CHAPTER 5

UNDERSTANDING THE ISSUES

1. The first approach that could be used to

reduce the overall consolidated interest

cost but maintain the subsidiary as the deb-

tor would have the parent advancing

the debt is retired. Therefore, interest ex-

pense would be eliminated during the con-

solidation process.

2. At the 6% annual interest rate, a loss on

retirement of bonds will occur in the current

year since the parent paid a premium to re-

tire the subsidiary’s bonds. In the current

and future years, consolidated net income

will be increased by the difference between

interest expense and interest revenue. This

amount represents the amortization of the

3. Since Company S was the original issuer of

the bonds, it will absorb the loss that results

in the current year from the parent retiring

the bonds at a premium. The noncontrolling

4. In the current year, consolidated net in-

come will include a gain on retirement of

bonds of $4,000 ($100,000 – $96,000). In

the current and each of the next four years,

5. It is true that intercompany operating leas-

es eliminated during the consolidation

process will not have an effect on consoli-

dated income. However, the excessive rent

expense amounts will still appear on the

subsidiary’s separately stated income

statement and will reduce the NCI share of

consolidated income. The high lease rates

will shift income from the NCI to the control-

ling interest.

6. Either type of lease can shift income to the

it is deferred and amortized over the life of

the asset or life of the lease. The controlling

interest has the opportunity to increase its

profit by leasing the asset to the subsidiary.

Ch. 5—Exercises 5–2

EXERCISES

EXERCISE 5-1

It is desirable to refinance for two reasons. First, interest rates are down, and it would be wise to

lock in at the lower rate. Second, the parent firm can borrow funds at a lower interest rate. The

simplest way to accomplish the refinancing is to have the parent incur the new debt and loan the

proceeds to the subsidiary; the subsidiary would use the funds to retire its debt with a gain on

retirement being recognized that would flow to the consolidated statements. The parent would

not only enjoy a lower interest rate, but it could also structure the loan terms, including the ma-

EXERCISE 5-2

(a) (1) The consolidated income statement for 2017 will include a gain on retirement of the

(2) The subsidiary income distribution schedule will get the benefit of the retirement gain of

$25,000 in the year the bonds are purchased, but subsidiary income will be reduced

each year for the amortization of the purchase discount recorded by the parent

(2) The income distribution of the subsidiary is reduced by $3,125 for the amortization of

5–3 Ch. 5—Exercises

EXERCISE 5-3

(1) Eliminations and Adjustments at December 31, 2015:

Interest Revenue ……………………………………………………………. 7,750

Bonds Payable ………………………………………………………………. 100,000

Loss on Retirement…………………………………………………………. 3,900c

Interest Expense ………………………………………………………… 8,400

Investment in Bonds ……………………………………………………. 101,250a

Discount on Bonds Payable …………………………………………. 2,000b

(2) Eliminations and Adjustments at December 31, 2016:

Interest Revenue ……………………………………………………………. 7,750

Bonds Payable ………………………………………………………………. 100,000

Retained Earnings—Dove (80% × $3,250*) ……………………….. 2,600

Retained Earnings—Cardinal (20% × $3,250*) …………………… 650

EXERCISE 5-4

Gain on retirement (January 2, 2016):

Balance on issuer’s books ………………………………………………… $48,734

Schedule of interest adjustments:

Intercompany Interest, Recorded Interest, Interest Expense

Year Effective Interest Effective Interest Adjustment to Issuer

Ending on Purchase (10%) on Issuance (9%) Income Distribution Schedule

12/31/16 $4,751 $4,386 $ 365

EXERCISE 5-5

(1) Eliminations and Adjustments at December 31, 2017:

Interest Revenue [(7% × $60,000) + ($6,400 ÷ 8)] ……………………. 5,000

Bonds Payable (60% × $100,000) ………………………………………….. 60,000

Premium on Bonds Payable (60% × $700) ……………………………… 420

Interest Expense [($4,200 – (60% × $100)] …………………………. 4,140

Investment in Bonds [balance at year-end $53,600 + ($6,400/8)] 54,400

Gain on Retirement* …………………………………………………………. 6,880

Exercise 5-5, Concluded

(2) Eliminations and Adjustments at December 31, 2018:

Interest Revenue …………………………………………………………………. 5,000

Bonds Payable ……………………………………………………………………. 60,000

Premium on Bonds Payable (60% × $600) ……………………………… 360

Interest Expense ……………………………………………………………… 4,140

EXERCISE 5-6

Partial Schedule of Bond Premium Amortization

10-Year, 6% Bonds Sold to Yield 8% (Linco)

