CHAPTER 5

SOLUTIONS TO EXERCISES—SET B

EXERCISE 5-1B

1. False. Measuring net income for a merchandiser is conceptually the

same as measuring net income for a service company.

2. True.

3. False. For a merchandiser, the primary source of revenues is the sale

of inventory.

EXERCISE 5-2B

(a) (1) April 5 Inventory ……………………………………. 25,000

Accounts Payable ………………… 25,000

(b) May 4 Accounts Payable ………………………………. 22,000

Cash …………………………………………… 22,000

EXERCISE 5-3B

Sept. 6 Inventory (70 X $20) …………………………………. 1,400

Cash ………………………………………………… 1,400

9 Inventory ………………………………………………… 70

Cash ………………………………………………… 70

14 Sales Returns and Allowances ………………… 34

Accounts Receivable ……………………….. 34

Inventory ……………………………………………….. 21

Cost of Goods Sold ………………………….. 21

EXERCISE 5-4B

(a) June 10 Inventory …………………………………………. 12,000

Accounts Payable ……………………… 12,000

11 Inventory …………………………………………. 500

Cash …………………………………………. 500

EXERCISE 5-4B (Continued)

(b) June 10 Accounts Receivable ………………………. 12,000

Sales Revenue …………………………. 12,000

Cost of Goods Sold …………………………. 7,200

Inventory ………………………………….. 7,200

EXERCISE 5-5B

(a) 1. Dec. 3 Accounts Receivable …………………. 400,000

Sales ………………………………….. 400,000

Cost of Goods Sold …………………… 240,000

Inventory ……………………………. 240,000

EXERCISE 5-6B

(a) GRIMMETT COMPANY

Income Statement (Partial)

