145

CHAPTER 5

INTERNAL CONTROL AND CASH

CLASS DISCUSSION QUESTIONS

1. a. Congress passed the Sarbanes-

Oxley Act because of the Enron,

WorldCom, Tyco, Adelphia, and oth-

er financial scandals that caused

stockholders, creditors, and other in-

to as publicly held companies.

2. Internal control is broadly defined as the

procedures and processes used by a

company to safeguard its assets, process

information accurately, and ensure

compliance with laws and regulations.

3. a. The five elements of internal control

are the control environment, risk

assessment, control procedures,

monitoring, and information and

communication. The control envi-

goals will be achieved. Monitoring is

the evaluation of the internal control

system. Information and communi-

cation provide management with

feedback about internal control.

b. No. All five elements are necessary

for effective internal control and are

equally important.

procedures. Also, rotation helps to disclose any

irregularities that may occur.

5. Authorizing complete control over a sequence of

related operations by one individual presents

opportunities for inefficiency, errors, and fraud.

should not be responsible for handling cash re-

ceipts (operations) and maintaining the accounts

receivable records (accounting).

7. No. Combining the responsibility for related op-

erations, such as the functions of purchasing,

receiving, and storing of supplies, increases the

possibility of errors and fraud. The responsibilities

for operations, custody of assets, and accounting

should be separated. In this way, the accounting

records serve as an independent check on the

operating managers and the employees who

records should be separated from the responsi-

bility for operations so that the accounting rec-

ords can serve as an independent check on

operations.

10. Controls that could have prevented or detected

the fraud include: (1) requiring supporting docu-

mentation, such as receiving reports and pur-

chase orders of all payments, (2) requiring

146

11. The three documents supporting the

liability are vendor’s invoice, purchase

order, and receiving report. The invoice

should be compared with the receiving

report to determine that the items billed

have been received and with the pur-

chase order to verify quantities, prices,

and terms.

13. The Cash balance and the bank state-

ment balance are likely to differ because

of (1) a delay by the bank or company in

recording transactions (e.g., outstanding

checks, deposits in transit, bank fees,

etc.) and (2) errors by the bank or com-

pany in recording transactions.

according to the bank statement. Once identified,

any errors can be corrected.

15. They represent (a) additions made by the bank to

the company’s balance. This is because on the

bank’s records the company’s account represents

a liability. A credit memorandum increases the

company’s account on the bank’s records.

payments, (3) requiring support (receipts) for

payments from the fund, and (4) periodic

review of the funds on hand and the pay-

ments by an independent person.

17. a. Cash and cash equivalents are usually re-

ported as one amount in the Current Assets

section of the balance sheet.

147

EXERCISES

E5–1

Section 404 requires management’s internal control report to do the following:

(1) state the responsibility of management for establishing and maintaining

an adequate internal control structure and procedures for financial report-

ing; and

The complete AICPA summary of Section 404 of Sarbanes-Oxley is as follows:

Section 404: Management Assessment of Internal Controls.

Requires each annual report of an issuer to contain an “internal control re-

port,” which shall:

(1) state the responsibility of management for establishing and maintaining

an adequate internal control structure and procedures for financial report-

The language in the report of the Committee which accompanies the bill to

explain the legislative intent states, “. . . the Committee does not intend that

the auditor’s evaluation be the subject of a separate engagement or the basis

for increased charges or fees.”

148

E5–2

a. Agree. Jittery has made one employee responsible for the cash drawer in ac-

cordance with the internal control principle of assignment of responsibility. In

addition, Jittery has segregated the operations (preparing the orders) from

the accounting (taking orders and payments).

E5–3

a. The sales clerks could steal money by writing phony refunds and pocketing

the cash supposedly refunded to these fictitious customers.

b. Honeybee Hippie suffers from inadequate separation of responsibilities for

related operations since the clerks issue refunds and restock all merchan-

dise. In addition, there is a lack of proofs and security measures since the

supervisors authorize returns two hours after they are issued.