Carrying

Interest Premium Amount

Date Cash Paid Expense Amortized of Bonds

January 1, 2015 …….. ……. …….. $86,580

January 1, 2016 $6,000 $6,926 $ 926 87,506

Partial Schedule of Bond Discount Amortization

7-Year (remaining), 6% Bonds Sold to Yield 9% (Sharp)

Carrying

Cash Interest Discount Value

Date Received Revenue Amortized of Bonds

Exercise 5-6, Concluded

(1) Eliminations and Adjustments at December 31, 2018:

Interest Revenue ……………………………………………………………. 7,641

Bonds Payable ………………………………………………………………. 100,000

Discount Bonds Payable ……………………………………………… 9,247

Gain on Retirement ($89,586 – $84,901) ……………………….. 4,685

(2)

Subsidiary Linco Industries Income Distribution

Interest adjustment Internally generated net

($7,641 – $7,167) ………………. $474 income …………………………… $500,000

Retirement gain on bonds ……… 4,685

5–7 Ch. 5—Exercises

EXERCISE 5-7

(1) 2015 entries for Grande Machinery Company:

Machine ……………………………………………………………………………… 60,000

Cash ………………………………………………………………………………. 60,000

(2) 2015 entry for Sunshine Engineering Company:

(3) 2015 consolidation worksheet eliminations and adjustments:

Machine ……………………………………………………………………………… 60,000

Accumulated Depreciation—Asset Under Operating Lease ……….. 12,000

EXERCISE 5-8

(1)

Lease Payment Amortization Schedule

Interest at 12% on Reduction Principal

Date Payment Previous Balance of Principal Balance

January 1, 2015 $40,822

January 1, 2015 $12,000 $12,000 28,822

January 1, 2016 12,000 $3,459 8,541 20,281

Exercise 5-8, Concluded

(2) Eliminations and Adjustments at December 31, 2015:

Interest Revenue (see amortization schedule) …………………………. 3,459

Interest Expense ……………………………………………………………… 3,459

To eliminate intercompany interest revenue and expense.

Obligations Under Capital Lease ($40,822 – $12,000 first payment) 28,822

Interest Payable …………………………………………………………………… 3,459

(3) Eliminations and Adjustments at December 31, 2016:

Interest Revenue (see amortization schedule) …………………………. 2,434

Interest Expense ……………………………………………………………… 2,434

To eliminate intercompany interest revenue and expense.

Obligations Under Capital Lease ……………………………………………. 20,281

5–9 Ch. 5—Exercises

EXERCISE 5-9

Eliminations and Adjustments at December 31, 2015:

Interest Income (see amortization schedule) …………………………….. 2,690

Interest Revenue ……………………………………………………………… 2,690

To eliminate intercompany interest revenue and expense.

($35,000/8 yrs.) ………………………………………………………………….. 4,375

Assets Under Capital Lease ………………………………………………. 35,000

Accumulated Depreciation—Property, Plant, and Equipment …. 4,375

To reclassify asset under capital lease and related

accumulated depreciation as a productive asset owned

by the consolidated entity. Asset is depreciated over

8-year life.

Sales Profit on Leases …………………………………………………………… 10,000

Property, Plant, and Equipment …………………………………………. 10,000

To eliminate unrealized profit on intercompany “sale” and

to reduce asset to its cost to the consolidated entity.

