5–57 Ch. 5—Problems

Problem 5-15, Concluded

(CL1a) Eliminate the intercompany interest expense and revenue on factory lease:

Original balance ………………………………………………………………… $103,770

First lease payment ……………………………………………………………. (25,000)

(CL2a) Eliminate obligation under capital lease plus accrued interest payable against mini-

mum lease payments receivable and unearned interest income:

Obligations balance, January 1, 2017:

Original balance ………………………………………………………………… $103,770

Principal, January 1, 2016 …………………………………………………… (25,000)

(CL3a) Reclassify asset under capital lease and related accumulated depreciation for two

years. Depreciation is $103,770 ÷ 10, or $10,377 per year.

(CL1b) Eliminate the intercompany interest expense and revenue on equipment lease. Inter-

est is 12% × ($52,298 original balance – $15,000 first payment), or $4,476.

(CL2b) Eliminate obligation under capital lease ($52,298 – $15,000, or $37,298) and accrued

interest payable, $4,476, against minimum lease payments receivable (3 × $15,000 +

$2,000 purchase option, or $47,000) and unearned interest income:

(CL3b) Reclassify the asset and related accumulated depreciation. Depreciation is $52,298 ÷

8, or $6,537 per year.

(F2) Reduce the depreciation to depreciation based on cost of equipment to consolidated

entity:

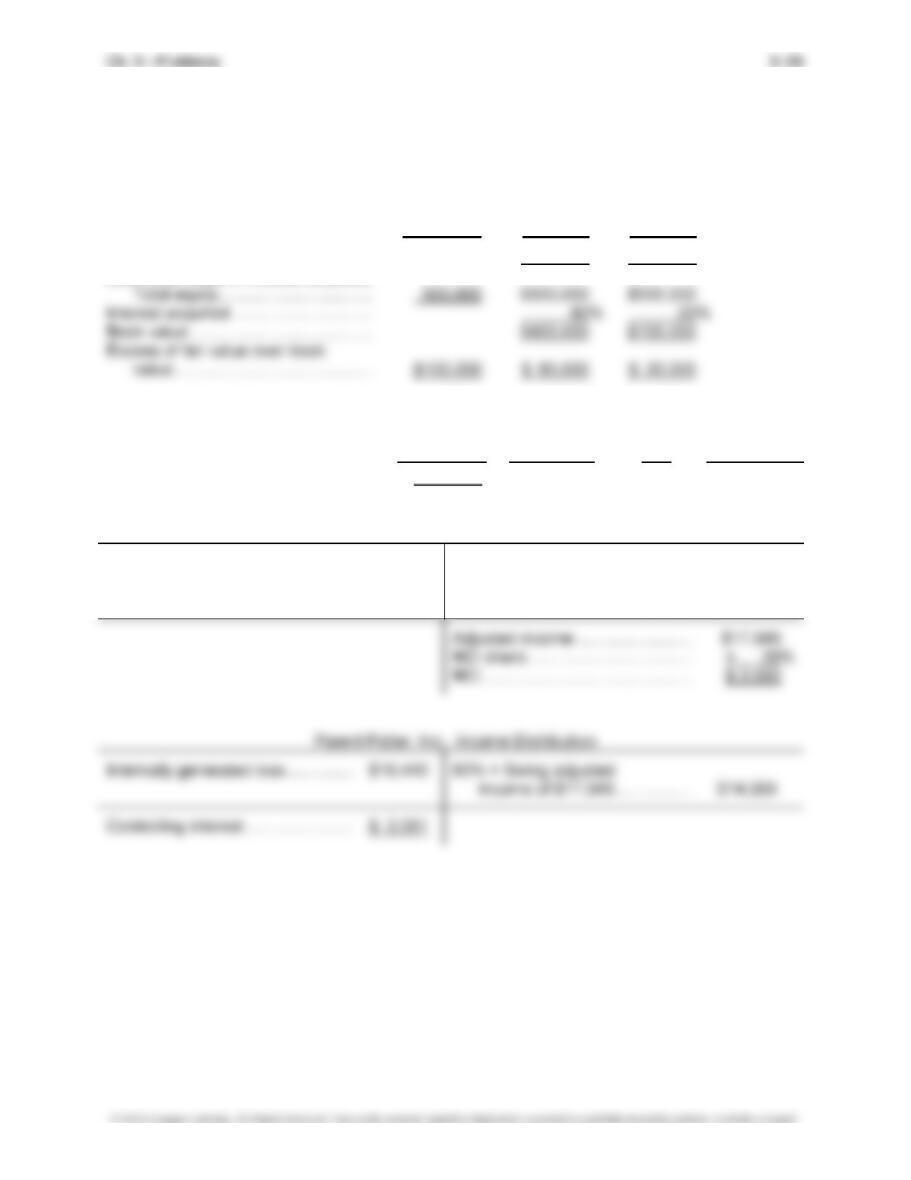

PROBLEM 5-16

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………………… $600,000 $480,000 $120,000

Less book value of interest acquired:

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Goodwill …………………………………….. $100,000 debit D