149

E5–3, Concluded

A disadvantage of issuing a store credit for returns without a receipt is that

preholiday sales might drop as gift-givers realize the return policy has been

tightened. After the holidays, customers wishing to return items for cash re-

funds may be frustrated when they learn the store policy has changed. The ill

will may reduce future sales. It may take longer to explain the new policy and

fill out the paperwork for a store credit, lengthening lines at the return counter

after the holidays. Sales clerks will need to be trained to apply the new policy

and write up a store credit. Sales clerks will also need to be trained to handle

the redemption of the store credit on future merchandise purchases.

E5–4

As an internal auditor, you would probably disagree with the change in policy.

One way to help minimize the risks associated with potential loan defaults is to

carefully evaluate loan applications. Large loans present a greater risk in the

event of default than do smaller loans. Thus, it is reasonable to have more than

one person involved in making the decision to grant a large loan. In addition,

150

E5–5

The trading losses show how small lapses in internal control can have large con-

sequences. When the losses became so large they could no longer be hidden, it

was too late. The loss could have been avoided with a number of internal con-

trols. First, the separation of duties control was overcome by the trader’s intimate

knowledge of the monitoring software. This knowledge of the monitoring system

allowed the trader to effectively hide trades. The design of the monitoring soft-

E5–6

This is an example of a fraud with significant collusion. Frauds that are perpetrat-

ed with multiple parties in different positions of control make detecting fraud

more difficult. In this case, the fraud began with an employee responsible for au-

thorizing claim payments. This is a sensitive position because his decisions

would initiate payments. However, claims would need to be authorized and veri-

fied before payment would be made. Knowing this, the employee made sure each

claim had a phony “victim.” Thus, there was a verifiable story behind each claim.

151

E5–7

Awesome Sound Inc. should not have relied on the unusual nature of the vendors

and delivery frequency to uncover this fraud. The purchase and payment cycle is

one of the most critical business cycles to control because the potential for

abuse is so great. Purchases should be initiated by a requisition document. This

document should be countersigned by an upper-level manager so two people agree

as to what is being purchased. The requisition should initiate a purchase order to

a vendor for goods or services. The vendor responds to the purchase order by

delivering the goods. The goods should be formally received using a receiving

E5–8

a. The most difficult frauds to detect are those that involve a company’s senior

management in a conspiracy to commit the fraud. The senior managers have

the power to access many parts of the accounting system, while the normal

separation of duties is being subverted by involving many people in the fraud.

In addition, the authorization control is subverted because most of the

authorization power resides with the senior management.

152

E5–9

a. The sales clerks should not have access to the cash register tapes.

b. The cash register tapes should be locked in the cash register and the key

retained by the cashier. An employee of the cashier’s office should remove the

cash register tape, record the total on the memo form, and note discrepancies.

E5–10

Mamma’s Burgers suffers from a failure to separate responsibilities for related

operations.

Mamma’s Burgers could stop this theft by limiting the drive-through clerk to taking

customer orders, entering them on the cash register, accepting the customers’

payments, returning customers’ change, and handing customers their orders that

another employee has assembled. By making another employee responsible for

assembling orders, the drive-through clerk must enter the orders on the cash reg-

ister. This will produce a printed receipt or an entry on a computer screen at the

food bin area, specifying the items that must be assembled to fill each order. Once

E5–11

a. The remittance advices should not be sent to the cashier.

E5–12

a. $3,625

153

d. The reason(s) for the differences should be investigated. As a result of the in-

vestigation, action should be taken. For example, if the cashier has not been

trained in how to account for cash receipts, the cashier should receive addi-

tional training.

E5–13

a. $9,380

b. $9,300

c. The cash overage of $80 should be recorded as Cash Short and Over.

