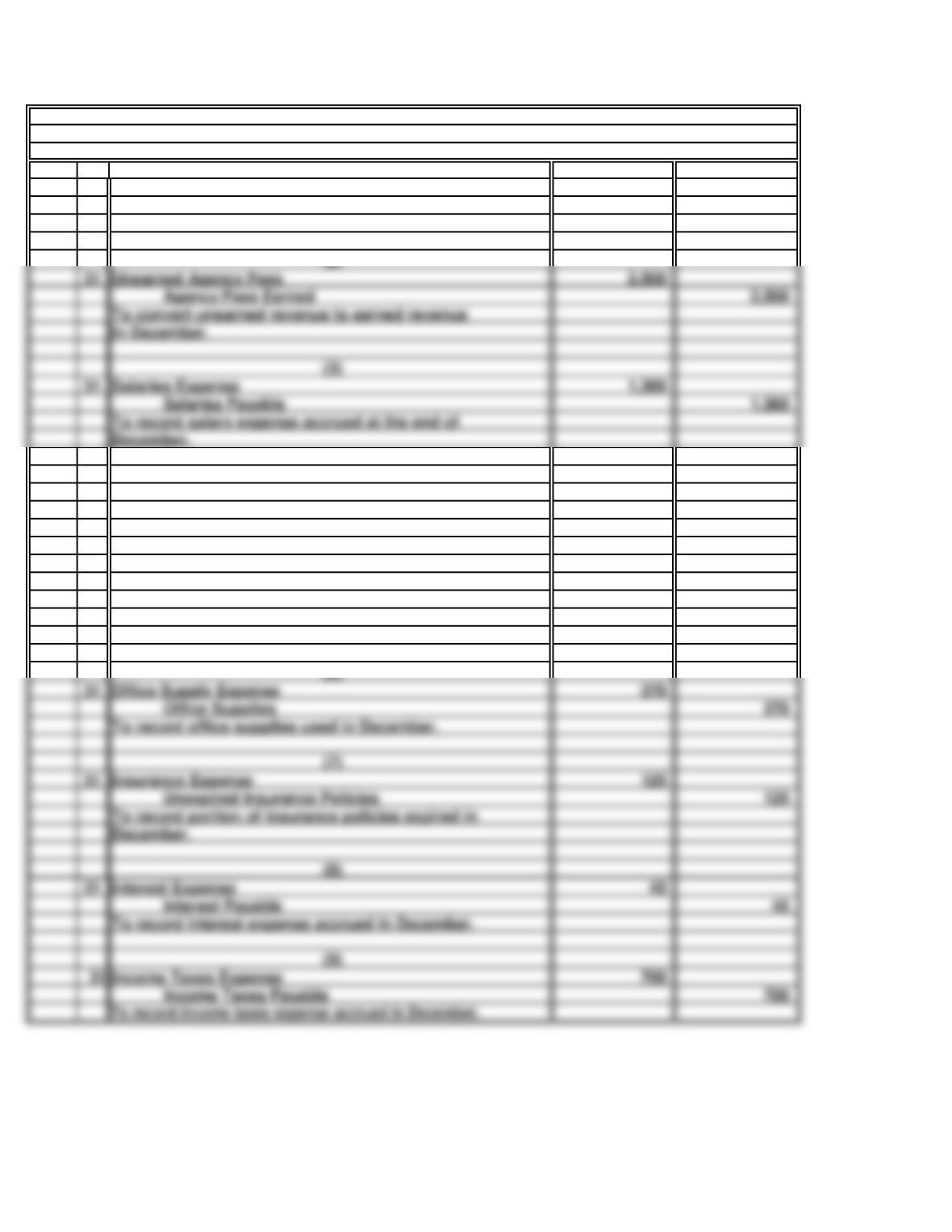

Dec. 31 250

Accumulated Depreciation: Office Equip. 250

31 600

Prepaid Rent 600

31 3,000

Agency Fees Earned 3,000

31 370

Office Supplies 370

31 125

Unexpired Insurance Policies 125

31 45

Income Taxes Payable 700

(9)

Income Taxes Expense

Insurance Expense

To record interest expense accrued in December.

December.

Interest Expense

(8)

(7)

To record portion of insurance policies expired in

(6)

To record office supplies used in December.

Office Supply Expense

PROBLEM 5.6B

TOUCHTONE TALENT AGENCY

70 Minutes, Strong

December 31, Current Year

To record depreciation of office equipment in December.

