AMAT has operating leases, warranty and other guarantees, but these

amounts do not add an unusual amount of risk to the debt structure.

Despite the decreasing profits and CFO, AMAT generates enough funds to

cover all necessary items. As long as the trend in profits and CFO can be

reversed, the firm should not have a long-term solvency problem.

Profitability

AMAT’s sales decreased 14% from 2012 to 2013, and 17% from 2011 to

2012. AMAT has four distinct segments: Silicon Systems Group, Applied

Global Services, Display and Energy and Environmental Solutions. The only

segment with increasing sales in 2013 was the Display segment which

Gross profit margin decreased in 2012, but recovered somewhat in 2013.

Despite lower sales in 2013, gross profit margin increased due to lower

costs, lower inventory charges and a favorable product mix. The decrease in

gross profit margin in 2012 was a result of lower sales (AMAT has fixed

costs), higher inventory charges and costs associated with the Varian

acquisition.

Selling, general and administrative (SG&A) expenses increased in dollars in

2012 and then returned to dollar levels comparable to 2011 in 2013;

however in percentage terms the change in percentage in 2013 was minimal

due to the large decrease in sales without a proportional decrease in

expenses. The increased costs in 2012 were a result of the Varian

acquisition. In 2013, those costs did not occur again and the firm was able to

reduce costs through their restructuring programs along with a reduction in

bad debt expense as a result of lower risk exposure in display and solar

customers.

AMAT’s effective tax rate has been volatile. The non-deductibility of the

goodwill impairment charges in 2012 caused the rate to be 65.5%. The

effective tax rate for the firm, with no goodwill impairment charges, was

19% in 2011. AMAT benefits from lower tax rates to a great extent and

realized a much lower tax rate as a result of global business in 2013. This

was offset, however, by more non-deductible goodwill impairment charges

resulting in an effective tax rate of 26.9% instead of a rate of 4.4% had

impairment charges not been taken.

Market Measures

Earnings per share has dropped significantly from 2011, although it

improved slightly in 2013. The PE ratio indicates that investors are not

alarmed by the past two years of lower profits and lower CFO. The PE ratio

increased from 8.64 in 2011 to 118.33, with the stock price dropping by

Strengths

Acquisition strategy

Good short-term liquidity

Weaknesses

Increasing average collection period

Increasing inventories

Investment Potential

AMAT has recognized challenges it faces in a very competitive industry and

has made changes to mitigate losses in the deteriorating solar industry while

Creditworthiness

AMAT has an average amount of debt and the ability to repay debt as it

comes dues. The firm has good short-term and long-term solvency with a

healthy cash balance and short-term investments. The firm is a good credit

risk.

(c)

