PROBLEM 5-6B (Continued)

(c) BUSE’S FASHION CENTER

Adjusted Trial Balance

November 30, 2014

Debit Credit

Cash …………………………………………………….

Accounts Receivable …………………………….

Accumulated Depreciation—

Equipment ………………………………………..

Notes Payable ………………………………………

Accounts Payable …………………………………

Dividends ……………………………………………..

Sales Revenue ………………………………………

Sales Returns and Allowances ………………

Cost of Goods Sold ………………………………

Salaries and Wages Expense ………………..

Advertising Expense …………………………….

$ 37,700

33,700

12,000

6,200

505,400

110,000

26,400

$ 61,000

62,000

17,800

757,200

PROBLEM 5-6B (Continued)

(d) BUSE’S FASHION CENTER

Income Statement

For the Year Ended November 30, 2014

Sales

Cost of goods sold …………………………………… 505,400

Gross profit ……………………………………………… 245,600

Operating expenses

Salaries and wages expense ……………… $110,000

Maintenance and repairs expense ……… 12,100

Freight-out ………………………………………… 11,700

Supplies expense ……………………………… 4,800

Total operating expenses ……………. 223,000

Income from operations …………………………… 22,600

Other expenses and losses

BUSE’S FASHION CENTER

Retained Earnings Statement

For the Year Ended November 30, 2014

Retained earnings, December 1, 2013 ……….. $30,000

Plus: Net income ……………………………………. 15,200

PROBLEM 5-6B (Continued)

BUSE’S FASHION CENTER

Balance Sheet

November 30, 2014

Assets

Current assets

Cash …………………………………………. $37,700

Accounts receivable ………………….. 33,700

Inventory…………………………………… 43,000

Liabilities and Stockholders’ Equity

Current liabilities

Long-term liabilities

Notes payable ($62,000 – $24,000) ………………. 38,000

Total liabilities …………………………………….. 87,200

Stockholders’ equity

PROBLEM 5-7B

ALMA’S DEPARTMENT STORE

Income Statement (Partial)