(4)

To record revenue accrued at the end of

To record prepaid rent expired in December.

Fees Receivable

Rent Expense

(5)

December.

TOUCHTONE TALENT AGENCY

Depreciation Expense: Office Equipment

General Journal

(1)

(2)

31 2,500

Agency Fees Earned 2,500

31 1,360

Salaries Payable 1,360

To convert unearned revenue to earned revenue

Unearned Agency Fees

December.

(3)

in December.

To record salary expense accrued at the end of

Salaries Expense

a.

1.

Computations for each of the adjusting journal entries:

$15,000 (office equipment per trial balance)/60 months = $250 per month.

PROBLEM 5.6B

TOUCHTONE TALENT AGENCY (continued)

(continued)

2.

3.

4.

5.

6.

7.

8.

9.

Salaries payable of $1,360 for salaries accrued at the end of December.

Unearned agency fees reduced by the $2,500 amount earned in December.

$1,800 initial prepayment/3 mo. = $600 rent expense incurred in December.

Fees receivable increased by the $3,000 of accrued revenue in December.

$3,900 total expense – $3,200 (per trial balance) = $700 accrued in December.

$6,000 (note payable per trial balance) x 9% x 1/12 = $45 int. expense per mo.

$750 initial prepayment/6 mo. = $125 ins. expense incurred in December.

$900 (supplies per trial balance) – $530 (at 12/31) = $370 used in December.

14,950$

38,300

600

250

530

15,000

12,250$

PROBLEM 5.6B

TOUCHTONE TALENT AGENCY (continued)