Ch. 5—Problems 5–10

PROBLEMS

PROBLEM 5-1

(1) Bonds Payable ……………………………………………………………………. 50,000

Interest Income ($3,500 + $250 amortization) ………………………….. 3,750

(2) Jones Corporation and Subsidiary Dancer Corporation

Consolidated Income Statement

For Year Ended December 31, 2016

Sales ……………………………………………………………………………………….. $3,040,000

Cost of goods sold …………………………………………………………………….. 1,405,000

5–11 Ch. 5—Problems

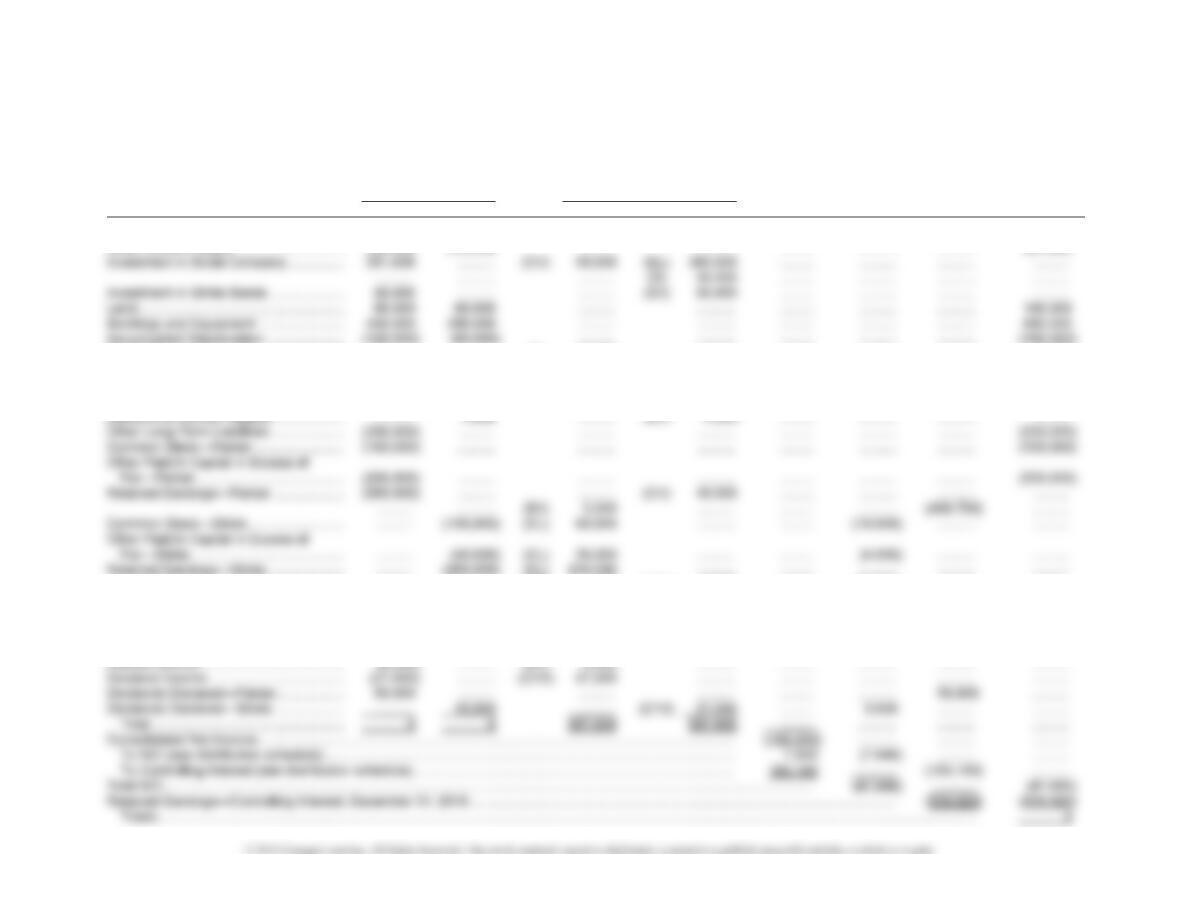

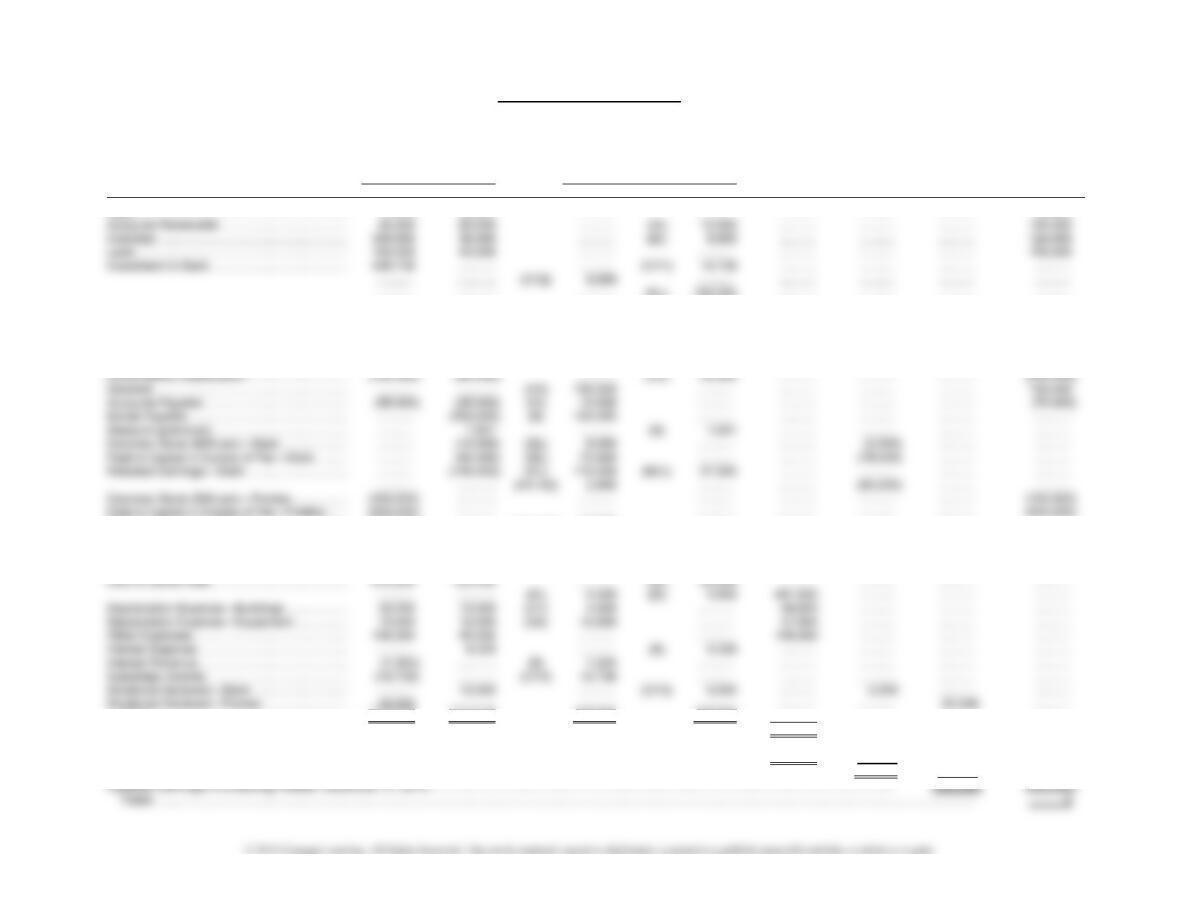

PROBLEM 5-2

Parker Company and Subsidiary Stride Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Parker Stride Dr. Cr. Statement NCI Earnings Sheet

Interest Receivable ………………………….. 4,000 ………. ………. (B2) 4,000 ……… ………. ….…… ……….

Other Current Assets ……………………….. 246,400 315,200 ………. ………. ……… ………. ………. 561,600

Accumulated Depreciation ………………… (120,000) (60,000) ………. ………. ……… ………. …….… (180,000)

Goodwill …………………………………………. ………. ………. (D) 40,000 ………. ……… ….…… ………. 40,000

Interest Payable ………………………………. ………. (4,000) (B2) 4,000 ………. ……… ………. .……… ……….

Other Current Liabilities ……………………. (98,000) (56,000) ………. ………. ……… ………. ………. (154,000)

Bonds Payable (8%) ………………………… ………. (100,000) (B1) 100,000 ………. ……… ………. ..…….. ……….

………. ………. (B1) 360 (NCI) 4,000 ……… (29,640) ………. ……….

Net Sales ……………………………………….. (640,000) (350,000) ………. ………. (990,000) ………. ………. ……….

Cost of Goods Sold ………………………….. 360,000 200,000 ………. ………. 560,000 ………. ………. ……….

Operating Expenses …………………………. 168,400 71,400 ………. ………. 239,800 ………. ………. ……….

Interest Expense ……………………………… ………. 8,600 ………. (B1) 8,600 ……… ………. ….…… ……….

Problem 5-2, Continued

Eliminations and Adjustments:

(CV) Convert to simple equity method as of January 1, 2016.

(B1) Eliminate intercompany interest revenue and expense. Eliminate the balance in

the investment in bonds against bonds payable and the discount on bonds paya-

ble. The loss on retirement at the start of the year is calculated as follows:

Loss remaining at year-end:

Investment in bonds at

December 31, 2016 …………………….. $98,400

Bonds payable …………………………………. $100,000

5–13 Ch. 5—Problems

Problem 5-2, Concluded

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (90%) (10%)

Fair value of subsidiary ………………… $390,000 $351,000 $ 39,000

Less book value of interest acquired:

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Goodwill …………………………………….. $ 40,000 debit D

