CHAPTER 5

Merchandising Operations

and the Multiple-Step Income Statement

Learning Objectives

1. Describe merchandising operations and inventory systems.

2. Record purchases under a perpetual inventory system.

3. Record sales under a perpetual inventory system.

4. Prepare a multiple-step income statement and a comprehensive income statement.

5. Determine cost of goods sold under a periodic inventory system.

6. Compute and analyze gross profit rate and profit margin.

*7. Record purchases and sales of inventory under a periodic inventory system.

Summary of Questions by Learning Objectives and Bloom’s Taxonomy

Item

LO

BT

Item

LO

BT

Item

LO

BT

Item

LO

BT

Item

LO

BT

Questions

1.

1

C

7.

3

K

12.

4

AP

17.

4

K

22.

6

K

2.

1

C

8.

3

AP

13.

3

C

18.

2

K

23.

6

C

3.

1

C

9.

3

C

14.

4

C

19.

2

K

24.

6

AN

4.

1

C

10.

3

C

15.

4

K

20.

5

K

25.

6

C

5.

1

AP

11.

2

AP

16.

1

K

21.

5

K

26.

7*

AP

6.

3

C

Brief Exercises

1.

1, 4

AP

4.

2

AP

7.

4

AP

10.

5

AP

13.

6

C

2.

2, 3

AP

5.

4

AP

8.

5

AP

11.

6

AP

14.

7

AP

3.

3

AP

6.

4

AP

9.

5

AP

12.

6

AP

Do It! Exercises

1.

1

C

3.

3

AP

4.

5

AP

6.

6

AN

2.

2

AP

4.

4

AP

5.

5

AP

Exercises

1.

2

AP

4.

2, 3

AP

7.

4, 6

AP

10.

4

AP

13.

5

AP

2.

2, 3

AP

5.

4

AP

8.

4, 6

AP

11.

4

AP

14.

6

C

3.

3

AP

6.

4, 6

AP

9.

4, 6

AP

12.

5

AP

15.

7

AP

Problems: Set A

1.

2, 3,

4, 6

AP

3.

2, 3,

4

AP

5.

4

AP

7.

4, 5

AP

9.

5, 7*

AP

2.

2, 3

AP

4.

4, 6

AP

6.

4

AP

8.

4, 5,

6

AN

*Continuing Cookie Solutions for this chapter are available online.

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Journalize, post, prepare partial income statement, and

calculate ratios.

Simple

30–40

2A

Journalize purchase and sale transactions under a

perpetual system.

Moderate

20–30

3A

Journalize, post, and prepare trial balance and partial

income statement.

Simple

30–40

4A

Prepare financial statements and calculate profitability

ratios.

Moderate

40–50

5A

Prepare a correct multiple-step income statement.

Complex

20–30

6A

Journalize, post, and prepare adjusted trial balance and

financial statements.

Moderate

40–50

7A

Determine cost of goods sold and gross profit under a

periodic system.

Moderate

40–50

8A

Calculate missing amounts and assess profitability.

Moderate

20–30

*9A

Journalize, post, and prepare trial balance and partial

income statement under a periodic system.

Simple

30–40

ANSWERS TO QUESTIONS

1. (a) Disagree. The steps in the accounting cycle are the same for both a merchandising company

and a service company.

(b) The measurement of income is conceptually the same. In both types of companies, net

income (or loss) results from the matching of expenses with revenues.

LO 1 BT: C Diff: M TOT: 2 min. AACSB: None AICPA FC: Reporting

2. The components of revenues and expenses differ as follows:

Merchandising

Service

Revenues

Expenses

Sales revenue

Cost of Goods Sold and Operating

Fees, Rents, etc.

Operating (only)

LO 1 BT: C Diff: E TOT: 1 min. AACSB: None AICPA FC: Reporting

3. Under a periodic inventory system the company does not keep track of how many units are on

hand. Instead it takes a physical count at the end of the period to determine ending inventory and

cost of goods sold. Under a perpetual system the company adjusts its inventory account each time

it purchases or sells inventory. Thus it always has a record of its available inventory. Having

knowledge of inventory balances helps a company avoid lost sales due to “stock–outs” as well as

carrying too much inventory on hand (which results in additional storage and handling costs). The

purchasing department can make better decisions with the aid of perpetual inventory records.