E5–14

The use of the voucher system is appropriate, the essentials of which are out-

lined below. (Although invoices could be used instead of vouchers, the latter

more satisfactorily provide for account distribution, signatures, and other signifi-

cant data.)

2. The file for unpaid vouchers should be composed of 31 compartments, one

for each day of the month. Each voucher should be filed in the compartment

representing the last day of the discount period or the due date if the invoice

is not subject to a cash discount.

3. Each day, the vouchers should be removed from the appropriate section of

the file and checks issued by the disbursing official. If the bank balance is

insufficient to pay all of the vouchers, those that remain unpaid should be

refiled according to the date when payment should next be considered.

154

E5–15

To prevent the fraud scheme described, Torpedo must separate responsibilities

for related operations. As in the past, all service requisitions should be submitted

to the Purchasing Department. After receiving the service request, Purchasing

should complete a Service Verification form, stating what service has been or-

dered and the name of the company that will provide the service. This form

should be delivered via intracompany mail to the person responsible for verifying

E5–16

a. Additions to the balance per bank: (3), (5)

b. Deductions from the balance per bank: (6)

E5–17

(1), (2), (4), (7)

The preceding additions to and deductions from the cash balance according to

the company’s records require entries in the company’s records. Additions to

155

E5–18

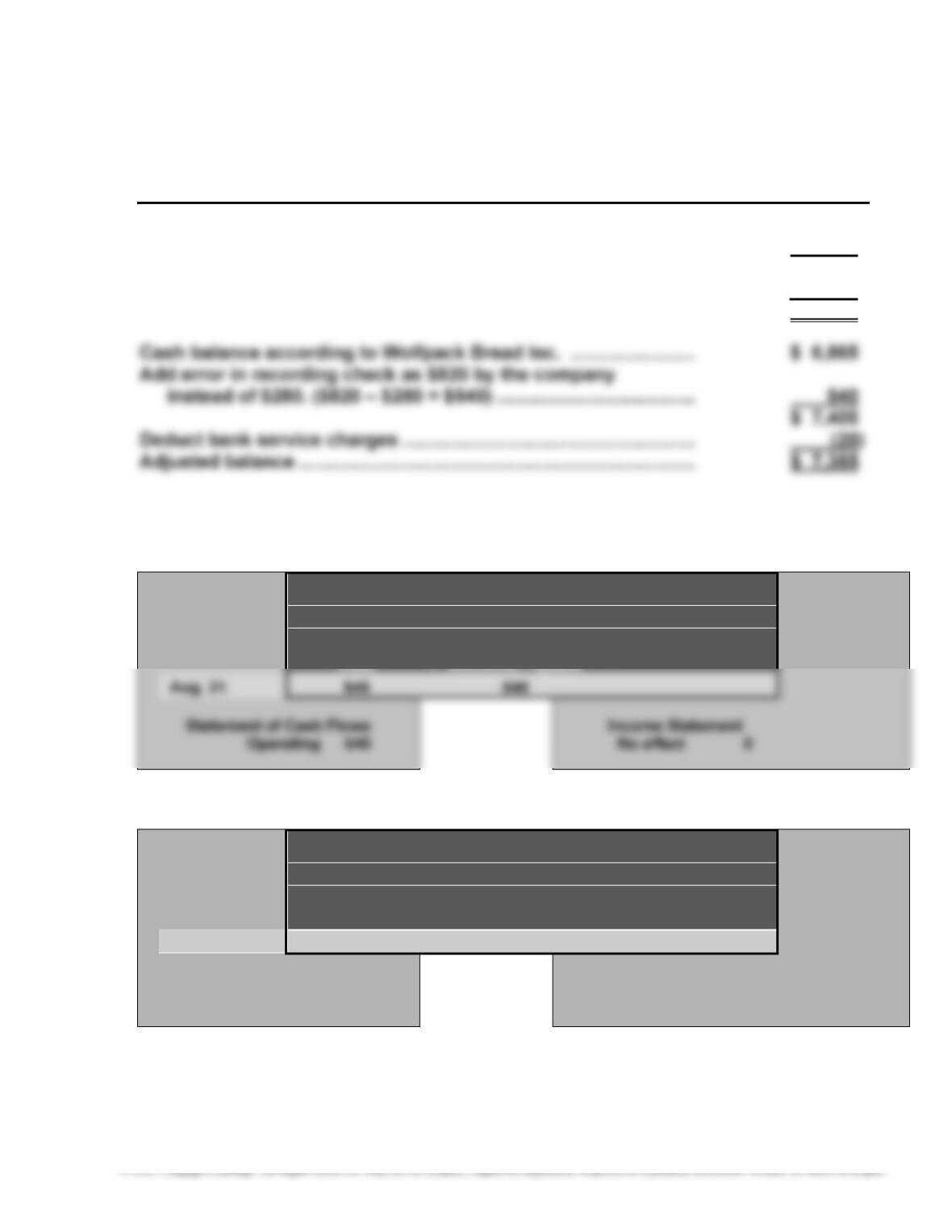

WOLFPACK BREAD INC.

Bank Reconciliation

August 31, 20Y9

Cash balance according to bank statement …………………………… $ 9,165

Add deposit in transit, not recorded by bank …………………………. 1,075

$10,240

Deduct outstanding checks ………………………………………………….. (2,855)

Adjusted balance …………………………………………………………………. $ 7,385

E5–19

Increase in Cash

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

g

Decrease in Cash

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

Retained

Cash = Earnings

Aug. 31. (20) (20)

Statement of Cash Flows Income Statement

Operatin

g

(

20

)

Misc. expense

(

20

)