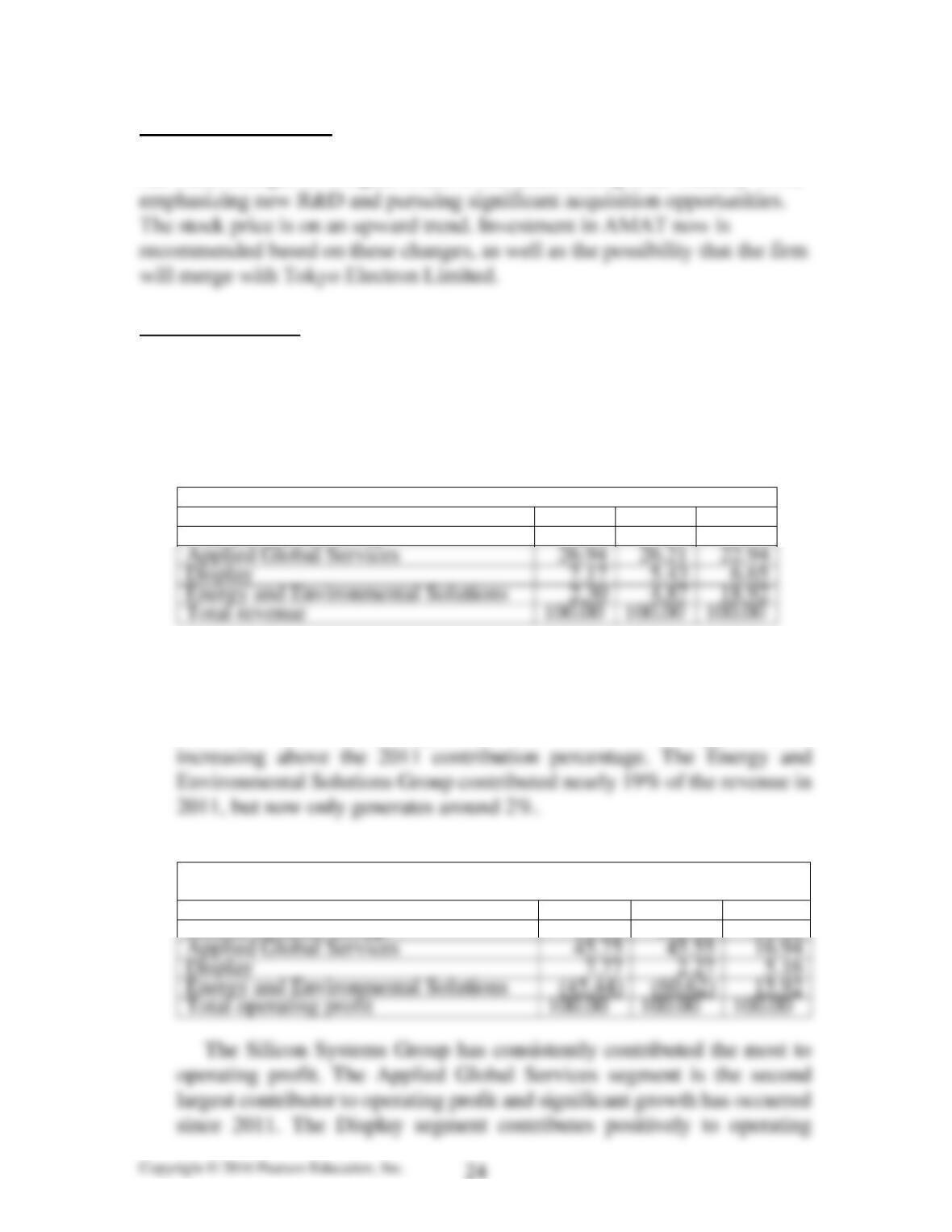

Table 5A.1 Contribution by Segment to Revenue (Percentages)

2013

2012

2011

Silicon Systems Group

63.59

63.49

51.49

Applied Global Services

26.94

26.21

22.94

Display

7.17

5.43

6.65

Energy and Environmental Solutions

2.30

4.87

18.92

Total revenue

100.00

100.00

100.00

The Silicon Systems Group and the Applied Global Services segments

are the largest revenue producers. Both segments have experienced

increased sales from 2011 to 2013. The Display segment produces less

than 10% of revenue each year and in 2012 revenues dropped before

Table 5A.2 Contribution by Segment to Operating Profit

(Percentages)

2013

2012

2011

Silicon Systems Group

91.92

112.80

61.98

Applied Global Services

45.75

45.55

16.94

Display

Energy and Environmental Solutions

15.92

Total operating profit

100.00

100.00

100.00

profit, but the contribution declined in 2012 before recovering in 2013.

The Energy and Environmental Solutions segment has generated

operating losses in 2012 and 2013.