LO 1 BT: C Diff: M TOT: 4 min. AACSB: None AICPA FC: Reporting

4. (a) The income measurement process is as follows:

Sales

Revenue

Less

Cost of

Goods

Sold

Equals

Gross

Profit

Less

Operating

Expenses

Equals

Net

Income

(Loss)

(b) Income measurement in a merchandising company differs from a service company as

follows: (a) sales are the primary source of revenue and (b) expenses are divided into two

main categories: cost of goods sold and operating expenses.

LO 1 BT: C Diff: M TOT: 4 min. AACSB: None AICPA FC: Reporting

5. Sales revenue …………………………………………………………………………………………….. $100,000

Cost of goods sold……………………………………………………………………………………….. 70,000

Gross profit …………………………………………………………………………………………………. $ 30,000

LO 1 BT: AP Diff: E TOT: 2 min. AACSB: Analytic AICPA FC: Reporting

6. Agree. In accordance with the revenue recognition principle, sales revenues are generally con–

sidered to be recognized when the goods are transferred from the seller to the buyer; that is,

when the performance obligation is satisfied. The recognition of revenue is not dependent on the

collection of credit sales.

LO 3 BT: K Diff: E TOT: 2 min. AACSB: None AICPA FC: Measurement & Reporting

7. (a) The primary source documents are (1) cash sales—cash register tapes and (2) credit sales—

sales invoice.

(b) The entries are:

Debit

Credit

Cash sales—

Cash ……………………………………………………………

Sales Revenue ………………………………………

Cost of Goods Sold ……………………………………….

Inventory ……………………………………………….

XX

XX

XX

XX

Credit sales—

Accounts Receivable ……………………………………..

Sales Revenue ………………………………………

Cost of Goods Sold ……………………………………….

Inventory ……………………………………………….

XX

XX

XX

XX

LO 3 BT: AP Diff: M TOT: 3 min. AACSB: Analytic AICPA FC: Reporting

8. July 19 Cash ($800 – $8) …………………………………………………………………. 792

Sales Discounts ($800 X 1%) ………………………………………………… 8

Accounts Receivable ($900 – $100) ………………………………… 800

LO 3 BT: AP Diff: M TOT: 3 min. AACSB: Analytic AICPA FC: Reporting

9. Shipping unwanted goods to customers is generally considered unethical behavior. In addition, if

proper accounting is applied, in most cases it won’t achieve the desired result of increasing sales. If

it is expected that the unwanted goods will be shipped back to the seller, then they should not be

treated as sales in the first place. (Note: The practice of shipping more goods than were ordered in

order to meet sales goals and get rid of extra inventory is referred to as channel stuffing.)

LO 3 BT: E Diff: H TOT: 5 min. AACSB: Analytic & Reflective Thinking AICPA BB: Critical Thinking

10. In most industries returns are not significant, and they are therefore accounted for as they occur.

When returns are expected to be significant, the company should make an adjusting entry at the

end of the period to estimate the amount of returns that will result from the period’s sales, so that

revenues will not be overstated during the period.

LO 3 BT: C Diff: M TOT: 3 min. AACSB: Analytic AICPA FC: Reporting

11. July 24 Accounts Payable ($1,900 – $300) …………………………………………. 1,600

Cash ($1,600 – $32) …………………………..…………………………. 1,568

Inventory ($1,600 X 2%) ………………………………………………… 32

LO 2 BT: AP Diff: M TOT: 2 min. AACSB: Analytic AICPA FC: Reporting

12. Gross profit ………………………………………………………………………………………… $560,000

Less: Net income ……………………………………………………………………………….. 230,000

Operating expenses …………………………………………………………………………….. $330,000

LO 4 BT: AP Diff: E TOT: 2 min. AACSB: Analytic AICPA FC: Reporting

13. Its current terms of 1/10, n/30 means that customers get a 1% discount if they pay within 10 days,

otherwise they have to pay the full amount within 30 days. If they switch to 2/10, n/45 customers

would get a 2% discount for paying within 10 days, otherwise they have to pay the full amount in

45 days. By offering 2%, more of Mai’s customers would likely pay within the 10 day period.

Management would have to determine whether it is worth the additional cost to be paid quicker.

Also, by extending the full payment period from 30 to 45 days, Mai would end up receiving its

money even later from its slow payers.

LO 2 & 3 BT: E Diff: H TOT: 5 min. AACSB: Analytic & Reflective Thinking AICPA BB: Critical

Thinking

14. The gain on the sale of the plant represents a one–time gain. That is, it won’t be recurring next

year. If you eliminate the effect of this one-time gain, then the company’s income actually declined

by $5 million relative to the prior year. When predicting future earnings investors frequently place

little weight on non-recurring events such as this.

