Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

5-21

EXERCISE 5-44 (20 MINUTES)

There are many key activities that can be suggested for each business. Some possibilities

are listed below. After each activity, a suggested cost driver is given in parentheses.

(1)

airline:

(a)

reservations (reservations booked)

(2)

restaurant

(a)

purchasing (pounds or cost of food purchased)

(3)

fitness club:

(a)

front desk operations (number of patrons)

(4)

bank:

(a)

teller window operations (number of customers)

(e)

security (number of customers)

(5)

hotel:

(a)

front desk operations (number of guests)

(6)

hospital:

(a)

admissions (patients admitted)

Chapter 05 - Activity-Based Costing and Management

5-22

SOLUTIONS TO PROBLEMS

PROBLEM 5-45 (35 MINUTES)

2. Allocation of administrative cost based on billable hours:

Information

5-23

PROBLEM 5-45 (CONTINUED)

3. Activity-based application rates:

Activity

Cost

Activity

Driver

Application

Rate

Staff support, in-house computing, and miscellaneous office charges of e-commerce

consulting and information systems services:

Activity

E-Commerce

Consulting

Information

Systems

Services

Staff support:

5-24

PROBLEM 5-45 (CONTINUED)

Profitability e-commerce consulting and information systems services:

E-Commerce

Consulting

Information

Systems

Services

Billings:

4. Yes, his attitude should change. Even though both services are needed and

professionals are paid the same rate, the income percentages show that e-commerce