Table 5A.3 Operating Profit Margin by Segment (Percentages)

2013

2012

2011

Silicon Systems Group

18.35

22.45

32.58

Applied Global Services

21.55

21.97

19.98

Display

13.76

5.29

21.03

Energy and Environmental Solutions

(250.29)

(157.18)

22.76

The operating profit margin of the Silicon Systems Group is declining

every year. Applied Global Services is the only segment that has produced

Table 5A.4 Capital Expenditures by Segment (Percentages)

2013

2012

2011

Silicon Systems Group

89.39

82.56

52.21

Display

27.43

Energy and Environmental Solutions

14.16

Total capital expenditures

100.00

100.00

100.00

AMAT has chosen to invest the most in the Silicon Systems Group,

while cutting expenditures significantly in the Display and Energy and

Environmental Solutions segments. This is not surprising given the poor

performance in the Energy and environmental Solutions segment.

Investments in the Applied Global Services segment increased in 2012,

but declined the following year. Despite the lower investment this

segment has performed well for AMAT.

Table 5A.5 Return on Investment by Segment (Percentages)

2013

2012

2011

Silicon Systems Group

15.86

24.34

86.64

Applied Global Services

22.27

24.67

36.05

Display

25.26

32.03

has produced negative returns all years except 2011. Continued

investment in this segment may not be warranted.

Table 5A.6 Ranking of Segments in 2013

Percentag

e of Total

Segment

Assets

Percent

Contributio

n to

Operating

Profit

Operatin

g Profit

Margin

Return on

Investmen

t

Silicon

Systems

Group

69.42

91.92

18.35

15.86

Applied

Global

Services

24.60

45.75

21.55

22.27

Display

13.76

25.26

The Silicon Systems Group is Applied’s largest segment in terms of

investment and contribution to operating profits, but does not deliver the

highest operating profit margin or ROI. The Applied Global Services

segment delivers the highest operating profit margin and solid ROI with

Case 5.3

(a)

