(a), (c) & (e)

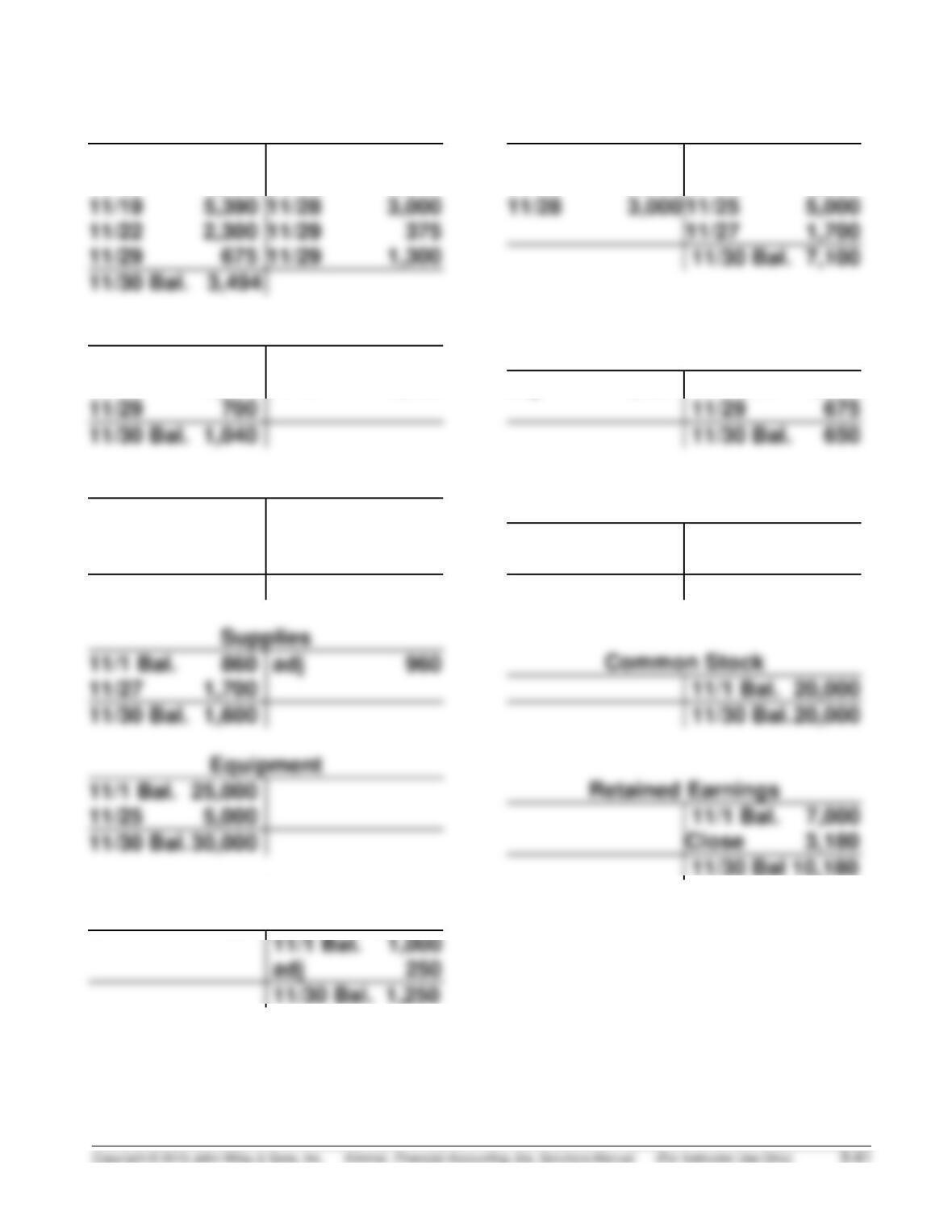

Cash

11/30 Bal. 3,494

11/30 Bal. 7,100

11/1 Bal. 9,000

11/10 1,900

11/8 3,550

11/20 7,546

Accounts Receivable

11/30 Bal. 1,040

11/30 Bal. 650

11/1 Bal. 2,240

11/12 5,500

11/10 1,900

11/19 5,500

Inventory

11/11 8,000

11/12 4,000

11/15 300

11/20 154

11/30 3,546

11/1 Bal. 860

adj 960

11/30 Bal. 1,600

11/1 Bal. 25,000

11/30 Bal. 30,000

11/1 Bal. 20,000

11/30 Bal. 20,000

11/1 Bal. 7,000

Close 3,180

11/30 Bal 10,180

Accumulated Depreciation—

Equipment

11/1 Bal. 1,000

11/30 Bal. 1,250

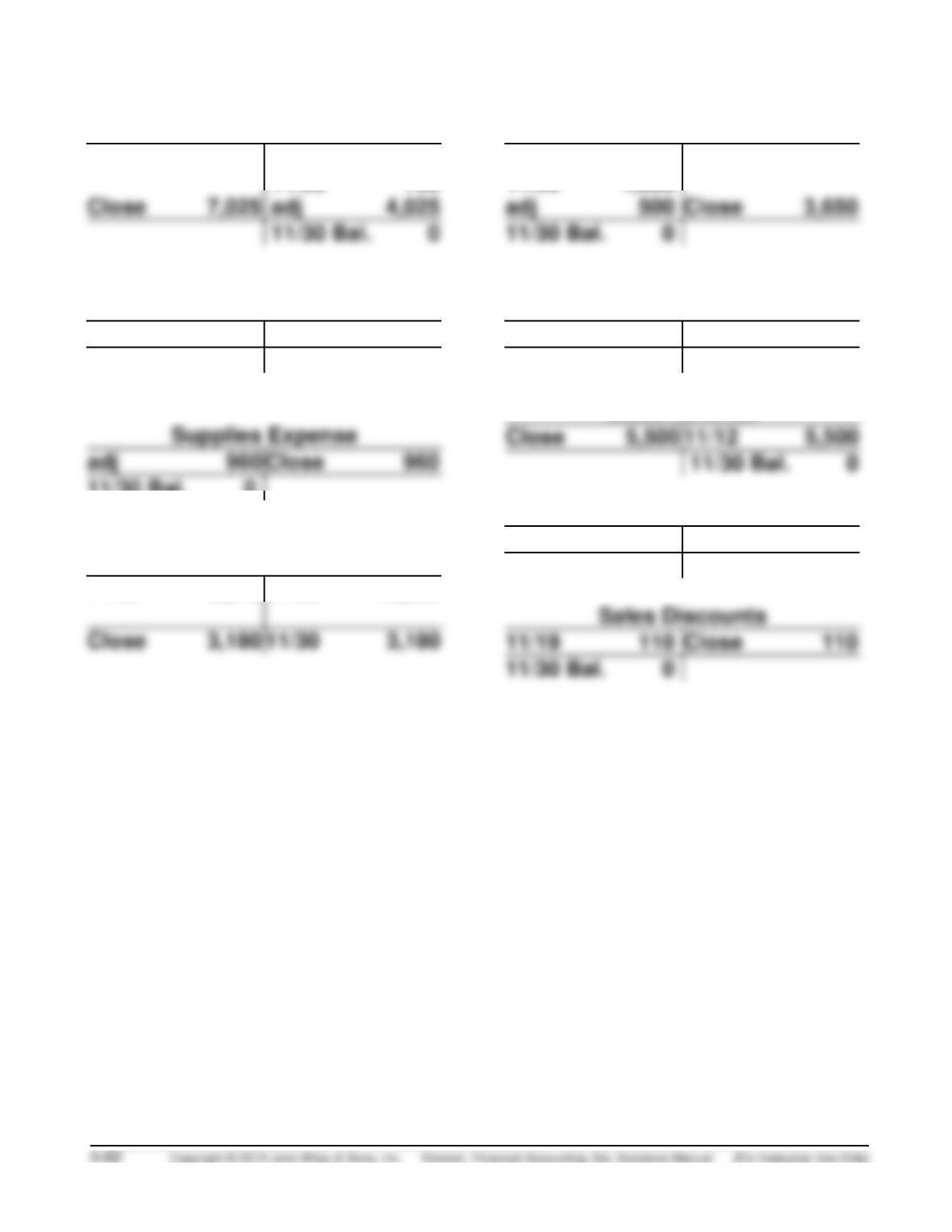

Accounts Payable

11/15 300

11/20 7,700

11/1 Bal. 3,400

11/11 8,000

Unearned

Service Revenue

adj 4,025

11/1 Bal. 4,000

Salaries and Wages Payable

11/8 1,700

11/1 Bal. 1,700

adj 500

11/30 Bal. 500

ACR5-2 (Continued)

Service Revenue

11/30 Bal. 0

11/30 Bal. 0

11/22 2,300

11/29 700

Depreciation Expense

adj 250

Close 250

11/30 Bal. 0

adj 960

Close 960

Close 5,500

11/12 5,500

11/30 Bal. 0

11/30 Bal. 0

Income Summary

11/30 Bal. 0

11/30 9,345

11/30 12,525

Salaries and Wages Expense

11/8 1,850

11/29 1,300

Rent Expense

11/29 375

Close 375

11/30 Bal. 0

Sales Revenue

Cost of Goods Sold

11/12 4,000

Close 4,000

11/30 Bal. 0

ACR 5-2 (Continued)

(d) IKONK, INC.