5. Probably not. Although both services produce an attractive return for Clark and

Chapter 05 - Activity-Based Costing and Management

5-25

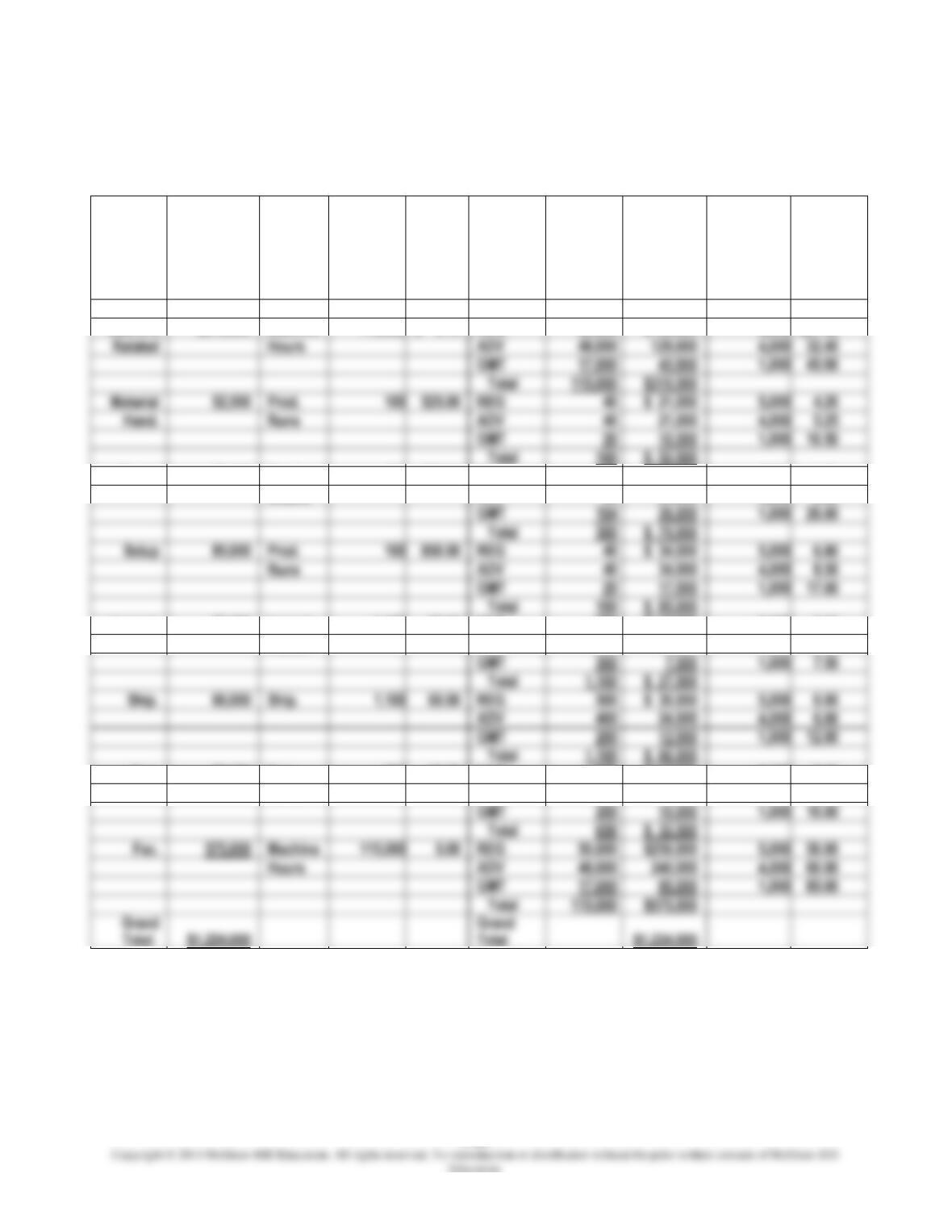

PROBLEM 5-46 (60 MINUTES)

1. The predetermined overhead rate is calculated as follows:

*Direct labor, budgeted hours:

Chapter 05 - Activity-Based Costing and Management

5-26

PROBLEM 5-46 (CONTINUED)

2. Activity-based-costing analysis:

Activity

Activity

Cost Pool

Cost

Driver

Cost

Driver

Quantity

Pool

Rate

Product

Line

Cost

Driver

Quantity

for

Product

Line

Activity

Cost for

Product

Line

Product

Line

Prod.

Volume

Activity

Cost per

Unit of

Product

Machine

$310,500

Machine

115,000

$ 2.70

REG

50,000

$135,000

5,000

$27.00

Purch.

75,000

Purch.

300

250.00

REG

100

$ 25,000

5,000

5.00

Orders

ADV

96

24,000

4,000

6.00

Inspect.

27,500

Inspect.

1,100

25.00

REG

400

$ 10,000

5,000

2.00

Hours

ADV

400

10,000

4,000

2.50

Eng.

32,500

Eng.

650

50.00

REG

250

$ 12,500

5,000

2.50

Hours

ADV

200

10,000

4,000

2.50

Chapter 05 - Activity-Based Costing and Management

5-27

PROBLEM 5-46 (CONTINUED)