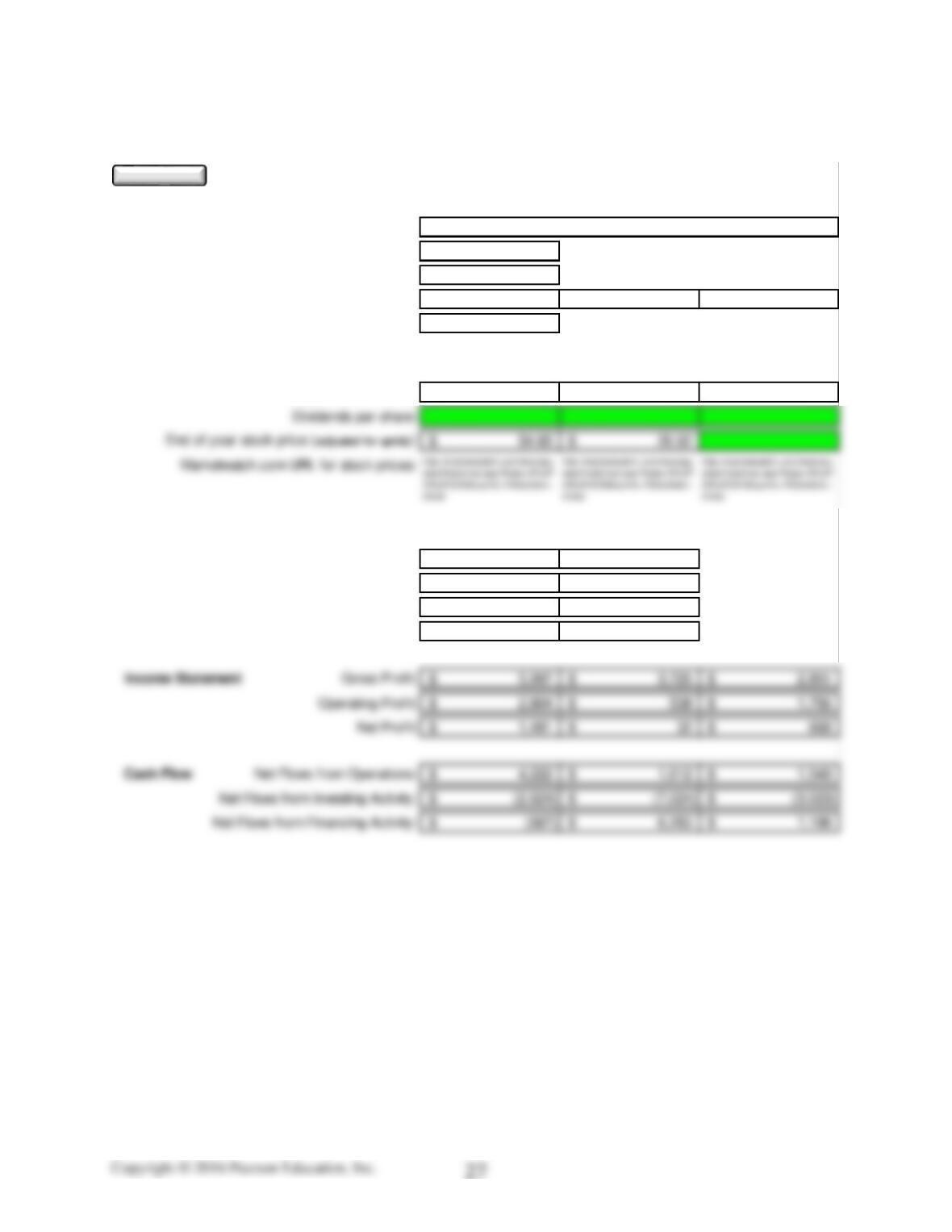

Company Name:

Stock Ticker Symbol: FB

U.S. Stock Exchange: NASDAQ Fixed

1 /31/ 000

Statement Year-end Dates: 12/31/2013 12/31/2012 12/31/2011

Financial Reports Rounded to : Millions

Supplemental Ratio Requirements: 2013 2012 2011

Rent expense (in millions): 130$ 196$ 219$

Check Figures:

Balance Sheet Current Assets: 13,070$ 11,267$

Total Assets: 17,895$ 15,103$

Current Liabilities: 1,100$ 1,052$

Total Stockholders’ Equity: 15,470$ 11,755$

Facebook, Inc.

The ‘Analysis ToolPak‘ add–in must be installed and active.

Enter data on this sheet before other financial statement information.