Subsidiary Stride Company Income Distribution

Internally generated net

income …………………………….. $70,000

Interest adjustment ………………… 400

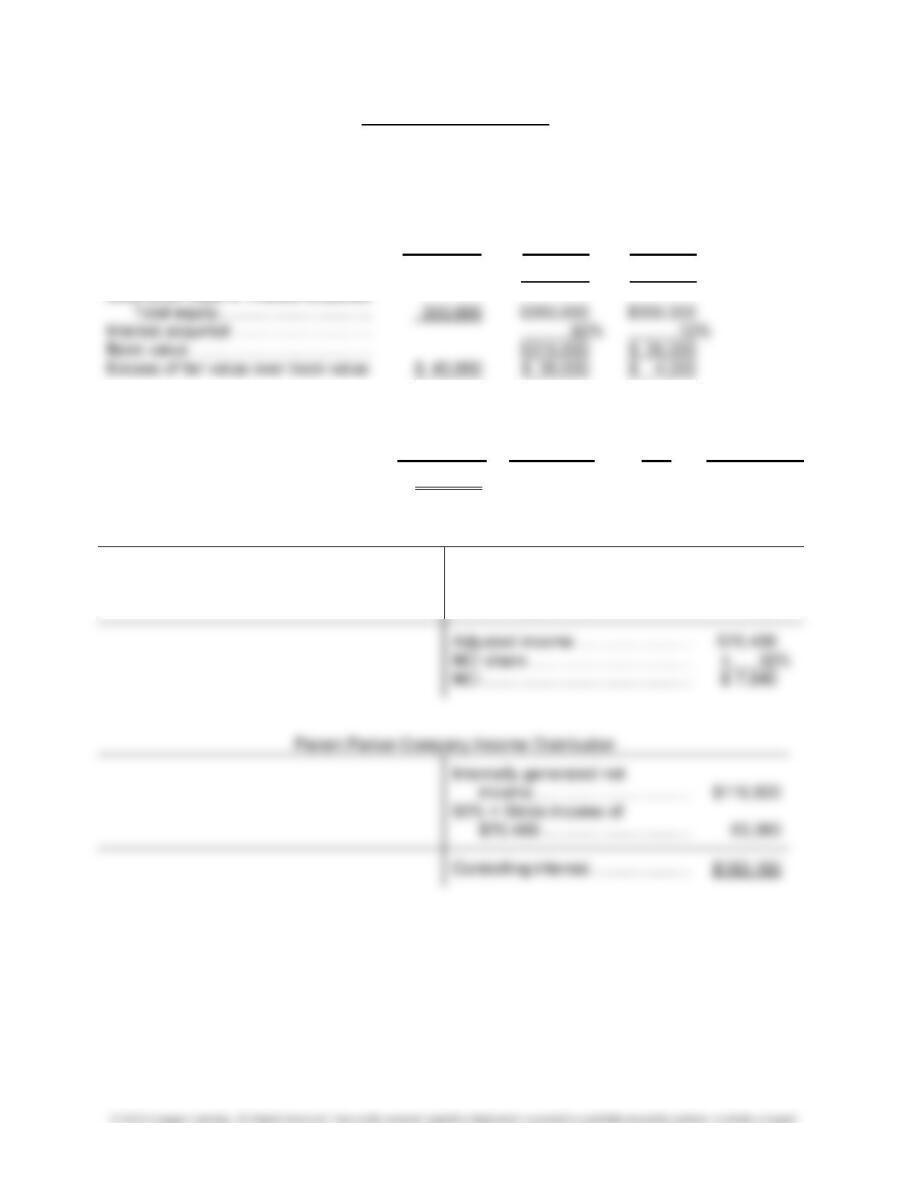

PROBLEM 5-3

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………………… $2,125,000 $1,700,000 $ 425,000

Less book value of interest acquired:

Total equity……………………………. 1,875,000 $1,875,000 $1,875,000

Problem 5-3, Continued

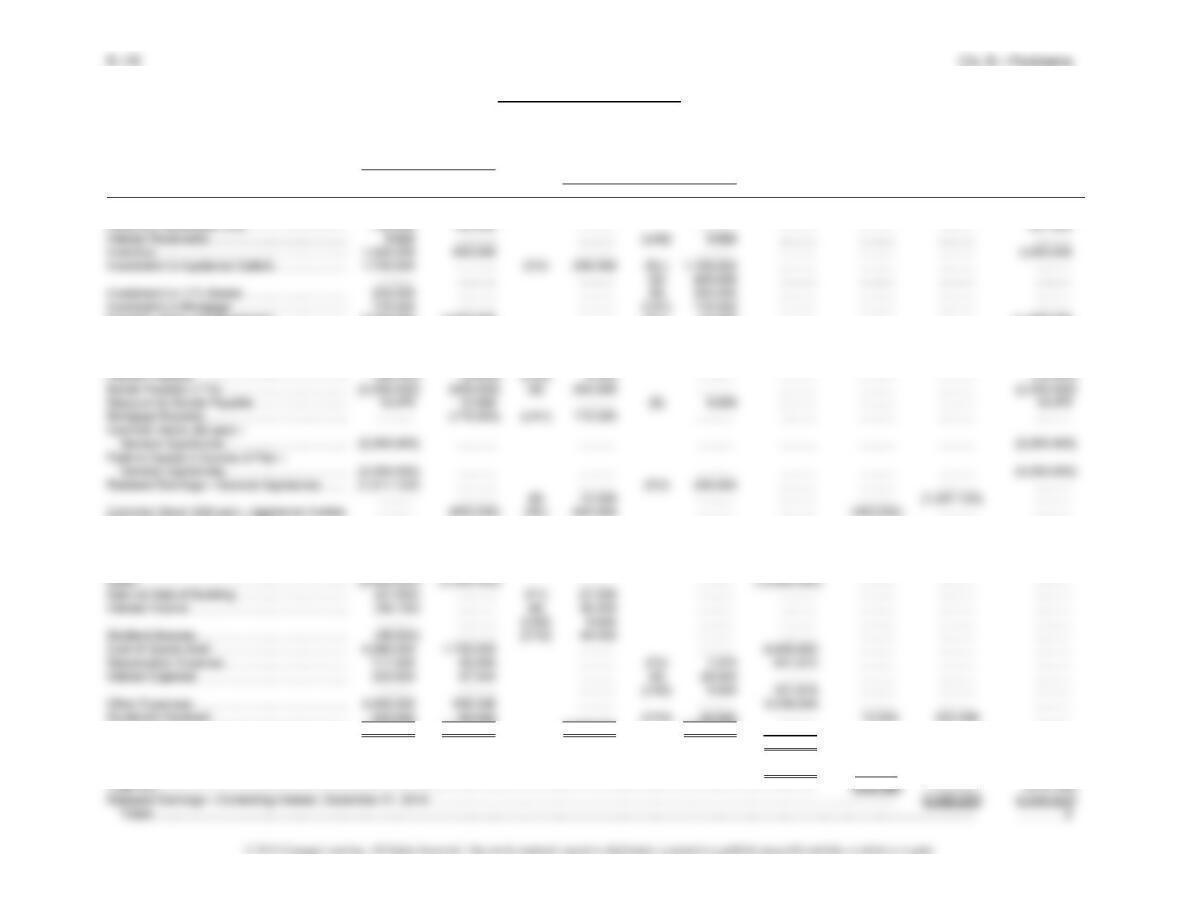

General Appliances and Subsidiary Appliance Outlets

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2016

Trial Balance

Eliminations Consolidated Controlling Consolidated

General Appliance and Adjustments

Income Retained Balance

Appliances Outlets Dr. Cr. Statement NCI Earnings Sheet

Cash ………………………………………………………. 404,486 72,625 ……….. ……….. ……….. ……….. ……….. 477,111

Property, Plant, and Equipment …………………. 9,000,000 2,950,000 ……….. (F1) 27,500 ……….. ……….. ……….. 11,922,500

Accumulated Depreciation ………………………… (1,695,000) (940,000) (F2) 1,375 ……….. ……….. …….…. ……….. (2,633,625)

Goodwill …………………………………………………. ……….. ………… (D) 250,000 ……….. ..……… ……….. ……….. 250,000

Accounts Payable ……………………………………. (670,000) (80,000) ……….. ……….. ……….. .………. ……….. (750,000)

Paid-In Capital in Excess of Par—

Appliance Outlets …………………………………. ……….. (625,000) (EL) 500,000 ……….. ……….. (125,000) ……….. ………..

Retained Earnings—Appliance Outlets ……….. ……….. (770,000) (EL) 616,000 (NCI) 50,000 ……….. ……….. ……….. ………..

……….. ………… (B) 2,500 ……….. ……….. (201,500) ……….. ………..

0

0 2,822,125 2,822,125 ……….. ……….. ……….. ………..

Consolidated Net Income ………………………………………………………………………………………….………………………………………. (1,560,000) ……….. ……….. ………..

To NCI (see distribution schedule) ……………………………………………………………………………………………………………….…. 40,600 (40,600) ……….. ………..