For the Year Ended October 31, 2014

Sales revenues

Sales revenue …………………………………………. $940,000

(b) (1) Oct. 31 Sales Revenue ……………………….. 940,000

Income Summary …………….. 940,000

EXERCISE 5-7B

(a) Cost of Goods Sold ………………………………………. 1,200

Inventory ……………………………………………….. 1,200

(b) Sales Revenue ……………………………………………… 165,000

Income Summary …………………………………… 165,000

EXERCISE 5-8B

(a) Cost of Goods Sold ………………………………………. 1,400

Inventory ……………………………………………….. 1,400

(b) Sales Revenue ……………………………………………… 550,000

Income Summary …………………………………… 550,000

Income Summary ………………………………………….. 520,400

Cost of Goods Sold ($332,000 + $1,400) …… 333,400

EXERCISE 5-9B

(a) OAKLEY COMPANY

Income Statement

For the Month Ended March 31, 2017

Sales revenues

Sales revenue ………………………………………… $360,000

Less: Sales returns and allowances ……….. $13,000

Sales discounts …………………………... 8,000 21,000

EXERCISE 5-10B

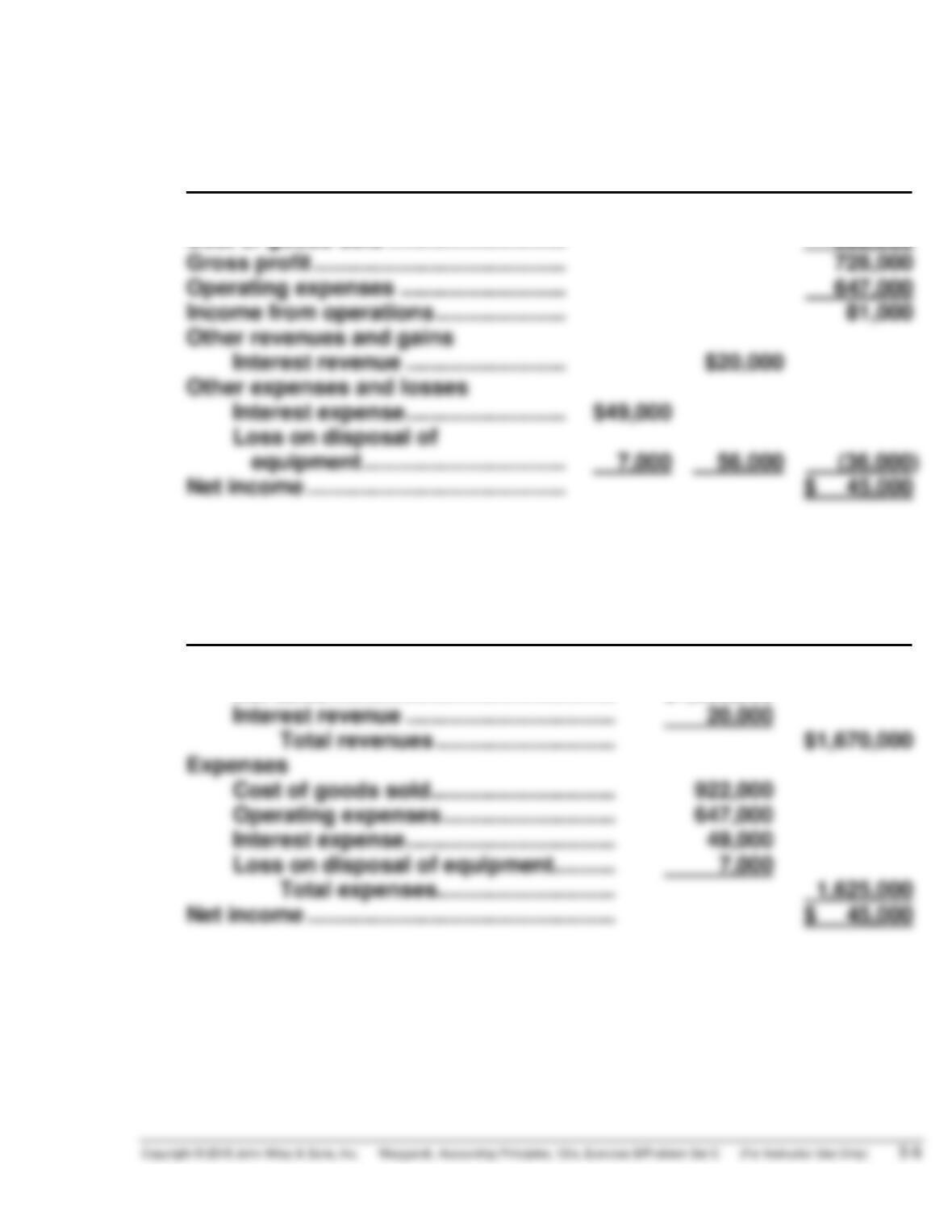

(a) KRUEGER COMPANY

Income Statement

For the Year Ended December 31, 2017

Net sales ………………………………………. $1,650,000

Cost of goods sold ……………………….. 922,000

Other revenues and gains

Interest revenue …………………….. $20,000

Other expenses and losses

Interest expense …………………….. $49,000

(b) KRUEGER COMPANY

Income Statement

For the Year Ended December 31, 2017

Revenues

Net sales ………………………………………. $1,650,000

Interest revenue ……………………………. 20,000

Total revenues ……………………….. $1,670,000

Expenses

EXERCISE 5-11B

1. Sales Returns and Allowances …………………………………. 205

Sales Revenue ………………………………………………….. 205

3. Sales Discounts ………………………………………………………. 130

Sales Returns and Allowances ………………………….. 130

EXERCISE 5-12B

(a) $1,000,000 – $670,000 = $330,000.

(b) $330,000/$1,000,000 = 33%. The gross profit rate is generally considered

to be more useful than the gross profit amount. The rate expresses a

more meaningful (qualitative) relationship between net sales and gross

(c) Income from operations is $130,000 ($330,000 – $200,000), and net income

is $120,000 ($130,000 – $10,000).

(d) The amount shown for net income is the same in a multiple-step income

(e) Inventory is reported as a current asset immediately below accounts

receivable.