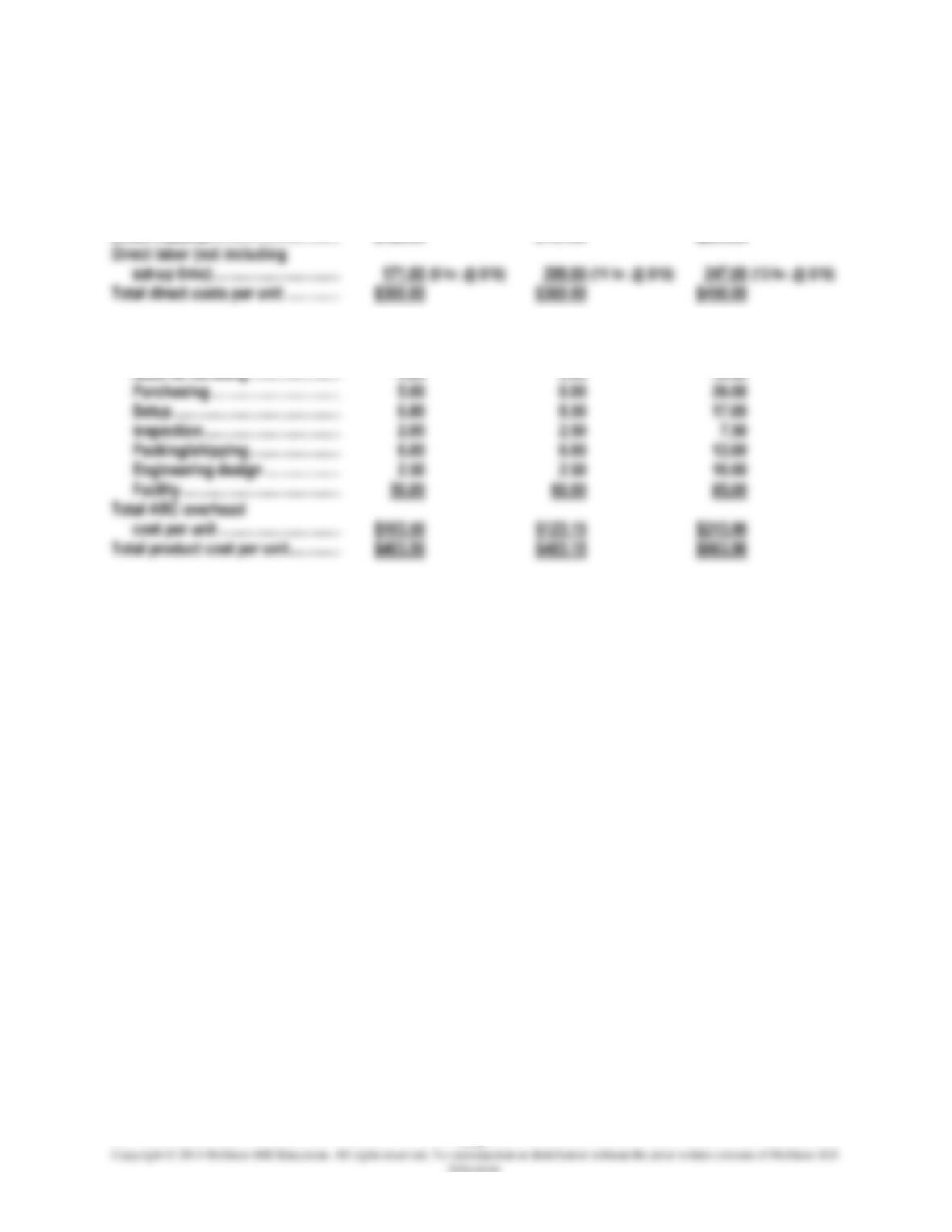

3. Calculation of new product costs under ABC.

REG

ADV

GMT

Direct material .................................

$129.00

$151.00

$203.00

Manufacturing overhead (based on ABC):

Machine-related .........................

$ 27.00

$ 32.40

$ 45.90

Chapter 05 - Activity-Based Costing and Management

5-28

PROBLEM 5-46 (CONTINUED)

4. Comparison of costs and target prices under two alternative product-costing

systems:

REG

ADV

GMT

Reported unit overhead cost:

Traditional, volume-based costing system ............

$108.00

$132.00

$156.00

5. The REG and ADV products were overcosted by the traditional system, and the GMT

product was undercosted by the traditional system

5-29

PROBLEM 5-47 (25 MINUTES)

The information supplied by the ABC project team is in columns A, B, C, D, F, G, and I.

Activity

Activity

Cost

Pool

Cost

Driver

Cost

Driver

Quantity

Pool

Rate

Product

Line

Cost

Driver

Quantity

for

Product

Line

Activity

Cost for

Product

Line

Product

Line

Production

Volume

Activity

Cost

per Unit

of

Product

The results of the ABC calculations are in columns E, H and J. The ABC calculations are as

follows:

(1) Compute pool rate for material-handling activity:

(2) Compute total activity cost for each product line:

Product

Line

Pool Rate

x

Cost Driver

Quantity for

Product Line

=

Activity Cost for

Each Product Line

(3) Compute product cost per unit for each product line:

Product

Line

Activity Cost

for Each

Product

Line

÷

Product Line

Production Volume

Activity Cost

per Unit

= of Product

5-30

PROBLEM 5-48 (30 MINUTES)

1. Deluxe manufacturing overhead cost:

$3,600,000 ÷ 30,000 units = $120 per unit

Deluxe

Executive

2. Activity-based application rates:

Activity

Cost

Activity

Driver

Application

Rate

5-31

PROBLEM 5-48 (CONTINUED)

Manufacturing setup, machine processing, and product shipping costs of a Deluxe

unit and an Executive unit:

Activity

Deluxe

Executive

Manufacturing setups:

Machine processing:

Product shipping:

The manufactured cost of a Deluxe cabinet is $253.50, and the manufactured cost of

an Executive cabinet is $194.80. The calculations follow:

Deluxe

Executive

Direct material…………………………………

$ 40.00

$ 65.00

3. The Deluxe storage cabinet is undercosted. The use of machine hours produced a

Chapter 05 - Activity-Based Costing and Management

5-32

PROBLEM 5-48 (CONTINUED)

4. Cost distortion:

Deluxe Executive

5. No, the discount is not advisable. The regular selling price of $270, when compared

against the more accurate ABC cost figure, shows that each sale provides a profit to

Chapter 05 - Activity-Based Costing and Management

5-33

PROBLEM 5-49 (25 MINUTES)

1.

a.