To Controlling Interest (see distribution schedule)…………………………………………………………………………………………….. 1,519,400 ………… (1,519,400) ………..

Problem 5-3, Concluded

Eliminations and Adjustments:

(CV) Convert investment to equity, 80% × ($770,000 – $450,000) = $256,000.

(CY2) Eliminate dividend income.

(EL) Eliminate 80% of the subsidiary equity balances.

(D)/(NCI) Distribute the excess and the NCI adjustment according to the determination and dis-

tribution of excess schedule.

(F1) Eliminate the intercompany gain on sale of building.

(F2) Reduce depreciation expense on the building for one-half year, ($27,500 ÷ 10) × 1/2.

(LN1) Eliminate the intercompany mortgage.

(LN2) Eliminate the intercompany interest payable and receivable on mortgage. Eliminate

the intercompany interest revenue and expense on mortgage, 1/2 × 11% × $175,000

= $9,625.

Subsidiary Appliance Outlets Income Distribution

Internally generated net

income …………………………….. $200,000

Interest adjustment

($29,000 – $26,000) ………….. 3,000

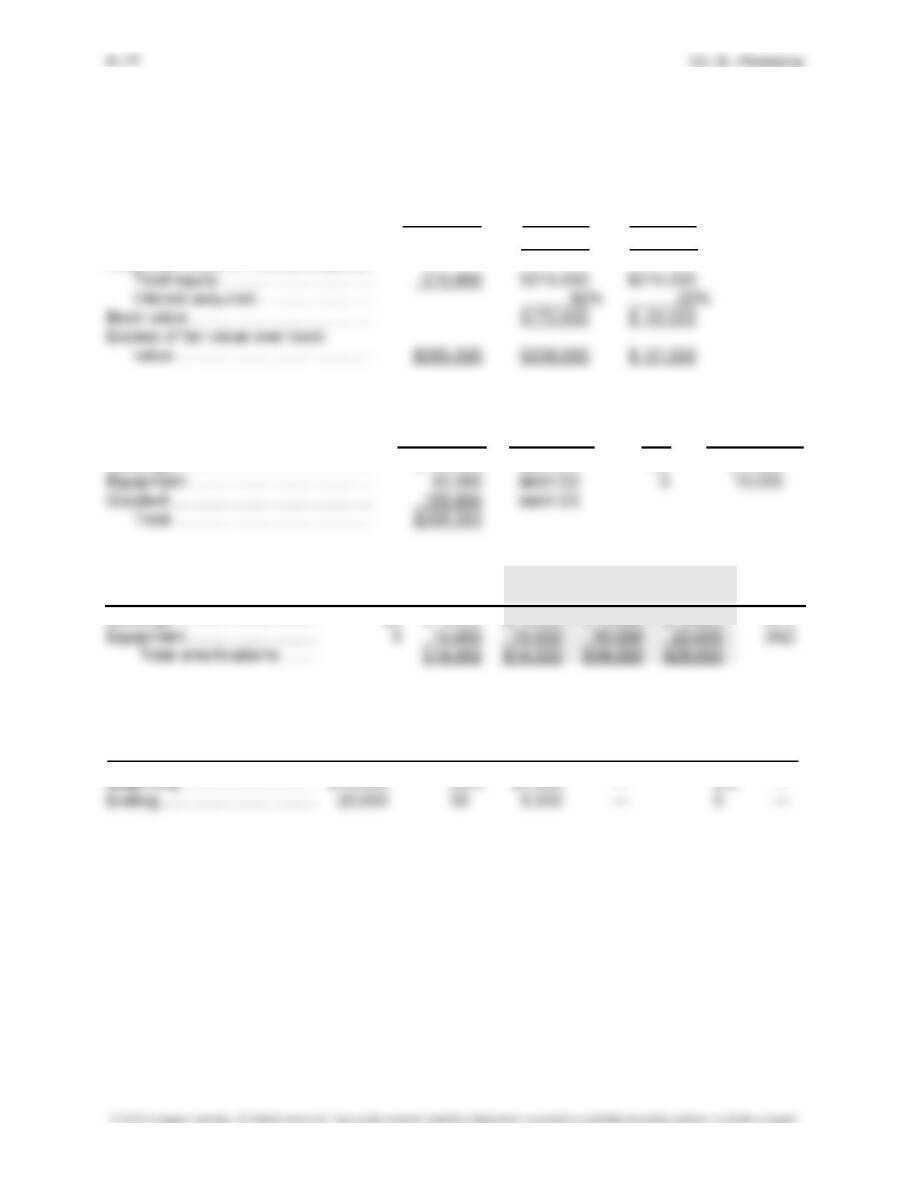

PROBLEM 5-4

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………………… $500,000 $400,000 $100,000

