CHAPTER 5 Accounting Systems

Prob. 5-4B (Continued)

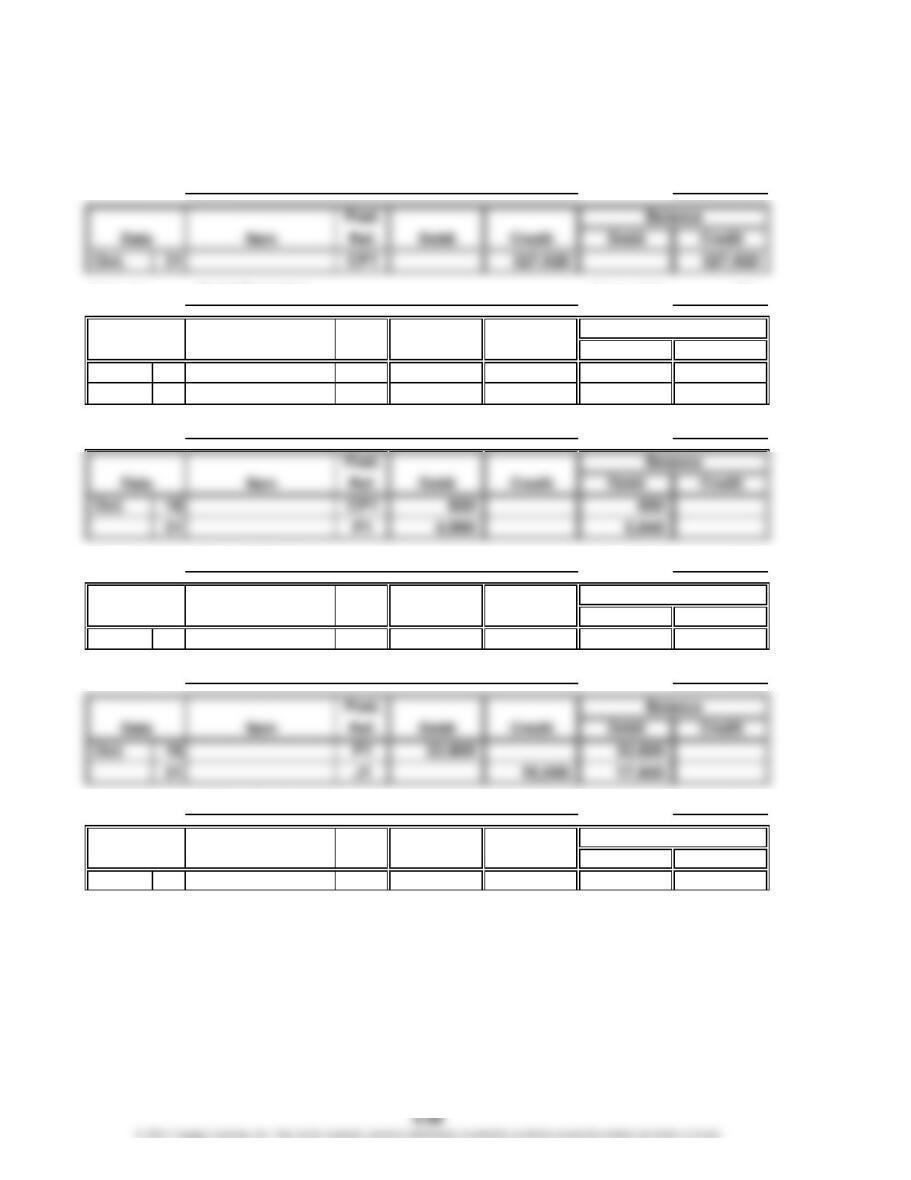

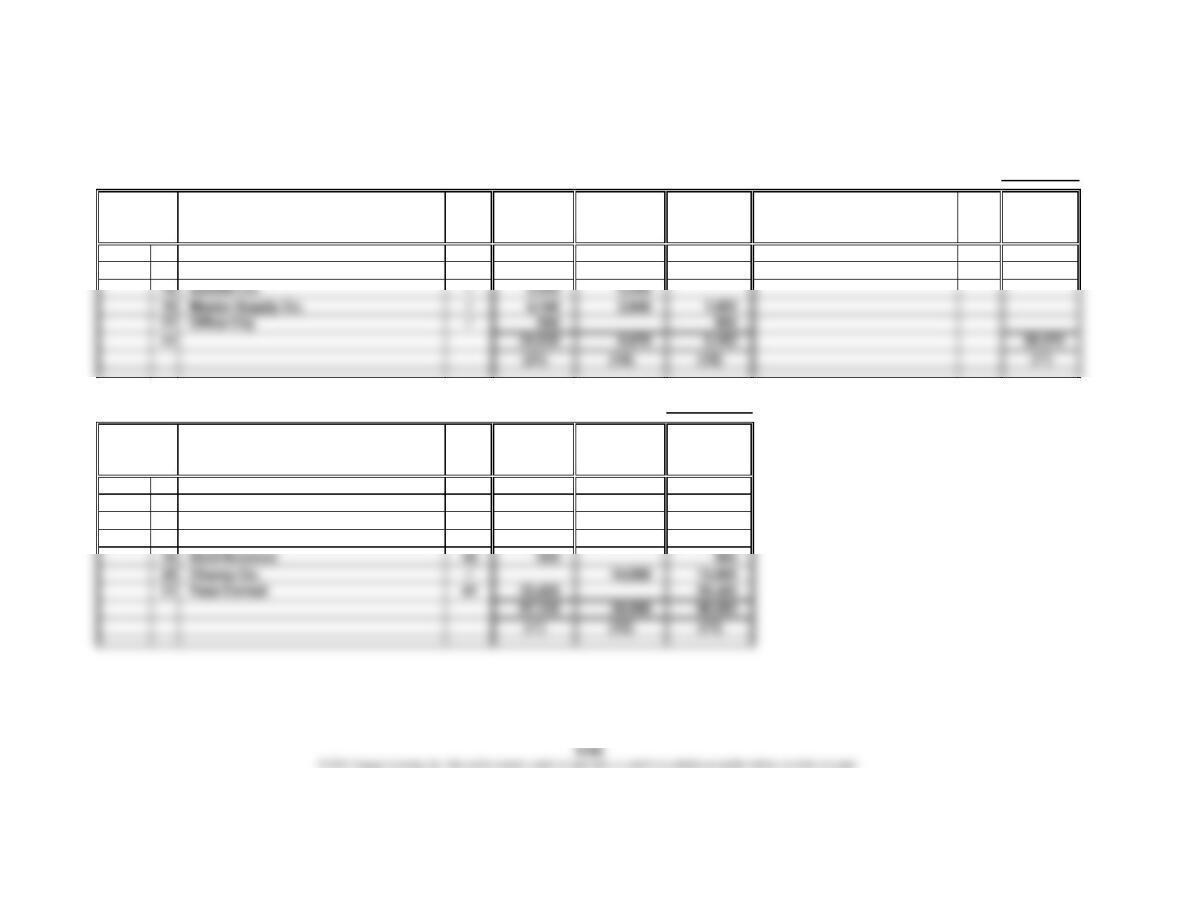

1.

Post.

Item Ref. Debit Credit Balance

Oct. 17 P1 9,780 9,780

26 CP1 9,780 —

30 P1 12,450 12,450

ACCOUNTS PAYABLE SUBSIDIARY LEDGER

Name: Petro Services Inc.

Name: Midland Supply Co.

Date

A-One Office Supply Co.

Name:

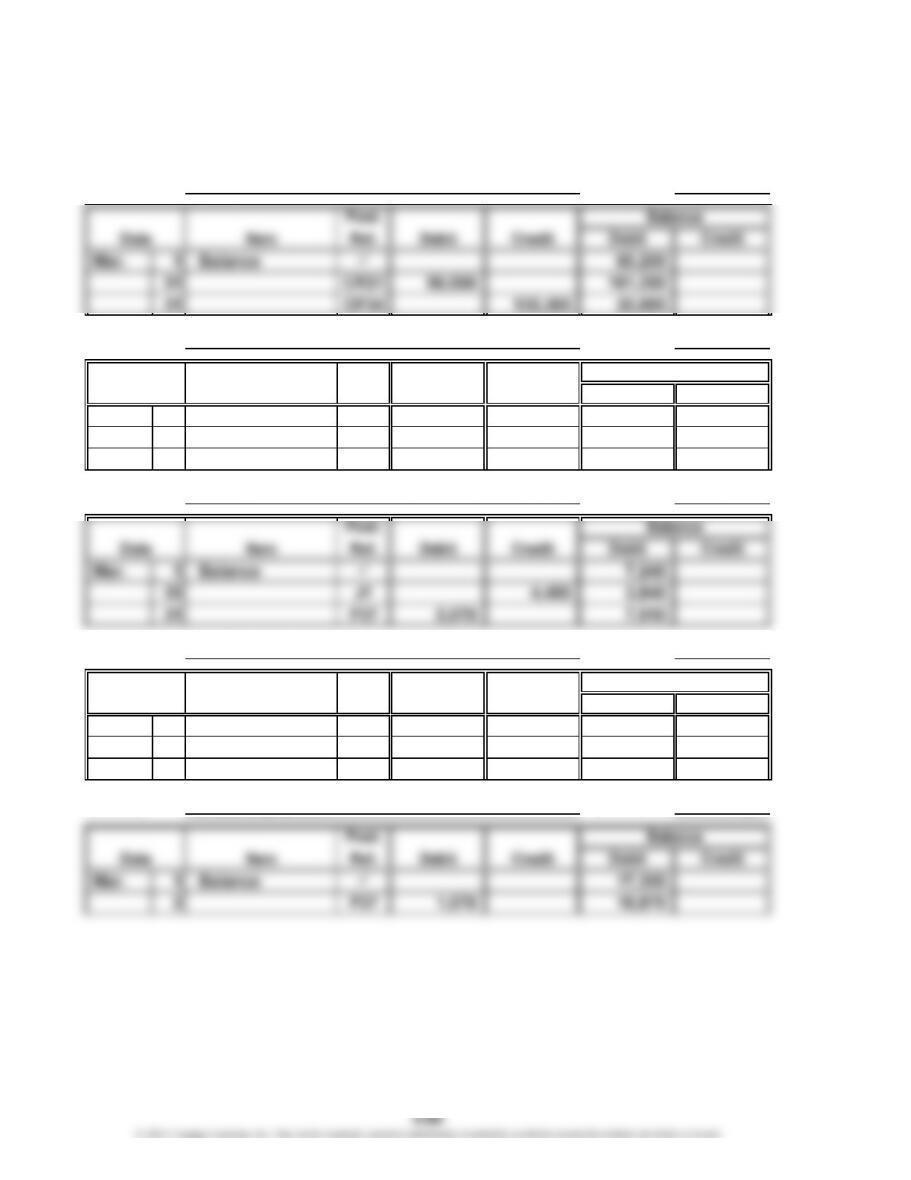

CHAPTER 5 Accounting Systems

Prob. 5-4B (Continued)