Subsidiary Swing Company Income Distribution

Internally generated net

income …………………………….. $17,440

Realized gain on machine ……….. 509

5–59 Ch. 5—Problems

Problem 5-16, Continued

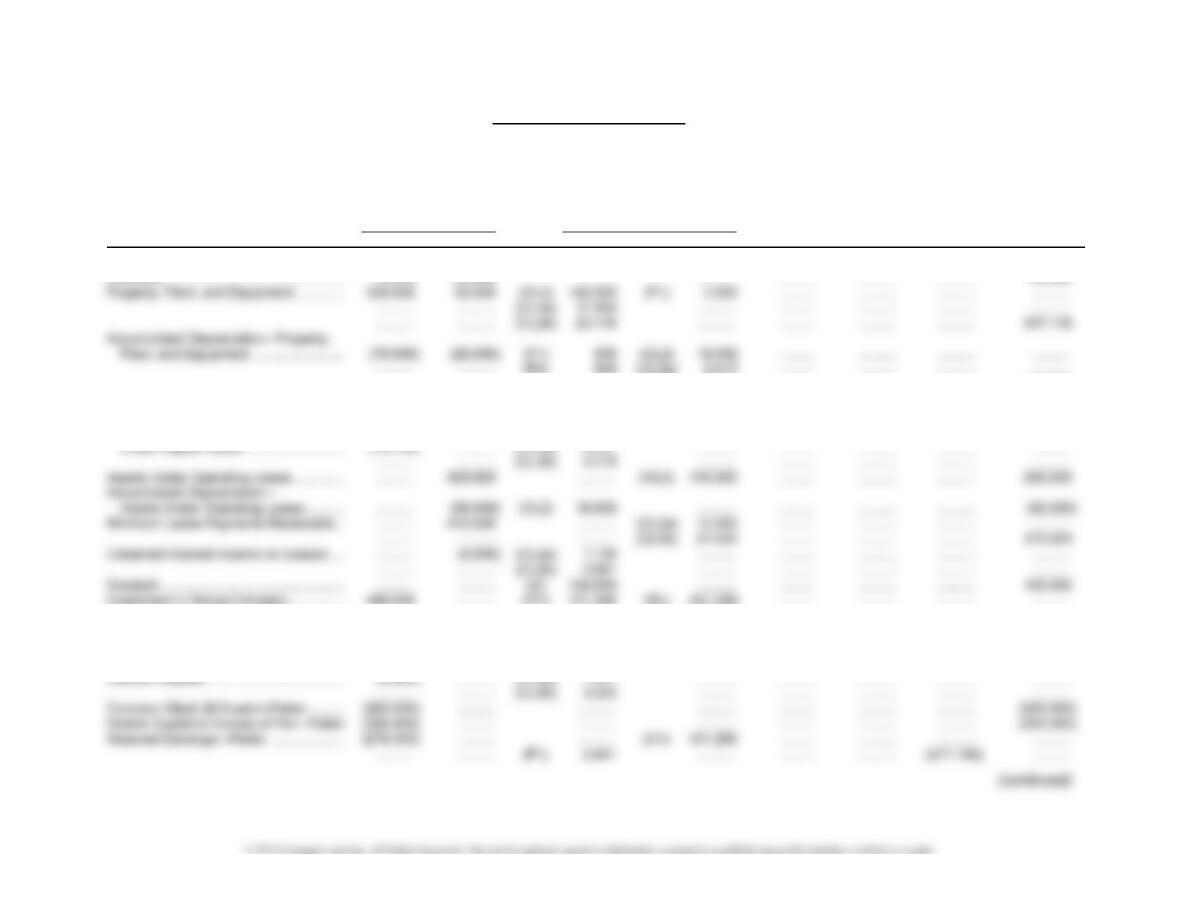

Patter, Inc., and Subsidiary Swing Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2015

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Patter Swing Dr. Cr. Statement NCI Earnings Sheet

Cash ………………………………………………. 91,013 26,050 ………. ………. ……… ………. ………. 117,063

………. ………. (F2) 509 (CL3a) 5,017 ……… ………. ………. ……….

………. ………. ………. (CL3b) 5,779 ……… ………. ………. (117,778)

Assets Under Capital Lease ………………. 40,676 ………. ………. (CL3a) 17,560 ……… ………. ………. ……….

………. ………. ………. (CL2b) 23,116 ……… ………. ………. ……….

Accumulated Depreciation—Assets

………. ………. ………. (D) 80,000 ……… ………. ………. ……….

Accounts Payable ……………………………. (130,000) (180,000) ………. ………. ……… ………. .……… (310,000)

Obligations Under Capital Lease ………… (24,560) ………. (CL2a) 9,444 ………. ……… ………. ………. ……….

………. ………. (CL2b) 15,116 ………. ……… ………. ………. ……….

