the Framing Department, because the Printing Department

has higher asset value than the Framing Department. However, because the

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

Prob. 19–2A (FIN MAN); Prob. 5–2A (MAN)

1. Maintenance costs should not continue to be allocated based on machine hours,

because a more accurate cost driver for maintenance costs has been identified

2. Total cost to be allocated from Maintenance (M):

Total costs of Maintenance include $200,000 ÷ ($200,000 + $300,000 + $300,000)

= 25% of Security costs

Thus, M = $25,000 + (0.25 × S)

Now plug the value for S into the M equation:

M = $25,000 + (0.25 × $50,000)

= $25,000 + $12,500

= $37,500

Maintenance cost allocation:

Security:

20 ÷ (20 + 60 + 20) = 20%

20% × $37,500 = $7,500

60% × $37,500 = $22,500

CHAPTER 19 (FIN MAN); CHAPTER 5 (MAN) Support Department and Joint Cost Allocation

Prob. 19–2A (FIN MAN); Prob. 5–2A (MAN) (Concluded)

Security cost allocation:

Maintenance:

$200,000 ÷ ($200,000 + $120,000 + $480,000) = 25%

25% × $50,000 = $12,500

Mining:

$120,000 ÷ ($200,000 + $120,000 + $480,000) = 15%

15% × $50,000 = $7,500

Cutting:

$480,000 ÷ ($200,000 + $120,000 + $480,000) = 60%

60% × $50,000 = $30,000

Production activities total costs:

Mining:

$22,500 + $7,500 + $160,000 = $190,000

Cutting:

$7,500 + $30,000 + $95,000 = $132,500

3. Maintenance cost allocation:

Mining:

75% × $25,000 = $18,750

Cutting:

25% × $25,000 = $6,250

Security cost allocation:

Mining:

$120,000 ÷ ($120,000 + $480,000) = 20%

20% × $42,500 = $8,500

Cutting:

$480,000 ÷ ($120,000 + $480,000) = 80%

80% × $42,500 = $34,000

Production activities total costs:

Mining:

$18,750 + $8,500 + $160,000 = $187,250

Cutting:

$6,250 + $34,000 + $95,000 = $135,250