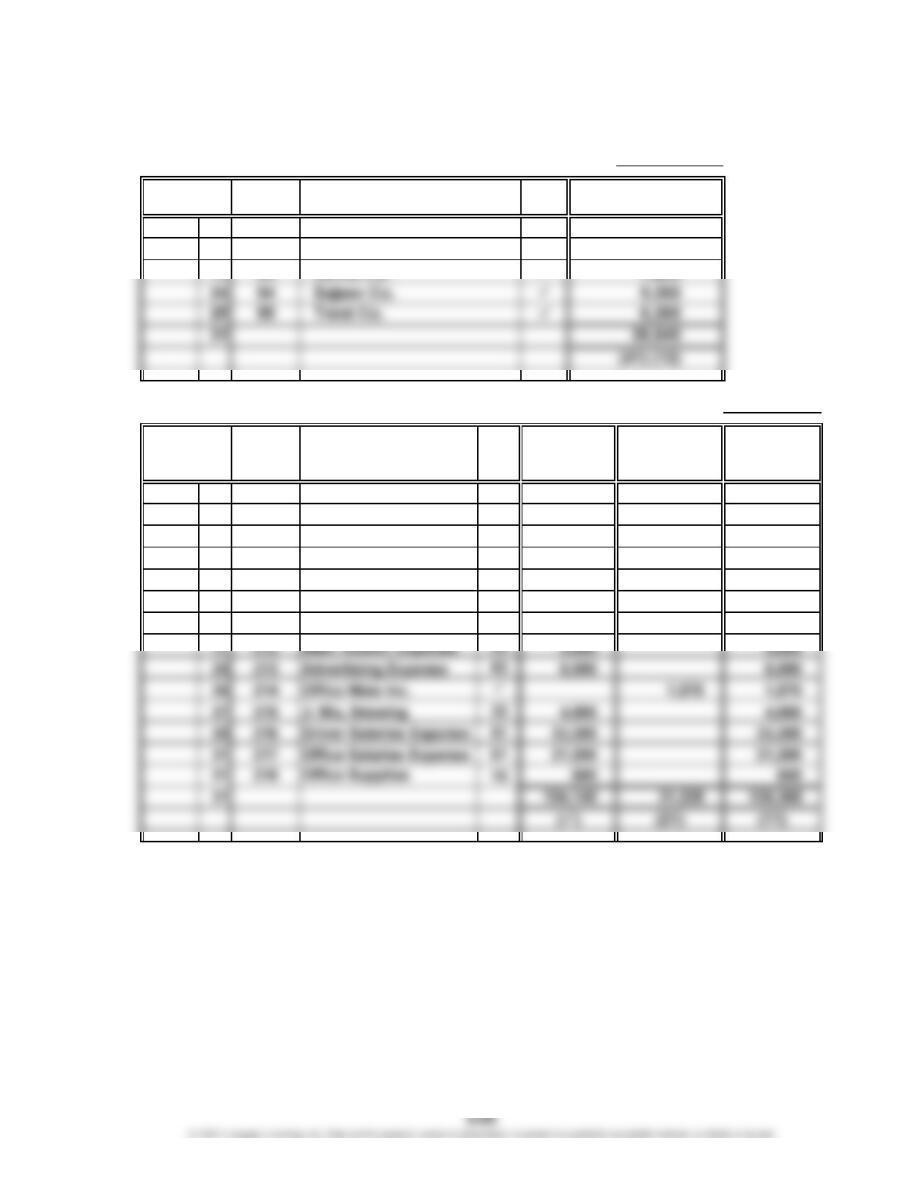

2. and 3.

Account No. 11

Account No. 14

Post.

Item Ref. Debit Credit Debit Credit

18 CP1 4,570 4,570

31 P1 47,530 52,100

Account No. 15

Account No. 16

Post.

Item Ref. Debit Credit Debit Credit

31 J1 15,000 15,000

Account No. 17

Account No. 18

Post.

Item Ref. Debit Credit Debit Credit

31 P1 5,500 5,500

GENERAL LEDGER

Account: Prepaid Rent

Oct.

Account:

Balance

Field Supplies

Account:

Balance

Oct.

Account:

Account: Office Equipment

Balance

Date

Office Supplies

Date

Field Equipment

Account: Cash

Oct.

