Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

5-61

PROBLEM 5-59 (CONTINUED)

3.

The unit costs of the products using activity-based costing are calculated as follows:

Fabricating:

Total cost ................................................................................................

$2,951,820

Less: Direct material ................................................................

480,000

Assembly:

Total cost ................................................................................................

$978,180

Less: Direct labor ................................................................................................

624,000

Tuff Stuff unit cost:

Direct material ................................................................................................

$15.00

5-62

PROBLEM 5-59 (CONTINUED)

Ruff Stuff unit cost:

Direct material ................................................................................................

$ 9.00

4.

Ruff Stuff unit costs:

Cost with overhead assigned on direct-labor hours ................................

$112.50

Chapter 05 - Activity-Based Costing and Management

5-63

PROBLEM 5-60 (60 MINUTES)

1.

Based on the cost data from Gigabyte's traditional, volume-based product-costing

system, product G is the firm's least profitable product. Its reported actual gross

2.

Again, based on the product costs reported by the firm's traditional, volume-based

product-costing system, product W appears to be very profitable. As in requirement

3.

Gigabyte's competitors have moved aggressively into the market for gismos (product

G), but they have abandoned the whatchamacallit (product W) market to Gigabyte.

These competing firms apparently believe they can sell gismos at a much

lower price than Gigabyte's management feels is feasible. This evidence suggests that

4.

Percentages for raw-material costs:

Percentage

Annual

of Total

Raw-Material

Annual

Raw-Material

Raw-Material

Product

Cost per Unit

Volume

Cost

Cost*

G

$105.00

8,000

$ 840,000

25%

Chapter 05 - Activity-Based Costing and Management

5-64

PROBLEM 5-60 (CONTINUED)

5.