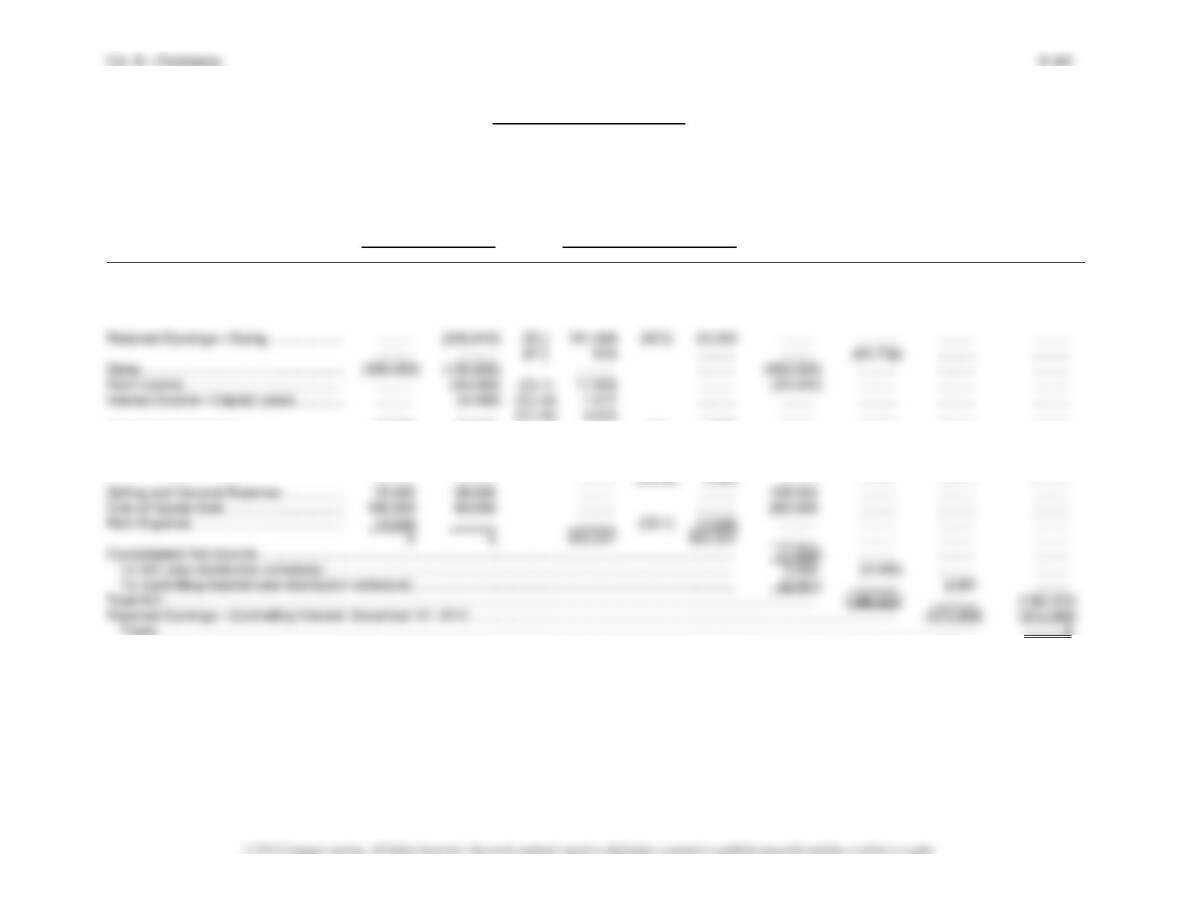

Problem 5-16, Continued

Patter, Inc. and Subsidiary Swing Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2015

(Concluded)

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Patter Swing Dr. Cr. Statement NCI Earnings Sheet

Common Stock ($10 par)—Swing ………. ………. (100,000) (EL) 80,000 ………. ……… (20,000) ………. …..…..

Paid-In Capital in Excess of Par—Swing ………. (300,000) (EL) 240,000 ………. ……… (60,000) ………. …..…..

Depreciation Expense ………………………. 41,000 23,000 ………. (F2) 509 ……… ………. ………. ..……..

………. ………. ………. ………. 63,491 ………. ………. ……….

Interest Expense ……………………………… 4,440 ………. ………. (CL1a) 1,417 ……… ………. .……… ……….

Problem 5-16, Continued

Eliminations and Adjustments:

(CV) Conversion to equity at the beginning of the year [80% × ($226,610 – $100,000)].

(EL) Eliminate the 80% ownership portion of the subsidiary equity accounts against the in-

vestment.

(D)/(NCI) Distribute the excess cost to goodwill.

Original balance ………………………………………………………………… $17,560

First lease payment ……………………………………………………………. (5,000)

First-year interest (15% × $12,560) ………………………………………. 1,884

(CL2a) Eliminate the obligation under capital lease plus accrued interest payable against min-

imum lease payments receivable and unearned interest income:

Obligations balance, January 1, 2015:

Original balance …………………………………………………………. $17,560

Principal, January 1, 2014 ……………………………………………. (5,000)

Principal, January 1, 2015 ($5,000 – $1,884)………………….. (3,116)

Balance ………………………………………………………………… $ 9,444

Minimum lease payments, January 1, 2015:

*($5,000 × 4) + $2,000

(CL3a) Reclassify the machine under the capital lease and related depreciation. Cost,

$17,560; accumulated depreciation, [($17,560 ÷ 7) × 2] = $5,017.

(F1) Defer remaining gain on asset at the beginning of the year, $3,560* less one year’s

amortization of $509** = $3,051. Because profit was recorded by the subsidiary, the

(F2) Adjust the current year’s depreciation for 1/7 of the gain, $509.