Date

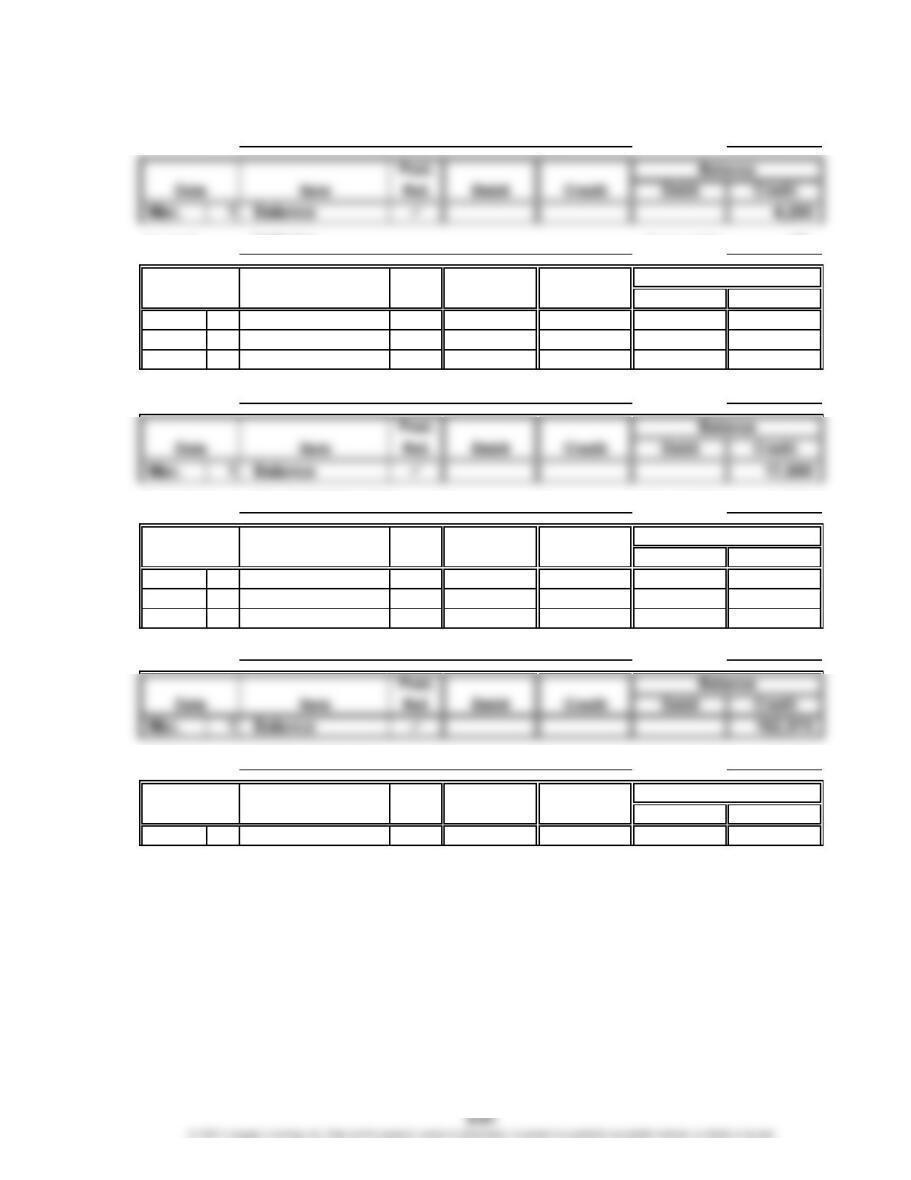

CHAPTER 5 Accounting Systems

Prob. 5-4B (Concluded)

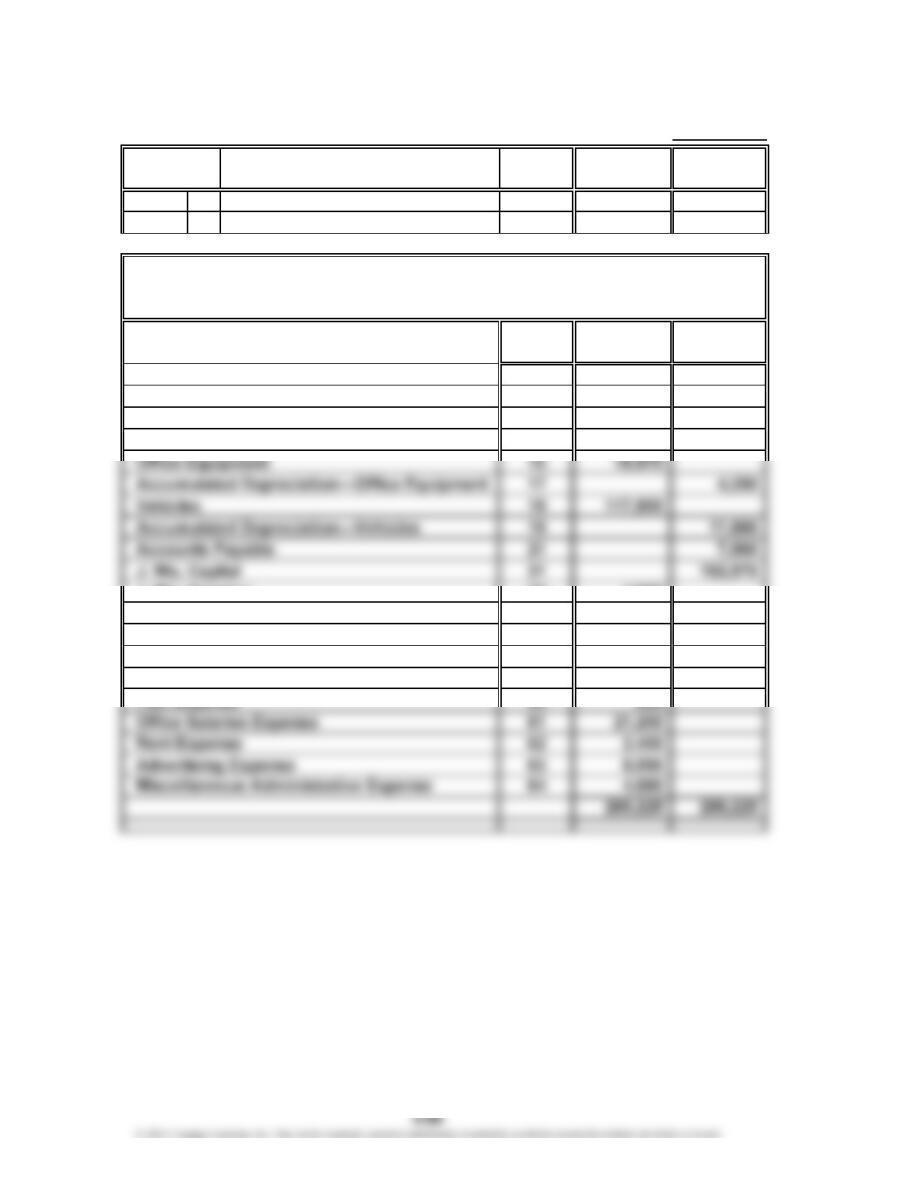

Account No. 19

Account No. 21

Post.

Item Ref. Debit Credit Debit Credit

31 P1 90,620 90,620

31 CP1 43,700 46,920

Account No. 61

Account No. 71

Post.