EXERCISE 5-13B

(a) (*missing amount)

a. Sales revenue …………………………………………………….. $ 210,000)

b. Net sales ……………………………………………………………. $ 200,000)

c. Gross profit ………………………………………………………… $ 80,000)

Operating expenses ……………………………………………. (50,000)

*Net income …………………………………………………………. $ 30,000)

e. Net sales ……………………………………………………………. $ 95,000)

*Cost of goods sold ……………………………………………… 53,000)

Gross profit ………………………………………………………… $ 42,000)

)

(b) Doty Company

Gross profit ÷ Net sales = $80,000 ÷ $200,000 = 40%

EXERCISE 5-14B

(*Missing amount)

(a) Sales revenue ……………………………………………………………. $ 90,000

Sales returns and allowances ……………………………………… 2,000*

Net sales ……………………………………………………….…………… $ 88,000

(c) and (d)

Gross profit ……………………………………………………………….. $ 32,000

Operating expenses …………………………………………………… 15,000

(e) Sales revenue ……………………………………………………………. $ 98,000*

Sales returns and allowances ……………………………………… 5,000

Net sales ……………………………………………………….…………… $ 93,000

(g) and (h)

Gross profit ……………………………………………………………….. $ 33,000

(i) Sales revenue ……………………………………………………………. $127,000

Sales returns and allowances ……………………………………… 12,000

Net sales ……………………………………………………….…………… $115,000*

EXERCISE 5-14B (Continued)

(k) and (l)