LO 4 BT: AN Diff: H TOT: 4 min. AACSB: Analytic & Reflective Thinking AICPA BB: Critical Thinking

15. There are three distinguishing features in the income statement of a merchandising company:

(1) a sales revenues section, (2) a cost of goods sold section, and (3) gross profit.

LO 4 BT: K Diff: E TOT: 1 min. AACSB: None AICPA FC: Reporting

16. The normal operating cycle for a merchandising company is likely to be longer than for a service

company because inventory must first be purchased and sold, and then the receivables must be

collected.

LO 1 BT: C Diff: E TOT: 2 min. AACSB: None AICPA FC: Reporting

17. Apple uses the term gross margin. Total gross margin increased by $6,233 million.

LO 4 BT: AP Diff: M TOT: 3 min. AACSB: Analytic AICPA FC: Reporting

18. Of the merchandising accounts, only Inventory will appear in the post-closing trial balance.

LO 4 BT: E Diff: M TOT: 3 min. AACSB: Analytic AICPA FC: Reporting

19. Businesses most likely to use a perpetual inventory system would include automobile dealerships,

equipment supply companies, and other companies selling products having a high unit-value.

With automation, perpetual systems are becoming increasingly cost-effective.

LO 1 BT: C Diff: E TOT: 2 min. AACSB: None AICPA FC: Reporting

20. (a) (b)

Accounts Added/Deducted Normal Balance

Purchase Returns and Allowances Deducted Credit

Purchase Discounts Deducted Credit

Freight-In Added Debit

LO 5 BT: K Diff: E TOT: 2 min. AACSB: None AICPA FC: Reporting

21. (a) X = Purchase returns and allowances and

Y = Purchase discounts, or vice versa.

(b) X = Freight-in.

(c) X = Cost of goods purchased.

(d) X = Ending inventory.

LO 5 BT: C Diff: E TOT: 1 min. AACSB: None AICPA FC: Reporting

22. Profitability is affected by gross profit, as measured by the gross profit rate, and by manage-

ment’s ability to control operating expenses, as measured by the profit margin.

LO 6 BT: K Diff: E TOT: 1 min. AACSB: None AICPA FC: Reporting

23. Factors affecting a company’s gross profit rate include selling products with a higher (or lower)

“markup,” increased competition that results in lower selling prices, and price increases or

decreases from suppliers.

LO 6 BT: C Diff: M TOT: 2 min. AACSB: None AICPA FC: Reporting

24. Gross profit represents the amount by which sales exceeds cost of goods sold. In order for the

company to be profitable, gross profit must exceed the company’s operating expenses. Before

the selling price is cut, the company should do a careful analysis estimating what its gross profit

and operating expenses would be if more units were sold at a lower selling price. In addition, a

big concern is what the likely reaction of competitors will be. If competitors also cut their price,

then volume will not increase, and the company’s net income will be lower.

LO 6 BT: AN Diff: M TOT: 4 min. AACSB: Analytic AICPA BB: Critical Thinking

25. Mark Coney should calculate the company’s quality of earnings ratio. This is calculated by

dividing net cash provided by operating activities by net income. A measure significantly below 1

would suggest that the company might be using aggressive accounting techniques to recognize

income early.

LO 6 BT: AN Diff: M TOT: 3 min. AACSB: Analytic AICPA PC: Problem Solving

*26. July 24 Accounts Payable ($1,900 – $400) ……………………………. 1,500

Cash ($1,500 – $30) ………………………………………… 1,470

Purchase Discounts ($1,500 X 2%) …………………… 30

LO 7 BT: AP Diff: M TOT: 2 min. AACSB: Analytic AICPA FC: Reporting

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 5-1

(a) Sales = $181,500 ($71,900 + $109,600).

BRIEF EXERCISE 5-2

Rita Company

Inventory ………………………………………………………. 900

BRIEF EXERCISE 5-3

(a) March 2 Accounts Receivable …………………… 800,000

Sales Revenue ……………………. 800,000

2 Cost of Goods Sold …………………….. 540,000

BRIEF EXERCISE 5-3 (Continued)

(c) 12 Cash ($660,000 – $13,200) ……………. 646,800

BRIEF EXERCISE 5-4

(a) March 2 Inventory …………………………………….. 800,000

Accounts Payable ……………….. 800,000

BRIEF EXERCISE 5-5

BARTO COMPANY

Income Statement (Partial)

For the Month Ended October 31, 2017

Sales

Sales revenue ($300,000 + $150,000) …………………. $450,000

BRIEF EXERCISE 5-6

As the name suggests, numerous steps are required in determining net

income in a multiple-step statement.