Less book value of interest acquired:

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Buildings ……………………………………. $ 80,000 debit D1 20 $ 4,000

Account Adjustments Annual Current Prior

to Be Amortized Life Amount Year Years Total Key

Buildings …………………………. 20 $ 4,000 $ 4,000 $ 4,000 $ 8,000 (A1)

Intercompany Inventory Profit Deferral

Parent Parent Parent Sub Sub Sub

Amount Percent Profit Amount Percent Profit

Problem 5-4, Continued

Subsidiary Stark Company Income Distribution

Loss on bond retirement …………… $ 6,739 Internally generated net

Buildings depreciation ………………. 4,000 income ………………………………. $24,672

Equipment depreciation ……………. 10,000 Interest adjustment—bonds ………. 1,123

Parent Pontiac Company Income Distribution

Ending inventory profit ……………… $6,000 Internally generated net

income ………………………………. $42,845

Proof for Bond Elimination

Loss remaining at year-end:

Investment in bonds at December 31, 2015 ………………………… $103,975

Carrying value at December 31, 2015 ………………………………… 98,359 $5,616

5–19 Ch. 5—Problems

Problem 5-4, Continued

Pontiac Company and Subsidiary Stark Company

Worksheet for Consolidated Financial Statements

For Year Ended December 31, 2015

Eliminations Consolidated Controlling Consolidated

Trial Balance

and Adjustments Income Retained Balance

Pontiac Stark Dr. Cr. Statement NCI Earnings Sheet

Cash ………………………………………………………. 17,870 32,031 ……….. ……….. ……….. ……….. ……….. 49,901

……….. ………… ……….. (EL) 196,000 ……….. ……….. ……….. ………..

……….. ………… ……….. (D) 228,000 ……….. ……….. ……….. ………..

Investment in Stark Bonds ………………………… 103,975 ………… ……….. (B) 103,975 ……….. …..…… ……….. ………..

Buildings ………………………………………………… 500,000 250,000 (D1) 80,000 ……….. ……….. ……….. ……….. 830,000

Accumulated Depreciation ………………………… (300,000) (70,000) ……….. (A1) 8,000 ……….. ……….. ……….. (378,000)

Equipment ………………………………………………. 200,000 120,000 (D2) 50,000 ……….. ……….. ..……… ……….. 370,000

Retained Earnings—Pontiac ……………………… (400,000) ………… (A1–A2) 11,200 ……….. ……….. ……….. ……….. ………..

……….. ………… (BI) 4,500 ……….. ……….. ……….. (384,300) ………..

Loss (Gain) on Bond Retirement ……….. ………… (B) 6,739 ……….. 6,739 ……….. ……….. ….…….

Sales ……………………………………………………… (600,000) (220,000) (IS) 50,000 ……….. (770,000) ……….. ……….. ………..

Totals …………………………………………………. 0 0 721,182 721,182 ……….. ……….. ……….. ………..

Consolidated Net Income ………………………………………………………………………………………….………………………………………. (46,401) ……….. ……….. ………..

To NCI (see distribution schedule) ……………………………………………………………………………………………………………….…. 1,011 (1,011) ……….. ………..

To Controlling Interest (see distribution schedule)…………………………………………………………………………………………….. 45,390 ……….. (45,390) ………..

Total NCI ………………………………………………………………………………………………………………………………………………………………………………. (102,211) ……….. (102,211)

Problem 5-4, Concluded

Eliminations and Adjustments:

(CY1) Current-year subsidiary income.

(CY2) Current-year dividend.

(EL) Eliminate controlling interest in subsidiary equity.

(D)/(NCI) Distribute excess and NCI adjustment.

PROBLEM 5-5

Determination and Distribution of Excess Schedule

Company Parent NCI

Implied Price Value

Fair Value (80%) (20%)

Fair value of subsidiary ………………… $500,000 $400,000 $100,000

Less book value of interest acquired:

Adjustment of identifiable accounts:

Worksheet Amortization

Adjustment Key Life per Year

Buildings ……………………………………. $ 80,000 debit D1 20 $ 4,000

Equipment ………………………………….. 50,000 debit D2 5 10,000

Account Adjustments Annual Current Prior

to Be Amortized Life Amount Year Years Total Key

Buildings …………………………. 20 $ 4,000 $ 4,000 $ 8,000 $12,000 (A1)