Unexpired insurance policies

Office supplies

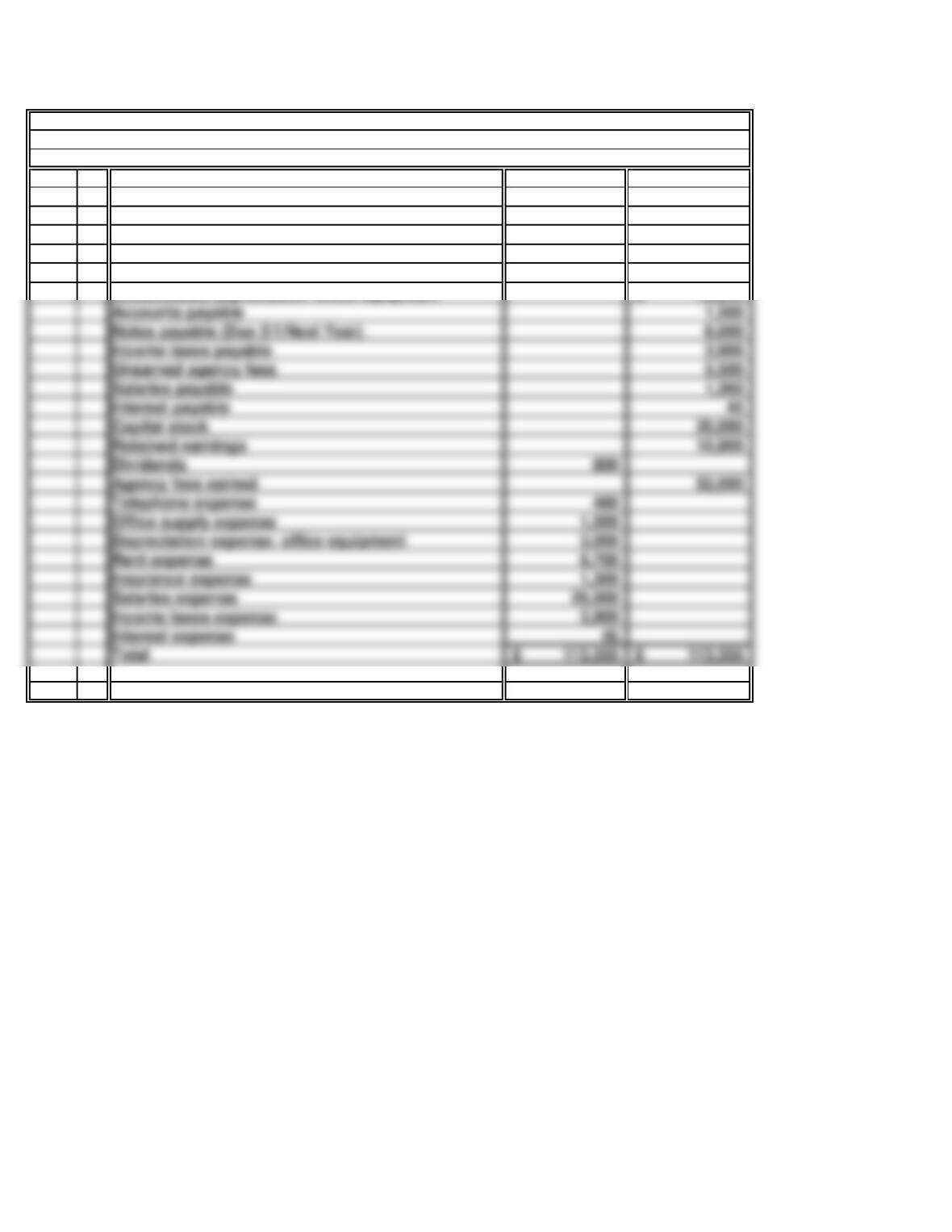

TOUCHTONE TALENT AGENCY

December 31, Current Year

Adjusted Trial Balance

Fees receivable

a. (cont’d.)

Office equipment

Cash

Prepaid rent

Accumulated depreciation: office equipment

Interest payable

Capital stock

Accounts payable

Income taxes payable

Notes payable (Due 3/1/Next Year)

Unearned agency fees

Salaries payable

b.

52,000$

480$

1,500

10,800$

Add: Net income

Retained earnings (12/31/Current Year)

Less: Dividends

Agency fees earned

Income Statement

Telephone expense

PROBLEM 5.6B

TOUCHTONE TALENT AGENCY (continued)

Revenues:

TOUCHTONE TALENT AGENCY

For the Year Ended December 31, Current Year

Expenses:

Office supply expense

Retained earnings (1/1/Current Year)

TOUCHTONE TALENT AGENCY

For the Year Ended December 31, Current Year

Statement of Retained Earnings

3,000

6,700

1,300

Salaries expense

Insurance expense

Income before taxes

Net income

Depreciation expense: office equipment

Rent expense

Income taxes expense

Interest expense

b. (cont’d.)

Assets

14,950$

38,300

1,500$

6,000

3,900

5,500

1,360

18,305$

20,000$

19,075

39,075$

57,380$

Total liabilities and stockholders’ equity

Interest payable

Capital stock

Retained earnings

Stockholders’ Equity

Total liabilities

Total stockholders’ equity

Salaries payable

Unearned agency fees

Income taxes payable

Note payable (Due 3/1/Next Year)

Liabilities

PROBLEM 5.6B

TOUCHTONE TALENT AGENCY

Accounts payable

TOUCHTONE TALENT AGENCY (continued)

Fees receivable

Balance Sheet

Cash

December 31, Current Year

Unexpired insurance policies

Office supplies

Prepaid rent

Less: Accumulated depreciation: office equipment

Office equipment

Total assets

c.