Gross profit ……………………………………………………………….. $ 31,000

*EXERCISE 5-15B

Accounts

Adjusted

Trial Balance

Income

Statement

Balance

Sheet

Debit

Credit

Debit

Credit

Debit

Credit

Cash

11,000

11,000

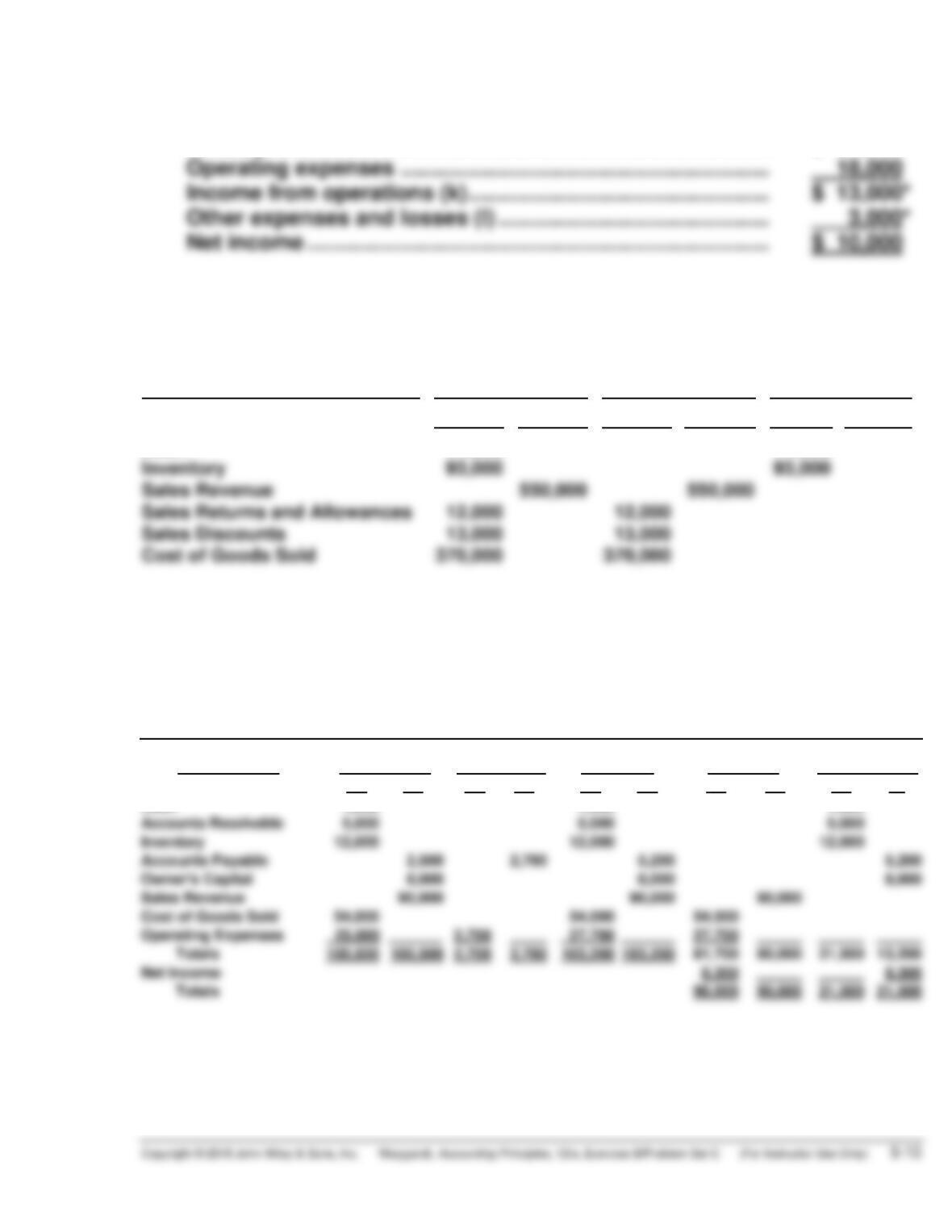

*EXERCISE 5-16B

LIPPERT COMPANY

Worksheet

For the Month Ended June 30, 2017

Account Titles

Trial Balance

Adjustments

Adj. Trial

Balance

Income

Statement

Balance Sheet

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Cash

4,500

4,500

4,500

Accounts Receivable

5,000

5,000

5,000

Inventory

12,000

12,000

12,000

Accounts Payable

2,500

2,700

5,200

8,000

Sales Revenue

90,000

90,000

90,000

Cost of Goods Sold

54,000

54,000

54,000

Operating Expenses

25,000

2,700

27,700

27,700

Totals

100,500

100,500

2,700

2,700

103,200

103,200

81,700

90,000

21,500

13,200

Net Income

8,300

Totals

90,000

90,000

21,500

21,500

*EXERCISE 5-17B

Inventory, September 1, 2016 ………………………………… $ 35,000

Purchases ……………………………………………………………. $300,000

*EXERCISE 5-18B

(a) Sales revenue ………………………………… $650,000

Less: Sales returns and allowances …. $ 12,000

Sales discounts …………………… 7,000 19,000

Net sales ……………………………………….. 631,000

Cost of goods sold

Inventory, January 1 ………………….. 35,000

(b) Gross profit $252,000 – Operating expenses = Net income $120,000.

*EXERCISE 5-19B

(a) $2,050 ($2,100 – $ 50)

(g) $ 3,250 ($ 150 + $ 3,100)