Ch. 5—Problems 5–62

Problem 5-16, Concluded

(CL1b) Eliminate intercompany interest expense/revenue on truck lease:

Original balance ……………………………………………………… $23,116

Initial payment ………………………………………………………… 8,000

5–63 Ch. 5—Problems

APPENDIX PROBLEMS

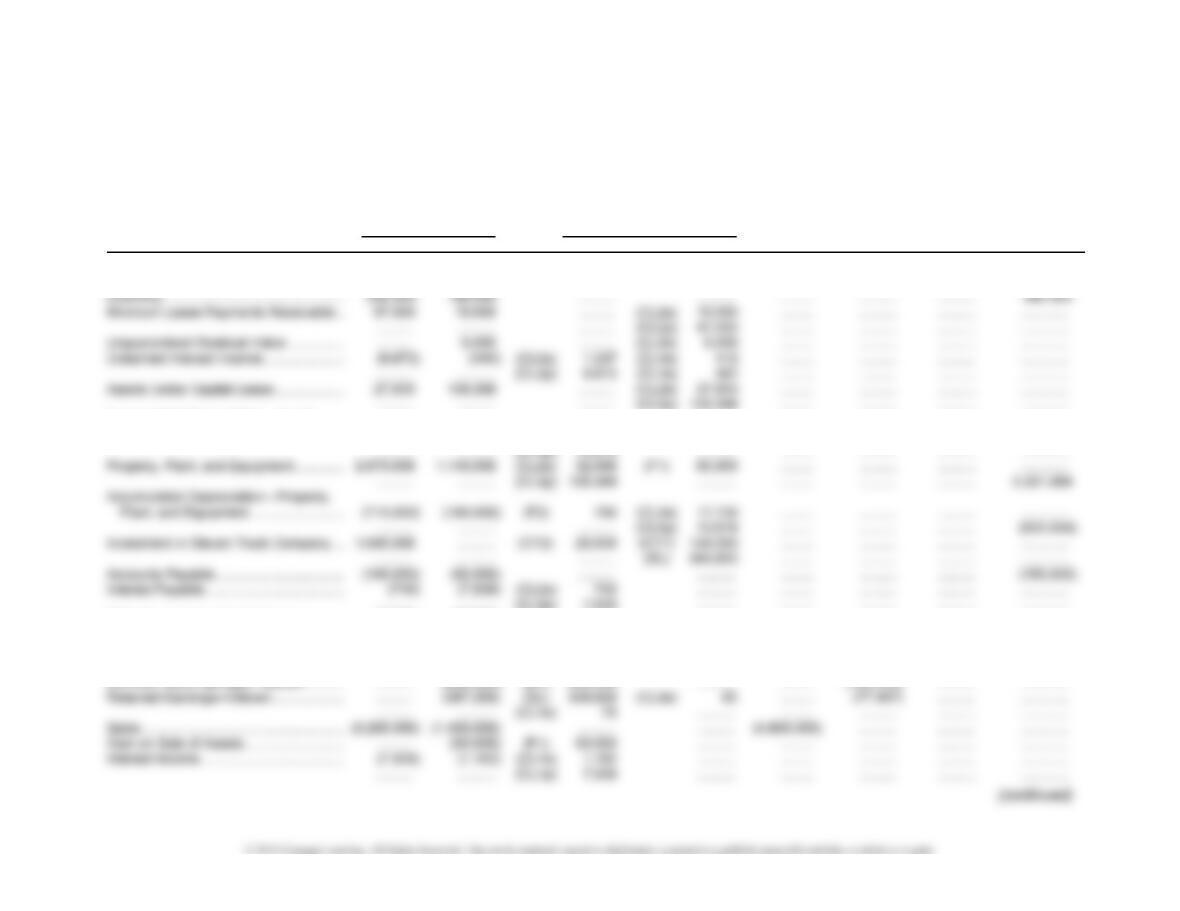

PROBLEM 5A-1

Paulz Heavy Equipment and Subsidiary Steven Truck Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Paulz Steven Dr. Cr. Statement NCI Earnings Sheet