Item

Section

Sales returns and allowances

Sales revenues

Gain on disposal of plant assets

Other revenues and gains

BRIEF EXERCISE 5-7

(a) Service revenue ……………………………………………. $ 62,500

Less:

Salaries and wages expense …………………………. $28,000

(b)

KAREN WEIGEL INC.

Comprehensive Income Statement

For the Year Ended December 31, 2017

Net income ………………………………………………………… $ 19,200

BRIEF EXERCISE 5-8

Beginning inventory ………………………………………….. $ 67,000

BRIEF EXERCISE 5-9

Purchases …………………………………………………………. $404,000

Less: Purchase returns and allowances……………. $13,000

BRIEF EXERCISE 5-10

Net sales …………………………..………………………………. $612,000

Beginning inventory ………………………………………….. $ 60,000

BRIEF EXERCISE 5-11

(a) Profit margin = $32,500 ÷ $250,000 = 13.0%

The profit margin measures the extent by which selling price covers all

(b) Gross profit rate = ($250,000 – $150,000) ÷ $250,000 = 40.0%

BRIEF EXERCISE 5-12

(a) Profit margin = $68,000 ÷ $800,000 = 8.5%

(b) Gross profit rate = ($800,000 – $520,000) ÷ $800,000 = 35.0%

BRIEF EXERCISE 5-13

The quality of earnings ratio is calculated by dividing net cash provided

by operating activities by net income. For Cabo Corporation this would

*BRIEF EXERCISE 5-14

(a) March 2 Purchases …………………………………… 800,000

Accounts Payable ……………….. 800,000

SOLUTIONS TO DO IT! EXERCISES

DO IT! 5-1

1. True

DO IT! 5-2

Oct. 5 Inventory …………………………………………………………… 5,000

Accounts Payable ………………………………………. 5,000

DO IT! 5-3

Oct. 5 Accounts Receivable …………………………………………. 5,000

Sales Revenue …………………………………………… 5,000

Oct. 8 Sales Returns and Allowances …………………………... 640

Accounts Receivable …………………………………. 640

DO IT! 5-4

BERLIN CORP.

Income Statement

For the Year Ended December 31, 2017

Sales

Sales revenue ……………………………………….. $592,000

Less: Sales returns and allowances ………. 40,000

Net sales ……………………………………………………. $552,000

Cost of goods sold ……………………………………… 156,000

BERLIN CORP.

Comprehensive Income Statement

For the Year Ended December 31, 2017

Net income ………………………………………………………. $146,580

DO IT! 5-5

(a) Cost of goods purchased $161,400:

Purchases – Purchase returns and allowances – Purchase

(b) Cost of goods sold $165,170:

DO IT! 5-6

2017

2016

Gross profit rate

($150,000–$90,000) = 40%

($120,000–$72,000) = 40%

Profit margin

$10,000 ÷ $150,000 = 6.7%

$22,000 ÷ $120,000 = 18.3%

SOLUTIONS TO EXERCISES

EXERCISE 5-1

(3) April 7 Equipment …………………………………. 30,000

Accounts Payable ………………. 30,000

(5) April 15 Accounts Payable

($28,000 – $3,600) ……………………. 24,400

(b) May 4 Accounts Payable ($28,000 – $3,600) …. 24,400

EXERCISE 5-2

Sept. 6 Inventory ……………………………………………….. 1,650

Accounts Payable ……………………………. 1,650

EXERCISE 5-2 (Continued)

Sept. 14 Sales Returns and Allowances …………………. 45

Accounts Receivable ………………………… 45

EXERCISE 5-3

(a) (1) Dec. 3 Accounts Receivable……………….. 500,000

(3) Dec. 13 Cash ($475,000 – $4,750)………….. 470,250

Sales Discounts

(b) Jan. 2 Cash ……………………………………………… 475,000

EXERCISE 5-4

(a) June 10 Inventory …………………………………………… 9,000

Accounts Payable ………………………. 9,000

(b) June 10 Accounts Receivable ……………………………… 9,000

Sales Revenue ………………………………… 9,000

Cost of Goods Sold ……………………………….. 5,000

Inventory ………………………………………… 5,000

EXERCISE 5-5

DOQE COMPANY

Income Statement (Partial)

For the Year Ended October 31, 2017

Sales

Sales revenue ……………………………………………… $900,000

EXERCISE 5-6

(a) LIEU CO.