For the Year Ended December 31, 2014

Sales

Cost of goods sold

Inventory, January 1 ………….. $ 40,500

Purchases …………………………. $456,000

Less: Purchase discounts …. $12,000

Purchase returns

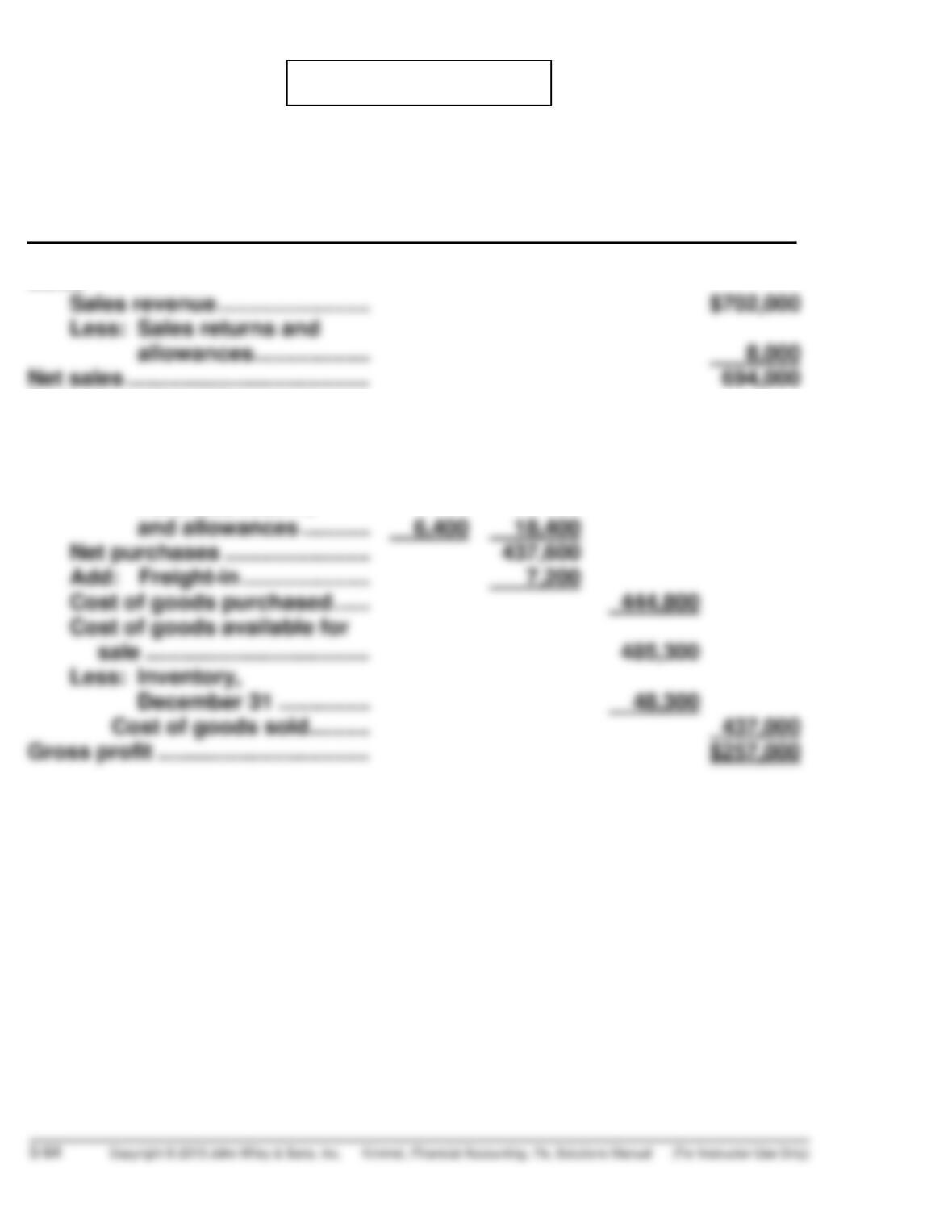

PROBLEM 5-8B

(a)

2013 2014 2015

Cost of goods sold:

Beginning inventory $ 16,000 $ 11,300 $ 16,400

(b)

2013 2014 2015

Sales revenue $229,700 $227,600 $220,000

(c)