Cash ………………………………………………. 90,485 123,307 ………. ………. ……… ………. ..…….. 213,792

Accounts Receivable (net) ………………… 228,000 120,000 ………. ………. ……… ………. ………. 348,000

Accumulated Depreciation—Assets

Under Capital Lease ……………………… (18,556) (13,674) (CL3s) 18,556 ………. ……… ………. ………. ………….

Obligations Under Capital Lease ………… (9,260) (79,388) (CL2s) 9,260 ………. ……… ………. ………. ………….

………. ………. (CL2p) 79,388 ………. ……… ………. ………. ………….

Common Stock ($5 par)—Paulz …………. (1,800,000) ………. ………. ………. ……… ………. ………. (1,800,000)

Retained Earnings—Paulz ………………… (864,834) ………. (CL1s) 305 (CL3s) 330 ……… ………. (864,859) ………….

Problem 5A-1, Continued

Paulz Heavy Equipment and Subsidiary Steven Truck Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

(Concluded)

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Paulz Steven Dr. Cr. Statement NCI Earnings Sheet

Rent Income ……………………………………. (2,182) ………. (CL4p) 2,182 ………. ……… …….... ………. ………….

Cost of Goods Sold ………………………….. 1,882,000 770,000 ………. ………. 2,652,000 ………. …..….. ………….

Subsidiary Income ……………………………. (124,000) ………. (CY1) 124,000 ………. ……… ………. ………. ..………..

Dividends Declared ………………………….. 144,000 35,000 ………. (CY2) 28,000 ……… 7,000 144,000 ………….

0

0 1,456,655 1,456,655 ……… ………. ………. ………….

Consolidated Net Income ………………………………………………………………………………………….…………………… (363,806) ………. ………. ………….

To NCI (see distribution schedule) ……………………………………………………………………………….……………… 19,150 (19,150) ………. ………….

Eliminations and Adjustments:

(CY1) Eliminate the current-year subsidiary income to the investment account.

(CY2) Eliminate the current-year dividends to the investment account.

(EL) Eliminate 80% of the subsidiary equity balances.

Lessee Lessor

Interest Interest Interest

Date Payment (8%) Balance Payment (8%) Balance Difference

January 1, 2015 $10,000 ………… $17,833 $10,000 ………… $22,596 ……….

5–65 Ch. 5—Problems

Problem 5A-1, Continued

(CL3s) Reclassify and adjust the depreciation on the truck, ($27,833 ÷ 3) versus ⅓ ×

($32,596 – $6,000 residual). Adjust past and current year by $413 ($9,278 – $8,865).

(CL1p) Eliminate interest revenue and expense on equipment lease, 10% × ($109,388 origi-

nal balance – $30,000 payment, January 1, 2016), or $7,939.

(CL3p) Reclassify the equipment under capital lease and related accumulated depreciation

for one year. Annual depreciation is $109,388 ÷ 8, or $13,674.

(CL4p) Eliminate the intercompany rent revenue and expense, $2,182, which is $1,500 ex-

ecutory costs plus $682 contingent payment, computed as follows:

Previous growth rate of net income ………………………………………………… 8%

(2015 net income, $81,650 ÷ 2014 net income of $75,600, or 1.08;

2014 net income, $75,600 ÷ 2013 net income of $70,000, or 1.08)

2016 net income, excluding gain on asset sale ………………………………… $95,000

Less 1.08 × $81,650, 2015 net income …………………………………………… 88,182

(F1) Eliminate the gain on the intercompany sale of warehouse and reduce the asset to its

cost to the consolidated entity.