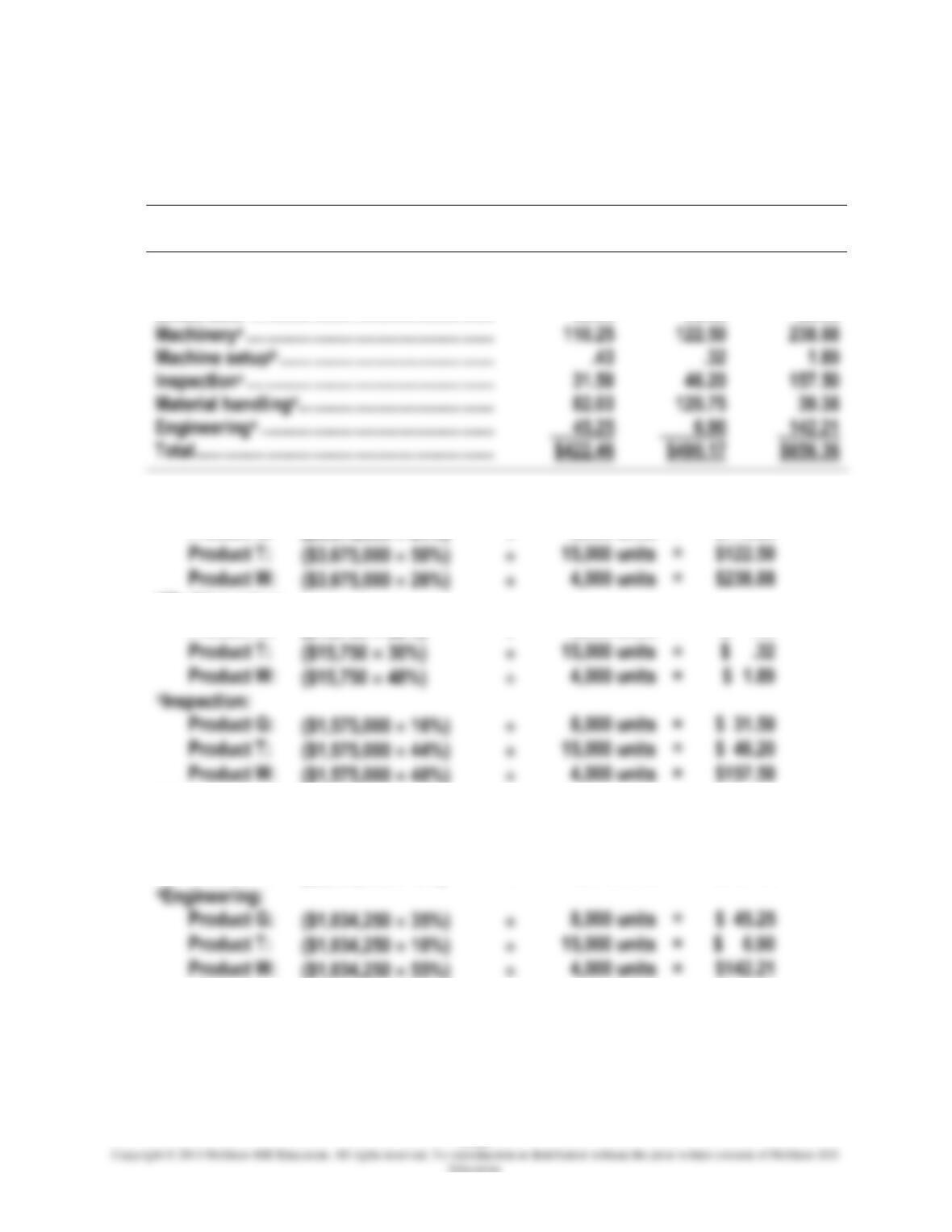

Product costs based on an activity-based costing system:

Product

G

Product

T

Product

W

Direct material................................................

$105.00

$157.50

$ 52.50

Direct labor ....................................................

48.00

36.00

24.00

aMachinery:

Product G:

($3,675,000 24%)

8,000 units

=

$110.25

bMachine setup:

Product G:

($15,750 22%)

8,000 units

=

$ .43

dMaterial handling:

Product G:

($2,625,000 25%)

8,000 units

=

$ 82.03

Product T:

($2,625,000 69%)

15,000 units

=

$120.75

Product W:

($2,625,000 6%)

4,000 units

=

$ 39.38

Chapter 05 - Activity-Based Costing and Management

PROBLEM 5-60 (CONTINUED)

6.

Comparison of reported product costs, new target prices, and actual selling prices:

Product

G

Product

T

Product

W

Reported product costs:

Traditional, volume-based costing system

$573.00

$508.50

$286.50

5-66

PROBLEM 5-61 (20 MINUTES)

MEMORANDUM

Date:

Today

To:

President, Gigabyte, Inc.

From:

I.M. Student

Subject:

Gigabyte's competitive position

Gigabyte's product-costing system has been providing misleading product cost

information. Our traditional, volume-based costing system overcosted gismos and

I recommend the following courses of action:

Chapter 05 - Activity-Based Costing and Management

5-67

PROBLEM 5-62 (20 MINUTES)

Product

G

Product

T

Product

W

Traditional, volume-based costing system:

Traditional

Traditonal

Traditional

system

system

system

overcosts

overcosts

undercosts

PROBLEM 5-63 (25 MINUTES)

1.

Process time: steps 3, 5, 6, 7, 8, 10, 11

Chapter 05 - Activity-Based Costing and Management

5-68

EXERCISE 5-63 (CONTINUED)

2.

Candidates for non-value-added activities

follow. (Note that elimination of some of

these activities would require reconfiguring

the production process.)

(a)

Step 1:

Storing ingredients (Could move toward JIT system.)

(f)

Step 6:

Carrying uncooked bagels to adjoining room.

(g)

Step 7:

Carrying bagels to oven room.

Chapter 05 - Activity-Based Costing and Management

5-69

PROBLEM 5-64 (40 MINUTES)

(1)

Redesigned bagel production process:

(a)

Ingredients, such as flour and raisins, are received and inspected in the morning

(b)

Dough is mixed in 40-pound batches in four heavy-duty mixers. The dough is

(e)

Bagels are removed from the vats with a long-handled strainer and placed on a

Chapter 05 - Activity-Based Costing and Management

5-70

PROBLEM 5-64 (CONTINUED)

(i)

After the bagels are cool, the wire baskets are placed on the conveyor and

(2 )

New equipment:

Bodacious Bagels, Inc. would need to purchase a new conveyor system that would

5-71

PROBLEM 5-65 (45 MINUTES)