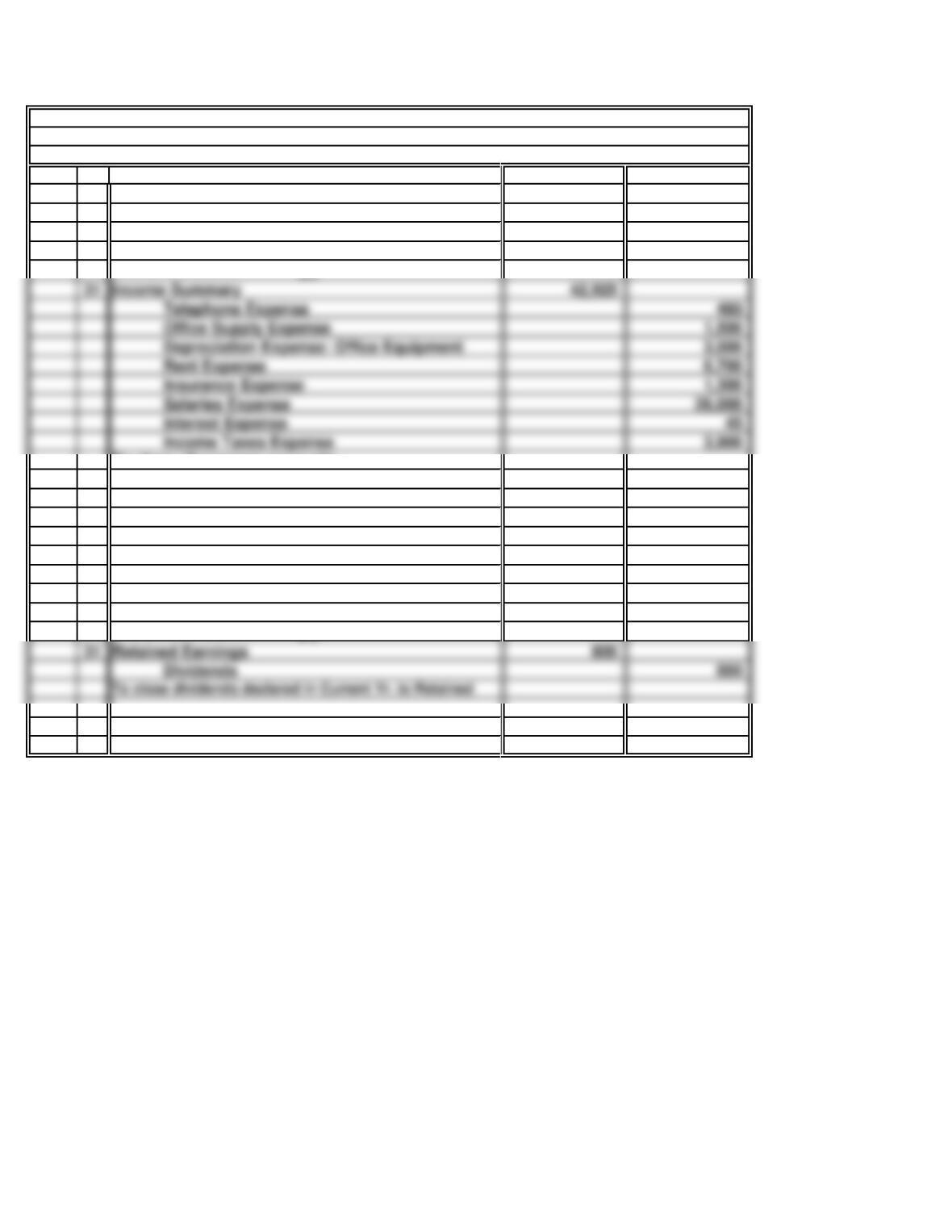

Dec. 31 52,000

Income Summary 52,000

31 9,075

Retained Earnings 9,075

Retained Earnings

PROBLEM 5.6B

TOUCHTONE TALENT AGENCY

December 31, Current Year

(1)

General Journal

TOUCHTONE TALENT AGENCY (continued)

Agency Fees Earned

To close Agency Fees Earned.

(2)

Retained Earnings account ($52,000 -$42,925 =

Income Summary

(3)

To close all expense accounts.

To transfer net income earned in Current Yr. to the

$9,075).

(4)

Telephone Expense 480

Office Supply Expense 1,500

Depreciation Expense: Office Equipment 3,000

Rent Expense 6,700

Salaries Expense 26,000

Interest Expense 45

Income Taxes Expense 3,900

Income Summary

d.

14,950$

38,300

600

3,900

5,500

1,360

45

Capital stock

Retained earnings

e.

12,250$

Divided by monthly depreciation expense

Total months agency has been in operation

Salaries payable

Accumulated depr.: office equipment (12/31/Current Yr.)

Interest payable

Fees receivable

PROBLEM 5.6B

TOUCHTONE TALENT AGENCY (continued)

TOUCHTONE TALENT AGENCY

December 31, Current Year

After-Closing Trial Balance

Cash

Prepaid rent

Unearned agency payable

Income taxes payable

250

530

15,000

6,000

Note payable (Due 3/1/Next Year)

Accounts payable

Unexpired insurance policies

Office supplies

Office equipment

Accumulated depreciation: office equipment

f.

6,700$

1,200 (at $600/mo.)

5,500$

g.