Clear

2013 2012

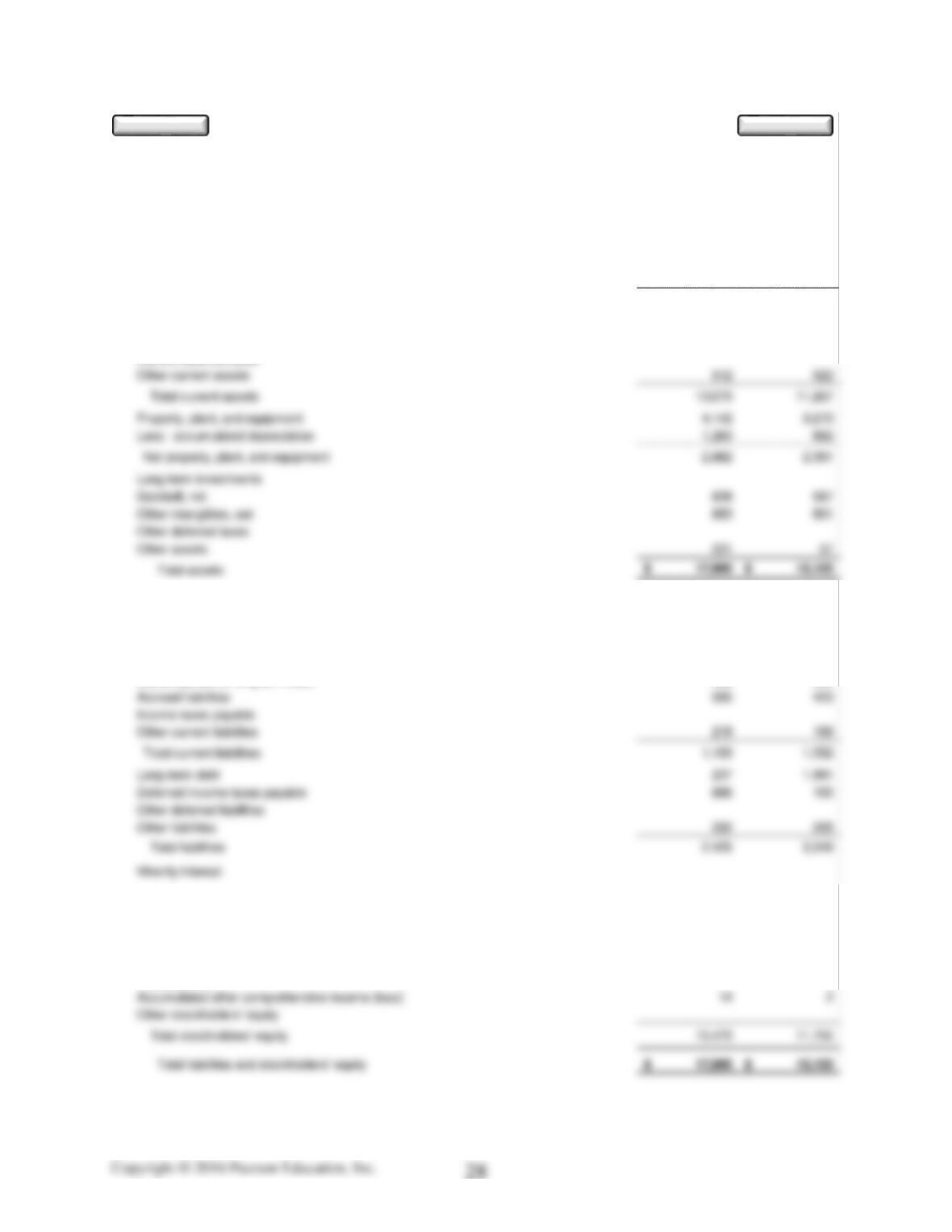

ASSETS

Current Assets:

Cash and cash equivalents 3,323$ 2,384$

Short-term investments 8,126 7,242

Total cash and short-term investments 11,449 9,626

Accounts receivable, net 1,109 719

Inventories, net

Current deferred taxes

LIABILITIES

Current Liabilities:

Accounts payable 87$ 65$

Short-term debt

Current portion of long-term debt 239 365

STOCKHOLDERS’ EQUITY

Preferred stock

Common stock, par value plus additional paid-in capital 12,297 10,094

Retained earnings (accumulated deficit) 3,159 1,659

Treasury stock

Facebook, Inc. (FB / NASDAQ)

Annual Consolidated Balance Sheet

Amou n ts Rou nd ed to : M illion s

Results as of December 31

Clear

Edit

2013 2012

ASSETS

Current Assets:

Cash and cash equivalents 18.6% 15.8%

Short-term investments 45.4% 48.0%

Total cash and short-term investments 64.0% 63.7%

Accounts receivable, net 6.2% 4.8%

Inventories, net 0.0% 0.0%

LIABILITIES

Current Liabilities:

Accounts payable 0.5% 0.4%

Short-term debt 0.0% 0.0%

Current portion of long-term debt 1.3% 2.4%

Accrued liabilities 3.1% 2.8%

STOCKHOLDERS’ EQUITY

Preferred stock 0.0% 0.0%

Common stock, par value plus additional paid-in capital 68.7% 66.8%

Retained earnings (accumulated deficit) 17.7% 11.0%

Treasury stock 0.0% 0.0%

Results as of December 31

S um mary p ercentag es in italics will n ot f oot d ue to rou nding

Annual Common Size Balance Sheet

Facebook, Inc. (FB / NASDAQ)