Adjusted Trial Balance

November 30, 2017

DR.

CR.

Cash ……………………………………………………….

$3,494

Accounts Receivable …………………………………..

1,040

Inventory …………………………………………………….

3,546

Supplies ……………………………………………………..

Equipment ………………………………………………….

Accumulated Depreciation …………………………..

Accounts Payable …………………………..…………..

7,100

Unearned Service Revenue ………………………….

Salaries and Wages Payable ………………………..

Common Stock ……………………………………………

Retained Earnings ………………………………………

7,000

Service Revenue …………………………………………

7,025

Sales Revenue …………………………………………….

5,500

Sales Discounts ………………………………………….

110

Cost of Goods Sold …………………………………….

4,000

Salaries and Wages Expense ………………………

Rent Expense …………………………..…………………

375

Depreciation Expense …………………………………

Supplies Expense ……………………………………….

ACR5-2 (Continued)

(f) IKONK, INC.

Income Statement

For the Month Ended November 30, 2017

Sales

Sales revenue ………………………………………….. ($5,500

Less Sales discounts ……………………………….. 110

Net sales ………………………………………. $5,390

Service revenue ……………………………………….. 7,025

Total revenues …………………………………. 12,415

IKONK, INC.

Retained Earnings Statement

For the Month Ended November 30, 2017

Retained earnings, November 1 ……………………….. $7,000

ACR5-2 (Continued)

IKONK, INC.

Balance Sheet

November 30, 2017

Assets

Current assets

Cash ………………………………………………………. $ 3,494

Accounts receivable ……………………………….. 1,040

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable ………………………………………. $ 7,100

Salaries and wages payable ………………………… 500

CT 5-1 FINANCIAL REPORTING PROBLEM

(a) Percentage change in total revenue:

2013 to 2014 ($182,795 – $170,910) ÷ $170,910 = 7.0%

(b) Profit margin:

2012 $41,733 ÷ $156,508 = 26.7%

(c) Gross profit rates:

2012 $68,662 ÷ $156,508 = 43.9%

2013 $64,304 ÷ $170,910 = 37.6%

CT 5-2 COMPARATIVE ANALYSIS PROBLEM

(a)

Columbia Sportswear

VFC

(1)

Profit margin

$141,859

$2,100,590

= 6.8.%

$1,047,505

$12,282,161

= 8.5%

(2)

(3)

Gross profit rate

(4)

Operating income

(000’s)

$198,844

$1,437,724

(b) VFC’s higher profit margin suggests that it was better at turning sales

dollars into net income. Its gross profit rate suggests that VFC can

command a higher markup on its goods or that it is better at

CT 5-3 COMPARATIVE ANALYSIS PROBLEM

(a)

Amazon.com

Wal-Mart stores

(1)

Profit margin

($241)

$88,988

= (0.3%)

$16, 363 3.4%

$485, 651

=

(2)

Gross profit (millions)

(3)

Gross profit rate

(4)

Operating income

(000’s)

$178

$27,147

(b) Wal-Mart’s higher profit margin suggests that it was better at turning

sales dollars into net income. Amazon’s gross profit rate suggests that

CT 5-4 INTERPRETING FINANCIAL STATEMENTS

(a)

Carrefour

(Euros)

Wal-Mart

(Dollars)

(b)

Profit margin

€1,738 ÷ €70,486 = 2.5%

$9,054 ÷ $256,329 = 3.5%

(c)

Current ratio

€14,521 ÷ €13,660 = 1.06:1

$34,421 ÷ $37,418 = .92:1

Debt to assets ratio

€29,434 ÷ €39,063 = .75

$61,289 ÷ $104,912 = .58

CT 5-4 (Continued)

(d) Ratios improve our ability to compare these two companies that report

financial information using different currencies. However, other factors

can still reduce our ability to compare them. Different accounting stan-

CT 5-5 REAL-WORLD FOCUS

Answers will vary depending on the company and article chosen by the

CT 5-6 DECISION MAKING ACROSS THE ORGANIZATION

(a) (1) GIGASALES DEPARTMENT STORE

Projected Income Statement

For the Year Ended December 31, 2018

Net sales [$700,000 + ($700,000 X 4%)] …. $728,000

Cost of goods sold ($728,000 X 75%)* …… 546,000

Gross profit ($728,000 X 25%)** ……………. 182,000

(2) GIGASALES DEPARTMENT STORE

Projected Income Statement

For the Year Ended December 31, 2018

Net sales ……………………………………………… $700,000

(b) Karen’s proposed changes will increase net income by $42,000. Reece’s

proposed changes will reduce operating expenses by $32,000 and result

in a corresponding increase in net income. Thus, if the choice is between

CT 5-6 (Continued)