1,300$

500

PROBLEM 5.6B

TOUCHTONE TALENT AGENCY (concluded)

Rent expense incurred in Current Year

Total rent expense incurred in January through October

Less: Total rent expense for November and December

through December (at $125 per month)

Less: Total insurance expense for September

Insurance expense incurred in Current Year

Monthly increase starting in November ($600-$550)

Monthly rent expense in January through October

50 Minutes, Strong

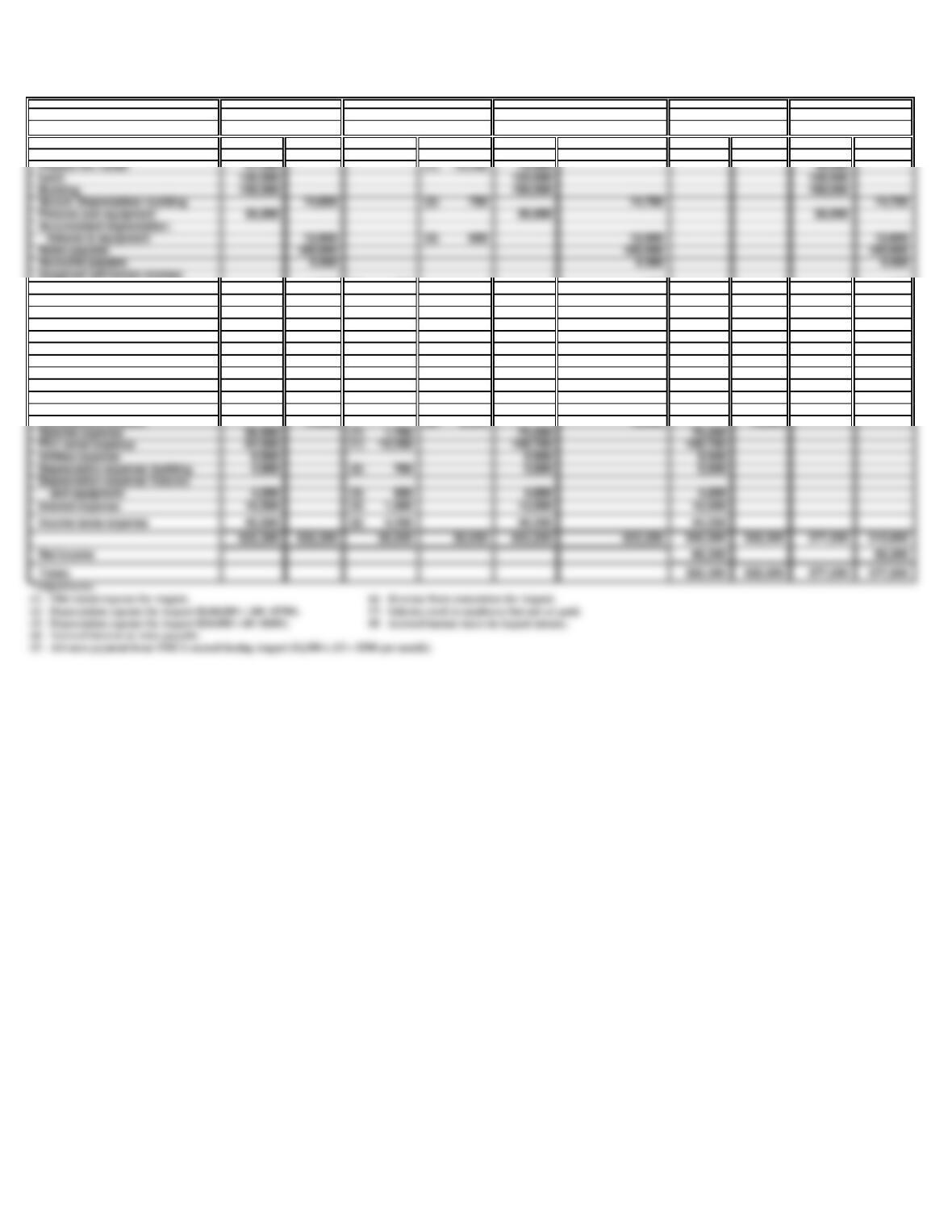

Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr.

Balance sheet accounts:

Cash 20,000 20,000 20,000

Unearned admission revenue

(YMCA) 1,000

(5)

500 500 500

Income taxes payable 4,740 (8) 4,200 8,940 8,940

Capital stock 40,000 40,000 40,000

Retained earnings 46,610 46,610 46,610

Dividends 15,000 15,000 15,000

Interest payable (4) 1,500 1,500 1,500

Concessions revenue receivable

(6)

2,250 2,250 2,250

Salaries payable (7) 1,700 1,700 1,700

Income statement accounts:

Admissions revenue 305,200 (5) 500 305,700 305,700

Concessions revenue 14,350 (6) 2,250 16,600 16,600

Salaries expense 68,500

(7)

1,700 70,200 70,200

Film rental expense 94,500

(1)