2013 2014 2015

Beginning accounts payable $ 17,000 $ 28,000 $ 24,700

(d) Gross profit rate 34.0% 33.8% 35.7%

No. Even though sales declined in 2015 from each of the two prior years,

the gross profit rate increased. This means that cost of goods sold

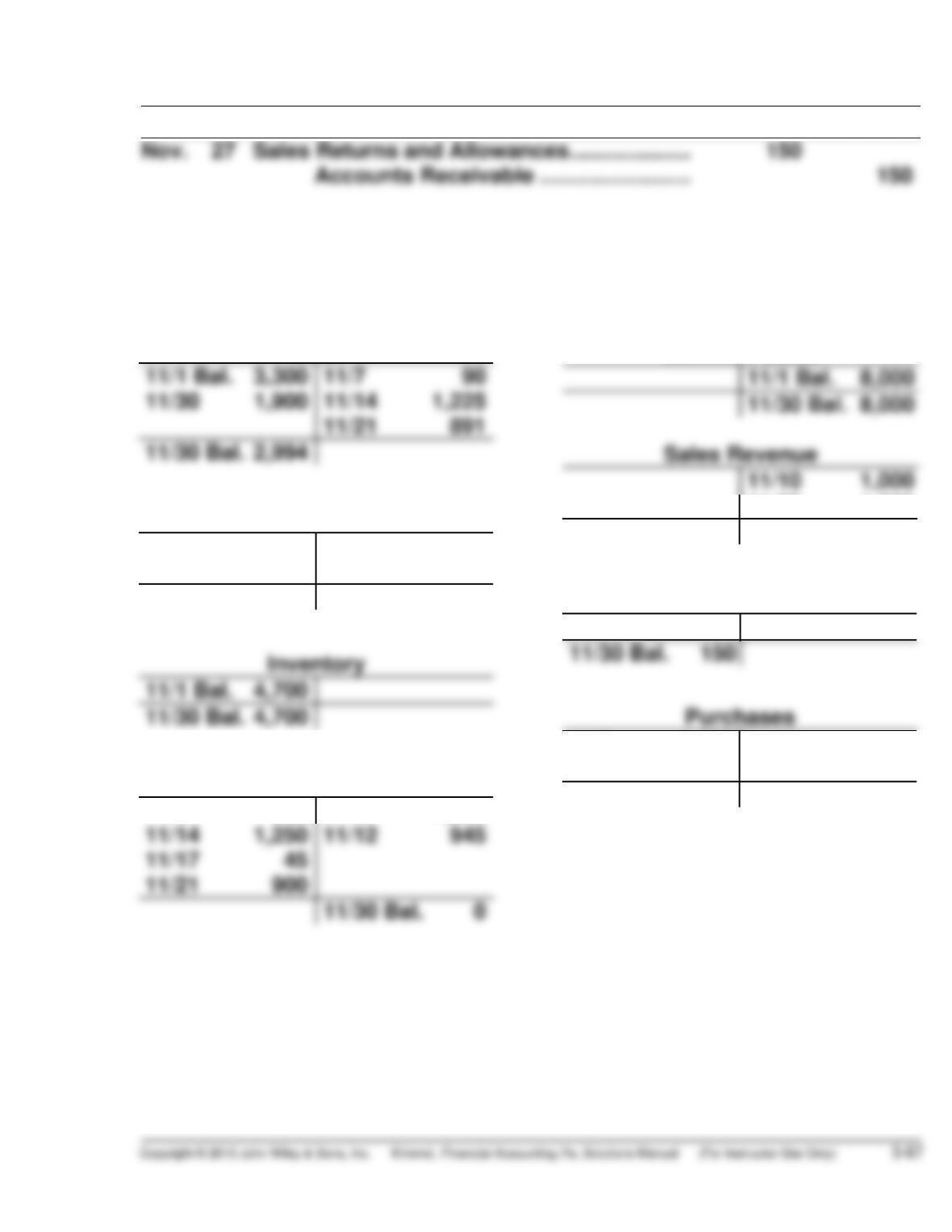

*PROBLEM 5-9B

(a) General Journal

Date Account Titles Debit Credit

9 Accounts Payable …………………………………… 350

Purchase Returns and

Allowances …………………………….

350

17 Accounts Payable …………………………………… 45

Purchase Returns and

Allowances …………………………….

45

20 Accounts Receivable ………………………………. 1,330

Sales Revenue ……………………………….. 1,330

*PROBLEM 5-9B (Continued)

Date

A

ccount Titles Debit Credit

30 Cash ……………………………………………………… 1,900

Accounts Receivable ……………………. 1,900

(b)

Cash

Accounts Receivable

11/10 1,000

11/20 1,330

11/27 150

11/30 1,900

11/30 Bal. 280

Accounts Payable

11/9 350

11/5 1,600

Common Stock

11/20 1,330

11/30 Bal. 2,330

Sales Returns and Allowances

11/27 150

11/5 1,600

11/12 945

11/30 Bal. 2,545

*PROBLEM 5-9B (Continued)

Purchase

Returns and Allowances

Purchase Discounts

Freight-In

11/7 90

(c)

WINONA SPORTS

Trial Balance

November 30, 2014

Debit Credit

Accounts Payable ……………………………………………… $ –0–

Common Stock ………………………………………………….. 8,000

Sales Revenue …………………………………………………… 2,330

*PROBLEM 5-9B (Continued)

(d)

WINONA SPORTS

Income Statement (Partial)

For the Month Ended November 30, 2014

_______________________________________________________________

Sales

Less: Purchase returns

and allowances …………… $395

Purchase discounts …… 34 429

Net purchases ……………………….. 2,116

Add: Freight-in …………………….. 90

Cost of goods purchased ………. 2,206

COMPREHENSIVE PROBLEM SOLUTION

(a) Dec. 6 Salaries and Wages Payable………………..

.

.

.

1,000

Sales Revenue ……………………………..

.

Cost of Goods Sold ……………………………..

.

Inventory ……………………………………..

.

4,100

6,300

4,100

.

.

.

.

.

20 Salaries and Wages Expense……………….

.

Cash …………………………………………….

.

1,800

1,800

.

COMPREHENSIVE PROBLEM SOLUTION (Continued)

Supplies Expense ………………………………..

.

Supplies ($3,200 – $1,500) ……………..

.

1,700

1,700

Income Tax Expense ……………………………

.

Income Taxes Payable …………………..

.