Manufacturing overhead costs include all indirect manufacturing costs (all

production costs except direct material and direct labor). Typical overhead costs

include:

b.

Companies develop overhead rates before production to facilitate the costing of

2.

The increase in the overhead rate should not have a negative impact on the

3.

Rather than using a plantwide overhead rate, Digital Light could implement

separate activity cost pools. Examples are as follows:

4.

An activity-based costing system might benefit Digital Light because it assigns

Chapter 05 - Activity-Based Costing and Management

5-34

PROBLEM 5-50 (30 MINUTES)

1. Predetermined overhead rate = budgeted overhead ÷ budgeted direct-labor hours

Medform

Procel

Direct material .................................

$ 30.00

$ 45.00

Direct labor:

2. Activity-based overhead application rates:

Activity

Cost

Activity Cost

Driver

Application

Rate

Order

$120,000

÷

600 orders

=

$200 per OP

Chapter 05 - Activity-Based Costing and Management

5-35

PROBLEM 5-50 (CONTINUED)

Order processing, machine processing, and product inspection costs of a Medform

unit and an Procel unit:

Activity

Medform

Procel

Order processing:

The manufactured cost of a Medform unit is $204.60, and the manufactured cost of a

Procel unit is $228.52:

Medform

Procel

Direct material……………………………….

$ 30.00

$ 45.00

Direct labor:

5-36

PROBLEM 5-50 (CONTINUED)

3. a. The Procel product is overcosted by $18.48 ($247.00 - $228.52) under the

traditional product-costing system. The labor-hour application base resulted

b. Yes, especially since Meditech’s selling prices are based heavily on cost. An

overcosted product will result in an inflated selling price, which could prove

Chapter 05 - Activity-Based Costing and Management

5-37

PROBLEM 5-51 (30 MINUTES)

1.

Valdosta Vinyl Company (VVC) is currently using a plantwide overhead rate that is

applied on the basis of direct-labor dollars. In general, a plantwide manufacturing-

overhead rate is acceptable only if a similar relationship between overhead and direct

labor exists in all departments or the company manufactures products that receive the

same proportional services from each department

2.

Because the company uses a plantwide overhead rate applied on the basis of direct-

labor dollars, the elimination of direct labor in the Molding Department through the

Chapter 05 - Activity-Based Costing and Management

5-38

PROBLEM 5-51 (CONTINUED)

3.

a.

In order to improve the allocation of overhead costs in the Cutting and Finishing

departments, management should move toward an activity-based costing system.

The firm should:

b.

In order to accommodate the automation of the Molding Department in its

overhead accounting system, the company should:

Chapter 05 - Activity-Based Costing and Management

5-39

PROBLEM 5-52 (40 MINUTES)

1.

Overhead to be assigned to chemical order:

Activity Cost

Pool

Pool

Rate

Level of

Cost Driver

Assigned

Overhead

Cost

Machine setups

$4,000 per setup

6 setups

$24,000

4.

Overhead to be assigned to chemical order, given a single predetermined overhead

rate:

5.

These chemicals entail a relatively large number of machine setups, a large amount of

hazardous materials, and several inspections. Thus, they are quite costly in terms of

Chapter 05 - Activity-Based Costing and Management

5-40

PROBLEM 5-52 (CONTINUED)

PROBLEM 5-53 (20 MINUTES)

1. Calculation of unit cost:

(a)

Overhead assigned to containers:

Activity Cost

Pool

Pool

Rate

Level of

Cost Driver

Assigned

Overhead

Cost

Machine setups

$4,000 per setup

4 setups

$16,000

(b)

Unit cost per container:

Direct material................................

$210