2013 2012 2011

Net sales 7,872$ 5,089$ 3,711$

Less: Cost of goods sold 1,875 1,364 860

Gross profit 5,997 3,725 2,851

Sales, general and administrative 1,778 1,788 707

Operating profit (loss) 2,804 538 1,756

Other income (expenses), net excluding interest expense 6 7 (19)

Earnings (loss) before interest and taxes 2,810 545 1,737

Interest expense 56 51 42

Results for the Years Ending December 31

Facebook, Inc. (FB / NASDAQ)

Annual Consolidated Income Statement

Amou n ts Rou nd ed to : M illion s ( except p er sh are am oun ts)

Edit

Clear

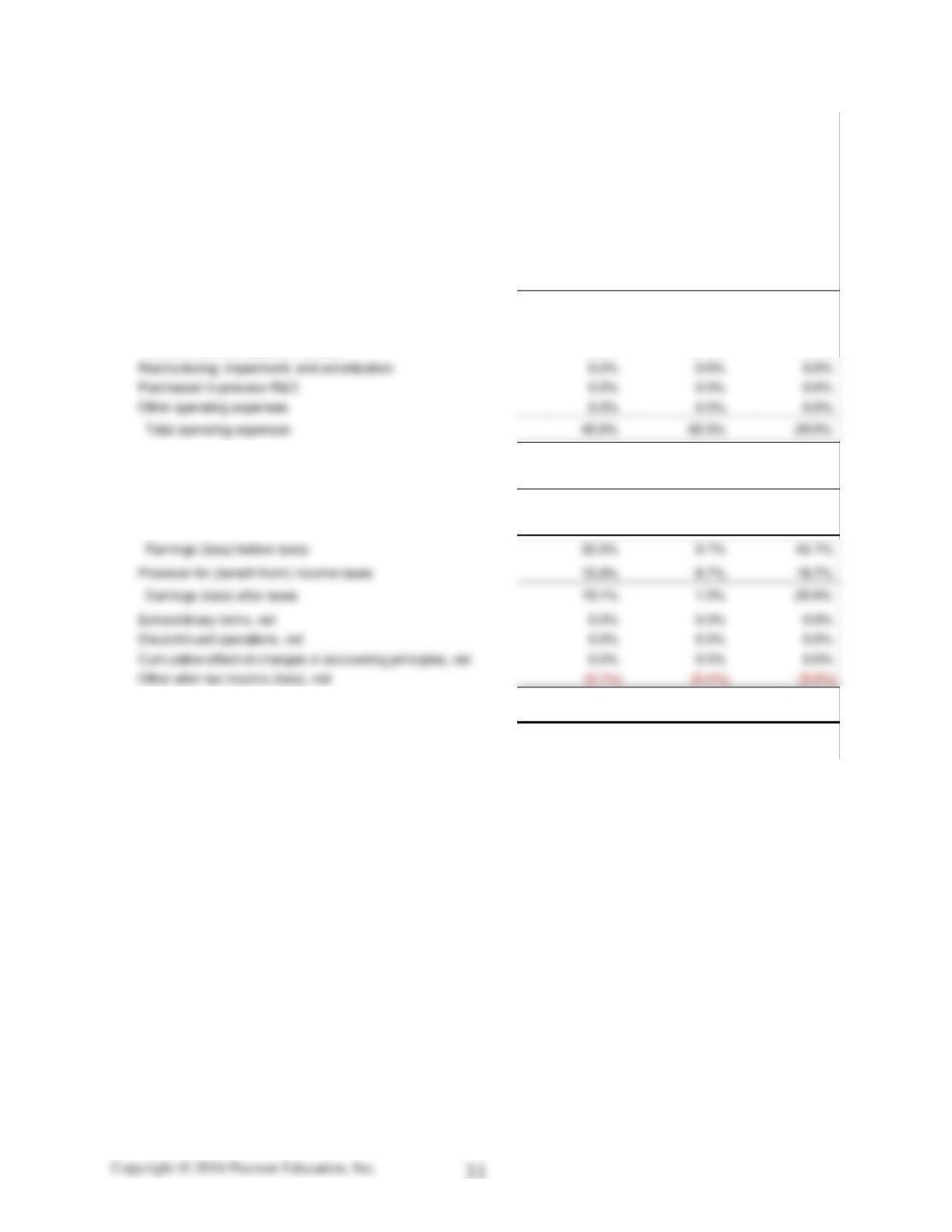

2013 2012 2011

Net sales 100.0% 100.0% 100.0%

Less: Cost of goods sold 23.8% 26.8% 23.2%

Gross profit 76.2% 73.2% 76.8%

Sales, general and administrative 22.6% 35.1% 19.1%

Research and development (R&D) 18.0% 27.5% 10.5%

Operating profit (loss) 35.6% 10.6% 47.3%

Other income (expenses), net excluding interest expense 0.1% 0.1% (0.5%)

Earnings (loss) before interest and taxes 35.7% 10.7% 46.8%

Interest expense 0.7% 1.0% 1.1%

Net profit (loss) 18.9% 0.6% 18.0%

Effective tax rate 45.5% 89.3% 41.0%

Results for the Years Ending December 31

Facebook, Inc. (FB / NASDAQ)

Annual Common Size Income Statement

S um mary p ercentag es in italics will not f oot d ue to roun din g

2013 2012 2011

Cash flows from operating activities:

Income (loss) from continuing operations 1,491$ 32$ 668$

Adjustments to reconcile to net cash provided by operating activities:

Depreciation and amortization 1,011 649 323

Stock-based compensation 906 1,572 217

accrued liabilities, and income taxes payable

(12) 153 43

Increase (decrease) in deferred liabilities 8 (60) 49

Other assets and liabilities, net 845 41 146

Net cash provided by (used in ) operating activities 4,222 1,612 1,549