200

200

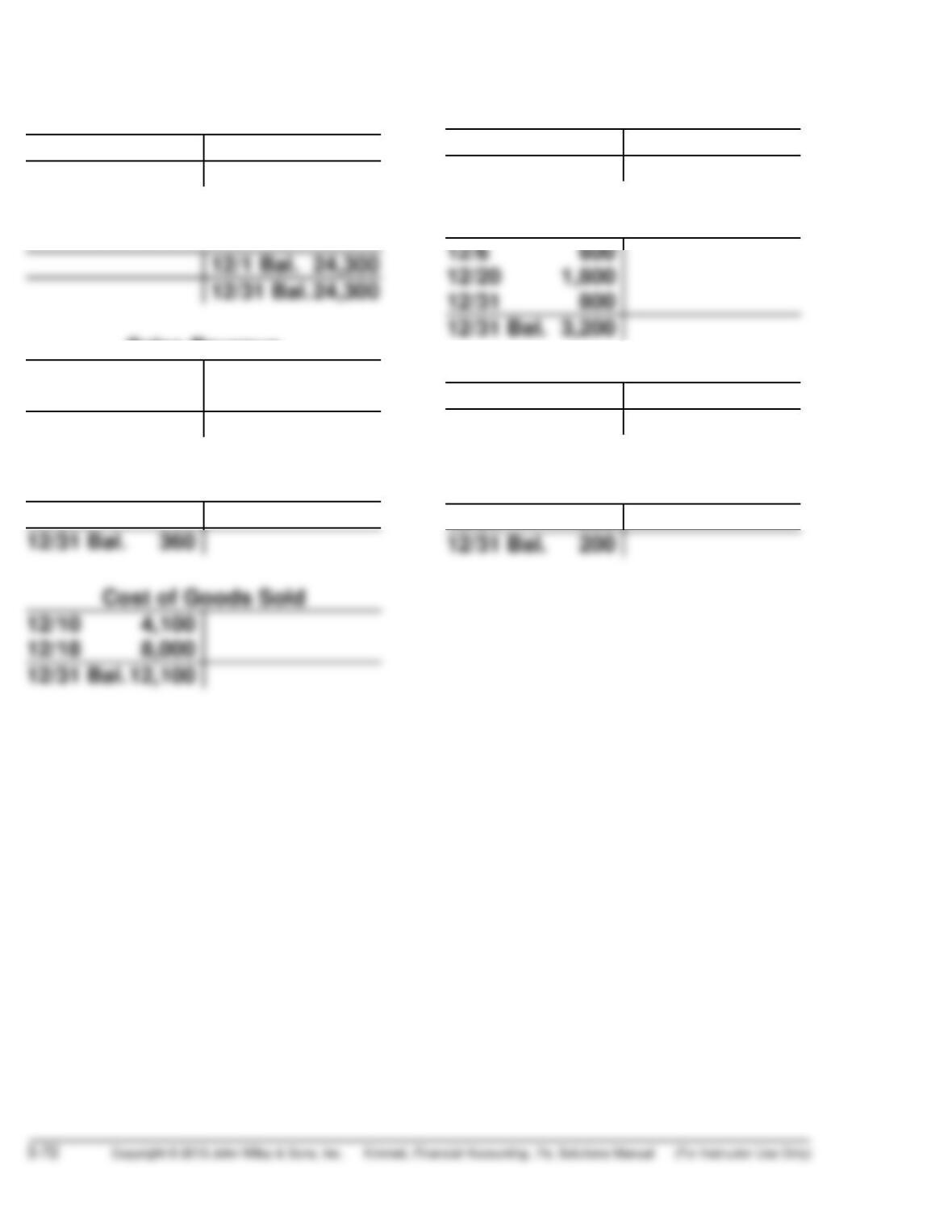

(b) & (c) General Ledger

Cash

12/1 Bal. 7,200

A

—

12/6 1,600

12/18 12,000

12/27 12,000

12/31 Bal. 2,700

Inventory

12/1 Bal. 12,000

12/10 4,100

Equipment

12/1 Bal. 22,000

A

ccounts Payable

12/23 9,000 12/1 Bal. 4,500

12/13 9,000

12/31 Bal. 4,500

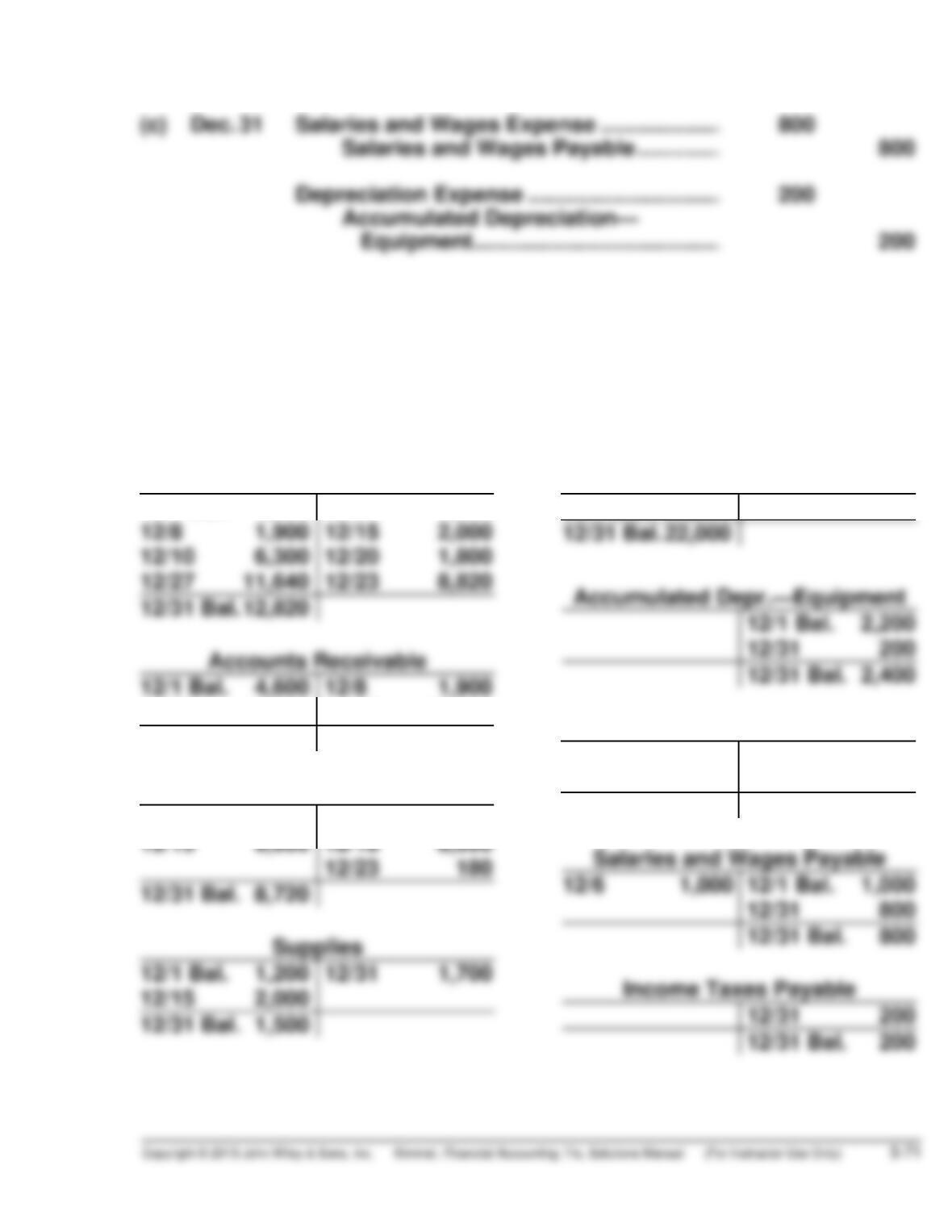

COMPREHENSIVE PROBLEM SOLUTION (Continued)

Common Stock

12/1 Bal. 15,000

12/31 Bal. 15,000

Retained Earnings

Sales Revenue

12/10 6,300

12/18 12,000

12/31 Bal. 18,300

Sales Discounts

12/27 360

Depreciation Exp.

12/31 200

12/31 Bal. 200

Salaries and Wages Expense

Supplies Expense

12/31 1,700

12/31 Bal. 1,700

Income Tax Expense

12/31 200

COMPREHENSIVE PROBLEM SOLUTION (Continued)

(d) BOLINE DISTRIBUTING COMPANY

Adjusted Trial Balance

December 31, 2014

DR. CR.

Cash ………………………………………………………

.

$12,820

Accounts Receivable………………………………

.

2,700

Inventory ………………………………………………..

.

8,720

Supplies …………………………………………………

.

1,500

Equipment ……………………………………………..

.