(c) GIGASALES DEPARTMENT STORE

Projected Income Statement

For the Year Ended December 31, 2018

Net sales …………………………………………………….. $728,000

Cost of goods sold ……………………………………… 546,000

Gross profit ………………………………………………… 182,000

Operating expenses

(d) A variety of factors might be presented by the student. For example,

increasing the quantity of inventory purchased will increase warehousing

and other costs of inventory. It will also increase the risk of holding

CT 5-7 COMMUNICATION ACTIVITY

(a), (b)

President

Surfing Hawaii Co.

Dear Sir:

As you know, the financial statements for Surfing Hawaii Co. are prepared

in accordance with generally accepted accounting principles. One of these

principles is the revenue recognition principle, which provides that revenues

should be recognized when the performance obligation is satisfied.

The circumstances pertaining to this sale may seem to you to be atypical

because Aiken has ordered a specific kind of surfboard. From an accounting

standpoint, this would be true only if you could not reasonably expect to sell

this surfboard to another customer. In such case, it would be proper under

generally accepted accounting principles to recognize sales revenue when

you have completed the surfboard for Aiken.

CT 5-8 ETHICS CASE

(a) Tabitha Andes, as a new employee, is placed in a position of respon-

sibility and is pressured by her supervisor to continue an unethical

practice previously performed by him. The unethical practice is taking

(b) The stakeholders (affected parties) are:

Tabitha Andes, the assistant treasurer.

Pete Wilson, the treasurer.

Southside Stores, the company.

Creditors of Southside Stores (suppliers).

Mail room employees (those assigned the blame).

(c) Tabitha’s alternatives:

1. Tell the treasurer (her boss) that she will attempt to take every

allowable cash discount by preparing and mailing checks within

the discount period—the ethical thing to do. This will offend her

boss and may jeopardize her continued employment.

3. Go over her boss’s head and take the chance of receiving just and

reasonable treatment from an officer superior to Pete. The

company may not condone this practice. Tabitha definitely has a

choice, but probably not without consequence. To continue the

CT 5-9 ALL ABOUT YOU ACTIVITY

In order for revenue to be recognized the performance obligation must be

CT 5-10 FASB CODIFICATION ACTIVITY

(a) 1. Inventory is the aggregate of those items of tangible personal

property that have any of the following characteristics:

a. Held for sale in the ordinary course of business

b. In process of production for such sale

c. To be currently consumed in the production of goods or services

to be available for sale.

The term inventory embraces goods awaiting sale (the merchandise

of a trading concern and the finished goods of a manufacturer),

goods in the course of production (work in process), and goods to

be consumed directly or indirectly in production (raw materials and

supplies). This definition of inventories excludes long-term assets

subject to depreciation accounting, or goods which, when put into

use, will be so classified. The fact that a depreciable asset is retired

2. A customer is a reseller or a consumer, either an individual or a

business that purchases a vendor’s products or services for end use

rather than for resale. This definition is consistent with paragraph

280-10–50–42, which states that a group of entities known to a report-

ing entity to be under common control shall be considered as a

single customer, and the federal government, a state government, a

CT 5-10 (Continued)

(b) 330–10–35-15 Only in exceptional cases may inventories properly be

stated above cost. For example, precious metals having a fixed

IFRS CONCEPTS AND APPLICATION

IFRS5-1

Expenses may be classified by “nature” or by “function”. The “nature–of–

expense” classification organizes expenses by type of expense, such as

salaries, depreciation, rent, or supplies. The “function–of–expense” classifica–

tion presents expenses by type of business activity. Examples would include

cost of goods sold, selling, administrative, operating, and non-operating.

LO 4 BT: K Difficulty: Easy TOT: 5 min. AACSB: Diversity AICPA FC: Measurement

IFRS5-2

By function

Cost of goods sold

By nature

Depreciation expense

By nature

Salaries and wages expense

By function

Selling expenses

By nature

Utilities expense

By nature

Delivery expense

IFRS5-3

MATILDA COMPANY

Comprehensive Income Statement

For the Year Ended 2017

(in thousands of euros)

Net income …………………………………………………………………….. €150

IFRS5-4 INTERNATIONAL FINANCIAL REPORTING PROBLEM

(a) Vuitton uses a multiple step format. The income statement isolates

gross margin, profit from recurring operations and operating profit

(b) Vuitton uses Cost of Net Financial Debt rather than Interest Expense on

its income statement.

(c) Inventory is composed of:

Wines and eaux-de-vie in process of aging