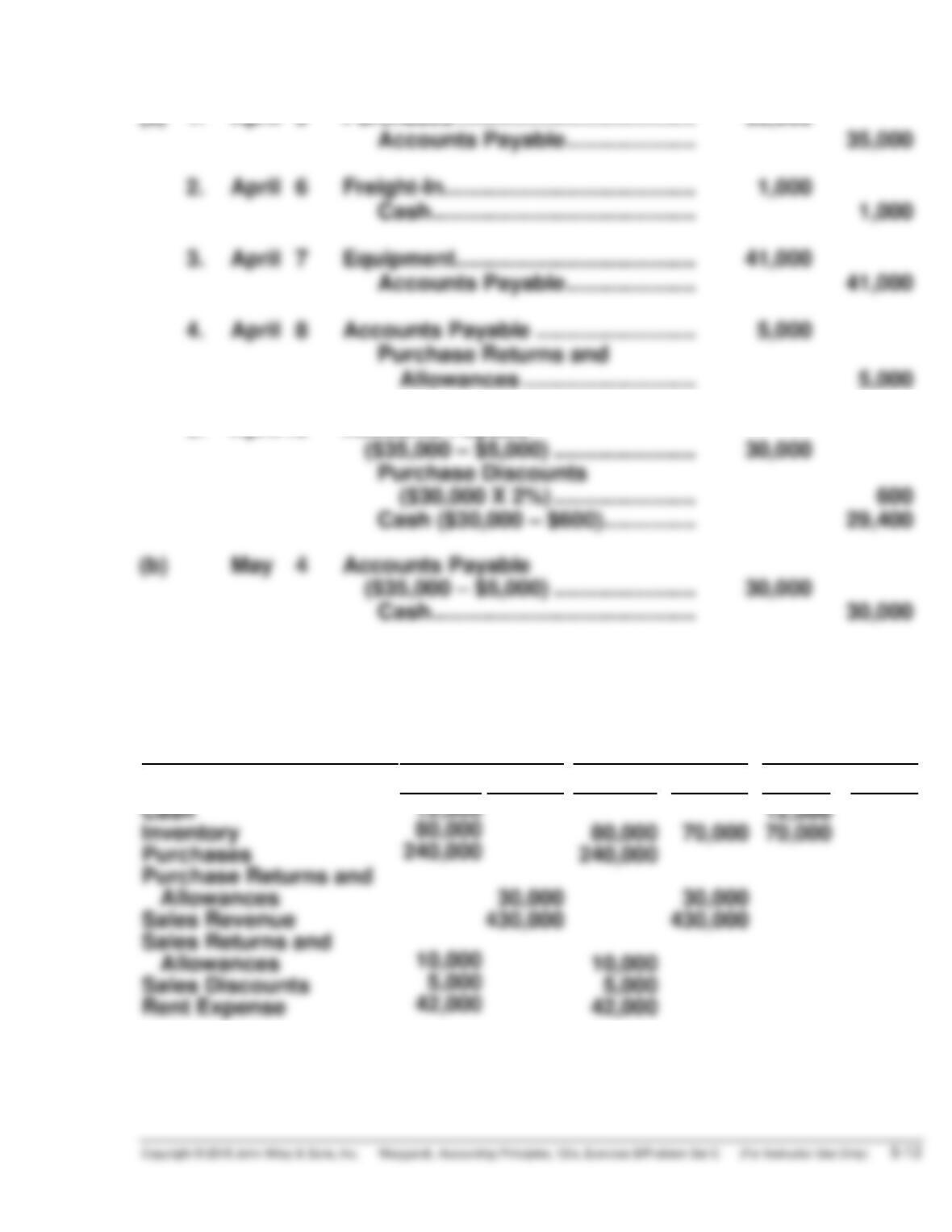

*EXERCISE 5-20B

(a) 1. April 5 Purchases ………………………………… 30,000

Accounts Payable ………………… 30,000

5. April 15 Accounts Payable

($30,000 – $3,000) ………………….. 27,000

Purchase Discounts

*EXERCISE 5-21B

(a) 1. April 5 Purchases ………………………………… 35,000

Accounts Payable ………………… 35,000

2. April 6 Freight-In………………………………….. 1,000

Cash……………………………………. 1,000

5. April 15 Accounts Payable

($35,000 – $5,000) ………………….. 30,000

Purchase Discounts

*EXERCISE 5-22B

Accounts

Adjusted

Trial Balance

Income

Statement

Balance

Sheet

Debit

Credit

Debit

Credit

Debit

Credit

Cash

12,000

12,000

SOLUTIONS TO PROBLEMS—SET C

PROBLEM 5-1C

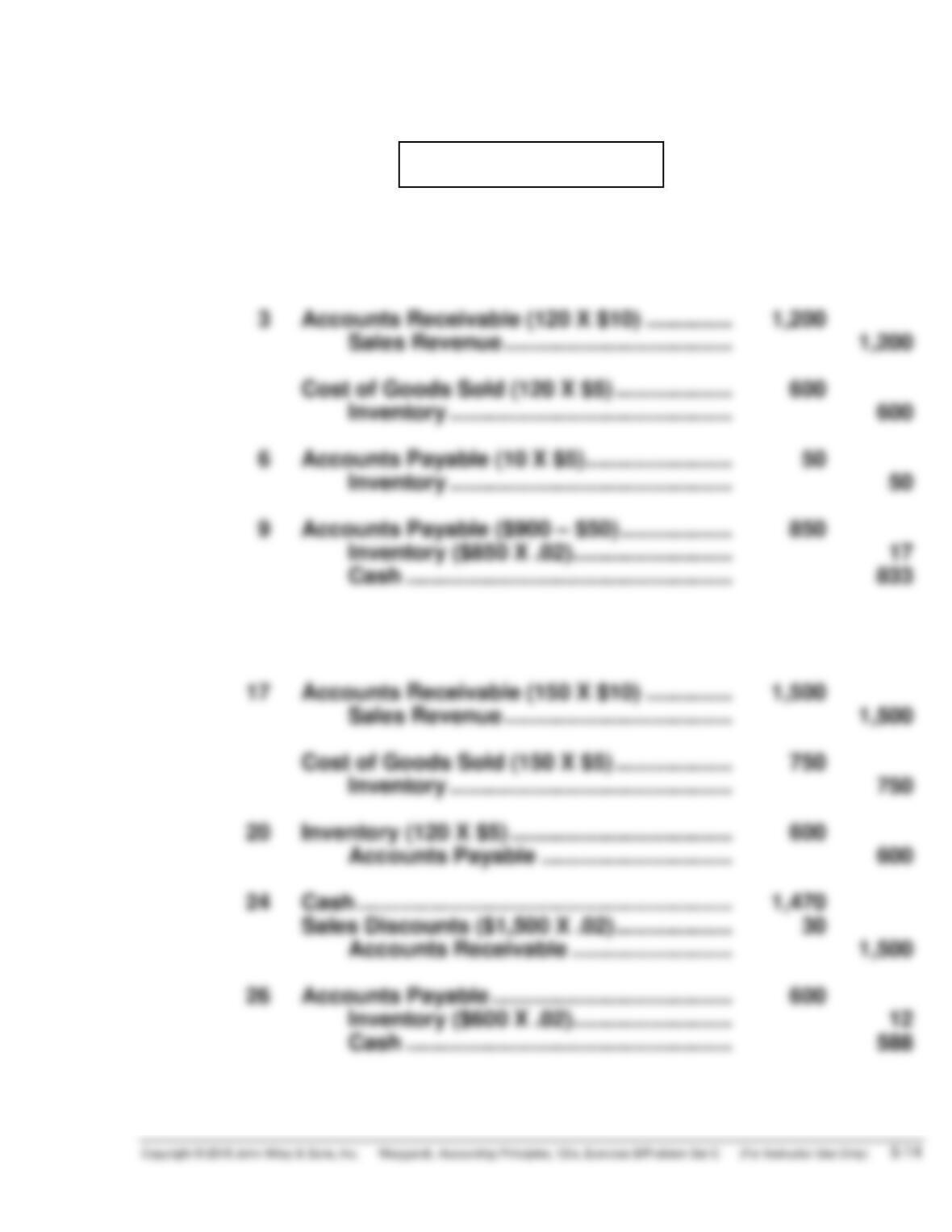

(a) June 1 Inventory (180 X $5) ……………………………… 900

Accounts Payable …………………………. 900

3 Accounts Receivable (120 X $10) ………….. 1,200

Sales Revenue ………………………………. 1,200

15 Cash ……………………………………………………. 1,200

Accounts Receivable …………………….. 1,200

17 Accounts Receivable (150 X $10) ………….. 1,500

Sales Revenue ………………………………. 1,500

26 Accounts Payable ………………………………… 600

Inventory ($600 X .02) …………………….. 12

Cash …………………………………………….. 588

PROBLEM 5-1C (Continued)

June 28 Accounts Receivable (110 X $10) ………….. 1,100