156

E5–20

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

Notes Retained

E5–21

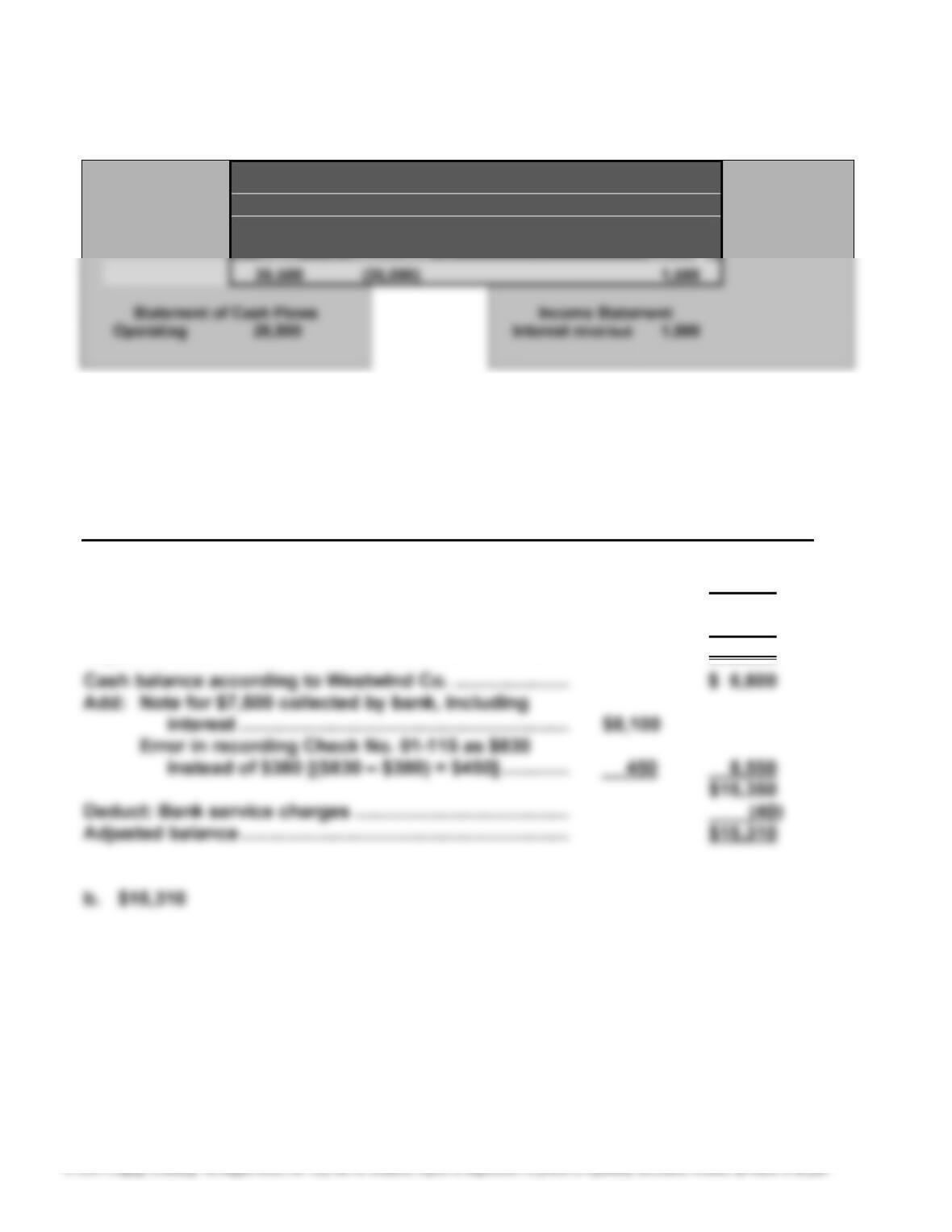

a.

WESTWIND CO.

Bank Reconciliation

August 31, 20Y6

Cash balance according to bank statement ……………….. $17,325

Add: Deposit in transit on August 31 …………………………. 2,175

$19,500

Deduct: Outstanding checks …………………………………….. (4,190)

Adjusted balance ……………………………………………………… $15,310

157

E5–22

a. 1. The heading should be June 30, 20Y3, and not For the Month Ended June

30, 20Y3.

2. The outstanding checks should be deducted from the balance per bank.

b. A correct bank reconciliation would be as follows:

DAKOTA CO.

Bank Reconciliation

June 30, 20Y3

Cash balance according to bank statement $ 22,900

Add deposit of June 30, not recorded by bank 6,200

$29,100

Deduct outstanding checks:

No. 7715 ……………………………………………. $1,450

7760 ……………………………………………. 915

7764 ……………………………………………. 1,850

7765 ……………………………………………. 775 (4,990)

Adjusted balance ………………………………………. $ 24,110

Cash balance according to Dakota Co. ………. $15,625

158

E5–23

a. The amount of cash receipts stolen by the sales clerk can be determined by

attempting to reconcile the bank account. The bank reconciliation will not

reconcile by the amount of cash receipts stolen. The amount stolen by the

sales clerk is $7,125, determined as shown below.

PALA CO.

Bank Reconciliation

April 30, 20Y1

Cash balance according to bank statement …………………………………… $28,175

Deduct: Outstanding checks ………………………………………………………… (12,100)

Adjusted balance …………………………………………………………………………. $16,075

b. The theft of the cash receipts might have been prevented by having more

than one person make the daily deposit. Collusion between two individuals

would then have been necessary to steal cash receipts. In addition, two

employees making the daily cash deposits would tend to discourage theft of

the cash receipts from the employees on the way to the bank.