Item Ref. Debit Credit Debit Credit

16 CP1 7,000 7,000

4.

A-One Office Supply Co. $ 3,670

*The total of the schedule of accounts payable is equal to the balance of the accounts

payable control account.

5. A subsidiary ledger for the field equipment would allow the company to track

each piece of equipment with respect to cost, location, useful life, and other

Account: Land

October 31

Oct.

Balance

Date

Accounts Payable

Accounts Payable Creditor Balances

Account:

West Texas Exploration Co.

Account: Salary Expense

Rent Expense

Account:

Oct.

Balance

Date

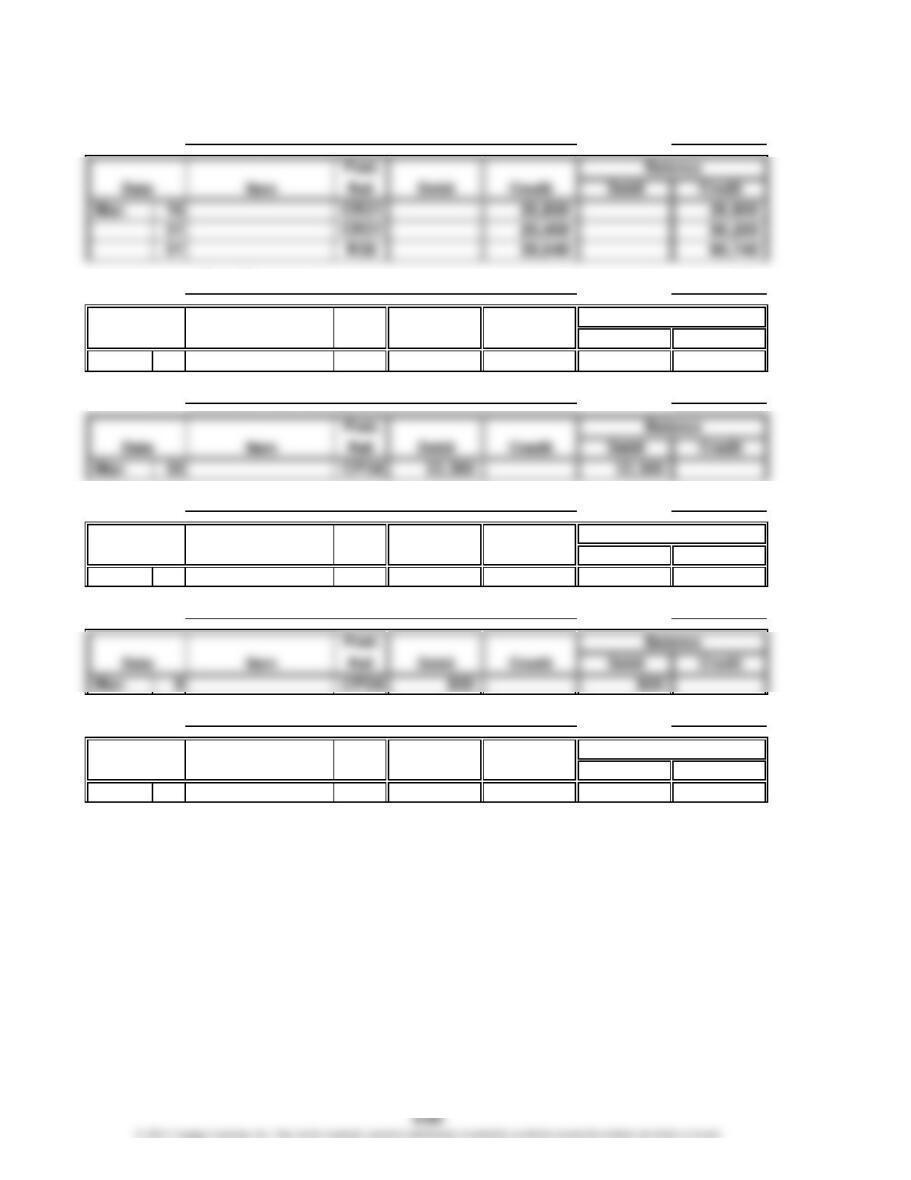

CHAPTER 5 Accounting Systems

Prob. 5-5B

1., 3., and 4.

Account No. 11

Account No. 12

Post.

Item Ref. Debit Credit Debit Credit

1 Balance 31,950

31 R35 39,540 71,490

31 CR31 38,950 32,540

Account No. 14

Account No. 15

Post.