(F2) Adjust current year’s depreciation for one-quarter year, or $750 ($60,000 gain ÷

Problem 5A-1, Concluded

Subsidiary Steven Truck Company Income Distribution

Unrealized gain on sale Internally generated net

of warehouse……………………. $60,000 income …………………………… $155,000

Unearned interest on Gain realized through use

residual……………………………. 412 of warehouse ………………….. 750

Adjustment of depreciation

on lease …………………………. 413

PROBLEM 5A-2

(1) Eliminations and Adjustments at December 31, 2015:

Interest Income ……………………………………………………………………. 5,136

Interest Expense ……………………………………………………………… 4,623

Unearned Interest Income …………………………………………………. 513

To eliminate intercompany interest revenue and expense.

Property, Plant, and Equipment (original cost to lessor) …………….. 50,098

Obligations Under Capital Lease ……………………………………………. 28,894

Interest Payable …………………………………………………………………… 4,623

Problem 5A-2, Concluded

(2) Eliminations and Adjustments at December 31, 2016:

Interest Income ……………………………………………………………………. 3,077

Interest Expense ……………………………………………………………… 2,483

Unearned Interest Income …………………………………………………. 594

To eliminate intercompany interest revenue and expense.

Retained Earnings—Penn …………………………………………………….. 513

Unearned Interest Income …………………………………………………. 513

To adjust for interest income recorded on residual

value in 2015.

CASE 5-1

First, let’s consider the existing outstanding bonds. There is a major difference in interest rates

between those available to Power Pro and Swift-Craft. To the extent possible, the debt should

be directly or indirectly retired. Direct retirement would be accomplished by Power Pro lending

funds to Swift-Craft, which Swift-Craft would in turn use to retire the bonds. The other alternative

is for Power Pro to purchase the existing bonds that it could and then hold them as an invest-

It would appear that Power Pro will build and equip the new plant. It can add a reasonable profit.

The higher the price, the greater the shift of income from the subsidiary to the parent. When

consolidating, the profit is removed from the gain account and the asset accounts. It is deferred

over the period of use as a decrease in depreciation expense.

Power Pro could sell the assets to Swift-Craft in return for a long-term mortgage. Again, any rate

under 11% is a bonus to the NCI shareholders. Again, the intercompany debt and interest

revenue/expense are eliminated in the consolidation process.

CASE 5-2

(1) Option (a):

Consolidated Income Statement

Sales ……………………………………………………………………………………….. $ 320,000

Cost of goods sold …………………………………………………………………….. (220,000)

Gross profit …………………………………………………………………………. $ 100,000

Consolidated Balance Sheet

Assets Liabilities and Equity

Cash ……………………………… $ 173,000 Current liabilities …………….. $ 45,000

Other current assets ………… 250,000 NCI ………………………………. 82,000*

(2) Option (b):

There would be no difference. The bonds would still be retired from a consolidated view-

point with the parent paying $185,000 to retire the bonds. The gain would still be credited to

CASE 5-3

(1) Entries:

Pannier:

Notes Receivable…………………………………………………………………. 125,000

(2) Consolidated statements:

Consolidated Income Statement

Sales ……………………………………………………………………………………….. $ 320,000

Cost of goods sold …………………………………………………………………….. (220,000)

Gross profit …………………………………………………………………………. $ 100,000

Consolidated Balance Sheet

Assets Liabilities and Equity

Cash ……………………………… $ 358,000 Current liabilities …………….. $ 45,000

Inventory ………………………… 90,000 Long-term debt ………………. 200,000

Other current assets ………… 210,000 NCI ………………………………. 79,000*

5–71 Ch. 5—Cases

Case 5-3, Concluded

(3) Entries:

Pannier:

Minimum Lease Payments Receivable (4 × $29,977) ……………….. 119,908

Cash ………………………………………………………………………………….. 29,977

Inventory ………………………………………………………………………… 100,000

Unearned Interest Income …………………………………………………. 24,885

(4) There would be no difference in the consolidated statements.