159

E5–24

a.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Petty

(

)

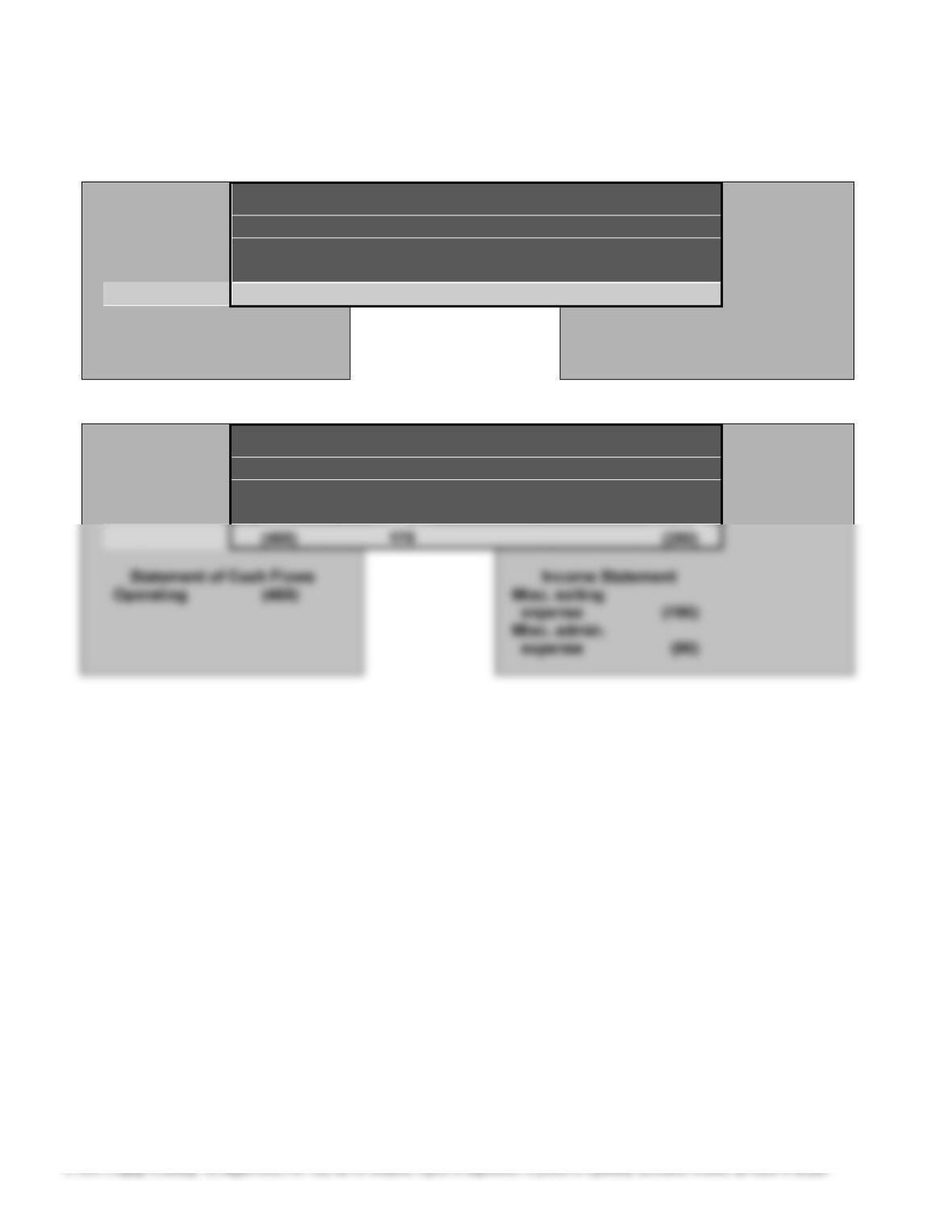

b.

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

Office Retained

Cash + Supplies = Earnings

(610) 325 (285)

Statement of Cash Flows Income Statement

Operating (610) Misc. selling

expense

(

200

)

Misc. admin.

expense

(

85

)

160

E5–25

a.

Balance Sheet

Assets = Liabilities + Stockholders’ Equit

y

Petty

Cash + Cash

(

500

)

500

Statement of Cash Flows Income Statement

No effect 0 No effect 0

b.

Balance Sheet

Assets = Liabilities + Stockholders’ Equity

Office Retained

(

)

(

)