Cash flows from investing activities:

Purchases of property, plant, and equipment (1,362) (1,235) (606)

Cash flows from financing activities:

Short-term borrowings, net

Proceeds from long-term borrowings 1,496

Payment of long-term borrowings (1,891) (366) (431)

Proceeds from sales of common stock 1,504 6,777 1,026

Repurchase of common stock / treasury stock

Dividends to shareholders

Income taxes (refunded) -339 53 197

Results for the Years Ending December 31

Facebook, Inc. (FB / NASDAQ)

Annual Consolidated Statement of Cash Flows

Amou n ts Rou nd ed to : M illion s

Clear

Edit

Payment of short-term borrowings, net – – –

Payment of long-term borrowings 1,891 16.7 366 2.5 431 10.6

Payment of dividends to shareholders – – –

2013 % 2012 % 2011 %

Inflows $ $ $

Proceeds from operating activities 4,222 34.4 1,612 10.5 1,549 40.6

Sales of property, plant, and equipment – – –

Sales of marketable securities and short-term investments 6,551 53.3 5,433 35.5 629 16.5

Proceeds from sales of common stock 1,504 12.2 6,777 44.2 1,026 26.9

Proceeds from discontinued operations – – –

Gains from effect of exchange rate changes on cash, net 8 0.1 1 – 3 0.1

Divestiture of acquisitions, net of cash acquired – – –

Total Inflows 12,285$ 100.0 15,319$ 100.0 3,813$ 100.0

Outflows $ $ $

Losses from operating activities – – –

Purchases of property, plant, and equipment 1,362 12.0 1,235 8.6 606 14.8

Purchases of marketable securities and short-term investments 7,433 65.5 10,307 71.3 3,025 74.0

Acquisitions, net of cash acquired 368 3.2 911 6.3 24 0.6

Facebook, Inc. (FB / NASDAQ)

Annual Summary Analysis Statement of Cash Flows

S u m m ary p ercen tag es i n italics d o n ot f oot d u e to rou ndin g di f f eren ce s

Results for the Years Ending December 31