22,000

Accumulated Depreciation

—

Equipment…..

.

$ 2,400

Accounts Payable …………………………………..

.

4,500

Salaries and Wages Payable……………………

.

800

.

.

(e) BOLINE DISTRIBUTING COMPANY

Income Statement

For the Month Ending December 31, 2014

Sales revenue …………………………………………

.

$18,300

Less: Sales discounts ……………………………

.

360

Net sales ………………………………………………..

.

17,940

.

.

.

COMPREHENSIVE PROBLEM SOLUTION (Continued)

BOLINE DISTRIBUTING COMPANY

Retained Earnings Statement

For the Month Ended December 31, 2014

Retained earnings, Dec. 1 ………………………………………

.

$24,300

.

BOLINE DISTRIBUTING COMPANY

Balance Sheet

December 31, 2014

Assets

Current assets

Cash ………………………………………………….

.

$12,820

Accounts receivable …………………………..

.

2,700

Liability and Stockholders’ Equity

Current liabilities

Accounts payable ………………………………

.

$ 4,500

.

BYP 5-1 FINANCIAL REPORTING PROBLEM

(a) Percentage change in total revenue:

(b) Profit margin:

2009 $53,157 ÷ $499,331 = 10.6%

(c) Gross profit rates:

2009 $175,817* ÷ $495,592 = 35.5%