Income Statement

For the Month Ended January 31, 2017

Sales

Sales revenue ………………………………………. $370,000

Less: Sales returns and allowances …….. $20,000

Sales discounts …………………………. 8,000 28,000

EXERCISE 5-6 (Continued)

(b) LIEU CO.

Comprehensive Income Statement

For the Month Ended January 31, 2017

Net income ………………………………………………………………………………. $14,000

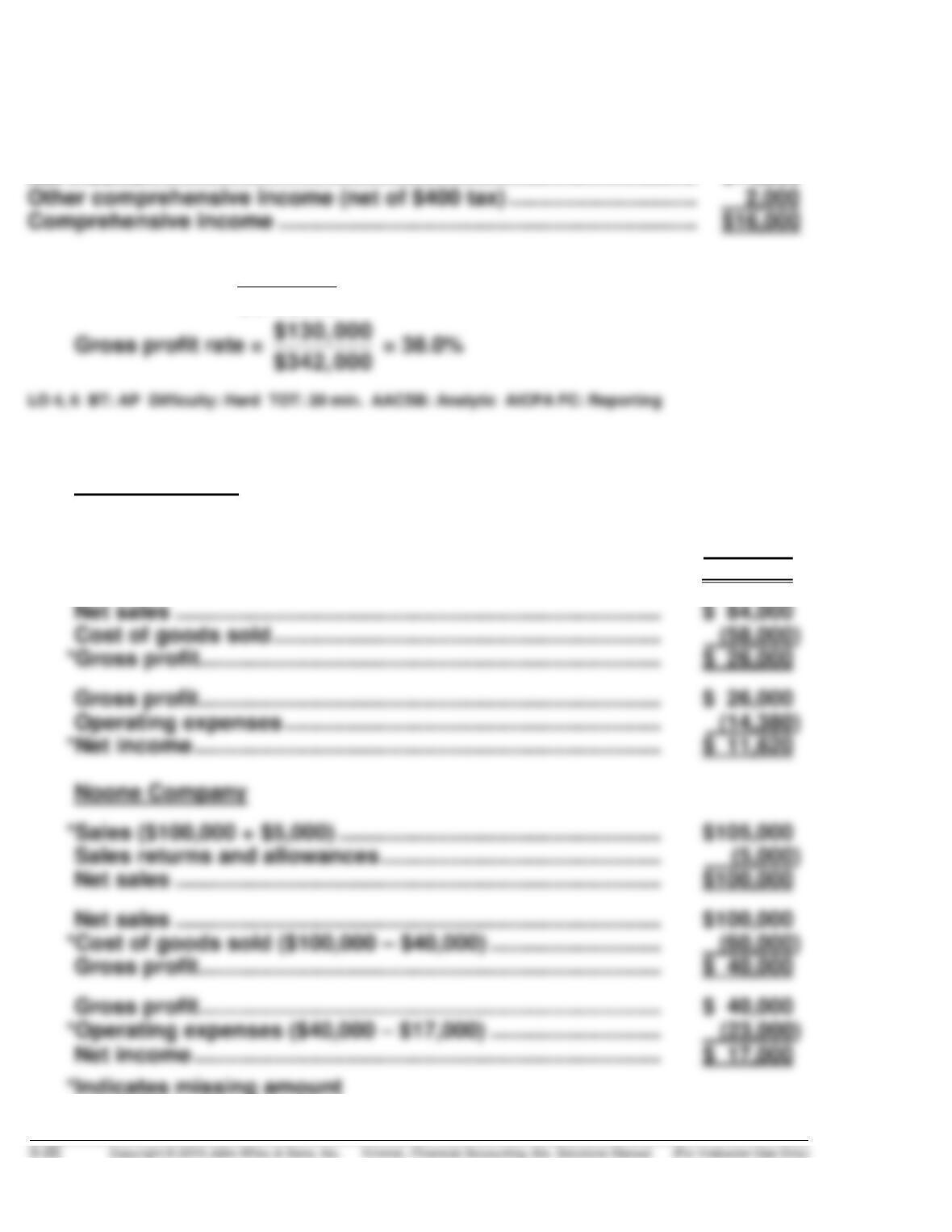

(c) Profit margin =

$14,000

$342,000

= 4.1%

EXERCISE 5-7

(a) Yoste Company

Sales …………………………………………………………………………… $ 90,000)

*Sales returns and allowances ($90,000 – $84,000) ………… (6,000)

Net sales …………………………………………………………………….. $ 84,000)