Utilities expense 9,500 9,500 9,500

Depreciation expense: building 4,900

(2)

700 5,600 5,600

Depreciation expense: fixtures

(3)

600 4,800 4,800

Interest expense 10,500

(4)

1,500 12,000 12,000

Trial Balance

Adjustments *

Adjusted Trial Balance

WORKSHEET

For the Month Ended August 31, Current Year

CAMPUS THEATER

Income Statement

Balance Sheet

PROBLEM 5.7B

CAMPUS THEATER

Prepaid film rental 31,200 (1) 15,200 16,000 16,000

Land 120,000 120,000 120,000

Building 168,000 168,000 168,000

Accum. Depreciation: building 14,000 (2) 700 14,700 14,700

Fixtures and equipment 36,000 36,000 36,000

Accumulated depreciation:

Notes payable 180,000 180,000 180,000

Accounts payable 4,400 4,400 4,400

15 Minutes, Medium

7.9%

c.

PROBLEM 5.8B

THE GAP, INC.

a.

$1.3 billion ÷ $16.4 billion =

Net income percentage: Net Income/Total Revenue

The company was profitable, given its net income of $1.3 billion. Its net income

percentage and its return on equity are both excellent, indicating that the company is

Beginning of year: $4.4 billion – $2.4 billion

Beginning of year: $4.4 billion ÷ $2.4 billion

End of year: $4.3 billion – $2.2 billion

Return on equity: Net Income/Average Stockholders’ Equity

$1.3 billion ÷ $3.05 billion*

Current ratio: Current Assets/Current Liabilities

End of year: $4.3 billion ÷ $2.2 billion

25 Minutes, Strong

a.

b.

c.

d.

e.

Normally, pending litigation should be disclosed in notes to the financial statements. But a

SOLUTIONS TO CRITICAL THINKING CASES

ADEQUATE DISCLOSURE

CASE 5.1

Mandella Construction Co. should disclose the accounting method that it is using in the

Generally accepted accounting principles do not require disclosure of changes in

The fact that one of the company’s two processing plants will be out of service for at least

No disclosure is required under generally accepted accounting principles, because any

Group assignment:

No time estimate

a.

•

b.

•

c.

An accountant has access to much information about a company’s business

affect a CPA’s objectivity.

During the interview (part b), the accountant probably described the ethical concept of

Accountants, like doctors, develop greater proficiency through specialization. By

Arguments for an accountant serving clients who are direct competitors include:

The principal argument against an accountant serving clients who are direct competitors is:

CASE 5.2

We do not provide comprehensive solutions for group problems. It is the nature of these problems

that solutions should reflect the collective experiences of the group. But the following observations

may be useful in stimulating class discussion:

WORKING FOR THE COMPETITION

ETHICS, FRAUD & CORPORATE GOVERNANCE

serving numerous clients in the same industry, accountants develop greater expertise in

industry problems and accounting practices.

In many cases, it is impractical to define “direct competitors.” Is a video rental business

a direct competitor of a movie theater? A television station? A miniature golf course?

5 Minutes, Easy

The purpose of the personal certification process is to make CEOs and CFOs more accountable

and personally responsible for the contents in the annual reports issued by their companies.

CASE 5.3

CEOs AND CFOs

CERTIFICATIONS BY

15 Minutes, Easy

CASE 5.4

Other Income/(Loss)

Share-Based Employee Compensation

ANNUAL REPORT DISCLOSURES

Listed below are the headings of the major disclosure items presented in Ford’s most recent financial statement footnotes.

Students are to discuss the general nature and content of the various topics. The advanced nature of some of these topics goes

beyond the scope of an introductory course.

Fair Value Measurements

Accumulated Other Comprehensive Income/(Loss)

Summary of Significant Accounting Policies

New Accounting Standards

INTERNET

Capital Stock and Earnings Per Share

Employee Separation Actions and Exit and Disposal Activities

Income Taxes

Redeemable Noncontrolling Interest

Variable Interest Entities

Retirement Benefits

Debt and Commitments

Equity in Net Assets of Affiliated Companies

Net Property and Lease Commitments

Other Liabilities and Deferred Revenue

Commitments and Contingencies

Selected Quarterly Financial Data

Segment Information

Geographic Information

Financial Services Sector Finance Receivables

Net Investment in Operating Leases

Financial Services Sector Allowance for Credit Losses

Changes in Investments in Affiliates