Item Ref. Debit Credit Debit Credit

1 Balance 3,690

31 CP34 600 4,290

31 P37 2,490 6,780

Account No. 16

Maintenance Supplies

GENERAL LEDGER

Balance

Accounts Receivable

Account:

Account: Cash

Account: Office Equipment

Balance

Date

Mar.

Account: Office Supplies

Mar.

Date

Account:

CHAPTER 5 Accounting Systems

Prob. 5-5B (Continued)

Account No. 17

Account No. 18

Post.

Item Ref. Debit Credit Debit Credit

1 Balance 62,400

2 P37 26,900 89,300

16 CP34 28,500 117,800

Account No. 19

Account No. 21

Post.

Item Ref. Debit Credit Debit Credit

1 Balance 2,755

31 P37 36,030 38,785

31 CP34 31,225 7,560

Account No. 31

Account No. 32

Post.

Item Ref. Debit Credit Debit Credit

27 CP34 4,000 4,000 Mar.

Account:

Balance

Date

Balance

Date

Mar.

Account: Accumulated Depreciation—Vehicles

Balance

Account: Accumulated Depreciation—Office Equipment

J. Wu, Drawing

Account: Vehicles

Account: J. Wu, Capital

Mar.

Account: Accounts Payable

Date

CHAPTER 5 Accounting Systems

Prob. 5-5B (Continued)

Account No. 41

Account No. 42

Post.

Item Ref. Debit Credit Debit Credit

18 CR31 900 900

Account No. 51

Account No. 52

Post.

Item Ref. Debit Credit Debit Credit

20 J1 4,400 4,400

Account No. 53

Account No. 61

Post.

Item Ref. Debit Credit Debit Credit

31 CP34 21,200 21,200

Date

Mar.

Account: Fuel Expense

Account: Maintenance Supplies Expense

Balance

Mar.

Balance

Date

Account: Office Salaries Expense

Account: Fees Earned

Account: Driver Salaries Expense

Account: Rent Revenue

Balance

Date

Mar.

CHAPTER 5 Accounting Systems

Prob. 5-5B (Continued)

Account No. 62

Account No. 63

Post.

Item Ref. Debit Credit Debit Credit

20 CP34 8,590 8,590

Account: Advertising Expense

Date

Mar.

Account: Rent Expense

Balance

CHAPTER 5 Accounting Systems

Prob. 5-5B (Continued)

2. and 4.

Page 37

Mar. 2 18 26,900

316 1,570

Page 31

Mar. 6 Chavez Co. 7,950

10 Sajeev Co. 10,000

12 Ellis Co. 7,000

16 Fees Earned 41 26,800

Date

Post.

Ref.

Amount

Maintenance

Supplies

Dr.

Office

Supplies

Dr.

PURCHASES JOURNAL

Date

Post.

Ref.

Accounts

Payable

Cr.

26,900

1,570

McIntyre Sales Co.

Post.

Ref.

Other

Accounts

Dr.

Vehicles

Office Equipment

Account Credited

Office Mate Inc.

Cash

Dr.

CASH RECEIPTS JOURNAL

Account Credited

Other

Accounts

Cr.

Accounts

Receivable

Cr.

7,950

10,000

7,000

26,800

CHAPTER 5 Accounting Systems

Prob. 5-5B (Continued)

2. and 4.

Page 35

5 91 Ellis Co.

7 92 Trent Co.

Page 34

1 205 Rent Expense 62 2,450

9 206 Fuel Expense 53 820

10 207 Office City 450 450

10 208 Bastille Co. 1,890 1,890

11 209 Porter Co. 415 415

13 210 McIntyre Sales Co. 26,900 26,900

16 211 Vehicles 18 28,500

Account Debited

REVENUE JOURNAL

Date

CASH PAYMENTS JOURNAL

Accounts

Payable

Dr.

7,000

Invoice

No.

Account Debited

Cash

Cr.

Other

Accounts

Dr.

9,840

Accounts Rec. Dr.

Fees Earned Cr.

Post.

Ref.

Date

Mar.

Post.

Ref.

Ck.

No.

820

Mar. 2,450

28,500

CHAPTER 5 Accounting Systems

Prob. 5-5B (Concluded)

3. Page 1

Mar. 20 Maintenance Supplies Expense 52 4,400

Maintenance Supplies 14 4,400

5.

Account Debit Credit

No. Balances Balances

Cash 11 25,885

Accounts Receivable 12 32,540

Maintenance Supplies 14 7,910

Office Supplies 15 6,780

J. Wu, Drawing 32 4,000

Fees Earned 41 95,740

Rent Revenue 42 900

Driver Salaries Expense 51 33,300

Maintenance Supplies Expense 52 4,400

JOURNAL

Date Description

Post.