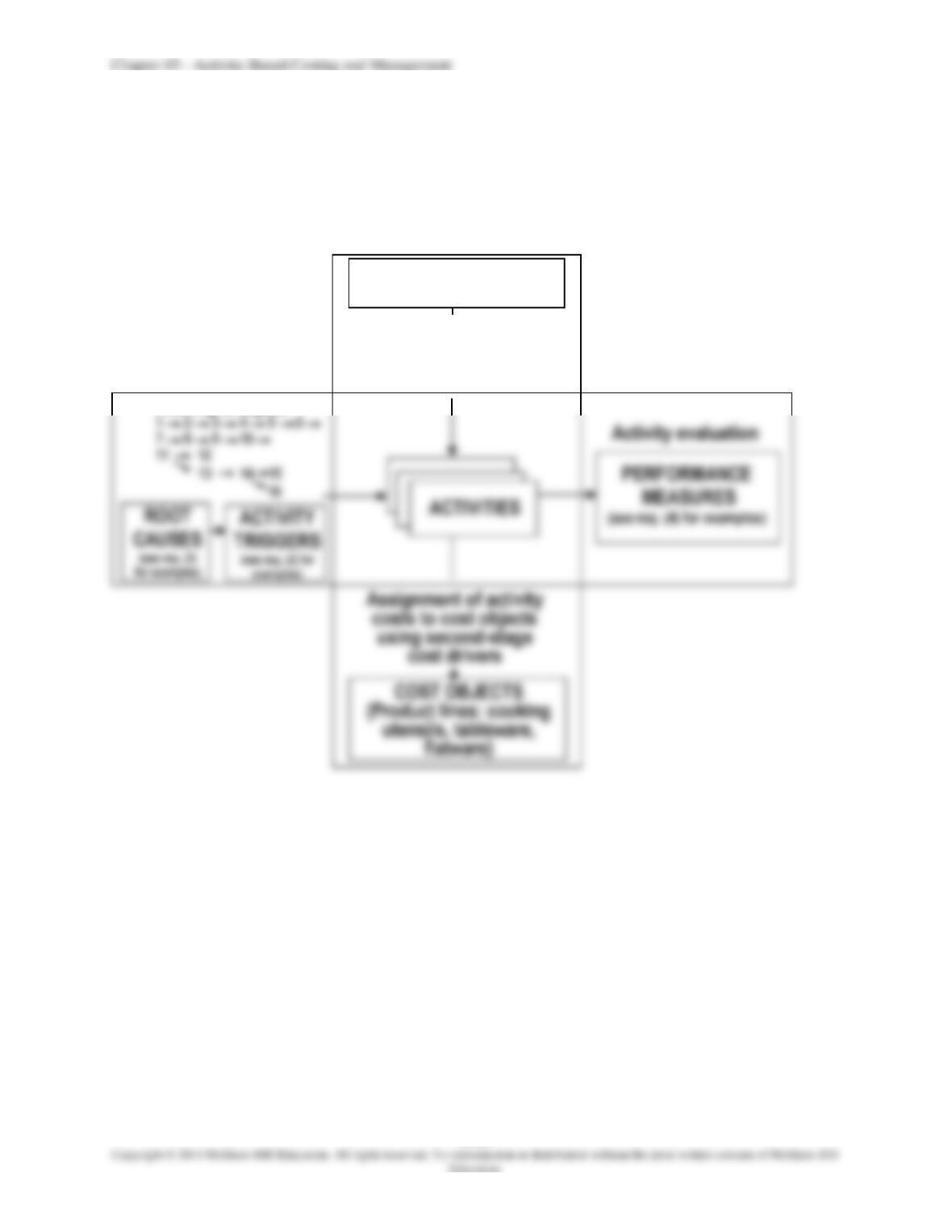

1.

Two dimensional ABC:

Cost Assignment View

RESOURCE COSTS

Assignment of resource costs

to activity cost pools

associated with

significant activities

Process View

Activity analysis

5-72

PROBLEM 5-65 (CONTINUED)

2.

Triggers for selected activities:

Activity

Number

Trigger

(2)

Realization by purchasing personnel that they do not fully understand the

3.

Possible root causes:

Activity

Number

Possible Root Causes*

(2)

Unclear specifications

(9)

Vendor delay

(12)

Misspecification of parts

(13)

Misspecification of parts

5-73

PROBLEM 5-65 (CONTINUED)

4.

Suggested performance measures:

Activity

Number

Performance

Measures

(5)

Average price paid

PROBLEM 5-66 (40 MINUTES)

1. Customer-profitability analysis:

Caltex

Computer

Trace

Telecom

Sales revenue ......................................................................

$380,000

$247,600