Sales Revenue ………………………………. 1,100

PROBLEM 5-2C

(a)

General Journal J1

Date

Account Titles and Explanation

Ref.

Debit

Credit

May 1

Inventory ……………………………………

Accounts Payable ………………..

120

201

9,000

9,000

5

Accounts Payable ……………………….

Inventory …………………………..…

201

120

600

600

9

Cash ($4,500 – $50) ……………………..

Sales Discounts ($4,500 X 1%) …….

Accounts Receivable ……………

101

414

112

4,455

45

5,000

10

Accounts Payable ($9,000 – $600) ..

Inventory ($8,400 X 2%) ………..

Cash ……………………………………

201

120

101

8,400

168

8,232

11

Supplies ……………………………………..

Cash ……………………………………

126

101

900

900

12

Inventory ……………………………………

Cash ……………………………………

120

101

2,700

2,700

15

Cash …………………………………………..

Inventory …………………………..…

101

120

230

230

17

Inventory ……………………………………

120

2,500

PROBLEM 5-2C (Continued)

General Journal J1

Date

Account Titles and Explanation

Ref.

Debit

Credit

May 24

Cash …………………………………………….

Sales Revenue ……………………….

101

401

6,200

6,200

27

Accounts Payable …………………………

Inventory ($3,000 X 2%) …………..

Cash …………………………..…………

201

120

101

3,000

60

2,940

29

31

Accounts Receivable …………………….

112

Sales Returns and Allowances ………

Cash …………………………..…………

412

101

100

100