Ref.

March 31

Debit Credit

AM Express Company

Unadjusted Trial Balance

CHAPTER 5 Accounting Systems

CP 5-1

a. The half-price offer is a normal business practice so long as it is not the result of

price collusion with other competitors or is considered “unfair pricing” according

to federal statutes. Many businesses offer low initial services to entice customers

b. Customer “lock-in” can be unethical if it is the result of fixing prices or acquiring

competitors to achieve monopolistic concentration within an industry. However,

in this case, the customer lock-in is a function and nature of the product. Namely,

the data that are created by the product cannot be easily migrated to another

application. Note that Netbooks is not denying the customer ownership of the data;

rather, Netbooks is making it costly to switch. Such lock-in is not considered an

unethical business practice. Indeed, we see such lock-in characteristics in many

●Sony designs video games so that they only work on its PlayStation®

equipment. Therefore, the games are locked in to the consoles. This allows

Sony and its licensees to limit and control competition for games.

●Many manufacturers control replacement parts for equipment by custom-

designing the parts. Customers then become locked in to the original

manufacturer for replacement parts.

CASES & PROJECTS

CHAPTER 5 Accounting Systems

CP 5-2

Note to Instructors: While the list of functions and services can be quite large, the key

services are identified below. The purpose of these services is fairly advanced for

most students. The activity asks for a listing rather than an explanation because most

students have limited experience by which to provide much explanation. Use this case

to demonstrate the scope and basic nature of these application tools.

Selected JDA Supply Chain Management Solutions

●Demand management

●Factory planning and scheduling

●Merchandise operations

●Supplier relationship management

Selected Salesforce.com Customer Relationship Management Solutions

●Provide the sales force with real-time information about all customer contacts

with the firm to improve the effectiveness of the sales call

●Provide real-time forecast estimation and accumulation tools

●Support promotion plans and integrate the plans with forecasting and

CHAPTER 5 Accounting Systems

CP 5-3

To: Senior Management

From: Student

Re: Cloud-based accounting software

A new approach to automating our accounting requirements is now available. It is

called cloud-based accounting using a cloud computing provider. Rather than

purchasing our accounting software and loading it on our own computers, cloud-

based accounting software is rented and resides on the provider’s computers. Our

data, along with the accounting software, stay with the provider. There are several

advantages to this approach.

1. We don’t need to administer the application or data on our own computers.

This becomes the job of the service provider, thus saving us computer system

personnel costs. All we need is a desktop computer and a browser to use the

software.

3. We don’t need to purchase and load software upgrades. All upgrades are

provided on the provider’s server when they are available. Thus, we are always

using the latest version.

are passed between us and our customers and suppliers.

We also need to consider a number of disadvantages.

1. The cost of the software is recurring. Thus, we are trading the recurring costs of

maintaining our system infrastructure for the recurring cost of the service. A

financial analysis should be conducted to determine whether the service is cost-

effective.

2. The Internet can be slow. During busy times, we may experience slow response

times.

MEMORANDUM

CHAPTER 5 Accounting Systems

CP 5-4

Kyle is missing some of the principal benefits of the computerized system. A

computerized system has three primary advantages. First, the computerized system is

more efficient and accurate at transaction processing. In the computerized system,

once the transaction data have been input, the information is simultaneously recorded

in the electronic journal (file) and posted to the ledger accounts. This saves a significant

amount of time in recording and posting transactions. Second, the computerized

environment is less prone to mathematical, posting, and recording errors. The computer

CP 5-5

a. The accounts receivable and accounts payable accounts consist of transactions

with individual customers and creditors (suppliers). In both cases, the subsidiary

ledger tracks what is collectible from customers or owed to suppliers. Thus, the

subsidiary ledger is required for tracking the collection and payment process to

CHAPTER 5 Accounting Systems

CP 5-6

1. Special journals are used to reduce the processing time and expense to record

transactions. A special journal is usually created when a specific type of

transaction occurs frequently enough so that the use of the traditional two-

column journal becomes cumbersome. The frequency of transactions for Omni

Care would probably justify the following special journals:

Purchases journal

Cash payments journal

CHAPTER 5 Accounting Systems

2.

Page 1

Page 1

Other

Accounts

Dr.

Accounts

Payable

Cr.

Post.

Ref.

Amount

Medical

Supplies

Dr.

Office

Supplies

Dr.

PURCHASES JOURNAL

Date

Post.

Ref.

REVENUE JOURNAL

Account Credited